VA Loan Limits for 2026

KEY TAKEAWAYS

- Since 2020, eligible borrowers who have full entitlement are not subject to loan limits.

- For borrowers with partial entitlement, VA loan limits vary based on the county you’re buying a home in. As of 2026, the standard VA loan limit in most parts of the country is $832,750.

- Limits placed on a VA loan by the VA do not reflect limits placed by individual mortgage lenders, only the maximum amount the VA will guarantee to the lender in the event of a default.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformBefore using the VA mortgage program, borrowers should understand what VA loan limits are and how they work. While VA loan limits no longer apply to borrowers with full entitlement, they are still relevant for those with partial entitlement.

Buying a house can be both an exciting and a stressful experience. For most home buyers, the process of securing funding for their dream home is one of the more stressful parts of the experience. For active-duty military members, reservists, veterans, and eligible surviving spouses, the U.S. Department of Veterans Affairs provides backing on mortgages in the form of a guarantee to pay the lender in the event of a default. For those military borrowers, having the backing of the VA can help alleviate some of the stress associated with seeking a mortgage.

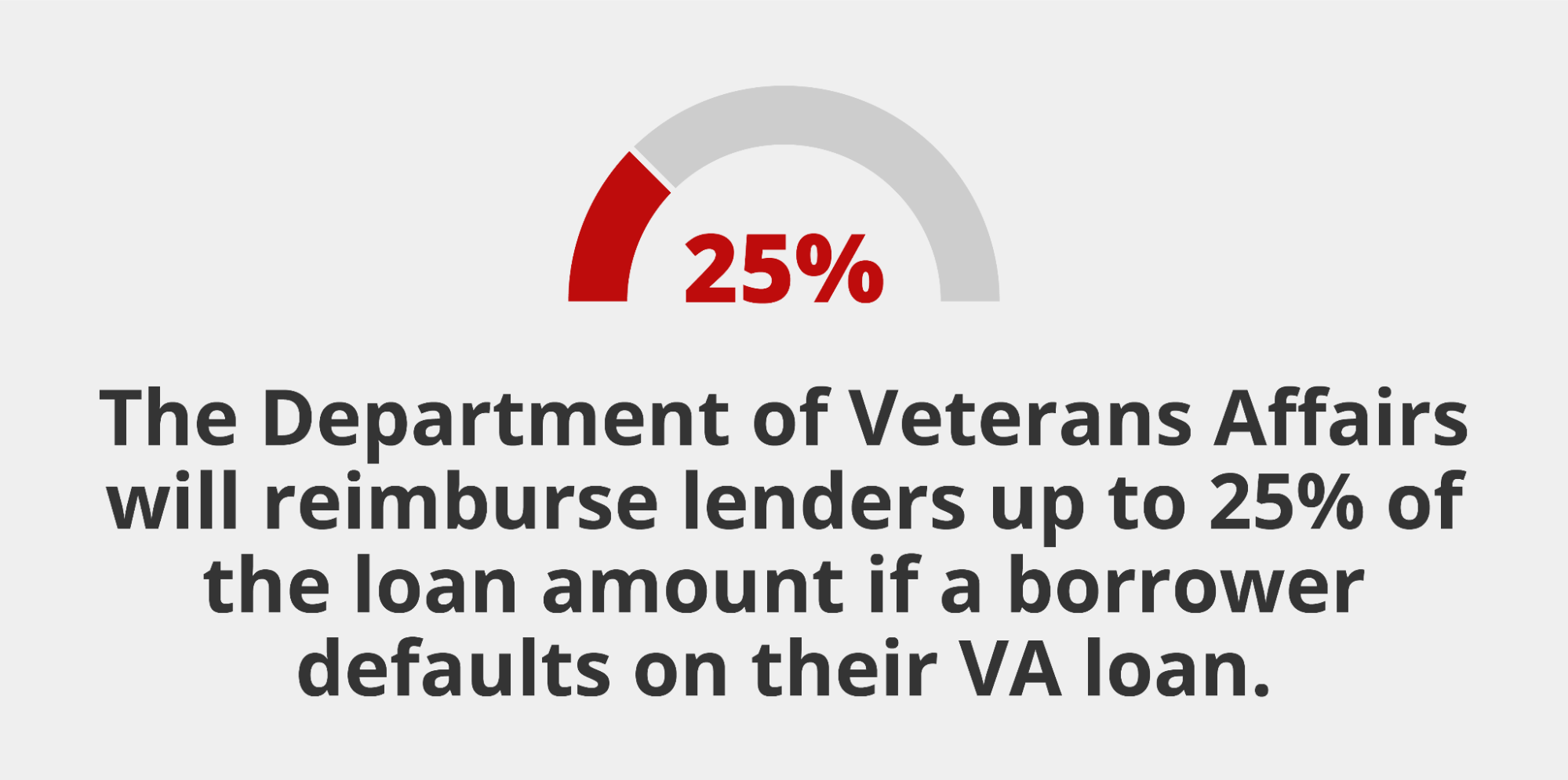

The VA guarantees up to 25% of the loan amount and, in most situations, eligible borrowers will not be limited in how much they can borrow without the need for a down payment. However, there are situations that can limit the eligible backing. Although some of the restrictions have been reduced in recent years, it is still important to understand what VA loan limits are and how they can impact the loan amount you’re eligible for.

Below, we take a look at the factors that can limit VA backing on a mortgage loan, while exploring the options we provide to help eligible military borrowers take full advantage of their VA loan benefits.

KEY TAKEAWAYS

- Since 2020, eligible borrowers who have full entitlement are not subject to loan limits.

- For borrowers with partial entitlement, VA loan limits vary based on the county you’re buying a home in. As of 2026, the standard VA loan limit in most parts of the country is $832,750.

- Limits placed on a VA loan by the VA do not reflect limits placed by individual mortgage lenders, only the maximum amount the VA will guarantee to the lender in the event of a default.

What Are VA Loan Limits?

VA home loan limits specify the maximum amount an eligible borrower can take out for a VA-backed loan without the need for a down payment. However, following the Blue Water Navy Vietnam Veterans Act of 2019, there have been no limits to VA loans for borrowers with full entitlement.

This means that since 2020, eligible active service members, reservists, veterans, and surviving spouses who have full entitlement have been able to purchase a house at any price with their loan backed by the U.S. Department of Veterans Affairs. For those borrowers who do not have full entitlement, limits remain in place. Those VA loan limits vary from year to year and can change based on current housing prices in the county where the home is located.

The limit on VA loans does not reflect the amount a borrower is eligible to take out for a mortgage, which is something that will be decided by the mortgage lender, and will be determined by certain other factors such as income and VA loan rates. While those taking out VA loans will have some flexibility when it comes to things like their credit score and DTI ratio, they will still need to meet minimum requirements in order to qualify for financing.

By working closely with a qualified VA lender like Griffin Funding, you can determine whether you’re eligible for a VA loan, compare VA loan options, and take part in a streamlined VA loan application process.

How Entitlement Affects VA Loan Limits

A borrower’s VA entitlement is the amount that the VA will pay to the lender in the event the borrower defaults. Many VA loan applicants will have their full entitlement, especially first-time home buyers. Specifically, so long as at least one of the following criteria are met by the borrower, they will have full entitlement for a VA mortgage loan:

- They have never used their VA home benefit.

- Any prior VA loan has been paid off and the home has been sold.

- Any previous VA loan foreclosure has been paid off.

For any eligible buyer who does not meet one of the above criteria, there are limits placed on the amount the VA will back on a mortgage. However, borrowers may still be eligible for partial entitlement, specifically if they meet one of the following:

- They are still paying back an active VA loan.

- A prior VA loan has been paid off but they still own the home.

- They have refinanced a VA loan into a non-VA loan and still own the home.

- They made a short-sale on a previous VA loan without paying the VA back in full.

- They entered into a deed in lieu of foreclosure on a previous VA loan.

- They have a previous VA loan foreclosure that has not been fully paid back.

Eligible VA buyers who meet one of the above criteria will be limited to some portion of the full entitlement based on their particular situation. That remaining entitlement can be used to cover the full purchase price of a home or combined with a down payment that makes up the difference between the purchase price and the entitlement. Understanding how much entitlement you have can help you determine whether you’re subject to VA loan limits and whether you need to make a down payment on a home.

VA Loan Limits in 2026

In 2026, the VA loan limit is $832,750 for most VA loans made to borrowers with partial entitlement. For those borrowers in higher-priced counties, the VA loan limits in 2026 are as high as $1,249,125 for a single-family home.

Additionally, the following areas have a baseline VA loan limit of $1,249,125 for single-unit properties:

- Alaska

- Hawaii

- Guam

- U.S. Virgin Islands

Note that these VA loan limits are determined by the VA and do not necessarily reflect the limits placed by the mortgage broker from which the loan is obtained. For any borrower that is limited in their VA backing eligibility, any home costs above the limit will need to be covered using a down payment. This means that there is no limit on how much a home can cost, just that any discrepancy between the VA loan maximum limit and the actual cost of the home will result in the borrower needing to make a down payment.

VA Loan Limit Example

To provide a quick illustration of how VA loan limits work in practice, here’s an example. Let’s say that you’re eligible for a VA loan and are currently using $40,000 of your entitlement. Meanwhile, the county you’re looking to buy in has a VA loan limit of $832,750.

Since the VA guarantees up to 25% of the loan limit in a given county, the max VA entitlement in this county would be $201,625. The next step would be deducting the entitlement you’re currently using from this maximum entitlement:

$201,625 – $40,000 = $161,625 in remaining entitlement

Now we multiply your remaining entitlement by four in order to get the max VA loan amount you can qualify for without needing a down payment:

$161,625 x 4 = $646,500 is max loan amount with no down payment

In this example, if you wanted to buy a home that costs more than $646,500, you would need to cover the difference between this max loan amount and the purchase price with a down payment.

Remember that if you have your full VA entitlement, none of the above will apply. Those with full entitlement are not subject to VA loan limits and will not be required to make a down payment, even if the price of the home they’re buying exceeds their county’s VA loan limits.

March 2026 Update

VA Loan Rates Are Near Multi-Year Lows — and With Full Entitlement, These Limits Don’t Apply to You

VA loan interest rates are currently averaging in the mid-5% range as of early March 2026 — down significantly from the 7%+ range seen throughout much of 2024. And if you have full entitlement, the loan limits on this page don’t apply to you at all — you can purchase a home at any price with no down payment required. Griffin Funding is a VA-approved direct lender with automatic VA loan approval authority, meaning we underwrite and approve your loan in-house with no third-party delays. Check today’s VA loan rates →

Not sure whether you have full or partial entitlement? Our VA loan specialists can review your Certificate of Eligibility and walk you through exactly what you can borrow — at no cost and no obligation. We’ve proudly partnered with Shelter to Soldier since 2014, donating $100 to the organization in every borrower’s name at closing. Talk to a VA loan specialist → Rates are subject to change daily based on market conditions.

What Is the Maximum VA Loan Amount?

The maximum VA loan amount available depends on whether the borrower has full or partial entitlement and the county in which the home is located.

For borrowers with full entitlement, there is no limit to the amount the VA will back — meaning you can finance a home at any price without a down payment requirement from the VA. However, you’ll still need to work with your lender to determine how much financing they’re willing to provide based on your income, credit, and other qualifying factors.

For borrowers with partial entitlement, the maximum amount the VA will guarantee is $832,750 for most U.S. counties. In high-cost counties, that limit rises to $1,249,125. Borrowers should check with the VA or their mortgage lender to determine whether the home they wish to purchase is located in a high-cost county.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Apply for a VA Loan Through Griffin Funding

When it comes time to apply for your first VA loan, Griffin Funding has the experience to help you through the process. We can help you determine the value of homes in your area and evaluate if you live in a high-cost county. With that information, we can look at your available entitlement and explore options for restoring your entitlement if necessary. We’ll also take a look at any other factors that may limit the amount the VA will guarantee and review your personal circumstances to determine your overall eligibility for a VA mortgage.

Our checklist provides borrowers with specific steps that need to be followed to simplify the process, reducing the stress they may be feeling with moving to a new home. You can also use our free VA home loan calculator to estimate your monthly payment.

If you have questions about any VA loan products, feel free to reach out to Griffin Funding to discuss your options and find out how we can best meet your needs as you start an exciting new chapter in your life. Start capitalizing on your VA loan benefits today!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can I buy a house that exceeds the VA home loan limit?

Are limits on VA loans the same in every state?

Can I buy multiple homes with my VA loan?

When do VA loan limits increase?

VA loan limits increased in 2024, again in 2025, and saw another increase in 2026. The 2026 VA loan limits were announced by the Federal Housing Finance Agency (FHFA) in November 2025, with the standard limit rising to $832,750 — up from $806,500 in 2025.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

The Ultimate Home Maintenance Checklist for Every Season

Why Every Homeowner Needs a Home Maintenance Checklist Below are a few reasons why every homeowner can benefit...

Do HELOCs Have Closing Costs?

Yes, most lenders charge closing costs on a home equity line of credit, though they’re typically lower than ...

Does a HELOC Require an Appraisal?

Yes. In most cases, a lender will require an appraisal for a home equity line of credit to determine your home...