How Long Does It Take to Get a VA Loan?

How Long Does It Take to Get a VA Loan?

KEY TAKEAWAYS

- Before starting the VA loan process, ensure that you’ve obtained your Certificate of Eligibility (COE) from the Veterans Administration (VA).

- Closing is expected within several weeks, but taking actionable steps like communicating frequently with lenders and gathering all necessary documentation can help expedite the process.

- If you get pre-approved for your VA loan, you can present yourself as a more competitive buyer while also knowing your budget ahead of time.

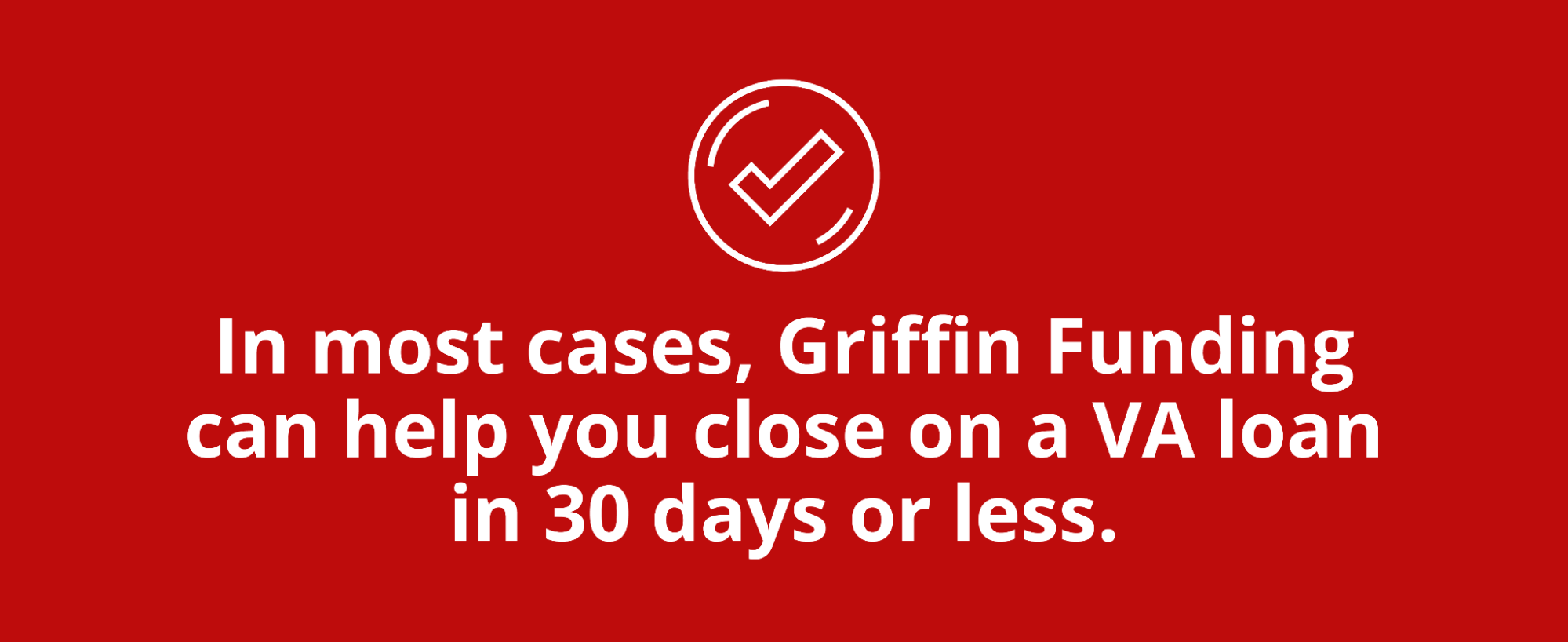

Are you considering purchasing your dream home with your first VA loan? If so, you may be wondering how long it takes to close on a house with a VA loan. With most lenders, you can expect your VA loan to close anywhere between 40 and 50 days. However, when you work with an experienced VA loan lender like Griffin Funding, you can typically close on your VA loan in 30 days or less.

Overall, there are various factors that will affect how long it takes to close on a VA loan. Below, we go through the VA loan timeline and discuss some of the factors that can impact how long the VA loan process takes.

KEY TAKEAWAYS

- Before starting the VA loan process, ensure that you’ve obtained your Certificate of Eligibility (COE) from the Veterans Administration (VA).

- Closing is expected within several weeks, but taking actionable steps like communicating frequently with lenders and gathering all necessary documentation can help expedite the process.

- If you get pre-approved for your VA loan, you can present yourself as a more competitive buyer while also knowing your budget ahead of time.

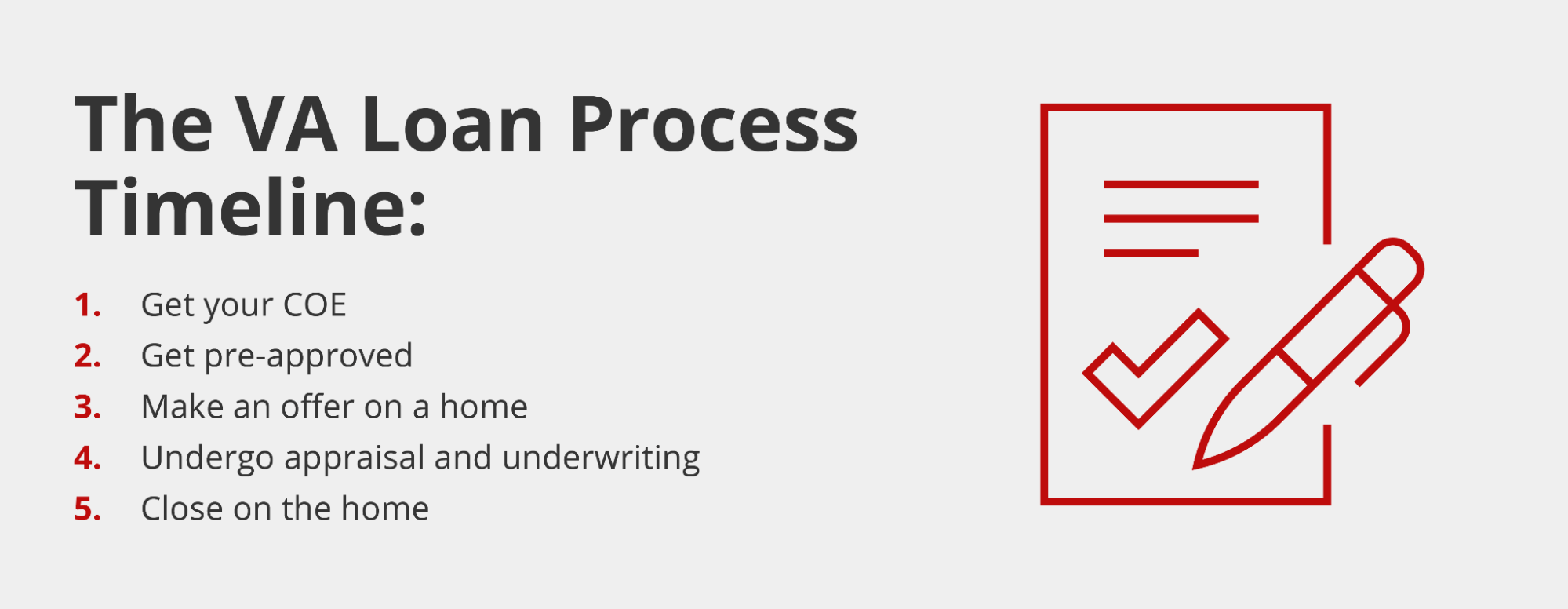

VA Loan Process Timeline

Embarking on your VA home buying journey? Kick it off by understanding the timeline of the VA loan process. There are multiple steps you should be aware of in order to make sure that everything goes smoothly in your application. Here’s a breakdown:

Obtain your Certificate of Eligibility (COE)

Before anything else, veterans must receive their COE from the Department of Veterans Affairs as proof they meet the eligibility requirements for the loan program. In order to get your COE, you must meet the minimum service requirements as outlined by the VA.

Obtaining a COE is relatively straightforward, as you can get your COE through your lender or request it directly from the VA via mail. Just be sure to request your COE sooner rather than later, as it can take weeks to receive it in some cases.

Get pre-approved

One of the best ways to streamline the process when applying for a VA loan is to get pre-approved. Pre approval means that you have met all of your lender’s basic requirements and are likely to get approved, as long as certain conditions are satisfied. A VA loan pre-approval shows sellers that you’re serious about buying and eliminates potential delays in the process. It also gives you a chance to review VA loan rates before you move forward.

To make sure things go smoothly, it’s best to start getting pre-approved before beginning your house hunt—that way any eligibility or income issues can be sorted out ahead of time, so there aren’t any surprises when it comes time to make an offer! Working with an experienced lender that knows how VA loans work will help ensure that everything goes according to plan. They’ll know which fees can be paid by the seller during negotiations so nothing gets left behind.

Make an offer

Making the most of your veteran benefits just got easier, because now you get to go house hunting. Working with a real estate pro who knows the ins and outs of the VA loan process will help ensure that you can maximize the value of your offer. If both parties agree, certain fees and costs can be paid for by the seller. After signing the purchase agreement, it’s time to move forward on this journey towards homeownership.

Appraisal and underwriting

Once you have your closing document in hand, your lender will get the ball rolling by ordering a VA appraisal. This appraiser makes sure that what you’re paying is on par with current market value as well as ensuring the home meets minimum property requirements (MPRs).

It’s important to note though that the appraisal isn’t meant to replace a professional home inspection, which assesses code violations and other defects or issues with the condition of the property. While a home inspection isn’t required for VA loans, lenders often recommend that home buyers order an inspection so that they can make themselves aware of any serious and potentially costly issues.

Meanwhile, submit documents confirming your ability to qualify for this loan while waiting on these results from related parties. When everything checks out – then comes final approval from the underwriter before the closing day arrives!

Close on the home

The next step? Get ready to close on your new place! Once approved by an underwriter, all that remains is signing documents confirming all terms are agreed upon and paying VA loan costs (if required). And don’t forget to make sure you have proof of homeowners insurance before getting those keys. Now comes what we’ve been waiting for: You’ll soon settle into your brand-new home!

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

How Long Does a VA Loan Take to Close?

If you’re a veteran looking to purchase your dream home, one of the biggest questions on your mind is probably, “How long does it take for a VA loan to close?” On average, from contract signing to closing day, you should expect the process to take around 40-50 days with most lenders. However, Griffin Funding is an experienced VA lender and our team aims to close most VA loans in 30 days or less.

There are also ways that you can expedite this process so that you can move into your new home as soon as possible. In the next section, we discuss some of the ways in which you can speed up the VA loan process and more quickly close on your new home.

Tips for Speeding Up the VA Loan Process Timeline

At this point in the game, all of your ducks need to be in a row if you want things done quickly and efficiently. To make sure everything goes as smoothly as possible, some of the things to focus on include:

- Double-check that all paperwork is up-to-date and accurate.

- Stay organized when submitting documents.

- Act quickly on any requests made by lenders.

- Know what you are looking for when the appraisal and inspection come in.

- Make sure every step meets deadlines set forth by banks or other financial institutions involved with processing payments.

Below, we go into a little more detail about some of these key steps.

Gather all of your documentation

Gathering your paperwork to speed up the VA loan process can be a challenge. But with some preparation, you’ll have all of the documentation required to get approved in no time!

You’ll need documents that prove who you are and where you live. This includes recent pay stubs (at least 30 days’ worth), W-2 forms from the last two years, 1099 forms, and IRS 1040 tax returns from each of those years along with any accompanying schedules or forms submitted with them.

If applicable to your situation, don’t forget to provide award letters from the VA if receiving disability benefits, Social Security benefit statements, pension award letters, and military retirement account statements.

It’s essential that everything is ready before applying for a loan so there won’t be any delays in obtaining approval. So take some time now and pull together these key pieces of information—it will make life much easier later on down the line!

Communicate with your lender

Communicating with your lender is crucial when you’re applying for a VA loan. As soon as the loan officer has collected all of your paperwork, they’ll send it to an underwriter who will review and approve or deny your application. Don’t be alarmed if some follow-up questions come up during this process, as that is totally normal.

The best way to make sure everything moves along quickly and efficiently is by your lender easy access to reach you. Provide them with cell phone numbers, email addresses, and fax numbers (if applicable) so they can get in contact with you at any time.

Understand VA requirements

Before you even begin the process of applying for a VA loan, it’s important to do some research so that you understand the VA’s requirements. The VA has specific eligibility and occupancy requirements that you must meet in order to get your VA benefits. Make sure you review all of the VA’s rules and requirements in order to ensure you can meet them and weigh the pros and cons of this loan type to make sure it’s right for you.

With these key tips in mind, rest easy knowing there’s nothing stopping you from getting to the closing table faster! If you have questions about the VA loan timeline, be sure to work with an expert who can help you. At Griffin Funding, it would be our pleasure to work with you.

Streamline the VA Loan Process With Griffin Funding

So how long does the VA loan process take? If you want to expedite the process, partner with a professional team. At Griffin Funding, we have plenty of experience helping individuals and families with the VA loan application process, and we can help you as well by closing your VA loan within 30 days.

Whether you’re in search of a VA loan or interested in other loan types, we can help you find the right financing to meet your needs, so give us a call today.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...