Debt Service

Coverage Ratio

(DSCR) Loans

Qualify for a DSCR loan with Griffin Funding using rental income, not personal income. No tax returns required. Last updated: July 2026

- Accessible for real estate investors

- Unlimited cash out

- No limit on the number of properties

- All types of rentals are eligible

DSCR Loans in July 2026: What Real Estate Investors Need to Know

Written and reviewed by Bill Lyons, President and CEO of Griffin Funding.

A DSCR loan qualifies real estate investors on a property’s rental income instead of tax returns, W2s, or DTI. The debt service coverage ratio equals gross monthly rent divided by PITIA (principal, interest, taxes, insurance, HOA). A 1.0 ratio means the rent covers the payment, and most lenders require 1.25. Griffin Funding qualifies down to 0.75 and offers no-ratio DSCR programs that do not use cash flow to qualify at all.

Fixed DSCR loan rates in July 2026 range from 6.125% to 7.5%, and adjustable DSCR loan rates range from 5.125% to 6.125%, based on credit score, DSCR ratio, down payment, buydown points, and prepayment penalty term (0 to 5 years), with sharpened pricing on jumbo DSCR loans up to $4.5M. View today’s DSCR loan rates →

In June 2026, our most recent closed month, Griffin Funding funded 84 DSCR loans totaling $24.1 million at an average borrower FICO of 743. Loans averaged $287,200 and ranged from $56,486 to $1,275,000. 51% were cash-out refinances (investors pulling equity to buy the next property), 29% were purchases, and the rest were rate-and-term refinances, at an average LTV of 67%.

DSCR loans account for 44% of Griffin Funding’s total funded volume YTD in 2026, $287,261,303 in DSCR originations, making us one of the most active DSCR lenders in the country. We close DSCR loans in as few as 6 days, with an average closing time of 34 days. Most DSCR lenders operate without licensing because these are business-purpose investment loans. As a national mortgage lender licensed in 47 states plus D.C., regulated by the CFPB, and approved by HUD as an FHA Non-Supervised Lender, we bring institutional accountability and transparent pricing to your portfolio. Rates are subject to change daily based on market conditions. 6/30/2026

Why DSCR Loans

DSCR Loan Benefits

No proof of income required:

Your eligibility for a DSCR loan is determined by your DSCR rather than tax returns or pay stubs. No proof of income or employment is required to qualify.

Flexible qualifying requirements:

DSCR loans aren’t subject to the strict requirements that conventional loan products must follow, meaning lenders can look past a lower credit score or down payment if other compensating factors are present.

Streamlined approval process:

Griffin Funding uses AI-driven underwriting to simplify and speed up DSCR loan approvals. Our proprietary Loan Intelligence Assistant (LIA) — which was recently featured in HousingWire — enhances accuracy and reduces underwriting times. In 2025, we closed DSCR loans in as little as six days, with an average closing time of 34 days.

Borrow in an LLC, S Corp, C Corp, or Trust:

You can take out a DSCR loan in the name of an LLC to protect your personal assets and potentially keep the loan off personal credit reports. This flexibility accommodates solo investors, business partners, and real estate syndications alike. Griffin Funding’s underwriting team can advise on the most appropriate vesting structure for your investment and tax situation. Trusts and corporations/S corps can generally hold title (vesting), but only LLCs are explicitly allowed to act as the actual borrower (with a personal guarantor required).

Purchase or refinance all types of rentals:

DSCR loans can be used for short-term, mid-term, and long-term rentals, as well as various property types, including single- and multi-family homes. Rural properties with limited acres and supporting rental comps are permitted as well.

Unlimited cash-out and no seasoning requirements:

Unlimited cash-in-hand allows you to take out money as needed to cover expenses like repairs and renovations. Additionally, no seasoning period is required — you can cash-out immediately after acquisition if you want.

Jumbo DSCR loans available:

Finance high-end and luxury rental properties with jumbo DSCR loans up to $4.5 million in-house, and up to $20 million on a case-by-case basis for larger deals.

No limit on the number of financed properties:

Conventional loans restrict investors to 6–10 financed properties, however DSCR loans have no such limit.

No private mortgage insurance:

While conventional loans require PMI for down payments under 20%, DSCR loans do not come with mortgage insurance, which can help you save on long-term costs.

How it Works

What Is a DSCR Loan & How Does It Work?

A DSCR loan is a type of non-qualified mortgage (non-QM) loan designed specifically for real estate investors that allows you to qualify for financing based on the real or potential cash flow of a property rather than tax returns or pay stubs.

This is an ideal mortgage solution for real estate investors who may claim significant tax write-offs that lower their personal taxable income, or who otherwise are unable to qualify for traditional home financing.

Key features of DSCR loans include:

- No income or employment verification

- Qualify based on rental property cash flow (DSCR)

- Only for income-generating investment properties

- Flexible qualification requirements

- Fast approval process

“DSCR loans are great financing alternatives to have borrowers build wealth along with their portfolio without showing any personal income to qualify. We don’t even verify if you have a job or not; we look solely at the property to see if the rent covers the payment. Another reason to take advantage of the DSCR loan is you can put them in LLCs, this will keep all your mortgage debt liability away from your personal credit, so when you need to personally qualify for a loan, there won’t be a mortgage to show, it will be completely separate and off your credit report!”

Cody Unger, Branch Manager, NMLS# 1295308

Loan Requirements

DSCR Loan Requirements

Property type

Rental properties only. Not for primary residences.

DSCR

≥ 1.0 ideal; < 1.0 allowed with extra reserves.

Down payment

Qualify with down payment as low as 15%.

Credit score

620+ minimum. Griffin borrowers averaged 739 in 2025.

Loan amount

$100K–$4.5M depending on property value.

Appraisal

Required for value + rental income verification.

DSCR Rates

Today’s DSCR Loan Rates

See today’s DSCR loan rates for your next investment purchase or refinance.

1-year ARMs start at 5.125%. 30-year fixed, 40-year fixed, and 5-year ARM options start at 6.125%.

“When I advise real estate investors on DSCR loans, the first step is comparing the payment difference between an interest rate with no points versus a lower rate with points. Recently, I worked with a borrower who could save $190 per month by buying down the rate. But since their plan was to refinance in four to five years and use equity to purchase another property, they chose the higher rate with no points. That strategy kept more cash in their pocket today, while rental income still covered the mortgage. By waiting to refinance when rates are lower, they’ll preserve liquidity now and use future equity to keep building their portfolio.”

Adam Ruvelson, Branch Manager, NMLS# 1283827

Loan Options

DSCR Loan Types We Offer

Traditional DSCR Loan Programs

The DSCR purchase loan is the best option for real estate investors buying a new rental property, allowing them to qualify based on the property’s expected rental income rather than personal income, W-2s, or tax returns.

The DSCR cash-out refinance is the best option for investors who want to access equity in an existing rental property and redeploy it into new acquisitions, with no seasoning period required and no cap on cash-in-hand at closing.

The DSCR rate and term refinance is the best option for investors transitioning out of high-rate hard money or bridge financing into a stable, long-term mortgage, or for those looking to lower their rate or extend their term to improve monthly cash flow.

The DSCR HELOAN is the best option for investors who want to tap equity in an existing rental property without touching their first mortgage, qualifying on rental income rather than personal income while keeping the existing first lien rate in place.

Unique DSCR Loan Programs

The DSCR no-ratio loan is the best option for investors purchasing properties in high-value, low-yield markets where rents do not cover PITIA at standard thresholds.

- Secure financing with DSCR below 1.0

- Down payment as low as 25%

- 700+ FICO

- Loan amount up to $1 million

- Cash-out as high as 75%

The 15% down DSCR loan is the best option for high-credit investors who want to maximize leverage and preserve capital across multiple acquisitions.

- Only 15% down payment required

- 740+ FICO

- Loan amount up to $1 million

The rental income plus assets program is the best option for high-net-worth investors whose rental income alone falls just short of standard DSCR thresholds, allowing them to blend verified liquid assets with property income to strengthen qualification and increase borrowing power without pledging those assets as collateral.

The six-month and 1-year SOFR ARM DSCR loan is the best option for investors with a short-to-medium-term hold strategy who want the lowest available starting rate, offering fully amortized or interest-only adjustable-rate financing tied to SOFR with rates starting as low as 5.125%.

“Between the creative financing options we offer, our ability to make some exceptions, and the flexible solutions we provide, we demonstrate a deep expertise when it comes to non-QM loans while providing personalized service and a commitment to the client’s success. Our long-term relationships with clients are built on trust and the mutual success of them closing on a loan. This leads to our clients having a little bit more financial freedom or being able to move into their dream home, where their kids all get a bedroom. So we are always dedicated to helping these clients achieve those financial objectives.”

Colby Freer, Senior Mortgage Consultant with 10 years of experience at Griffin Funding, NMLS# 1319705

What to Watch For With DSCR Loans

DSCR loans are not qualified mortgages, so they are not held to the same federal disclosure rules as conventional loans. That gives investors flexibility, but it also means you need to know what to look for before you sign.

Hidden Fees

Review the loan agreement to identify any fees or charges that may not have been clearly disclosed upfront. These can include:

- Loan origination fees

- Underwriting fees

- Administrative fees

Lenders present these fees on a “term sheet” or a “loan estimate.” Many unlicensed business-purpose lenders use a term sheet rather than a loan estimate, which can make the fees harder to understand. Because DSCR loans are not qualified mortgages, they are not held to the same disclosure requirements as loans that fall under federal TRID rules, and a term sheet can change without notice during the process.

“You need to make sure that you figure out what kind of prepayment penalty is being put on the loan because, in many cases, that’s not disclosed. DSCR loans don’t follow federal disclosure guidelines, so you technically don’t need to disclose anything at all until the end. We like to be transparent, so we actually send you a regular loan estimate that looks like what you’re getting on a conventional loan. This way, you know what your fees are and what your prepayment penalty is. You also know we vetted it out versus the rental income, so that the loan has a much higher chance of closing where it starts rather than changing along the way.”

Guy Troxler, Senior Loan Officer with 7 years of experience in the mortgage industry, NMLS# 1642169

Appraisal Issues

The lender requires a property appraisal to determine value. A lower-than-expected valuation, on either the property value or the rental income, can affect loan eligibility or require more money upfront. This is the issue most likely to cause fallout, but it does not have to. Discuss your options upfront and be prepared with a plan B and C, which in most cases means a larger down payment. You can use our free home value estimator to get an estimated value and range before the actual appraisal is performed.

“Who you work with on a DSCR loan makes all the difference. A typical loan officer who doesn’t specialize in DSCR loans may not anticipate common challenges, like an appraisal coming in low or rental comps underestimating actual rent potential. That’s why I always create a plan A, B, and C for my clients. No matter what obstacle comes up, we already have a solution in place to keep their investment strategy moving forward.”

Andre Shmoldas, Producing Sales Manager / Sr. Loan Officer, NMLS# 312335

Calculators

DSCR Loan Calculators

Use these tools to estimate your DSCR for a new purchase or refinance.

Where We Lend

Where We Offer DSCR Loans

Griffin Funding originates DSCR (Debt Service Coverage Ratio) loans for rental and investment properties in all 50 states and Washington, D.C. Open the list below for local DSCR loan requirements, qualifying rents, and rate guidance from a lender licensed in your market.

Don’t see your state? Griffin Funding lends nationwide. Request a quick quote and a licensed loan officer will confirm DSCR availability in your area.

America's Top DSCR Markets

Using the same methodology as our state-by-state market tables, we ranked the 50 largest U.S. metros by Example DSCR at a hypothetical 20% down. The spread is wide: rentals in New Orleans pencil at 1.21 while San Jose sits at 0.43, and seven of the ten strongest DSCR markets in America are in states where Griffin Funding has published a full market breakdown.

“Great team to work with from application through closing and afterwards for follow up needs. Very fast turnaround on rental property cash out mortgage. Have used them twice for this product and will again if I need to. Highly recommend for rental real estate investors!”

Sara J.

FAQ

Frequently Asked Questions

The debt service coverage ratio measures a property’s annual gross rental income against its annual mortgage debt, including principal, interest, taxes, insurance, and HOA (if applicable). Lenders use DSCR to assess loan affordability based on cash flow.

When calculating DSCR, lenders do not take into account expenses such as:

- Management

- Maintenance

- Utilities

- Vacancy rate

- Repair

Here’s how a DSCR loan works:

- Determine property income: The lender works with the borrower to determine the property’s gross monthly rental income. Rental income can be determined by either examining an existing lease or reviewing an appraiser’s comparable rent schedule. You can use our free rent estimator tool in the meantime to get an idea of what you might be able to rent the property for.

- Account for monthly expenses: The lender will tally up your monthly debt obligations associated with the property, which include principal, interest, taxes, insurance, and HOA fees (PITIA).

- Calculate DSCR: Using your monthly income and debt obligations, the lender can calculate DSCR. A DSCR above 1.0 indicates that a property earns enough to cover the mortgage, while a negative DSCR indicates that it does not.

- Loan approval based on DSCR: A lending decision for a DSCR loan is made based on the borrower’s DSCR and broader financial profile, as well as property details. No income documentation or tax returns are required.

Here’s what a DSCR loan looks like in practice. Consider a real estate investor purchasing a single-family rental priced at $400,000. They put 25% down ($100,000) and finance the remaining $300,000 at a DSCR loan rate of 7.0%.

| Principal + interest | $1,996 |

| Property taxes | $367 |

| Insurance | $167 |

| HOA | $120 |

| Total PITIA | $2,650 |

| Market rent (from comparable rent schedule) | $3,000 |

DSCR = $3,000 / $2,650 = 1.13

A 1.13 DSCR exceeds Griffin Funding’s 1.0 minimum, so the property qualifies through our standard DSCR loan program. The investor closes without submitting tax returns, W2s, or pay stubs. The property’s rent qualifies the loan.

What happens if the property rents for less? If the same property rents for $2,500/month against the same $2,650 PITIA, the DSCR drops to 0.94. Most lenders would decline at that ratio. Griffin Funding qualifies a DSCR loan down to 0.75 with additional reserves, or the investor can use our no-ratio DSCR loan program where the property’s cash flow isn’t used to qualify at all.

DSCR loans work especially well for active real estate investors whose rental property deductions and depreciation reduce their reported income and make conventional investor financing difficult to qualify for.

You can use a DSCR loan for rental property investments, including single-family homes, multifamily units, and short-term rentals. Lenders approve financing based on how much income the property generates, so you can focus on properties that strengthen your investment strategy and help you grow your portfolio.

Your DSCR changes as income and expenses shift. Rental rates, vacancies, and operating costs all affect the ratio. A strong DSCR signals a lower risk to lenders, while a weaker ratio can limit financing options.

Lenders often use market rent projections or appraisals to calculate DSCR, though some may also consider actual rental income. This flexibility helps investors secure financing for both established properties and those expected to generate strong income after purchase or renovation.

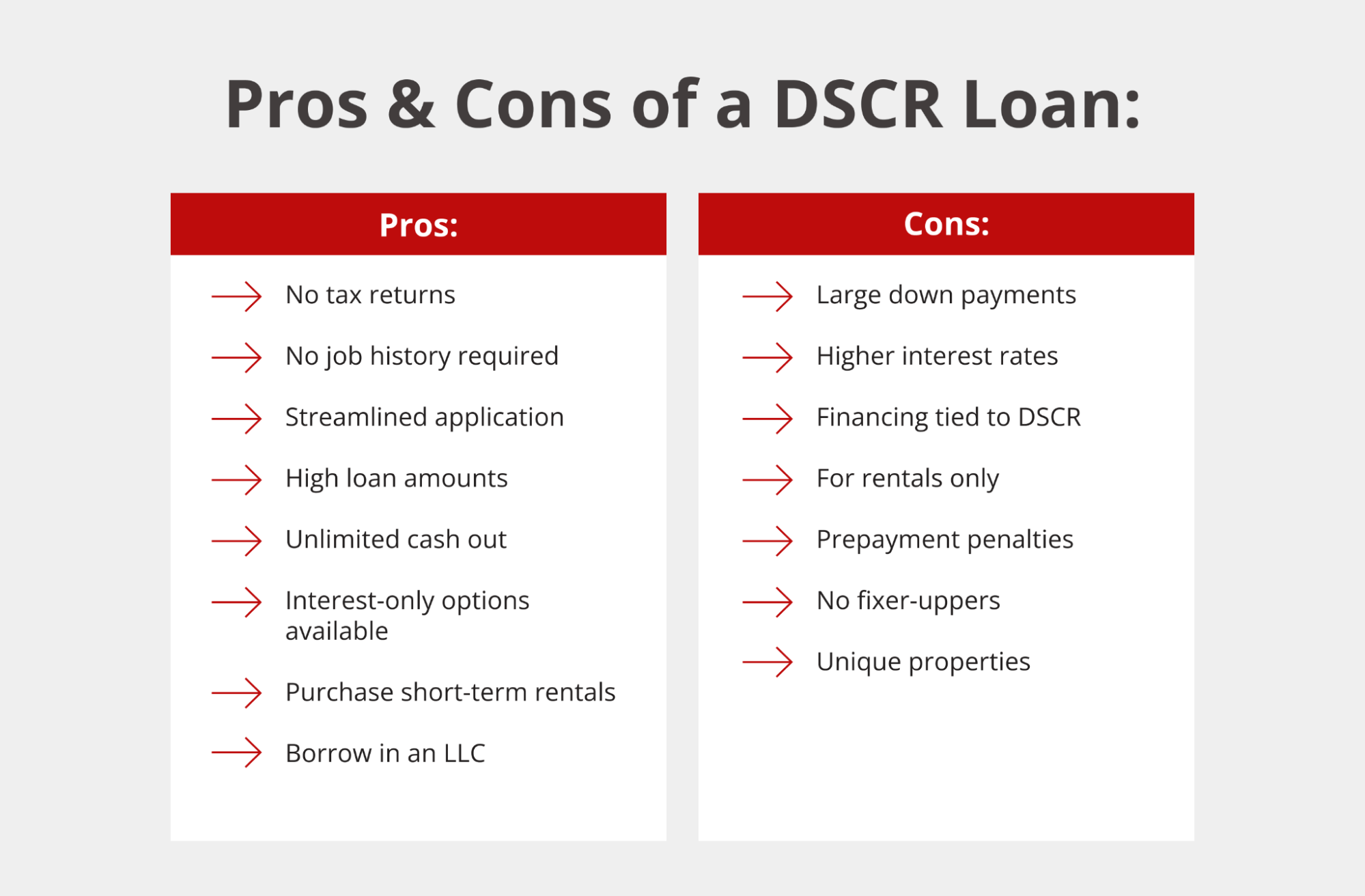

Pros of DSCR loans include:

- No tax returns required: Qualify for a mortgage without tax returns, W-2s, or any proof of personal income.

- No employment verification: Employment verification isn’t required to qualify for a DSCR loan. Underwriting is primarily concerned with a property’s DSCR rather than the borrower’s income or employment status.

- Streamlined application: Griffin Funding uses a proprietary AI-driven underwriting platform to speed up approvals for non-QM loans. Work with an experienced DSCR lender to get to the closing table quickly.

- Large loan amounts: Griffin Funding finances DSCR loans from $100,000 up to $4.5 million in-house, with exceptions available up to $20 million for larger portfolios and luxury markets.

- Unlimited cash-out: Capitalize on your equity and take money out of the property as needed. No seasoning period is required, which makes DSCR loans well suited for the BRRRR strategy (buy, rehab, rent, refinance, repeat).

- Interest-only loan options: Make interest-only payments for a set period of time in order to optimize cash flow.

- Buy short-term rentals: DSCR loans aren’t limited to long-term rentals; you can buy mid-term and short-term rentals as well.

- Borrow in an LLC: Protect your personal assets by taking out a DSCR loan in the name of an LLC.

Cons of DSCR loans include:

- Large down payment: Most lenders require a large down payment of 20-40%, which may be higher than some conventional mortgages. However, Griffin Funding allows for as little as 15% down.

- Higher interest rates: DSCR loans may have higher interest rates than some conventional investment property loans because they are underwritten based on the property’s rental income rather than the borrower’s personal income. However, recent loan-level price adjustment (LLPA) increases from Fannie Mae and Freddie Mac have pushed conventional investment loan pricing higher, which has narrowed the gap between DSCR and conventional rates.

- Loan size capped by rental income: Your maximum loan amount is driven by the property’s DSCR, so a property with weaker cash flow will qualify for a smaller loan even if you’re a strong borrower personally. Most programs require a DSCR of 1.0 or higher. Griffin Funding goes down to 0.75, and we also offer no-ratio DSCR loans where the property’s cash flow isn’t used to qualify at all.

- Rental properties only: DSCR loans are for buy-and-hold rental properties only, so they can’t be used for a primary residence or to fix and flip a home. You can only use a DSCR loan for a property that generates cash flow.

- Prepayment penalties: Most DSCR loans come with a prepayment penalty ranging anywhere from one to five years. You will get a lower interest rate in most cases if you opt for a prepayment penalty, however there are many different kinds of prepayment penalties so make sure to discuss the details with your loan officer. DSCR loans are available without prepayment penalties, and prepayment penalties can be bought out.

- No fixer-uppers: The property must be move-in ready for tenants and not in need of major repairs, renovations, or construction. DSCR loans are not for properties that need to be rehabbed. The appraiser cannot mark the appraisal “subject to”.

- Unique properties not always eligible: Unique properties, such as rural properties and those that can’t be compared to other like properties around the area, can be difficult to finance using a DSCR loan.

- Vacancy risk: Your ability to repay depends on consistent rental income. DSCR loans can still finance vacant properties, but underwriting applies additional restrictions when no tenant is in place.

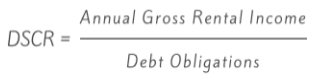

Debt service coverage ratio is a metric that represents how much income a property generates compared to its debt obligations. The formula for DSCR is:

DSCR = Gross Rental Income / Debt Service

- Gross rental income: The real or projected monthly income generated by a rental property.

- Debt service: The total monthly principal, interest, taxes, insurance, and HOA fees tied to the property.

Griffin Funding calculates DSCR using gross rental income divided by PITIA, not net operating income (NOI). This is an important distinction. Some lenders calculate DSCR using NOI, which deducts operating expenses like vacancy allowance, property management fees, maintenance, and repairs from rental income before dividing by debt service.

Because Griffin Funding uses gross rent, the full rental income before any expense deductions, the same property produces a higher DSCR under Griffin’s formula than it would with a lender using an NOI-based calculation. Griffin Funding explicitly excludes the following from the DSCR calculation: management fees, maintenance costs, utilities, vacancy rate, and repair expenses. This approach allows more properties to qualify, at better ratios, compared to lenders using NOI-based underwriting.

The debt service coverage ratio provides the lender with a metric that helps them gauge a borrower’s ability to pay off their DSCR mortgage. Lenders must forecast how much a real estate property can rent for so that they can predict a property’s rental value.

Most DSCR loans require a down payment of at least 20 to 25 percent. The exact amount depends on the property, lender, and your overall financial profile. A higher down payment may improve your loan terms and lower DSCR loan interest rates. Griffin Funding allows for down-payments as low as 15%.

Lenders typically look for a credit score of 620 or higher for DSCR loans. A stronger credit score may help you secure better terms and lower DSCR loan interest rates. Even if your score is lower, Griffin Funding can review your options to see what works best.

Many lenders will require a 1.25 DSCR to qualify for a DSCR mortgage loan. However, Griffin Funding allows real estate investors to qualify for a loan with a DSCR of less than 1.00.

Please note that borrowers with a good DSCR ratio can secure more beneficial rates and terms on their loans with fewer requirements. Interest rates are best on DSCR ratios of 1.25 or above, while a DSCR ratio of less than .75 requires more down payment/equity and more reserves to offset the negative cash flow.

Keep in mind that for DSCR loans that we fund, the average property has a DSCR of 1.05.

Yes, although qualifying may be more difficult. A DSCR below 1.0 means your rental income does not fully cover the debt, which increases lender risk. Some lenders still approve loans with lower ratios, but often at higher rates or stricter terms.

Some steps you can take to improve your DSCR include:

- Increasing rental income: Boost rental income by optimizing occupancy rates, increasing rental rates in line with market trends, or offering additional services or amenities to attract tenants.

- Refinancing existing loans:Explore refinance opportunities to lower your current rate, increase your loan term, or add an interest-only feature, thereby reducing your monthly debt service obligations.

- Increasing property value: Invest in upgrades or renovations to boost property value and command higher rental rates.

- Managing your expenses: Cost-saving measures like energy-efficient upgrades, outsourcing maintenance services, or negotiating vendor contracts can help reduce operating expenses.

In some cases, DSCR loan rates can be slightly higher than conventional investment mortgage rates due to the increased risk taken on by the lender. However, with loan-level price adjustments (LLPAs), DSCR loans can offer similar or even lower rates than conventional loans.

LLPAs are risk-based fees charged by Fannie Mae and Freddie Mac that can increase your rate when you invest in real estate using a conventional mortgage. LLPAs can add 0.5%-1.5%+ onto your conventional mortgage rate. DSCR loans, on the other hand, don’t conform to guidelines set by the Fannie Mae LLPA matrix, so they don’t come with LLPAs.

No, DSCR loans are only for investment properties. They are designed to help you purchase or refinance rental properties based on income potential. If you want financing for a primary residence, you’ll need to explore other mortgage options.

No, a DSCR loan is not a hard money loan. Hard money loans are short-term and come with very high rates. DSCR loans are structured like traditional mortgages, with longer terms and more favorable interest rates for investors.

PITIA stands for principal, interest, taxes, insurance, and association fees. Lenders compare your rental income to PITIA to calculate DSCR. The lower your PITIA compared to rental income, the stronger your ratio and the easier it is to qualify for financing.

Yes, in many cases gift funds can be used for the down payment or closing costs on a DSCR loan, but eligibility depends on the lender’s specific requirements. At Griffin Funding, gift funds are typically permitted; however, many DSCR programs require the borrower to contribute a minimum of 10% of their own funds to the transaction.

Our team can review your scenario, confirm whether gift funds are allowed for your DSCR loan structure, and help you document them properly to meet underwriting guidelines.

You can connect directly with a Griffin Funding loan specialist. They’ll walk you through DSCR loan pros and cons, current DSCR loan interest rates, and specific requirements. This personalized guidance helps you choose the best loan for your investment goals.

DSCR loans continue to be one of the most popular financing options for real estate investors in 2026, building on record demand throughout 2025. Strong investor demand, expanding rental markets, renewed tax incentives, and rising homeowner equity create a favorable environment for acquiring investment properties this year. Here’s why DSCR loans stand out:

- 1. Investor activity in the housing market remains strong

Real estate investors continue to play a major role in today’s market. According to Redfin’s Q3 2024 Investor Home Buying Report, investors purchased 15.9% of all U.S. homes sold in that quarter representing roughly $38.8 billion in acquisitions.

Investor activity is even higher in key rental markets, including:

- Miami: 28.2% investor share

- Anaheim: 24.3%

- San Diego: 23.3%

This sustained purchase activity signals ongoing demand for rental housing — an ideal environment for DSCR-backed financing.

- 2. Homeowner equity continues to climb, strengthening real estate fundamentals

CoreLogic reports that homeowner equity increased 9.6% year-over-year in Q1 2024, with the average borrower gaining approximately $28,000 in additional equity.

Rising equity:

- Supports property values

- Increases available cash-out opportunities

- Creates a favorable climate for acquiring additional rental properties using DSCR financing

- 3. Major tax benefits returned under the One Big Beautiful Bill (2025)

The passing of the One Big Beautiful Bill (OBBBB) in July 2025 reinstated 100% bonus depreciation, allowing real estate investors to write off certain property improvements and eligible components in the year acquired.

This renewed tax incentive is expected to drive even more investor demand in 2026 — making it an opportune time to buy rental properties using DSCR loans.

- 4. DSCR loans remain one of the strongest segments of the non-QM market

DSCR loans continue to dominate non-QM production due to their flexibility and investor-friendly structure. According to S&P Global Ratings, DSCR loans represented nearly half of the collateral (by balance) in the non-QM securitizations S&P rated between July 2022 and July 2024.

As of mid-2025, industry data shows DSCR loans accounting for roughly 28–29% of all non-QM originations, second only to bank-statement loans — confirming their continued popularity among real estate investors.

- 5. DSCR financing solves the biggest challenge investors face in 2026: income documentation

Traditional mortgage guidelines have tightened, and conventional loans still limit borrowers to 6–10 financed properties.

DSCR loans offer a streamlined alternative:

- No tax returns or paystubs required

- Qualification based on rental income

- Borrow in an LLC

- Unlimited property count

- Ideal for both short-term and long-term rentals

This makes DSCR financing particularly attractive for scaling a portfolio in a year where investor activity and tax incentives are both rising.

A DSCR loan is perfect for real estate investors who want to qualify using property income instead of personal income. This is especially useful if you are self-employed, own multiple properties, or want to scale your portfolio quickly.

Yes, first-time investors can qualify for DSCR loans. As long as the property meets income requirements, you can use this financing to get started in real estate investing.

Yes, DSCR loans are one of the best ways to build a rental property portfolio. Since approval focuses on property income rather than your personal income, you can keep growing your investments even as you add more properties.

Yes, you can refinance investment properties using a DSCR loan. Refinancing can help you lock in better interest rates, access equity, or restructure debt to improve cash flow.

While DSCR loans can be a helpful financing option for many real estate investors, there are certain scenarios in which using a DSCR loan may not be ideal. Here are some cases where a DSCR loan may not be the best choice:

- You’re buying a primary residence

- You want to purchase a distressed property

- You’re interested in a fix-and-flip project

- You’re purchasing a property worth less than $100,000

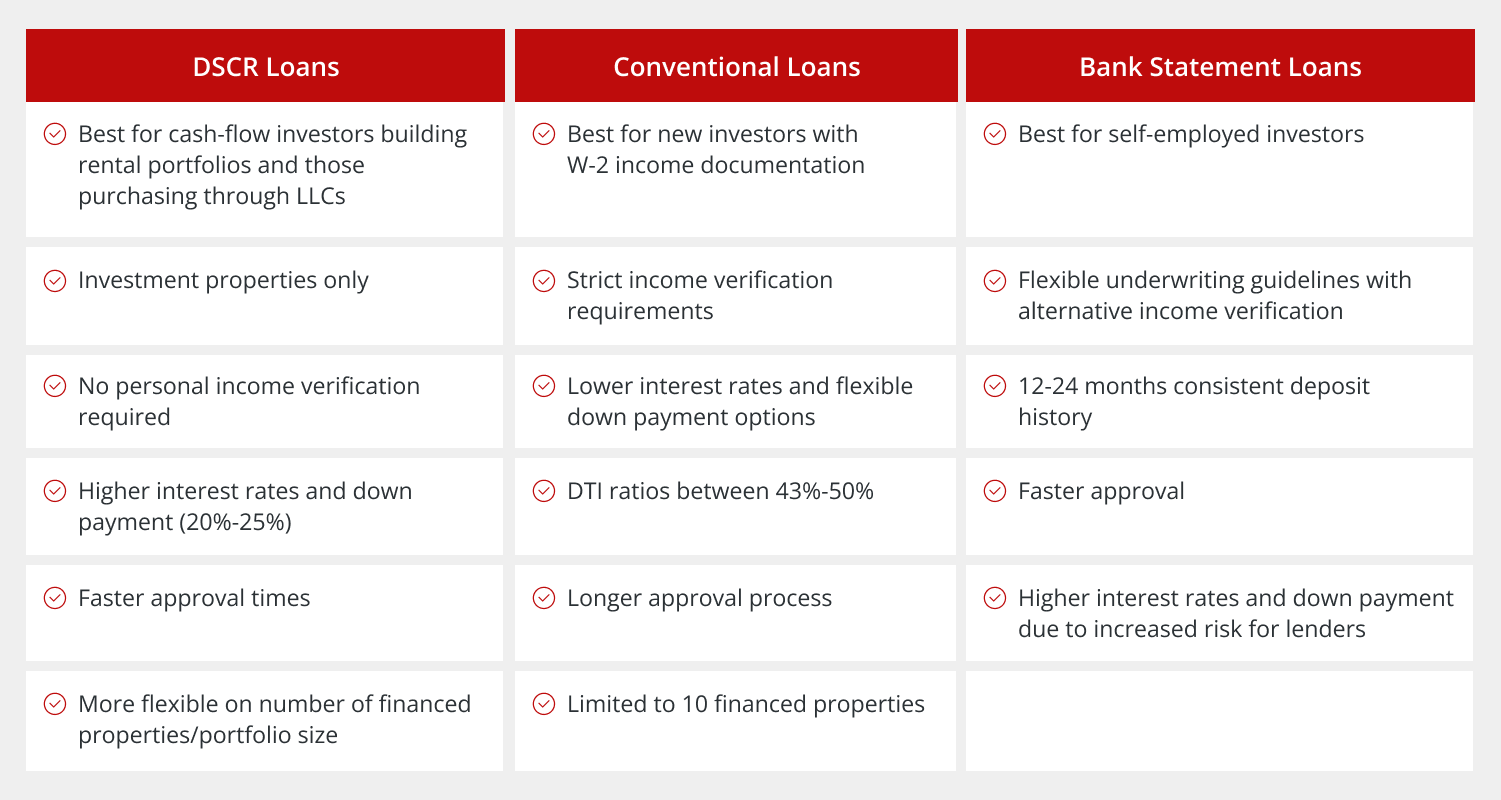

DSCR loans are designed specifically for real estate investors, and can be a great mortgage solution whether you’re a seasoned investor or you’re buying your first rental property. Review this comparison table below and read our blog about how DSCR loans differ from other investor mortgage products:

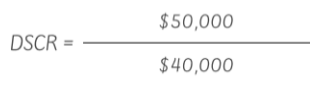

A real estate investor might be looking at a property with a gross rental income of $50,000 and an annual debt of $40,000. When you divide $50,000 by $40,000, you get a DSCR of 1.25, which means that the property generates 25% more income than what is necessary to repay the loan. This also means that there is a positive cash flow in the lender’s eye.

Real estate investors scaling a rental portfolio typically use one or more of the following financing strategies:

- DSCR loans: The most widely used vehicle for portfolio scaling. DSCR loans qualify based on each property’s rental income, not personal income or DTI. Because each property qualifies independently, investors can add properties without their personal debt load affecting approval. Griffin Funding imposes no limit on the number of DSCR-financed properties.

- Cash-out DSCR refinances: Once a property has built equity, investors extract that equity through a DSCR cash-out refinance—no seasoning period required, unlimited cash-out available at Griffin Funding—and use the proceeds to fund the next acquisition.

- BRRRR strategy: Buy, Rehab, Rent, Refinance, Repeat. Investors acquire a distressed property with short-term bridge financing, renovate it, lease it, then refinance into a long-term DSCR loan to recycle capital into the next deal.

- Conventional investment loans: Fannie Mae and Freddie Mac investment property loans are available up to 6–10 financed properties per borrower. Once that limit is reached, DSCR loans become the primary scaling vehicle.

- Portfolio loans: Blanket loans consolidating multiple properties under one note. Griffin Funding structures DSCR loans on a property-by-property basis, which gives investors more flexibility to sell or refinance individual assets without affecting the rest of the portfolio.

DSCR loans are the best financing option for Airbnb and short-term rental (STR) properties because they qualify based on a property’s projected or actual rental income rather than the borrower’s personal income, W-2s, or tax returns.

Griffin Funding calculates STR qualifying income using either a.) an appraiser’s income estimate, called a short-term rental narrative, b.) 12 month history of actual rental income from the existing property, or c.) AirDNA historical platform data.

Griffin Funding offers DSCR loans for STR properties across all 50 states with a minimum 640 credit score, minimum 0.75 DSCR, and as little as 15% down.

The best place is with a lender who specializes in DSCR loans, like Griffin Funding. You’ll benefit from competitive rates, flexible terms, and a team that understands how to tailor financing to your investment strategy.

Griffin Funding is one of the top direct-to-consumer DSCR lenders in the United States, helping real estate investors access non-traditional mortgage solutions nationwide. Founded in 2013, Griffin has grown into a trusted leader in DSCR loans, specializing in helping clients qualify based on rental income and property cash flow, not tax returns or W-2s.

Here’s why you should choose Griffin Funding as your DSCR mortgage lender:

- Excellent customer reviews: We’re backed by an A+ BBB rating and thousands of 5-star reviews across Google, Yelp, and the BBB.

- Nationwide DSCR lender: Griffin Funding is proud to serve investors in all 50 states with transparent terms, expert guidance, and exceptional client service.

- Innovative AI-driven underwriting platform: Our proprietary Loan Intelligence Assistant (LIA), recently featured by HousingWire, uses AI-driven underwriting to streamline the approval process, reduce manual errors, and fund loans faster. We’ve closed DSCR loans in as few as six days, with an average closing time of 34 days.

- Direct-to-consumer advantage: Griffin Funding is a consumer-direct mortgage lender, which means you can access flexible terms without dealing with any middleman.

- Easy-to-use digital tools: Our digital mortgage platform, Griffin Gold app, and free interactive financial calculators all serve to make the borrowing experience smoother and easier to understand.

- Institutional Security for Business-Purpose Financing

Because Debt Service Coverage Ratio (DSCR) loans are business-purpose loans for investment properties, the vast majority of DSCR brokers and lenders choose to operate completely unlicensed. Griffin Funding is different. We back our non-QM and DSCR investor programs with full institutional credentials. We are licensed in 47 states and D.C., federally overseen by the CFPB, and trusted as a HUD-approved FHA Non-Supervised Lender—giving you the peace of mind that your investment capital is backed by an established, fully compliant national lender.

“Our mission is to empower real estate investors to grow wealth through smarter financing by combining technology, transparency, and a client-first approach,” says Bill Lyons, CEO of Griffin Funding.

Whether you’re buying your first rental or expanding a multimillion-dollar portfolio, our team of experienced mortgage advisors is here to help you structure the DSCR loan that fits your investment strategy and goals.

Here’s how a DSCR loan can help you purchase a short-term rental:

- Short-term rentals are income-producing properties, making DSCR loans a perfect solution for investors who want to use the property’s rental income to qualify for the loan.

- By securing a DSCR loan with favorable terms, investors can potentially lower their borrowing costs and improve cash flow from their STR properties.

- Investors who already own STR properties can also refinance with a DSCR loan to lower their interest rates or access equity through a cash-out refinance. This can provide additional capital for property improvements, expansion, and other investment opportunities.

To get a DSCR loan on a short-term rental, you typically need to meet the following requirements:

- Minimum credit score of 640

- Minimum DSCR of 0.75

- Projected annual revenue divided by 12 months to demonstrate sufficient income to cover debts

Your DSCR directly impacts loan approval, interest rates, and terms. A higher ratio shows lenders that your rental income covers debt easily, which can lead to better rates. A lower ratio may limit options or increase costs.

Some lenders offer temporary rate buydowns on DSCR loans. This option lowers your initial interest rate, making early payments more manageable. Griffin Funding can help you explore whether a rate buydown fits your investment strategy.

DSCR loans are widely available, but not every lender operates in all states. Griffin Funding offers DSCR loans in all 50 states and the District of Columbia.

At Griffin Funding, qualified and organized borrowers can close on a DSCR loan in as little as six calendar days. Thanks to our AI-powered Loan Intelligence Assistant (LIA) and streamlined underwriting process, most DSCR mortgages close within 30 days or less from application to funding.

This efficiency gives real estate investors a competitive advantage, allowing them to secure financing, lock in rates, and close on properties faster than with traditional lenders.

Technically, no. Because DSCR mortgages are designated as business-purpose loans for residential investment properties rather than primary residences, most DSCR brokers and lenders are completely exempt from standard licensing rules in most states. However, Griffin Funding believes real estate investors deserve the same protections as traditional homebuyers. Unlike unregulated boutique brokers, we maintain active mortgage lender licenses across 46 states and D.C., strictly adhere to federal CFPB guidelines, and hold official HUD approval as an FHA Non-Supervised Lender.

The most important factors to evaluate when choosing a DSCR lender are:

- Minimum DSCR flexibility: Most lenders require a DSCR of 1.0–1.25. Griffin Funding qualifies down to 0.75 and offers no-ratio programs where the property’s cash flow isn’t used to qualify at all.

- Down payment requirements: Standard DSCR loans require 20–25% down. Griffin Funding allows as little as 15% for borrowers with 740+ FICO.

- Direct lender vs. broker: A direct lender originates, underwrites, and funds loans in-house. DSCR brokers add a middleman layer that can extend timelines and add fees without adding expertise.

- Licensing and regulation: Because DSCR loans are business-purpose loans, most DSCR brokers and lenders are not required to hold mortgage licenses. Griffin Funding maintains active licenses in 47 states and D.C., is federally regulated by the CFPB, and holds HUD approval as an FHA Non-Supervised Lender.

- Closing speed: Active real estate investors often need to move quickly on deals. Griffin Funding has closed DSCR loans in as few as 6 calendar days, with an average closing time of 34 days.

- LLC titling: Confirm the lender allows closing in an LLC to protect personal assets and keep loans off personal credit reports. Griffin Funding permits LLC and trust titling on all DSCR programs.

- Jumbo DSCR availability: If you’re investing in high-value markets, confirm the lender can fund large loans. Griffin Funding funds DSCR loans up to $4.5 million in-house, with case-by-case exceptions to $20 million.

- Nationwide reach: If you’re scaling across multiple states, work with a lender licensed in every market. Griffin Funding originates DSCR loans in all 50 states and Washington, D.C.