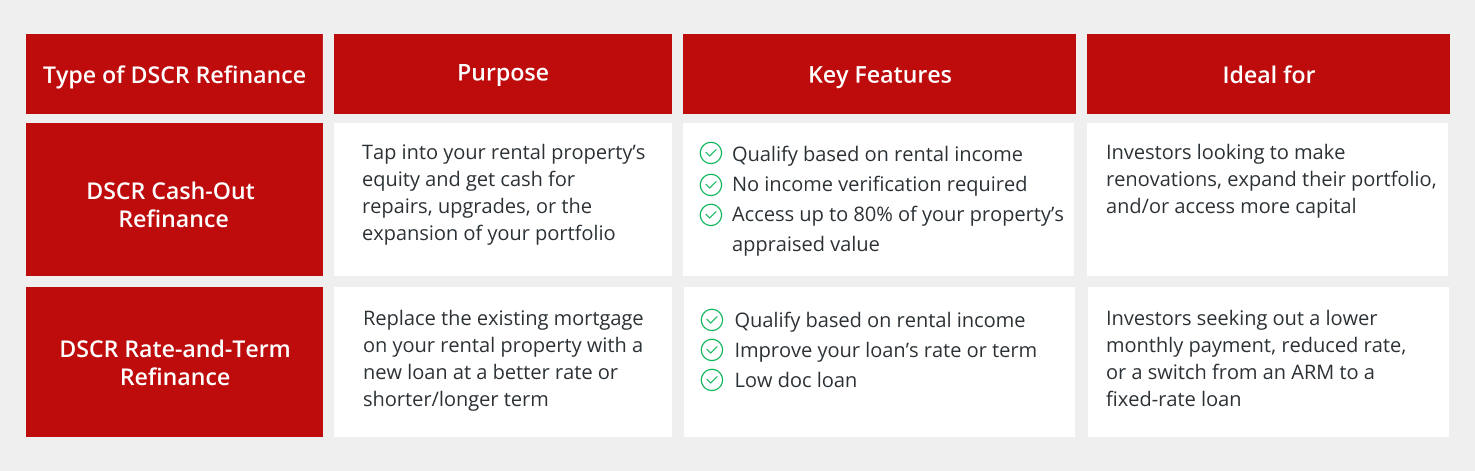

DSCR Cash-Out Refinance Loans

Real estate investors face a common challenge: accessing the equity they’ve built in their rental properties. DSCR cash-out refinance loans let you tap into your rental property’s value based on its rental income rather than your personal finances.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformWhat Is a DSCR Cash-Out Refinance Loan?

A DSCR cash-out refinance allows investment property owners to use a property’s rental income to qualify for a cash-out refinance rather than their personal income. The DSCR (debt service coverage ratio) measures how well your property’s rental income covers its mortgage payments.

A DSCR refinance works differently than traditional refinancing. Here’s what happens when you pursue a DSCR cash-out refinance on your investment property:

- Your lender evaluates your property’s current value and existing mortgage balance

- You can borrow up to 80% of the property’s appraised value

- The new loan pays off your existing investment property mortgage

- You receive the difference between your new loan amount and current mortgage as cash

DSCR Cash-Out Refinance Loan Example

With a DSCR cash-out refinance loan, if your property appraises for $400,000 and you owe $200,000, you might qualify for a new loan of $300,000 (75% of value). After paying off the existing $200,000 mortgage, you’d receive $100,000 in cash, minus closing costs.

Our DSCR loans make it easier to qualify compared to conventional refinancing options.

Pros and Cons of a DSCR Cash-Out Refinance

The benefits of a DSCR cash-out refinance are:

- No income verification needed: Skip the hassle of providing tax returns, W-2s, and pay stubs since qualification is based on property income alone.

- Streamlined approval process: Experience faster closings than conventional loans since there’s less documentation to review and verify.

- Portfolio-friendly qualification: Get approved even with multiple investment properties under your belt.

- Unrestricted fund usage: Use the cash for any purpose, from property improvements to personal investments, without restrictions.

- Tax planning opportunities: Potentially deduct interest payments and other costs, though consultation with a tax professional is recommended.

While DSCR cash-out refinancing offers significant advantages, it’s crucial to understand the potential challenges of an investment property cash-out refi before moving forward:

- Higher interest rates: You’ll typically pay more in interest compared to owner-occupied loans due to the increased risk to lenders.

- Increased property scrutiny: You’ll need to meet stricter requirements for property condition, location, and rental income history.

- Higher closing expenses: Due to the cash-out feature, you may pay more in closing costs compared to simple rate-and-term refinancing.

- Lower equity position: Refinancing your loan reduces your equity cushion, which could impact your options during market downturns.

- Future financing limitations: You may face potential restrictions on subsequent refinancing due to reduced equity and seasoning requirements.

DSCR Cash-Out Refinance Requirements

Before applying for a DSCR loan cash-out refinance, make sure you meet these general requirements:

- Minimum credit score of 620

- At least 20% remaining equity after cash-out

- Property must be an investment property (not owner-occupied)

- Clean title history

- Property must generate sufficient rental income

- DSCR ratio typically above 0.75 for cash-out (over 1.0 for cash-out to 80%)

- Seasoning period may apply (usually 6-12 months of ownership)

When you’re ready to explore a cash-out DSCR loan, you can use our DSCR calculator to quickly estimate the property’s DSCR and our DSCR refinance calculator to get a preview of what your loan may look like.

You can also manage your loan application process through the Griffin Gold app, which streamlines document submission and tracking.

Who Should Use a DSCR Cash-Out Refinance?

People who can benefit from a DSCR cash-out refinance on their investment property include:

- Real estate investors funding new purchases or upgrades

- Landlords with multiple rental properties

- Self-employed borrowers with steady rental income

- Owners needing renovation or repair funds

- Investors expanding their property portfolio

- Entrepreneurs seeking capital for business growth

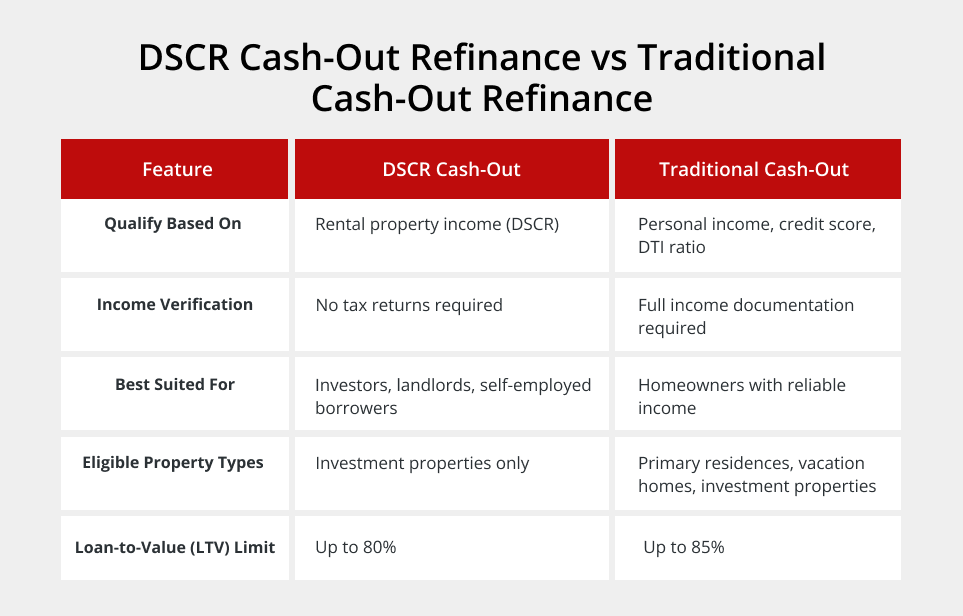

DSCR Cash-Out Refinance vs Traditional Cash-Out Refinance

Compare some of the key features of DSCR cash-out refinances compared to traditional cash-out refinance loans:

Get a Cash-Out Refinance Loan for Your Rental Property

Get a Cash-Out Refinance Loan for Your Rental Property

Real estate investors looking for easier ways to tap their property’s equity should consider DSCR cash-out refinancing. As long as you meet the minimum DSCR cash-out refinance requirements and understand the costs involved, you can use these funds for anything, from renovating rental properties to expanding your real estate portfolio.

Ready to invest in real estate or expand your portfolio? Our team specializes in investment property loans and can help you navigate the process for a cash-out refi on rental property. We also offer DSCR home equity loans as an alternative financing option.

Contact Griffin Funding to talk to a loan expert and learn more about your options or get started online right now.

Frequently Asked Questions

The funds from your cash-out refinance can be used for various business purposes, such as:

- Invest in real estate opportunities outside of the property

- Renovate existing properties already in your portfolio

- Consolidate high-interest debt

- Create an emergency fund

- Fund business opportunities

Typical costs for a cash-out refinance on an investment property include:

- Origination fees: These cover the lender’s processing costs.

- Appraisal costs: Expect to pay for a professional property valuation required by the lender.

- Recording fees: These are county-specific charges for documenting your new mortgage.

- Prepaid expenses: These costs include property taxes and insurance that must be paid in advance, often requiring several months’ worth.

DSCR cash-out refinance rates are usually higher than traditional cash-out refinance loans because this type of financing presents more risk for the lender and less income documentation required on behalf of the borrower.

Interest rates for DSCR cash-out refinance loans for multifamily properties and single-family homes vary depending on a number of factors, such as:

- Property income and stability

- Loan-to-value (LTV) ratio

- Credit score and borrower financial profile

- Property type and location

- Current market conditions and prevailing rates

See our current mortgage rates page for more information.

Securing competitive cash-out refinance investment property rates comes down to several key factors. Here’s what successful investors focus on to get the best terms:

- Keep your credit score above 700: A higher score means better rates and could save you thousands over the loan term.

- Maintain a DSCR ratio at least 25% above your monthly obligations: Lenders offer better rates when your rental income comfortably covers payments.

- Hold onto 25-30% equity after cash-out: More equity means less risk for lenders, translating to better rates.

- Document every rent payment and tenant history: Stable, long-term tenants and perfect payment records show lenders you’re a safe bet.

- Time your refinance with market trends: Even small rate changes can mean big savings over time.

- Get quotes from multiple lenders: DSCR loan rates vary widely between lenders, and shopping around pays off.

Remember, the lowest rate isn’t always the best deal. Consider the total cost of the loan, including points, fees, and other charges, when comparing offers. Some lenders may advertise attractive rates but make up for it with higher fees elsewhere in the transaction.

Yes, you can get a DSCR cash-out refinance if the property is held in an LLC. Griffin Funding allows properties to be titled in the name of a legal entity such as an LLC or corporation. This is often preferred by real estate investors who want to capitalize on added liability protection and potential tax advantages.

Lenders typically require a seasoning period that ranges from six to 12 months before allowing a DSCR cash-out refinance. This seasoning period lets the lender evaluate the income generation of the property and provides the borrower with time to build equity. Griffin Funding has no seasoning requirements on cash-out.

Yes, you can get a DSCR cash-out refinance loan on multiple properties at once. As long as all properties meet the minimum loan requirements, you can access equity across your real estate investment portfolio.

Yes, a DSCR cash-out refinance is designed for real estate investors, so properties held in an LLC or corporation are still eligible for financing. By holding the property in an LLC or corporation, real estate investors can capitalize on potential tax benefits and shield themselves from liability.