Bank Statement Loans

Say goodbye to W-2s and tax returns. A bank statement loan is a self-employed mortgage solution that allows borrowers to qualify using bank statements rather than tax returns or pay stubs.

- Ideal for business owners, freelancers, and self-employed individuals

- Flexible terms, higher loan limits

- More accurate reflection of your true income

June 2026 Update

Why Bank Statement Loans Beat Conventional Financing for Self-Employed Borrowers in 2026

Written and reviewed by Bill Lyons, President and CEO of Griffin Funding.

A bank statement loan is a mortgage for self-employed borrowers that qualifies the borrower based on 12 to 24 months of personal or business bank statement deposits rather than tax returns or W2s. Self-employed borrowers legally minimize taxable income through business expense deductions, which leaves their AGI too low and their conventional DTI too high to qualify on paper, even when their actual cash flow easily supports the mortgage. Conventional underwriting punishes the same tax planning their CPA recommends. A bank statement loan solves that by underwriting to actual deposit history. Griffin Funding bank statement loan rates currently range from 6.25% to 7.5% depending on credit score, down payment, loan amount, and buydown points, and we just sharpened pricing on jumbo bank statement loans up to $4M. View today’s bank statement loan rates →

Bank statement loans were Griffin Funding’s second most popular loan product in 2026, with $66,379,941 in bank statement loan volume YTD (including bank-statement-qualified HELOCs). Our average 2026 bank statement loan is $445,502, with an average borrower FICO of 719. 66% are cash-out refinances, 31% are purchase loans averaging 21% down, and 3% are rate-and-term refinances. Griffin Funding’s AI-driven underwriting platform allows borrowers to automatically sync their bank statements for a faster, streamlined approval process. Griffin Funding is a state-licensed non-bank mortgage lender authorized to originate non-QM loans, including bank statement loans, in 47 states plus DC, supervised by state mortgage regulators and the Consumer Financial Protection Bureau (CFPB). We’re also a VA-Approved Lender and a HUD FHA Non-Supervised Lender. As a CFPB-regulated lender originating bank statement loans, we are held to the same consumer-protection, fair-lending, and disclosure standards as any conventional mortgage lender, even though bank statement loans fall under the non-QM category. Self-employed borrowers get the qualification flexibility of a non-QM product with the regulatory accountability of a fully supervised lender. Rates are subject to change daily based on market conditions. 6/1/2026

Why Bank Statement Loans

Bank Statement Loan Key Benefits

Qualify using bank statements:

Ability to repay is based on bank statement deposits, not pay stubs or tax returns. Personal and business bank statements qualify.

No tax returns needed:

No need to submit tax returns or pay stubs.

Down payments as low as 10%:

Qualifying borrowers can get a bank statement loan with as little as 10% down.

Streamlined underwriting approval process:

We combine experience and technology — including our AI-driven underwriting platform — to speed up the underwriting process. Automatically sync 12 to 24 months’ worth of bank statements rather than manually uploading them.

Cash-out refinance up to 80% of the property’s value:

Access your built-up equity with a cash-out refinance. Alternatively, access equity via a bank statement HELOAN or HELOC.

Loan amounts of up to $4 million:

Griffin Funding finances Bank Statement loans from $100,000 up to $4 million in-house, with exceptions available up to $20 million for business owners purchasing luxury homes, high-value properties, or 2-4 unit residences.

DTI ratios of up to 50% can qualify (55% allowed by exception):

Flexible DTI ratio requirements make qualifying easier.

Fixed- and adjustable-rate options available:

Choose from a fixed- or adjustable-rate bank statement loan.

Interest-only option available:

Lower your monthly payment by only paying interest for a predetermined period of time.

How it Works

What Is a Bank Statement Loan?

A bank statement loan is a type of non-qualified mortgage (non-QM) loan that allows business owners, contractors, investors, and other self-employed individuals to qualify based on bank statements instead of tax returns and W-2s.

Bank statement loans look at your actual deposit history rather than the net income on your tax returns. Lenders review 12 to 24 months of personal or business statements, calculate average qualifying deposits, and use that figure to underwrite. This is why business owners and 1099 earners who write down their taxable income can still qualify for the home they can actually afford.

Key Bank Statement Loan Features:

- No employment verification

- No tax returns or pay stubs required

- Qualify using bank statements

- Self-employed mortgage solution

- Flexible qualification

Loan Requirements

Bank Statement Loan Requirements

Years self-employed:

Minimum 2+ years self-employed in most cases.

PITI reserves:

3+ months of PITI reserves required; larger loans require more.

Bank statements:

12 to 24 months of personal or business bank statements.

Down payment:

10% minimum down payment.

Credit score:

620+ minimum credit score.

Bank Statement Loan Rates

Today’s Bank Statement Loan Rates

Review today’s bank statement loan rates as you prepare to purchase or refinance.

Loan Options

Bank Statement Mortgage Loan Types

Purchase a home using 12 to 24 months of bank statements rather than traditional income verification. Available to self-employed borrowers. Primary residences, vacation homes, and investment properties all qualify.

Refinance your existing mortgage to potentially lower your rate, change your loan term, or replace your existing loan structure. Qualify with 12 to 24 months of bank statements, no tax returns or pay stubs required.

A bank statement cash-out refinance loan allows borrowers to pull cash out of their home equity by replacing their existing mortgage with a new, larger mortgage and pocketing the difference. Cash-out refinance up to 80% of the property’s value.

A bank statement HELOAN or HELOC allows borrowers with an existing home mortgage to pull cash out of their home equity by taking out a second mortgage. Use a HELOAN to obtain a lump sum or access a revolving line of credit with a bank statement HELOC.

A 6-month SOFR bank statement loan is an adjustable-rate mortgage (ARM) that starts at an initial rate and then adjusts every six months based on the 30-day average Secured Overnight Financing Rate (SOFR) index.

Calculators

Bank Statement Loan Calculators

Use our free bank statement loan calculators to see what buying or refinancing with a bank statement mortgage loan might look like.

Where We Lend

Griffin Funding offers bank statement loans to self-employed borrowers and business owners across the states where we are licensed. Open the list below for local qualifying guidelines, deposit requirements, and rate guidance from a loan officer licensed in your market.

Not sure if we lend in your state? Request a quick quote, and a licensed loan officer will confirm the availability of bank statement loans in your area.

Frequently Asked Questions

For all home loans, lenders need to verify your income before approval. In the case of bank statement loans, bank statements are used as income verification instead of W2s and your tax return. Typically, bank statement mortgage loans require 12 or 24 months’ worth of bank statements. One of our loan officers will then review your bank statements and verify the information with your bank.

Because of this alternative income-verification method, bank statement mortgages have become a popular option for self-employed individuals whose W2s and tax returns would not accurately reflect their full income.

Bank statement loans can benefit the following types of borrowers:

- Business owners (LLCs and S-Corps)

- Freelancers and consultants

- Gig economy workers (Uber, DoorDash, Instacart drivers, etc.)

- Independent contractors and 1099 earners

- Content creators and online entrepreneurs (YouTubers, influencers, e-commerce sellers)

- Realtors and commission-based professionals

- Real estate investors (Airbnb and Vrbo hosts, rental property owners, etc.)

- Creative professionals (photographers, artists, graphic designers, musicians, etc.)

Bank statement mortgages provide a flexible mortgage financing solution for self-employed borrowers. According to the Bureau of Labor Statistics, there are approximately 16 million self-employed workers in the United States as of mid-2025, representing about 10 percent of the total workforce when including both incorporated business owners and unincorporated self-employed individuals. Unfortunately, many of these business owners and self-employed individuals face roadblocks in securing traditional mortgage financing due to how they file their taxes.

- Calculate qualified income:

When you apply for a bank statement loan, an underwriter will calculate your qualified income by adding the total eligible deposits in your bank accounts for 12 or 24 months and dividing that number by 12 or 24 to give them an average monthly income.

- Meet basic loan requirements:

Self-employed borrowers can choose to use 12 or 24 months’ worth of bank statements, but there are other requirements. For instance, lenders like to see that you’ve been self-employed for at least two years or one year if you’ve remained in the same type of role or industry.

- Determine eligible deposits:

The deposits that can be used to calculate your income for a home loan depend on how you pay yourself:

- If you deposit money directly into your business account, lenders will typically use 50% of the deposits to determine your income.

- If you deposit money directly into your personal account (or transfer funds from a business account to a personal account), lenders may allow 100% of your deposits to qualify for the loan.

- Deposits that are not business-related are called “disallowed deposits” and will not be counted toward your income.

This doesn’t mean that you need monthly deposits, either. Instead, you may have seasonal income. For instance, if you earn $100,000 in just three months, lenders will divide that number by 12 (the number of months in a year) to find your average monthly income.

With a bank statement loan, it is possible to qualify for a mortgage with just bank statements. Bank statements are used in lieu of traditional income verification methods. Typically, 12 or 24 months’ worth of bank statements are required, but some individuals may be able to qualify based on the business’s P&L statement.

It’s also important to note that factors like your credit score and down payment will also be taken into consideration when establishing your loan terms.

Yes, you can get a second home, vacation home, or investment property with a bank statement loan. Second homes and investment properties can be purchased using bank statement loans for as little as 15% down payment.

Yes, bank statement loans are considered riskier than other mortgage options, especially for the lender. Since these loans are typically for self-employed borrowers who don’t have a traditional source of income and they’re not backed by Fannie Mae or Freddie Mac, they’re higher risk because they’re not guaranteed.

These loans may also be riskier for the borrower because they’re typically more expensive than conventional loans, so there’s an increased risk of defaulting on the loan. However, as long as you’re sure you can afford your monthly payments and your lender does their due diligence, there’s very little risk involved.

Interested in a bank statement loan but not sure where you stand financially? Here are some signs that you may be living beyond your means:

- Having a credit score below 620: Credit bureaus garner information regarding your payment history. This includes outstanding loans and credit card payments. From this information, they compile a credit score which reflects your worthiness for credit. The score is ranked from a low of 300 to a high of 850. Lenders use this score to determine whether you qualify for a loan. Typically, a credit score below 620 means that you are not financially viable enough to be approved for a loan.

- You are saving less than 5 percent: Lenders want to see that you are not spending more than you make. If you are saving less than 5 percent of your income, then you will probably not qualify for a bank statement loan.

- Your credit card balances are on the rise: If you are only paying the minimum due on your credit card balance and your balance is rising each month, you are not a likely candidate for a bank statement loan. To keep your debt under control, you should only charge what you can pay off each month.

- Your house payments take up more than 28 percent of your income: If you’re spending more than 28 percent of your gross income on your mortgage payments, then you are unlikely to qualify for a bank statement loan.

- Your total payments (house plus the minimum payments on your credit report) take up more than 50 percent of your income: If you’re spending more than 50 percent of your gross income on your mortgage payments, then you are unlikely to qualify for a bank statement loan. If you can prove that the business pays the payment then it will not be counted against you.

- You are behind in payment of your bills: Buying items on credit and paying off the balance in installments has become a popular way to live in the U.S. Problems arise when the bills start to spiral out of control. If a large proportion of your monthly income is taken up by this type of payment plan on top of your utility bills, it is unlikely you will be eligible for a bank statement loan.

Generally, bank statement loans are considered higher risk for lenders, so they typically come with slightly higher interest rates and down payment requirements than traditional loans. But ultimately, it depends on the home’s purchase price and the loan amount.

Bank statement loan rates tend to be slightly higher than conventional loan rates. However, rates are dependent on the lender you work with and your unique financial situation.

If traditional income verification methods don’t account for your true earning power, then you may not qualify for a conventional loan or your rate may be higher than you want. Additionally, if your goal is to purchase an investment property, loan-level price adjustments (LLPAs) can be added to your conventional rate and increase the cost of borrowing. Non-QM loans like bank statement loans and DSCR loans don’t come with LLPAs.

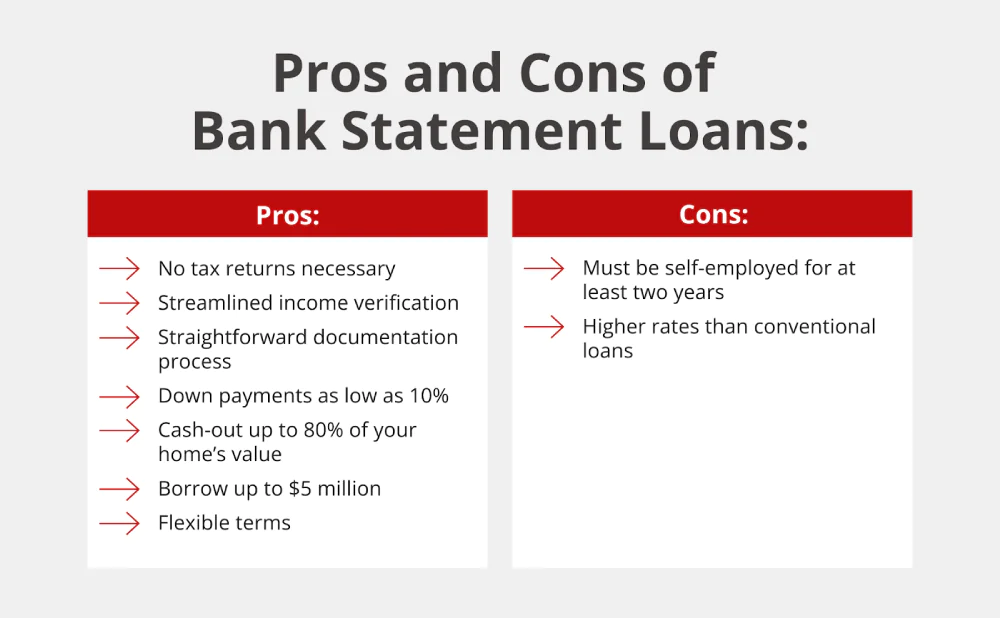

Potential downsides of a bank statement loan include:

- Must be self-employed for at least two years: One of the drawbacks for self-employed borrowers is that you have to be able to prove that you’ve been self-employed for two years—and if you haven’t quite reached that milestone, you’re out of luck and will have to wait. Exceptions are considered for business owners that have been in business for one year if you have at least two years of experience in the same line of work.

- Potentially higher interest rates: You may also have to contend with higher interest rates and down payments than more traditional loan options, but of course, this depends on your FICO score and overall financial circumstances. That said, Griffin Funding strives to secure competitive interest rates for our customers.

There aren’t any other loans that require bank statements, but you can use bank statements as a way to prove your income and qualify for other types of mortgages. In fact, you can use bank statements as one source of income verification for many of our Non-QM loans, such as jumbo loans and asset-based loans.

As an alternative to bank statement loans, we also offer P&L loans and 1099 mortgage loans.

- Qualify using a 12-month trailing profit and loss (P&L) statement only, prepared and signed by a licensed CPA or Enrolled Agent (EA).

- Griffin Funding uses the net income from your P&L – adjusted for ownership percentage and allowable add-backs – as your qualifying income.

- As an independent contractor, you can qualify for a 1099 mortgage loan with your 1099s, not your tax returns.

- Griffin Funding uses 100% of the income from your most recent year’s 1099(s) to qualify. You must have been contracted for at least two years.

If you’re looking for a self-employed mortgage, a bank statement loan is usually the best option. However, depending on your other sources of income, such as a full-time job in addition to your self-employed business endeavors, there may be other loan options for you to consider, such as:

- Conventional loans: Traditional home loans that meet the conforming loan limits and that meet the requirements set by Fannie Mae and Freddie Mac.

- Asset-based loans: These loans convert your assets to income to determine your ability to repay the loan.

- DSCR loans: Debt service coverage ratio (DSCR) loans are for real estate investors, focusing on rental property income rather than the borrower’s personal income.

- VA loans: Backed by the Department of Veterans Affairs, VA loans offer military veterans and active-duty service members favorable loan terms, including no down payment requirements.

- FHA loans: Supported by the Federal Housing Administration, these loans cater to first-time home buyers and those with lower credit scores, as they boast low down payments and flexible qualification criteria.

- Jumbo loans: These are mortgages that exceed the conventional loan limits, tailored for high-end properties or homes in competitive real estate markets.

- Bank statement home equity loans: Designed for self-employed individuals, these loans utilize bank statements to determine eligibility and allow homeowners to borrow against the equity built up in their property. You can check your mortgage statement for a breakdown of your outstanding balance to help you understand the equity built up in the property and use the Griffin Gold app to track your home value over time.

Griffin Funding is proud to offer several self-employed home loan products including both personal and business bank statement loans. Whatever your employment and income circumstances, our loan officers can help find the best mortgage solution for your needs.

Non-QM loans like bank statement mortgages differ from traditional mortgages when it comes to how income is verified. Instead of using W-2s or tax returns, lenders evaluate 12–24 months of bank statements to determine the borrower’s income, making them ideal for self-employed borrowers or those with non-traditional income sources.

Non-QM loans also offer more flexible credit guidelines and debt-to-income ratios but often come with higher interest rates than conventional loans. Traditional loans follow stricter government regulations and guidelines, while non-QM loans are privately underwritten and more flexible as far as qualifications, loan terms, and usage.

| Bank Statement Loan | Traditional Mortgage |

|---|---|---|

| Who is it for? | Bank Statement LoanBusiness owners, freelancers, investors, or anyone who doesn’t receive a W-2 | Traditional MortgageMost employees who

receive a W-2 |

| What is it used for? | Bank Statement LoanPurchasing a primary

residence, a vacation home,

or an investment property | Traditional MortgagePurchasing a primary

residence, a vacation home,

or an investment property |

| How is income verified? | Bank Statement Loan12-24 months of bank statements | Traditional MortgageTax returns and pay stubs |

| What’s the down payment? | Bank Statement Loan10% minimum | Traditional Mortgage 3% to 5% minimum (20% to avoid PMI) |

| What’s the minimum credit score? | Bank Statement Loan620 | Traditional Mortgage620 |

| How long is the loan term? | Bank Statement Loan15 to 40 years | Traditional Mortgage15 to 30 years |

To better understand how a bank statement loan works, consider the following example.

Christine is a self-employed digital marketing consultant based in Boston who has built a successful business managing campaigns for e-commerce brands. Her revenue has continued to grow over the past three years, averaging $20,000 per month in deposits over that period. However, due to business-related tax write-offs, Christine’s taxable income appears much lower on paper, which resulted in her being denied for a conventional mortgage.

To accommodate her situation, Christine applied for a bank statement loan through Griffin Funding. After reviewing 12 months of bank statements, the lender was able to calculate her true cash flow based on her monthly deposits.

Using a bank statement loan, Christine was able to get approved for the home loan amount she wanted without needing to provide tax returns, W-2s, or traditional income documentation.

It depends. On most of our personal and business bank statement loans, we require the last 12 or 24 months’ worth of bank statements.

In addition to bank statement, you may need to provide documentation such as:

- Personal identification

- Proof of residency

- Credit authorization

- Loan application

- Business documentation

- P&L statements

- Purchase agreement

See our bank statement loan document checklist for a full breakdown of all of the documentation you’ll need for a bank statement loan.

A credit score is one of the basic bank statement loan requirements for every lender.

Having a higher credit score is a good way to improve the chances of approval and keep your interest rates low on any type of mortgage including a bank statement loan. In order to qualify for bank statement loans with Griffin Funding, borrowers need a credit score of 620 or higher.

Income is just one of the lending criteria you’ll need to meet to qualify for a bank statement loan. If you’re trying to learn how to get a bank statement loan, you should understand that they work like many other loans.

So whether you’re a first-time buyer or this is your second, third, or fourth time purchasing a house, you’ll need to make a down payment. Of course, there are some types of government-sponsored loans that don’t require down payments, but Non-QM loans like bank statement loans do.

How much your down payment will be primarily depends on your credit score. For example, if you have a score of 680 or higher, you may qualify for a down payment of 10%. Meanwhile, if you have a credit score of 620, you’ll need to have a down payment of at least 20%. As you can see, bank statement loan down payments vary but can be higher than a traditional mortgage down payment.

In some cases it may be possible to get a bank statement loan if you’re not self-employed but have non-traditional income streams. For instance, freelance workers, gig economy workers, contractors, and realtors may be eligible for bank statement lending. However, it’s important to keep in mind that this type of financing is primarily for self-employed borrowers and business owners.

You can get a bank statement loan if you’ve filed for bankruptcy, but there are a few caveats. For instance, you’ll need to wait at least two years to apply for any type of mortgage loan after bankruptcy, but there are some exceptions. For instance, mortgage lenders may be more lenient if you can afford a large down payment and higher interest rates.

Yes, you can often qualify for a bank statement loan if you receive 1099 wages. If you work as an independent contractor or freelancer, you may receive Form 1099 rather than a W-2, which can complicate the process of qualifying for a conventional mortgage. This makes a bank statement loan a convenient alternative to traditional financing.

While a bank statement loan can be a viable option for those receiving 1099 income, we also offer a specialized 1099 mortgage program. This program is very similar to our bank statement loan program, but allows borrowers to use 1099 forms rather than bank statements to qualify. Reach out today to learn more about our 1099 mortgage program and other self-employed mortgage options! Griffin Funding counts 100% of the 1099 amount as your income.

The expense factor for a bank statement loan is typically 50%, meaning lenders count only half of your deposits as qualifying income. This accounts for estimated business expenses.

While we typically count 50% of bank statement deposits as income for business bank statement loans, we can offer an expense factor as low as 10% in some cases, depending on the type of business and number of employees. Keep in mind that for personal bank statement mortgage loans, we count 100% of bank statement deposits as income.

Yes, bank statement home loans and refinance loans typically require an appraisal. Like with other mortgage types, an appraisal serves to confirm the value of the property before the purchase is made.

If you’re wondering how to provide bank statements for a bank statement loan, the good news is that the process is fast and simple—and you don’t need tax returns or pay stubs to qualify. For a bank statement mortgage, all you need are 12–24 months of personal or business bank statements that show your income and deposits.

Bank statements serve as the primary method lenders use to verify income for self-employed borrowers. If you’re not sure what counts as a bank statement or what lenders review, you can read our full guide on what a bank statement is.

The easiest way to provide bank statements is through Griffin Funding’s secure digital portal. Using industry-leading bank-connection technology, you can instantly and securely sync 12–24 months of statements from nearly all U.S. banks and credit unions with just one click. This eliminates the need for manual uploads and significantly speeds up your loan process.

Alternatively, you can also download your statements directly from your bank’s online portal by logging into your account and navigating to the statements section. And if you can’t find them online, your bank can mail printed copies to you upon request.

When lenders are reviewing your bank statements to determine whether they can approve you for a loan they are looking for the following information:

- Positive account balance

- Little to no overdrafts

- Regular monthly income deposits

- Enough money to cover at least 10% down payment (10% down requires 680 minimum credit score, up to a $1,000,000 loan amount)

- Enough money to cover several months’ worth of mortgage payments as well as closing costs

- When income was deposited into your account (generally, they want the income to be seasoned, meaning it’s been in your account for a while and wasn’t all just deposited right before you applied for your loan)

Eligibility for a bank statement requires total deposits minus disallowed deposits. This amount is then divided by the number of bank statements, whether it is the 12 or 24 months statement.

Another option is that if the co-borrower is a W2 employee you can use a hybrid of W2 and tax return income from the co-borrower and bank statement income from the borrower or assets from the co-borrower and bank statements from the borrower. Non-QM loans can use multiple sources of blended incomes to qualify.

Deposits which are disallowed in regards to a bank statement loan include transfers between bank accounts and cash or large deposits, which can raise a level of concern and may require a letter of explanation.

It can be difficult to find a bank statement loan with a reliable lender. However, since these loans are based on bank statements instead of traditional income verification methods, they often open doors of opportunity for many borrowers who otherwise wouldn’t be able to qualify for a mortgage. As long as you have the bank statements to prove your income and a decent credit score, it otherwise shouldn’t be too difficult to qualify.

When it comes to getting a bank statement loan, the main hurdle is finding the right lender to work with. Our team at Griffin Funding works hard to ensure access to bank statement loans for self-employed workers of all backgrounds and industries. Many gig workers, freelancers, contractors, and other workers rely on these options to afford their homes, and our goal is to help more professionals find the right bank statement loan for their specific needs.

After completing the bank statement mortgage process and closing on the loan, we fund the mortgage and then the escrow or title agent must record the deed with the county recorder’s office. Escrow cannot disburse funds until they receive recording confirmation from the county. Depending on how early in the day the loan is funded and the county where the transaction is taking place, funds will typically be disbursed the same day or the next business day.

As an experienced bank statement lender, Griffin Funding offers a streamlined mortgage process that helps you get to the closing table quickly and get the funds you need.

Note that for certain refinance loans, a 3-day waiting period may be required before the loan is funded. However, this waiting period does not apply to purchase loans.

At Griffin Funding, we strive to complete the bank statement mortgage process and close on the loan in 30 days or less. When taking out a self-employed mortgage such as a bank statement loan, you can generally expect a closing timeline similar to that of a traditional mortgage loan.

In order to ensure the quickest closing time on your bank statement loan, we recommend preparing and organizing all necessary documentation prior to applying. Additionally, once you’ve begun the mortgage process, make sure to be honest with your lender and answer any questions they may have in a timely manner.

Here are a few general steps to take to find the right mortgage lender:

- Check their ratings and reviews: First, you want to determine whether they’re a credible lender you can trust. One of the ways you can do that is by checking their ratings and reviews across several platforms. Do they have good reviews? What are the biggest complaints, if any?

- Feel them out: See what their customer service is like before moving forward with your loan. Do they seem to have your best interest in mind? Are they helpful or are they inattentive?

- Know what questions to ask: Savvy borrowers will ask questions and learn about all the attached fees, requirements, and costs aside from interest rate payments in the principal amount. You want to find the best loan terms before you settle on a bank statement mortgage.

- Proven track record funding bank statement loans: Make sure the lender has the experience and expertise with self-employed borrowers and bank statement loans. Not all bank statement loans are the same; therefore, the lender should have multiple products and programs for all types of bank statement non-QM loans. Choosing a lender that specializes in bank statement loans gives your loan a better chance of closing.

Not all lenders specialize in non-QM products like bank statement loans, and many banks or credit unions have strict overlays that make qualifying harder for self-employed borrowers. Griffin Funding is your trusted partner for flexible and fast bank statement loans. Here’s why:

- Specialized expertise: We are a direct-to-consumer non-QM lender with deep experience helping self-employed borrowers and business owners qualify when traditional lenders say no.

- AI-powered speed: Our AI underwriting platform (“LIA”) — which was featured in HousingWire and earned us a spot on Inc.’s Best in Business 2025 — helps navigate hundreds of pages of investor guidelines instantly, delivering faster approvals and faster closings. Meanwhile, other lenders underwrite their bank statement loans manually.

- Proven track record: With thousands of 5-star reviews on Google, Yelp, and the BBB, we’re recognized for outstanding service and reliability.

- Flexible solutions: Loan amounts up to $4M, as little as 10% down, and multiple qualification paths make us the lender of choice for entrepreneurs and self-employed borrowers nationwide.

- Multiple bank statement programs: Self-employed borrowers often have unique and complex financial situations, which is why we offer three flexible options. Plan A uses a standard expense ratio, Plan B allows your CPA to verify actual expenses (with ratios as low as 10%), and Plan C requires only the first page of your bank statements – designed for the fastest possible qualification, approvals, and closings.

Griffin Funding has been in business since 2013 and has become a leader in non-QM lending by combining innovative programs with cutting-edge technology. Our goal is simple: help you qualify with confidence and close quickly so you can move forward with your goals.

Review the table below to see how bank statement loans compare to other types of self-employed mortgages.

| Bank Statement Loan | 1099 Loan | P&L Loan | Asset-Based Loan | |

| Income Documentation | 12-24 months of bank statements | 1-2 years of 1099 forms | 1+ P&L statements | Proof of liquid assets |

| Best For | Business owners & self-employed borrowers with strong deposits | Independent contractors who receive a 1099 | Established businesses with strong documented revenue | High-net-worth borrowers with liquid assets |

| Employment Type | Self-employed | 1099 contractor | Self-employed business owner | Self-employed or retired |

| Income Calculation Method | Average monthly deposits | Gross 1099 income | Net income from CPA-prepared P&L | Value of qualifying assets is divided by 5, 7, or 10 years (depending on program) |

| Ideal Scenario | Borrower has strong revenue but tax write-offs | Contractor with consistent 1099 income | Business owners who don’t receive a W-2 or pay stubs | Retirees or investors with significant liquid assets but limited reported income |

| Down Payment Requirement | 10%+ | 10%+ | 10%+ | 20%+ |

Refinancing your home loan allows you to turn your home’s equity into cash in some cases. Those with existing mortgage loans may be able to refinance their loan with bank statements with a cash-out refinance or HELOAN.

This option allows you to leverage the equity in your home in exchange for cash, which you can then use to pay off debts or other major expenses. In most cases, borrowers can have a cash-out refinance loan matching up to 80% of the value of their property (or up to 85% with a HELOAN).

Use our free bank statement loan refinance calculator to calculate your monthly savings.

Wondering if it’s time to refinance? There are a few different reasons you may want to refinance your bank statement loan. These include:

- Lower mortgage rates: If current mortgage rates are less than your loan’s mortgage rate, refinancing could earn you a loan with a better interest rate. As a general rule of thumb, experts typically suggest refinancing when interest rates are at least 1% lower than your current interest rates, but remember that this is a general rule. If a slightly lower interest rate could be beneficial to you, it may be worth refinancing.

- Different loan terms: Refinancing your loan also opens you up to different loan terms. If your financial situation has changed and you can afford to pay more each month, you may want to shorten the term of your loan. Alternatively, if you’d like to pay less each month and are comfortable paying over a longer period of time, lengthening the terms of your loan may be right for you.

- Changing listed borrowers: Refinancing also allows you to change the borrowers listed on your loan. You may choose to remove a borrower from your loan or add a new borrower. These can be achieved through refinancing.

- Different loan type: Refinancing allows you to change the type of loan you have. Through refinancing, you can switch between an adjustable-rate mortgage or a fixed-rate mortgage.

- Cash-out refinancing: Cash-out refinancing is a way to draw on your home’s equity to obtain cash. In these cases, you’ll take out a new loan and use it to pay off your old loan. Then, you can use the remaining balance for cash.

Yes, you can refinance from a bank statement loan into a conventional mortgage. This can be an option if your career or financial circumstances change and you’re able to use your tax returns to qualify for a conventional mortgage.