DSCR Loans: Qualify on Rental Income, Not Tax Returns

No minimum DSCR requirement. Loans from $100K to $4.5M. Close in as few as 6 days. Last updated: August 2026

- $4.5M Max loan amount

- 15% Minimum down payment

- No min DSCR required, no‑ratio available

- 6 days Fastest closing

DSCR Loans in August 2026: What Real Estate Investors Need to Know

Written and reviewed by Bill Lyons, President and CEO of Griffin Funding.

A DSCR loan qualifies real estate investors on a property’s rental income instead of tax returns, W2s, or DTI. The debt service coverage ratio equals gross monthly rent divided by PITIA (principal, interest, taxes, insurance, HOA). A 1.0 ratio means the rent covers the payment, and most lenders require 1.25. Griffin Funding has no minimum DSCR requirement, with no-ratio programs that do not use cash flow to qualify at all.

DSCR loan rates in August 2026: 1-year ARMs start at 5.375%, while 30-year fixed, 40-year fixed, and 5-year ARM options start at 6.375%, based on credit score, DSCR ratio, down payment, buydown points, and prepayment penalty term (0 to 5 years), with sharpened pricing on jumbo DSCR loans up to $4.5M. With conventional rates pushing toward 7% and no Fed meeting until September, investors are locking DSCR terms rather than waiting on a cut. View today’s DSCR loan rates →

In July 2026, our most recent closed month, Griffin Funding funded 71 DSCR loans, including DSCR HELOCs and first mortgages, totaling $19.5 million. Loans averaged $274,515 with a high of $1,351,000, and coverage ratios ranged from 0.70 to 2.23, including two loans that qualified below a 1.0 DSCR. 72% were cash-out refinances (investors pulling equity to buy the next property), 21% were purchases, and 7% were rate-and-term refinances. Wondering where investors are deploying that capital? See our most landlord-friendly states index and the top 50 metros for DSCR investors further down this page.

DSCR loans account for 40% of Griffin Funding’s total funded volume in 2026, making us one of the most active DSCR lenders in the country. We close DSCR loans in as few as 6 days, with an average closing time of 34 days. Most DSCR lenders operate without licensing because these are business-purpose investment loans. As a national mortgage lender licensed in 47 states plus D.C., regulated by the CFPB, and approved by HUD as an FHA Non-Supervised Lender, we bring institutional accountability and transparent pricing to your portfolio. Rates are subject to change daily based on market conditions. Updated 8/1/2026.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformWhat Is a DSCR Loan?

A DSCR loan is a mortgage for rental properties that qualifies you based on the property’s income instead of your own. The debt service coverage ratio equals gross monthly rent divided by PITIA, which is principal, interest, taxes, insurance, and HOA dues (if applicable). A ratio of 1.0 means the rent covers the full payment.

Most lenders require a 1.25 ratio. Griffin Funding has no minimum DSCR requirement. We fund loans with ratios below 1.0 when reserves support the deal, and our no-ratio program does not use cash flow to qualify at all. In July 2026 alone, we closed loans with coverage ratios from 0.70 to 2.23, including two below 1.0.

No tax returns. No W2s. No DTI calculation. No limit on the number of financed properties. Borrow as an individual or through your LLC, and title can be held in a partnership, corporation, S corp, or revocable trust depending on the program.

Key features of DSCR loans include:

- No income or employment verification

- Qualify based on rental property cash flow (DSCR)

- Only for income-generating investment properties

- Flexible qualification requirements

- Fast approval process

DSCR Loan Requirements

Property type

Rental properties only. Not for primary residences.

DSCR

≥ 1.0 ideal; < 1.0 allowed with extra reserves.

Down payment

Qualify with down payment as low as 15%.

Credit score

620+ minimum. Griffin borrowers averaged 739 in 2025.

Loan amount

$100K–$4.5M depending on property value.

Appraisal

Required for value + rental income verification.

DSCR Rates

Today’s DSCR Loan Rates

See today’s DSCR loan rates for your next investment purchase or refinance.

1-year ARMs start at 5.375%. 30-year fixed, 40-year fixed, and 5-year ARM options start at 6.375%.

“When I advise real estate investors on DSCR loans, the first step is comparing the payment difference between an interest rate with no points versus a lower rate with points. Recently, I worked with a borrower who could save $190 per month by buying down the rate. But since their plan was to refinance in four to five years and use equity to purchase another property, they chose the higher rate with no points. That strategy kept more cash in their pocket today, while rental income still covered the mortgage. By waiting to refinance when rates are lower, they’ll preserve liquidity now and use future equity to keep building their portfolio.”

Adam Ruvelson, Branch Manager, NMLS# 1283827

Loan Options

DSCR Loan Types We Offer

Traditional DSCR Loan Programs

The DSCR purchase loan is the best option for real estate investors buying a new rental property, allowing them to qualify based on the property’s expected rental income rather than personal income, W-2s, or tax returns.

Cash-Out Refinance. No seasoning required. Pull equity up to 80% LTV and redeploy it into your next acquisition.

The DSCR rate and term refinance is the best option for investors transitioning out of high-rate hard money or bridge financing into a stable, long-term mortgage, or for those looking to lower their rate or extend their term to improve monthly cash flow.

The DSCR HELOAN is the best option for investors who want to tap equity in an existing rental property without touching their first mortgage, qualifying on rental income rather than personal income while keeping the existing first lien rate in place.

Unique DSCR Loan Programs

The DSCR no-ratio loan is the best option for investors purchasing properties in high-value, low-yield markets where rents do not cover PITIA at standard thresholds.

- Secure financing with DSCR below 1.0

- Down payment as low as 25%

- 700+ FICO

- Loan amount up to $1 million

- Cash-out as high as 75%

The 15% down DSCR loan is the best option for high-credit investors who want to maximize leverage and preserve capital across multiple acquisitions.

- Only 15% down payment required

- 740+ FICO

- Loan amount up to $1 million

The rental income plus assets program is the best option for high-net-worth investors whose rental income alone falls just short of standard DSCR thresholds, allowing them to blend verified liquid assets with property income to strengthen qualification and increase borrowing power without pledging those assets as collateral.

The six-month and 1-year SOFR ARM DSCR loan is the best option for investors with a short-to-medium-term hold strategy who want the lowest available starting rate, offering fully amortized or interest-only adjustable-rate financing tied to SOFR with rates starting as low as 5.125%.

“Between the creative financing options we offer, our ability to make some exceptions, and the flexible solutions we provide, we demonstrate a deep expertise when it comes to non-QM loans while providing personalized service and a commitment to the client’s success. Our long-term relationships with clients are built on trust and the mutual success of them closing on a loan. This leads to our clients having a little bit more financial freedom or being able to move into their dream home, where their kids all get a bedroom. So we are always dedicated to helping these clients achieve those financial objectives.”

Colby Freer, Senior Mortgage Consultant with 10 years of experience at Griffin Funding, NMLS# 1319705

Pros and Cons of DSCR Loans

Pros

- No tax returns or W2s

- No employment verification

- Streamlined application

- Loan amounts to $4.5M

- Cash-out up to 80% LTV

- Interest-only options available

- Short-term rentals eligible

- Borrow through an LLC

Cons

- Larger down payments than owner-occupied loans

- Rates can run higher, though LLPAs have narrowed the gap

- Loan size tied to the property’s cash flow

- Rental properties only

- Most carry prepayment penalties

- No fixer-uppers

- Unique and rural properties can be harder to finance

DSCR loans trade documentation for structure. You skip tax returns, W2s, and employment verification, and in exchange the property has to carry the deal: it must be rent-ready, the loan size follows the cash flow, and most programs carry a prepayment penalty. None of the cons are dealbreakers if you know them going in, and two of them deserve a closer look before you sign with any lender.

The first is disclosure. DSCR loans are business-purpose loans, not qualified mortgages, so federal TRID disclosure rules don’t apply, and some lenders use that gap to leave terms vague until closing. The document format matters less than what’s in it and when you get it. At Griffin Funding, you see the interest rate, points, fees, and any prepayment penalty in writing upfront, whether your file uses a loan estimate or a term sheet, and if anything changes during the process, we disclose it in advance. No surprises at the closing table, and no prepayment penalty options are available if you want maximum flexibility.

“You need to make sure you figure out what kind of prepayment penalty is being put on the loan because, in many cases, that’s not disclosed. DSCR loans don’t follow federal disclosure guidelines, so a lender technically doesn’t need to disclose anything at all until the end. We do the opposite: your rate, fees, and prepayment penalty are in writing upfront, and we vet the numbers against the rental income, so the loan has a much higher chance of closing where it starts rather than changing along the way.”

Guy Troxler, Senior Loan Officer with 7 years of experience in the mortgage industry, NMLS# 1642169

The second is the appraisal. A low valuation on the property or the market rent is the most common reason DSCR deals wobble, so have a plan B agreed with your loan officer upfront, usually a larger down payment, and check our free home value estimator and our free rent estimator before the appraisal is ordered.

For the full breakdown of every advantage and tradeoff, see our complete guide to DSCR loan pros and cons.

Calculators

DSCR Loan Calculators

Use these tools to estimate your DSCR for a new purchase or refinance.

Where We Lend

Where We Offer DSCR Loans

Griffin Funding originates DSCR (Debt Service Coverage Ratio) loans for rental and investment properties in all 50 states and Washington, D.C. Open the list below for local DSCR loan requirements, qualifying rents, and rate guidance from a lender licensed in your market.

Don’t see your state? Griffin Funding lends nationwide. Request a quick quote and a licensed loan officer will confirm DSCR availability in your area.

America's Top DSCR Markets

Using the same methodology as our state-by-state market tables, we ranked the 50 largest U.S. metros by Example DSCR at a hypothetical 20% down. The spread is wide: rentals in New Orleans pencil at 1.17 while San Jose sits at 0.43, and seven of the ten strongest DSCR markets in America are in states where Griffin Funding has published a full market breakdown.

“Great team to work with from application through closing and afterwards for follow up needs. Very fast turnaround on rental property cash out mortgage. Have used them twice for this product and will again if I need to. Highly recommend for rental real estate investors!”

Sara J.

FAQ

Frequently Asked Questions

A DSCR of 1.0 means the rent exactly covers the monthly payment, and most lenders want 1.25 or higher. As a rule of thumb: 1.25 and up earns the best pricing, 1.00 to 1.24 is excellent, 0.75 to 0.99 still qualifies with us, and below 0.75 we can look at reserves-based or no-ratio options. At Griffin Funding, there is no minimum ratio, so a weak number narrows your options and pricing but doesn’t end the conversation.

Our minimum is 620. Higher scores unlock better rates and lower down payments, including 15% down at 740 and above. For context, our funded DSCR borrowers in 2025 averaged a 739 score, so a mid-600s investor is well inside our credit box even if other lenders have said no.

As low as 15% with 740+ credit, and 20% is typical. A larger down payment improves your DSCR because it lowers the monthly payment the rent has to cover, which can also improve your rate. On a cash-out refinance there is no down payment; your equity does that job.

Not much anymore. Conventional loans on investment properties carry agency loan-level price adjustments that typically add 0.5% to 0.75% over the owner-occupied rates you see advertised, which puts conventional investor pricing in the same range as DSCR. The difference is what you have to hand over to qualify: a conventional investor loan still requires tax returns, W2s, and a DTI calculation. Your exact rate depends on credit score, DSCR, down payment, points, and prepayment penalty term. See how LLPAs affect your rate.

Yes. A ratio below 1.0 means the rent doesn’t fully cover the payment, and most lenders decline those files. We approve them when reserves and down-payment support the deal, and our no-ratio program doesn’t use cash flow to qualify at all.

Yes. You can borrow through a U.S. LLC with a personal guarantee, and the loan generally won’t report to consumer credit bureaus.

“DSCR loans are great financing alternatives to have borrowers build wealth along with their portfolio without showing any personal income to qualify. We don’t even verify if you have a job or not; we look solely at the property to see if the rent covers the payment. Another reason to take advantage of the DSCR loan is you can close in an LLC, which keeps the mortgage off your personal credit report.”

Cody Unger, Branch Manager, NMLS# 1295308

Title can also be vested in a partnership, corporation, S corp, or revocable trust, depending on the program. To keep your closing fast, have your articles of organization, operating agreement, EIN letter, and certificate of good standing ready when you apply.

Most do, typically 1 to 5 years, and the term you choose affects your rate: a longer penalty period means a lower rate, and buying the penalty out means a higher one. We disclose yours in writing upfront, which many unlicensed DSCR lenders won’t do. Planning to sell or refinance soon? Tell your loan officer so the structure fits. Here’s how prepayment penalties work in detail.

Griffin Funding’s fastest DSCR closing is 6 days, and the average is 34 days. No tax returns, W2s, or employment verification means less paperwork in underwriting. Pacing depends on the appraisal, title work, and borrower responsiveness, including having entity documents ready if closing in an LLC.

Generally no. DSCR loans closed through an entity aren’t reported to consumer credit bureaus, so they don’t add tradelines or payment history to your report. Two caveats: a personally guaranteed loan can still be considered when you apply for other financing, since applications ask about real estate owned and guaranteed debt. And if the loan defaults, the personal guarantee means collection activity can reach your personal credit and the default will follow you in future lending decisions. Off your report doesn’t mean off the hook.

While DSCR loans can be a helpful financing option for many real estate investors, there are certain scenarios in which using a DSCR loan may not be ideal. Here are some cases where a DSCR loan may not be the best choice:

- You’re buying a primary residence

- You want to purchase a distressed property

- You’re interested in a fix-and-flip project

- You’re purchasing a property worth less than $100,000

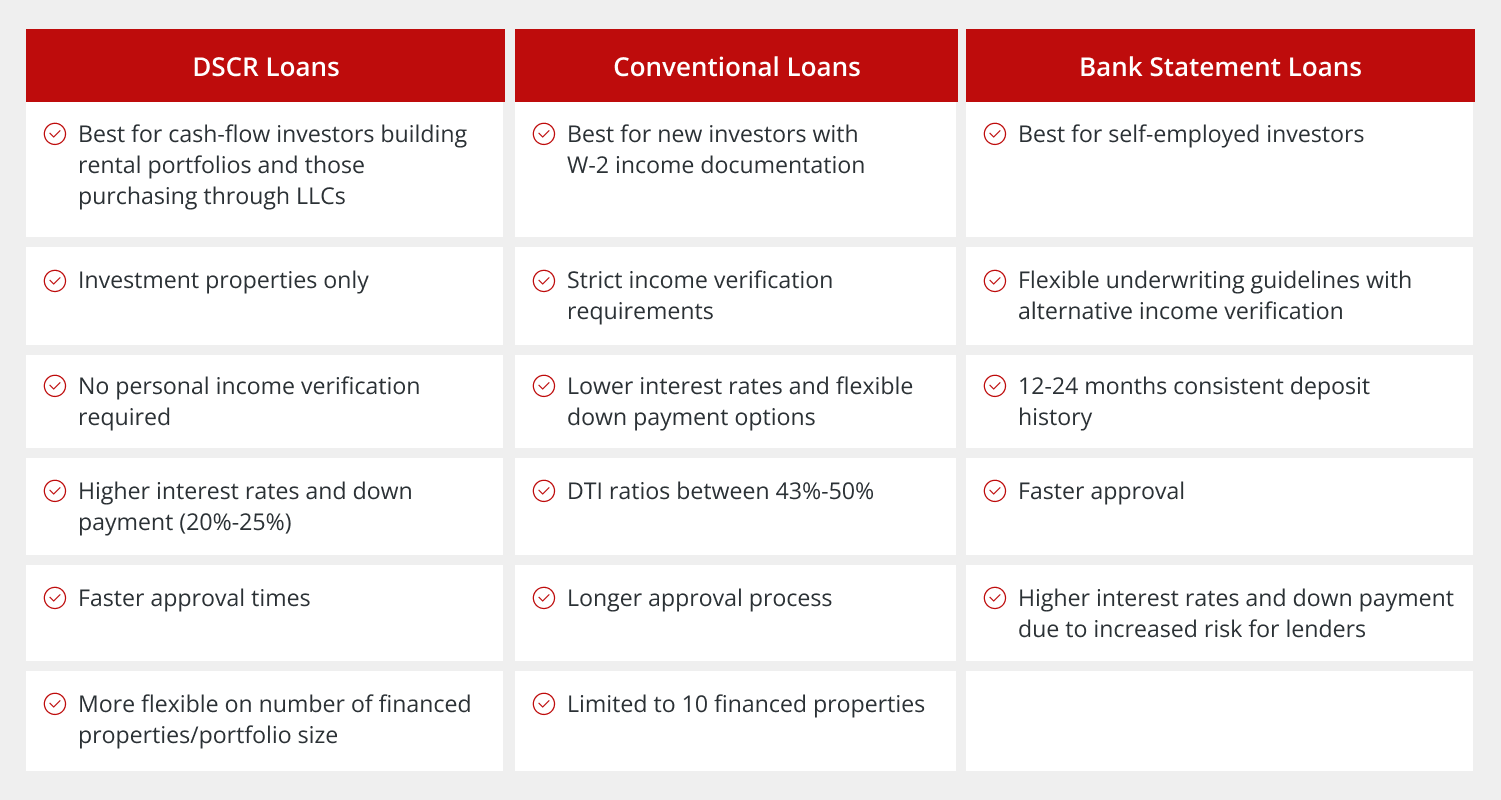

DSCR loans are designed specifically for real estate investors, and can be a great mortgage solution whether you’re a seasoned investor or you’re buying your first rental property. Review this comparison table below and read our blog about how DSCR loans differ from other investor mortgage products:

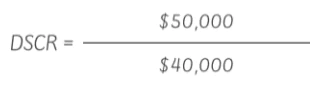

A real estate investor might be looking at a property with a gross rental income of $50,000 and an annual debt of $40,000. When you divide $50,000 by $40,000, you get a DSCR of 1.25, which means that the property generates 25% more income than what is necessary to repay the loan. This also means that there is a positive cash flow in the lender’s eye.

Real estate investors scaling a rental portfolio typically use one or more of the following financing strategies:

- DSCR loans: The most widely used vehicle for portfolio scaling. DSCR loans qualify based on each property’s rental income, not personal income or DTI. Because each property qualifies independently, investors can add properties without their personal debt load affecting approval. Griffin Funding imposes no limit on the number of DSCR-financed properties.

- Cash-out DSCR refinances: Once a property has built equity, investors extract that equity through a DSCR cash-out refinance—no seasoning period required, unlimited cash-out available at Griffin Funding—and use the proceeds to fund the next acquisition.

- BRRRR strategy: Buy, Rehab, Rent, Refinance, Repeat. Investors acquire a distressed property with short-term bridge financing, renovate it, lease it, then refinance into a long-term DSCR loan to recycle capital into the next deal.

- Conventional investment loans: Fannie Mae and Freddie Mac investment property loans are available up to 6–10 financed properties per borrower. Once that limit is reached, DSCR loans become the primary scaling vehicle.

- Portfolio loans: Blanket loans consolidating multiple properties under one note. Griffin Funding structures DSCR loans on a property-by-property basis, which gives investors more flexibility to sell or refinance individual assets without affecting the rest of the portfolio.

DSCR loans are the best financing option for Airbnb and short-term rental (STR) properties because they qualify based on a property’s projected or actual rental income rather than the borrower’s personal income, W-2s, or tax returns.

Griffin Funding calculates STR qualifying income using either a.) an appraiser’s income estimate, called a short-term rental narrative, b.) 12 month history of actual rental income from the existing property, or c.) AirDNA historical platform data.

Griffin Funding offers DSCR loans for STR properties across all 50 states with a minimum 640 credit score, minimum 0.75 DSCR, and as little as 15% down.

The best place is with a lender who specializes in DSCR loans, like Griffin Funding. You’ll benefit from competitive rates, flexible terms, and a team that understands how to tailor financing to your investment strategy.

Griffin Funding is one of the top direct-to-consumer DSCR lenders in the United States, helping real estate investors access non-traditional mortgage solutions nationwide. Founded in 2013, Griffin has grown into a trusted leader in DSCR loans, specializing in helping clients qualify based on rental income and property cash flow, not tax returns or W-2s.

Here’s why you should choose Griffin Funding as your DSCR mortgage lender:

- Excellent customer reviews: We’re backed by an A+ BBB rating and thousands of 5-star reviews across Google, Yelp, and the BBB.

- Nationwide DSCR lender: Griffin Funding is proud to serve investors in all 50 states with transparent terms, expert guidance, and exceptional client service.

- Innovative AI-driven underwriting platform: Our proprietary Loan Intelligence Assistant (LIA), recently featured by HousingWire, uses AI-driven underwriting to streamline the approval process, reduce manual errors, and fund loans faster. We’ve closed DSCR loans in as few as six days, with an average closing time of 34 days.

- Direct-to-consumer advantage: Griffin Funding is a consumer-direct mortgage lender, which means you can access flexible terms without dealing with any middleman.

- Easy-to-use digital tools: Our digital mortgage platform, Griffin Gold app, and free interactive financial calculators all serve to make the borrowing experience smoother and easier to understand.

- Institutional Security for Business-Purpose Financing

Because Debt Service Coverage Ratio (DSCR) loans are business-purpose loans for investment properties, the vast majority of DSCR brokers and lenders choose to operate completely unlicensed. Griffin Funding is different. We back our non-QM and DSCR investor programs with full institutional credentials. We are licensed in 47 states and D.C., federally overseen by the CFPB, and trusted as a HUD-approved FHA Non-Supervised Lender—giving you the peace of mind that your investment capital is backed by an established, fully compliant national lender.

“Our mission is to empower real estate investors to grow wealth through smarter financing by combining technology, transparency, and a client-first approach,” says Bill Lyons, CEO of Griffin Funding.

Whether you’re buying your first rental or expanding a multimillion-dollar portfolio, our team of experienced mortgage advisors is here to help you structure the DSCR loan that fits your investment strategy and goals.

Yes. We qualify short-term rentals using market rent from the appraisal, documented rental history, or AirDNA-style market data, depending on the program. Short-term rental files carry their own requirements, including coverage minimums and LTV limits that differ from long-term rentals, and your market must permit STR use, so bring your revenue history and your loan officer will match you to the right program. Long-term, mid-term, and short-term strategies are all eligible. Details in our guide to DSCR loans for Airbnb properties.

Your DSCR directly impacts loan approval, interest rates, and terms. A higher ratio shows lenders that your rental income covers debt easily, which can lead to better rates. A lower ratio may limit options or increase costs.

Some lenders offer temporary rate buydowns on DSCR loans. This option lowers your initial interest rate, making early payments more manageable. Griffin Funding can help you explore whether a rate buydown fits your investment strategy.

DSCR loans are widely available, but not every lender operates in all states. Griffin Funding offers DSCR loans in all 50 states and the District of Columbia.

Technically, no. Because DSCR mortgages are designated as business-purpose loans for residential investment properties rather than primary residences, most DSCR brokers and lenders are completely exempt from standard licensing rules in most states. However, Griffin Funding believes real estate investors deserve the same protections as traditional homebuyers. Unlike unregulated boutique brokers, we maintain active mortgage lender licenses across 46 states and D.C., strictly adhere to federal CFPB guidelines, and hold official HUD approval as an FHA Non-Supervised Lender.

The most important factors to evaluate when choosing a DSCR lender are:

- Minimum DSCR flexibility: Most lenders require a DSCR of 1.0–1.25. Griffin Funding qualifies down to 0.75 and offers no-ratio programs where the property’s cash flow isn’t used to qualify at all.

- Down payment requirements: Standard DSCR loans require 20–25% down. Griffin Funding allows as little as 15% for borrowers with 740+ FICO.

- Direct lender vs. broker: A direct lender originates, underwrites, and funds loans in-house. DSCR brokers add a middleman layer that can extend timelines and add fees without adding expertise.

- Licensing and regulation: Because DSCR loans are business-purpose loans, most DSCR brokers and lenders are not required to hold mortgage licenses. Griffin Funding maintains active licenses in 47 states and D.C., is federally regulated by the CFPB, and holds HUD approval as an FHA Non-Supervised Lender.

- Closing speed: Active real estate investors often need to move quickly on deals. Griffin Funding has closed DSCR loans in as few as 6 calendar days, with an average closing time of 34 days.

- LLC titling: Confirm the lender allows closing in an LLC to protect personal assets and keep loans off personal credit reports. Griffin Funding permits LLC and trust titling on all DSCR programs.

- Jumbo DSCR availability: If you’re investing in high-value markets, confirm the lender can fund large loans. Griffin Funding funds DSCR loans up to $4.5 million in-house, with case-by-case exceptions to $20 million.

- Nationwide reach: If you’re scaling across multiple states, work with a lender licensed in every market. Griffin Funding originates DSCR loans in all 50 states and Washington, D.C.