What Is a DSCR Loan? Complete Investor’s Guide (2026)

A DSCR loan allows real estate investors to secure financing based on the rental income of a property rather than their personal income. If you cannot qualify for a conventional loan, DSCR loans are a great option. Without having to submit tax returns and W-2s, you can secure capital to invest in rental properties with a DSCR loan. Answer a few quick questions to get started on your journey in investing in rental property with a DSCR loan today.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformTable of Contents

Unlock real estate financing with DSCR loans — a type of non-traditional mortgage loan designed for real estate investors who want to qualify based on a property’s cash flow, not personal income. Qualifying using a property’s actual or projected rental income rather than tax returns, can help you avoid common barriers associated with traditional mortgages, such as rigid debt-to-income limits, excessive documentation, and personal income verification.

Securing a DSCR loan can help you expand your investment property portfolio more easily than ever. As a real estate investor, you can avoid the high rates and strict lending criteria of private loans with this flexible non-traditional mortgage option. Read on to learn what a DSCR loan is, how it works, and key DSCR loan requirements.

KEY TAKEAWAYS

- The debt service coverage ratio (DSCR) is a number that measures a property’s current rental income compared to its debt obligations. A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow.

- A DSCR above 1.0 indicates positive cash flow, while a DSCR below 1.0 indicates negative cash flow.

- A DSCR loan allows a borrower to qualify for financing based on the projected rental income of a property rather than personal income.

- DSCR loans are designed for real estate investors and can only be used to purchase income-generating properties. DSCR loans can’t be used to buy a primary residence or a fixer-upper.

Think you qualify for a loan? Contact us today to find out!

Contact UsWhat Is the Debt Service Coverage Ratio (DSCR)?

The debt service coverage ratio measures a property’s annual gross rental income against its annual mortgage debt, including principal, interest, taxes, insurance, and HOA (if applicable). Lenders use DSCR to assess loan affordability based on cash flow.

When calculating DSCR, lenders do not take into account expenses such as:

- Management

- Maintenance

- Utilities

- Vacancy rate

- Repairs

How to Calculate DSCR

To calculate your debt service coverage ratio, follow the steps below:

Step 1

- To find your gross rental income, we take your annual rental income based on your lease agreement and the appraiser’s comparable rent schedule (form 1007) and use the lesser of the two.

- In some cases, if you can prove a two- to three-month history of long term rental income, you can qualify off that rather than the appraiser’s market rent.

Step 2

- Next, you’ll need to find your annual debt. For DSCR loan qualification purposes, your annual debt equals the total annual principal, interest, taxes, insurance, and HOA (if applicable) payments.

- Annual Debt = Total Annual PITIA payments.

Step 3

- Next, you’ll divide your annual gross rental income by your annual debt for your ratio.

- DSCR = Annual gross rental income/Annual debt.

Please note that net operating income (NOI), capitalization rate (Cap Rate), cash on cash return (COCR), and return on investment (ROI) are not considered for DSCR mortgage loan qualifying purposes.

Example of Debt Service Coverage Ratio Calculation

A real estate investor might be looking at a property with a gross rental income of $50,000 and an annual debt of $40,000. When you divide $50,000 by $40,000, you get a DSCR of 1.25, which means that the property generates 25% more income than what is necessary to repay the loan. This also means that there is a positive cash flow in the lender’s eye.

How to Improve Your DSCR

Here’s how you can optimize your DSCR to make yourself more qualified when applying:

1. Increase rental income:

Boost your rental income by optimizing your property’s occupancy rates, increasing rental rates in line with market trends, or offering additional services or amenities to attract more tenants. Minimize vacancies by implementing effective marketing strategies, maintaining properties in good condition to attract and retain tenants, and quickly addressing tenant concerns or issues.

2. Refinance existing loans:

Explore opportunities to refinance existing loans at lower interest rates with longer repayment terms and consider adding an interest-only feature. Refinancing your existing mortgage can reduce your monthly debt service obligations and improve your DSCR.

3. Increase property value:

Invest in property upgrades or renovations to increase its market value, allowing you to command higher rental rates and improve your overall financial position. Upgrades can also help attract tenants, helping you increase your rental income by reducing vacancies.

4. Manage your expenses:

Implement cost-saving measures like energy-efficient upgrades, outsourcing maintenance services, or renegotiating vendor contracts to reduce operating expenses. The lender does not consider these expenses when calculating your DSCR, but this will help you improve your overall cash flow.

“DSCR loans are great financing alternatives to have borrowers build wealth along with their portfolio without showing any personal income to qualify. We don’t even verify if you have a job or not; we look solely at the property to see if the rent covers the payment. Another reason to take advantage of the DSCR loan is you can put them in LLCs, this will keep all your mortgage debt liability away from your personal credit, so when you need to personally qualify for a loan, there won’t be a mortgage to show, it will be completely separate and off your credit report!”

Cody Unger, Branch Manager

Think you qualify for a loan? Contact us today to find out!

Get StartedWhat Is a DSCR Loan?

A DSCR loan is a type of non-qualified mortgage (non-QM) loan designed specifically for real estate investors. Rather than using tax returns or pay stubs to qualify, lenders assess your eligibility based on the real or potential cash flow of the property.

This is an ideal mortgage solution for real estate investors who may claim significant tax write-offs that lower their personal taxable income, or who otherwise are unable to qualify for traditional home financing.

Key features of DSCR loans include:

- No income or employment verification

- Qualify based on rental property cash flow (DSCR)

- Only for income-generating investment properties

- Flexible qualification requirements

- Fast approval process

Using a DSCR Loan in 2025

DSCR loans offer a convenient pathway for real estate investors looking to start or expand their investment portfolio in 2025. Here’s a glimpse of what the real estate investment looks like in 2025:

- Real estate investors are continuing to seize opportunities in the U.S. housing market. Investor purchases accounted for 33% of all single-family homes sold in Q2 2025, according to the BatchData Q2 2025 Investor Pulse Report.

- This surge occurred just before the passage of the One Big Beautiful Bill (OBBBB) on July 4, 2025, which reinstated 100% bonus depreciation for real estate investors, a tax incentive expected to further fuel investor demand in the months ahead.

- As 2025 unfolds, the outlook remains bright in select markets, with emerging trends and strategic opportunities paving the way for growth and success. However, securing the right type of mortgage financing is not always easy for real estate investors.

When it comes to non-QM mortgages, DSCR loans are one of the most popular options among all borrowers. In fact, debt service coverage ratio (DSCR) loans remain a leading segment in non-QM:

- S&P Global Ratings notes DSCR loans made up roughly half (by balance) of the collateral in non-QM securitizations S&P rated from July 2022 through July 2024, underscoring sustained investor demand.

- As of July 2025 DSCR loans accounted for ~28.7% of non-QM originations by volume, second only to bank-statement loans, showing the product’s continued popularity with real-estate investors even in today’s rate environment.

Think you qualify for a loan? Contact us today to find out!

Get StartedHow Does a DSCR Loan Work?

Here’s how a DSCR loan works:

- Determine property income: The lender works with the borrower to determine the property’s gross monthly rental income. Rental income can be determined by either examining an existing lease or reviewing an appraiser’s comparable rent schedule. You can use our free rent estimator tool in the meantime to get an idea of what you might be able to rent the property for.

- Account for monthly expenses: The lender will tally up your monthly debt obligations associated with the property, which include principal, interest, taxes, insurance, and HOA fees (PITIA).

- Calculate DSCR: Using your monthly income and debt obligations, the lender can calculate DSCR. A DSCR above 1.0 indicates that a property earns enough to cover the mortgage, while a negative DSCR indicates that it does not.

- Loan approval based on DSCR: A lending decision for a DSCR loan is made based on the borrower’s DSCR and broader financial profile, as well as property details. No income documentation or tax returns are required.

DSCR loans can be a great tool for capitalizing on new real estate investment opportunities. They offer flexibility that allows borrowers to purchase different types of properties for various purposes, such as long-term rentals or short-term vacation rentals.

Some of the property types you can use a DSCR loan for include:

- Single Family Residences (SFR), including single-family homes, condos, and townhomes.

- Multifamily properties (2-10 Units).

- Rural (acreage limitations apply, and the property’s income must be supported by comparable rents in the area).

If you’re interested in purchasing or building a property and unsure about whether you can use a DSCR loan to do so, reach out to Griffin Funding. We can help you decide whether a DSCR loan is right for you.

Types of DSCR Loans

We offer the following types of DSCR loans:

- DSCR Purchase Loans: New and experienced real estate investors can use a DSCR purchase loan to buy a rental property with no proof of income needed. Start or expand your real estate portfolio by applying for a DSCR purchase loan, which allows you to qualify using a property’s rental income. We can fund DSCR loans for borrowers with a DSCR of less than 1.0 and a credit score as low as 620.

- DSCR Home Equity Loans: Tap into the equity of your investment property with a DSCR home equity loan (HELOAN). This investor-focused mortgage solution makes it possible for real estate investors to access their equity without touching their first mortgage. Access up to $500,000 in financing and qualify with a DSCR as low as 1.0. Keep in mind that while DSCR HELOANs allow you to avoid touching your first mortgage, DSCR cash-out refinance loans offer higher loan amounts, lower rates, and more flexible qualifying requirements.

- DSCR Cash-Out Refinance Loans: A DSCR cash-out refinance lets real estate investors leverage the equity in the investment properties to access capital for business purposes. You can use these funds to buy more rentals, renovate existing properties, or expand your investment portfolio — however, funds cannot be used for personal expenses. This strategy, known as the Property Multiplier Effect, helps grow wealth and maintain liquidity. Qualified borrowers can access up to 80% of their property’s appraised value and may qualify with a DSCR below 1.0, depending on credit and property performance.

- DSCR Rate and Term Refinance Loans: A DSCR rate and term refinance loan helps real estate investors improve their financing terms without taking cash out of their property. With this type of refinance, you can lower your interest rate, shorten your loan term, or replace an existing hard money loan – all while qualifying based on your property’s rental income instead of personal income or tax returns. This makes DSCR rate and term refinances an ideal solution for investors looking to transition out of short-term or high-cost hard money financing into a long-term, stable mortgage.

- 6-MO SOFR DSCR Loans: A 6-month SOFR DSCR loan is an adjustable-rate mortgage (ARM) that starts at an initial rate and then adjusts every six months based on the 30-day average Secured Overnight Financing Rate (SOFR) index. This program is ideal for real estate investors who prefer a flexible, market-responsive rate. While fixed-rate DSCR loans provide stability, their interest rates are typically higher than the introductory rates available on SOFR-based ARMs.

Why Does DSCR Matter?

The debt service coverage ratio provides the lender with a metric that helps them gauge a borrower’s ability to pay off their DSCR mortgage. Lenders must forecast how much a real estate property can rent for so that they can predict a property’s rental value.

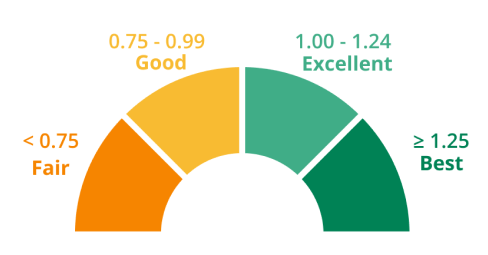

What Is a Good DSCR Ratio?

Many lenders will require a 1.25 DSCR to qualify for a DSCR mortgage loan. However, Griffin Funding allows real estate investors to qualify for a loan with a DSCR of less than 1.00.

Please note that borrowers with a good DSCR ratio can secure more beneficial rates and terms on their loans with fewer requirements. Interest rates are best on DSCR ratios of 1.25 or above, while a DSCR ratio of less than .75 requires more down payment/equity and more reserves to offset the negative cash flow.

If you have a DSCR of less than 1.0, it means that a property has the potential for negative cash flow. DSCR loans can still be made on properties with a ratio below 1.0; however, these are usually purchase loans with home improvements, upgrades, or remodeling that will increase the monthly rent or for homes with high equity and potential for higher rents in the future.

You can also potentially get the property above a 1.0 ratio with a DSCR interest-only loan and/or a 40-year term to maximize cash flow.

Keep in mind that for DSCR loans that we fund, the average property has a DSCR of 1.05.

Think you qualify for a loan? Contact us today to find out!

Get StartedDSCR Loan Requirements

Below are some of the basic requirements one must meet to qualify for a DSCR loan:

- Property type: DSCR loans can only be used for investment properties that generate rental income. The property you are purchasing or refinancing must be a non-owner-occupied, income-producing investment property used for business purposes. DSCR loans cannot be used on primary residences.

- DSCR: Keeping a DSCR above 1 typically reduces equity and reserve requirements; however, it’s still possible to get a loan with a DSCR below 1 with additional reserves, higher down payments, and strong compensating factors.

- Minimum credit score of 620: Borrowers’ credit histories and financial stability are evaluated, although credit requirements can vary depending on the lender and specific loan terms. Year to date in 2025 (as of 10/13/25), borrowers who take out a DSCR loan with Griffin Funding have an average credit score of 739, but we can work with borrowers with credit scores as low as 620.

- Minimum loan amount of $100,000: DSCR loans offer loan amounts ranging from $100,000 to $20,000,000, providing a flexible financing option for properties that range in cost.

- Appraisal: An appraisal is conducted to determine the property’s current market value and rental income.

This matrix shows the minimum DSCR, PITI reserve requirements, credit score, and down payments required for different loan amounts.

DSCR Purchase Loan Qualification Requirements

Matrix of DSCR loan requirements for cash-out refinances by loan amount, DSCR band, PITI reserves, minimum credit score, and maximum loan-to-value (LTV).

| Loan Amount | DSCR | PITI Reserves | Minimum Credit Score | Down Payment |

|---|---|---|---|---|

| < $1.5 million | > 1 | 0–6 months | 720+ | 15% |

| 680+ | 20% | |||

| 640+ | 25% | |||

| 620+ | 50% | |||

| < 1 | 2–9 months | 720+ | 20% | |

| 700+ | 25% | |||

| 680+ | 30% | |||

| 660+ | 35% | |||

| $1.5 – $2 million | > 1 | 2–9 months | 700+ | 20% |

| 680+ | 25% | |||

| 660+ | 30% | |||

| 640+ | 35% | |||

| < 1 | 2–9 months | 700+ | 30% | |

| 680+ | 35% | |||

| $2 – $3 million | > 1 | 6–12 months | 700+ | 30% |

| 660+ | 35% | |||

| 640+ | 40% | |||

| < 1 | 6–12 months | 700+ | 35% | |

| 680+ | 40% | |||

| $3 – $4 million | > 1 | 12 months | 720+ | 40% |

| < 1 | 12 months | n/a | n/a |

DSCR Loan Qualification Guide for Refinancing Investment Properties

Matrix of DSCR loan requirements for cash-out refinances by loan amount, DSCR band, PITI reserves, minimum credit score, and maximum loan-to-value (LTV).

| Loan Amount | DSCR | PITI Reserves | Minimum Credit Score | Max LTV |

|---|---|---|---|---|

| < $1.5 million | > 1 | 0-6 months | 720+ | 80% |

| 680+ | 75% | |||

| 640+ | 70% | |||

| < 1 | 2-9 months | 700+ | 70% | |

| 680+ | 65% | |||

| $1.5 – 2 million | > 1 | 2-9 months | 680+ | 75% |

| 660+ | 70% | |||

| < 1 | 2-9 months | 700+ | 65% | |

| 680+ | 55% | |||

| $2 – 3 million | > 1 | 6-12 months | 700+ | 65% |

| 680+ | 60% | |||

| < 1 | 6-12 months | 700+ | 60% | |

| 680+ | 50% | |||

| $3 – 3.5 million | > 1 | 12 months | 700+ | 55% |

Today’s DSCR Loan Rates

Griffin Funding offers both fixed and adjustable-rate DSCR mortgages with no balloon payments. DSCR fixed rates are offered on 40-year, 30-year, and 15-year terms. DSCR adjustable rates are provided on 10-year, 7-year, 5-year, 1-year, and 6-month adjustment periods. All DSCR programs have the option for full amortization or interest-only payments upon approval.

Where We Offer DSCR Loans

Griffin Funding offers DSCR loans in all 50 states and the District of Columbia to help real estate investors find investment properties in their ideal locations.

![]()

Pros, Cons, and Other Considerations

In the sections below, we go through DSCR loan pros and cons, lay out the situations when a DSCR loan may not be ideal, and discuss the unexpected elements that can arise from this type of financing.

Pros and Cons of DSCR Loans

Pros |

|---|

| Accessibility |

| Streamlined approval process |

| Unlimited cash-out |

| No cash-out seasoning requirements |

| No limit on the number of properties |

| All types of rentals are eligible |

| Borrower in an LLC |

| Jumbo DSCR loans |

| Flexible qualifying requirements |

Cons |

|---|

| Large down payments |

| Higher interest rates |

| Limited financing |

| For rentals only |

| Vacancies |

| Prepayment penalties |

| No Fixer-Uppers |

| Unique Properties |

|

Benefits of DSCR loans

DSCR loans are often easier to qualify for and offer a streamlined approval process because there’s no personal income or job history requirement. Advantages of DSCR loans include the following:

- Accessibility: Your eligibility for a DSCR loan is determined by a single figure: your DSCR. Since lenders don’t consider personal finances, they’re more accessible to all types of borrowers, including novice and veteran investors.

- Streamlined approval process: Griffin Funding uses AI-driven underwriting to simplify and speed up DSCR loan approvals. Our proprietary Loan Intelligence Assistant (LIA) — which was recently featured in HousingWire — enhances accuracy, reduces underwriting times, and accelerates closings. In 2025, we’ve closed DSCR loans in as little as six days, with an average closing time of 34 days. This new tech-driven approach now helps investors act even faster, while securing better terms and growing their portfolios without delays.

- Unlimited cash-out: DSCR loans offer unlimited cash-in-hand, which means you can continue taking out money when needed to cover expenses like repairs.

- No cash-out seasoning requirements: Unlike conventional financing, DSCR loans do not require a six-month holding period before you can refinance a property as cash-out. Instead, properties can be refinanced for cash-out immediately after acquisition. This flexibility enables investors to unlock liquidity faster and reinvest in new opportunities without waiting months to access their equity.

- No limit on the number of properties: DSCR loans allow investors to purchase multiple properties simultaneously. With traditional loans, borrowers are limited by the number of properties they finance. However, with DSCR loans, investors can purchase as many properties as they want to build their portfolios. DSCR loans can also have a multiplier effect. For instance, you can qualify for a loan with one property then once it gains enough equity you can refinance it and use the cash to purchase an additional rental property.

- All types of rentals are eligible: DSCR loans can be used for all types of rentals, such as short and long-term rentals and various properties, including single and multi-family homes. Rural properties with limited acres and supporting rental comps are permitted.

- Borrower in an LLC: A limited liability company (LLC) can be used to purchase investment properties for business purposes. Taking out the DSCR loan in the name of an LLC helps protect your personal assets, and if structured properly, the loan will not be reported to your personal credit report. There can be multiple members in the LLC, and not all members need to personally guarantee the loan. DSCR LLC mortgage loans are perfect for real estate syndications. Syndicators can raise money from investors, pool the funds for down payments, purchase investment properties, and use DSCR mortgage loans to finance them. In addition to its ability to be held by an LLC, a DSCR loan can also be held in a revocable trust.

- Jumbo DSCR loans: Jumbo DSCR loans are ideal for real estate investors who focus on investing in high-end luxury properties. At Griffin Funding, we offer jumbo DSCR loans of up to $20,000,000.

- Flexible qualifying requirements: DSCR loans aren’t subject to the strict requirements that conventional loan products must follow, and this allows for more flexibility when it comes to qualifying. Lenders may be able to look past a lower credit score or down payment if there are other compensating factors or if they are presented with a great loan opportunity.

“When I advise real estate investors on DSCR loans, the first step is comparing the payment difference between an interest rate with no points versus a lower rate with points. Recently, I worked with a borrower who could save $190 per month by buying down the rate. But since their plan was to refinance in four to five years and use equity to purchase another property, they chose the higher rate with no points. That strategy kept more cash in their pocket today, while rental income still covered the mortgage. By waiting to refinance when rates are lower, they’ll preserve liquidity now and use future equity to keep building their portfolio.”

Adam Ruvelson, Producing Sales Manager / Sr. Loan Officer

Think you qualify for a loan? Contact us today to find out!

Get StartedCons of DSCR loans

Unfortunately, like all types of loans, DSCR loans have some risks and drawbacks that may not make them suitable for every borrower. The cons of DSCR loans include the following:

- Large down payments: Most lenders require a large down payment of 20-40%, which may be higher than some conventional mortgages. However, Griffin Funding allows for as little as 15% down.

- Higher interest rates: DSCR rates are typically higher because these loans are riskier investments for the lender. Additionally, the lender can require you to pay higher fees; the higher your loan amount, the more those will cost.

- Limited financing: DSCR loans offer amounts from $100,000 minimum to $20,000,000 maximum. If you’re purchasing properties for under $100,000 or an expensive property in a luxury market for over $20,000,000, these loans might not be suitable for you.

- For rentals only: DSCR loans are for buy and hold rental properties only, so they can’t be used for a primary residence or to fix and flip a home. Instead, you can only use a DSCR loan for a property that generates cash flow. If you plan to flip a home, you’ll need another type of mortgage loan.

- Vacancies: It’s normal for rental properties to have vacancies every now and then. However, you’re not generating any cash flow if you have vacancies. Lenders don’t assess your ability to repay your mortgage if your property or units within the property are vacant, so you could end up getting deeper into debt if you’re not consistently generating cash flow. This does not mean that vacant properties do not qualify for DSCR financing; it means that there are additional restrictions and limitations on properties that are not occupied by a tenant.

- Prepayment penalties: Most DSCR loans come with a prepayment penalty ranging anywhere from one to five years. You will get a lower interest rate in most cases if you opt for a prepayment penalty, however there are many different kinds of prepayment penalties so make sure to discuss the details with your loan officer. DSCR loans are available without pre-payment penalties, and pre-payment penalties can be bought out.

- No Fixer-Uppers: The property must be move-in ready for tenants and not in need of major repairs, renovations, or construction. DSCR loans are not for properties that need to be rehabbed. The appraiser cannot mark the appraisal “subject to”.

- Unique Properties: Unique properties, such as rural properties and those that can’t be compared to other like properties around the area, can be difficult to finance using a DSCR loan.

When Not to Use a DSCR Loan

While DSCR loans can be a helpful financing option for many real estate investors, there are certain scenarios in which using a DSCR loan may not be ideal. Here are some cases where a DSCR loan may not be the best choice:

- When purchasing a primary residence: DSCR loans are designed for investment properties rather than primary residences because the DSCR is calculated based on the rental income of the property. If you’re buying a home to live in yourself, you’d likely be better served by exploring traditional or non-traditional mortgage options tailored to owner-occupied properties.

- When you want to purchase distressed property/fix and flip a home: DSCR loans may not be suitable for purchasing distressed properties or for fix-and-flip projects where the intention is to quickly renovate and resell the property for a profit. In these cases, short-term financing options like hard money loans or bridge loans may be more appropriate due to their flexibility and faster funding times.

- When purchasing a property worth less than $100,000: DSCR loans are often more suitable for financing larger real estate investments with higher property values. For properties valued at less than $100,000, the transaction costs and underwriting requirements associated with DSCR loans may outweigh the benefits. In such cases, alternative financing options may be more practical.

Managing DSCR Loan Surprises

When applying for a DSCR loan, several unexpected elements or surprises may arise that you should be aware of, such as:

Prepayment Penalties

Prepayment penalties are fees lenders charge if you pay off your loan earlier than the agreed-upon term by either selling the home or refinancing the loan. The penalties are outlined in the loan agreement, can vary in terms of calculation method and amount, and are dependent upon the laws in the state in which the property is located. Below are some examples of common ways that prepayment penalties are structured:

- 5-4-3 prepayment structure: The most common type of prepayment penalty structure is a 5-4-3, or step-down, meaning it goes down from 5% to 4% to 3%. With the 5-4-3 structure, if you pay off the loan in year one, you’ll have a 5% prepayment penalty. In year two, you’ll have a 4% penalty, and in year three, you’ll have a 3% penalty. After that, you’ll have no penalty.

- 5-4-3-2-1 prepayment structure: There’s also a 5-4-3-2-1 structure, so your penalty can be anywhere from 1% to 5%, depending on whether you pay your mortgage off in the 1st year or 5th year.

- 3 or 5% flat fee structure: You can also choose a pre-payment penalty of either a 3% or 5% fixed percentage of the loan balance for one to five years.

- 6 months of interest structure: Depending on the number of years the prepayment penalty is structured, typically 1 to 5 years, you’ll have a penalty equal to 6 months of the interest portion of your mortgage payment if paid off before the prepayment period.

“You need to make sure that you figure out what kind of prepayment penalty is being put on the loan because, in many cases, that’s not disclosed. DSCR loans don’t follow federal disclosure guidelines, so you technically don’t need to disclose anything at all until the end. We like to be transparent, so we actually send you a regular loan estimate that looks like what you’re getting on a conventional loan. This way, you know what your fees are and what your prepayment penalty is. You also know we vetted it out versus the rental income, so that the loan has a much higher chance of closing where it starts rather than changing along the way.”

Guy Troxler, a Senior Loan Officer at Griffin Funding with 7 years of experience in the mortgage industry.

Hidden Fees

Review the loan agreement to identify any hidden fees or charges that may not have been clearly disclosed upfront. These fees could include things like:

- Loan origination fees

- Underwriting fees

- Administrative fees

Lenders may present these fees to you on a “term sheet” or a “loan estimate.” Many unlicensed business purpose lenders use a term sheet rather than a loan estimate, which makes it harder in some cases to understand the fees.

DSCR loans are not qualified mortgages (QM) and, therefore, are not held to the same disclosure requirements as loans that fall under federal TRID rules. Term sheets can be changed without notice at any time during the process.

Appraisal Issues

The lender will require a property appraisal as part of the loan process to determine its value. Unexpected appraisal issues, like lower-than-expected valuations of either the property’s value or the rental income, could impact loan eligibility or require additional money upfront from the borrower.

An appraisal coming in lower than expected for either value or rent can cause the most fallout, but it doesn’t have to. It is important to discuss your options upfront and be prepared with a plan B and C, which, in most cases, requires a larger down payment.

You can use our free home value estimator, which will give you an estimated value of the property and an estimated range to get an idea of the value ahead of the actual appraisal being performed.

Market Conditions

Economic and market conditions can influence lending criteria and interest rates. Be prepared for potential changes in market conditions that may affect DSCR loan terms or availability of financing.

Think you qualify for a loan? Contact us today to find out!

Get Started“Who you work with on a DSCR loan makes all the difference. A typical loan officer who doesn’t specialize in DSCR loans may not anticipate common challenges – like an appraisal coming in low or rental comps underestimating actual rent potential. That’s why I always create a plan A, B, and C for my clients. No matter what obstacle comes up, we already have a solution in place to keep their investment strategy moving forward.”

Andre Shmoldas, Producing Sales Manager / Sr. Loan Officer

Applying for a DSCR Loan

As an experienced DSCR mortgage lender, Griffin Funding offers a streamlined application and approval process. Whether you’re interested in purchasing an investment property to attract long-term renters or you want to set up a short-term vacation rental business, read on to learn more about the basic steps involved in applying for a DSCR loan.

How to Apply for a DSCR Loan

To apply for a DSCR loan, the first step is finding a bank or lender with a robust DSCR loan program. Griffin Funding offers DSCR loans and has a history of qualifying borrowers at various income levels for small and large investment property loans.

Here’s an overview of how to apply for a DSCR loan with Griffin Funding:

| How to get a DSCR Loan |

|---|

| 1 Fill out a loan application |

| 2 Calculate your DSCR |

| 3 Lock in your interest rate |

| 4 Get approved |

| 5 Loan is funded |

- Fill out a loan application: Once you’ve chosen a reputable lender, it’s time to fill out a loan application. You can quickly apply for a DSCR loan through Griffin Funding using our online application, or you can call our office and have one of our Sr. Loan Officers fill out the application with you over the phone.

- Calculate your DSCR: Calculate the DSCR and fill out a rent schedule. The rent schedule validates the property’s fair market value, showing whether you can cover additional mortgage payments on a new property. Your DSCR will impact the interest rate that you qualify for.

- Lock in your interest rate: After calculating your DSCR and reviewing your application, we will offer you an interest rate for your loan. You can lock in this interest rate as we proceed through the final steps of the loan approval process.

- Get approved: Close the loan. You don’t need to bring proof of personal income or other information about your financial history. DSCR loan requirements are less stringent than traditional loans, making the closing go much faster.

- Loan is funded: Once the loan is approved, we will quickly fund it and deposit the loan amount into your escrow account.

Upon approval for our DSCR loan program, you’ll receive an estimate of the interest rate, closing costs, and monthly mortgage payments. Prepare to pay for an appraisal and undergo the underwriting process prior to signing the closing documents. The underwriting process includes:

- Credit report review

- Appraisal

- Rental income verification

- Title search

- Final underwriting decision

“It’s a common misconception that a DSCR loan is just an easier way to get a loan than Fannie Mae and Freddie Mac. While we don’t look at direct income, there are still several qualification hurdles that aren’t widely discussed when you do a simple search online. With a DSCR loan, since we’re not looking at an individual’s income, we ideally want to see that a borrower has a history of managing residential real estate. Many times people think that by going with a DSCR loan, they don’t have to divulge the history of other properties they’ve owned and the past payment history on those, but that really just isn’t the case. We want to show that you have experience with managing investment properties, because this is essentially buying into a business with the way these loans are perceived by underwriting. One of the biggest stumbling blocks when going through underwriting is finding properties that are not scheduled within the application.”

Charles Toll, a Senior Loan Officer with 7 years of experience as an LO in the mortgage industry.

How to Get a DSCR Loan on a Short-Term Rental

DSCR loans aren’t just used to finance long-term rentals like business offices and apartment complexes; they can be used for short-term rentals like those listed on Airbnb and VRBO.

Short-term vacation rentals are a $64 billion market in America, with each listing taking in an average of $26,024 each year. This represents a huge financial opportunity for real estate investors, especially for those looking to buy in areas that are highly desirable for vacations and tourism.

More recently, AirDNA’s 2025 market outlook report indices indicate that occupancy rates are expected to rebound (to ~54.9% by the end of 2025) and listing growth remains strong, signaling continued strength in STR demand and revenue potential.

Here’s how a DSCR loan can help you purchase a short-term rental:

- Short-term rentals are income-producing properties, making DSCR loans a perfect solution for investors who want to use the property’s rental income to qualify for the loan.

- By securing a DSCR loan with favorable terms, investors can potentially lower their borrowing costs and improve cash flow from their STR properties.

- Investors who already own STR properties can also refinance with a DSCR loan to lower their interest rates or access equity through a cash-out refinance. This can provide additional capital for property improvements, expansion, and other investment opportunities.

To qualify for a DSCR loan on a short-term rental property, you typically need to meet certain criteria, such as:

How to get a DSCR Loan on a Short Term Rental |

|---|

| Minimum credit score of 640 |

| Minimum DSCR of 0.75 |

| Projected annual revenue divided by 12 months to demonstrate sufficient income to cover debts |

- Minimum credit score of 640

- Minimum DSCR of 0.75 (No Ratio / <1 DSCR available with larger downpayment)

- Projected annual revenue divided by 12 months to demonstrate sufficient income to cover debts.

“Between the creative financing options we offer, our ability to make some exceptions, and the flexible solutions we provide, we demonstrate a deep expertise when it comes to non-QM loans while providing personalized service and a commitment to the client’s success. Our long-term relationships with clients are built on trust and the mutual success of them closing on a loan. This leads to our clients having a little bit more financial freedom or being able to move into their dream home, where their kids all get a bedroom. So we are always dedicated to helping these clients achieve those financial objectives.”

Colby Freer, a Senior Mortgage Consultant with 10 years of experience at Griffin Funding.

Questions to Ask Your DSCR Mortgage Lender

Here are some essential questions to ask your DSCR mortgage lender:

What are the interest rate, loan terms, and fees?

Understand the interest rate on the loan, whether it’s fixed or adjustable, and how it will impact your monthly payments and overall cost of borrowing. Additionally, you should inquire about the duration of the loan, repayment schedule, and any prepayment penalties or balloon payments that may apply.

To determine the total cost of borrowing, ask about:

- Origination fees

- Discount points

- Closing costs

- Any other fees associated with the loan

What property types qualify?

Eligible property types can vary between lenders. Ask your lender about any restrictions on the types of properties that qualify for the loan, such as residential, commercial, rural, or multi-family properties.

Are you experienced with DSCR loans and working with investors?

Working with lenders experienced in DSCR loans is crucial because they understand the unique aspects of investment properties. Key features of experienced DSCR lenders include:

- Understanding investors’ needs to offer financing solutions that align with their investment strategies.

- Expertise in property analysis to determine their income potential and accurately calculate DSCRs, evaluate property cash flow projections, and determine loan eligibility based on property performance.

- A streamlined approval process because the lender understands the documentation requirements, underwriting criteria, and due diligence process for investment properties to facilitate efficient loan approval and funding.

- There should be multiple money sources that have an appetite for all types of DSCR non-QM loans. The lender should not have one money source with one set of guidelines. Not all investment properties are equal; if the lender has access to funding from private equity, securitization, and large insurance companies, then your loan has a better chance of closing.

Apply for a Non-QM Investment Property Loan

Begin or continue building your real estate investment portfolio without the need for a hard money private loan. Our DSCR loans are an excellent mortgage option for new and seasoned investors to help you build your portfolio without mortgage challenges standing in your way.

Whether you are a first-time investor or an experienced investor investing in a long-term rental property or a short-term vacation rental, our DSCR loans have you covered. Capitalize on current DSCR loan rates and start building your rental property portfolio.

Want to learn more about our non-QM loans before applying? Get started online, contact us, or online or call us at 855-698-1098 to speak to one of our experienced loan specialists.

Unique DSCR Loan Programs

At Griffin Funding, we don’t just offer standard DSCR loans—we provide specialized DSCR loan solutions designed to serve real estate investors with unique financial profiles and investment strategies.

DSCR No Ratio Loans up to 75% LTV (25% Down-Payment)

Many lenders shy away from DSCR loans where the rental income doesn’t cover the mortgage payment, but Griffin Funding offers less than one ratio DSCR loans up to 75% LTV (25% down-payment) with a 700+ FICO and up to $1 million loan amounts. This option is ideal for investors focused on long-term appreciation or high-end properties with value-add potential.

15% Down DSCR Loans with High Credit

For investors with excellent credit, we offer DSCR loans with only 15% down (85% LTV) for loan amounts up to $1 million when you have a 740+ credit score. Preserve capital for your next investment while still locking in competitive rates and favorable terms.

DSCR Qualification Using Rental Income Plus Assets

Our innovative DSCR calculation goes beyond rental income alone. You can now qualify using monthly qualifying income calculated from both rental income and eligible assets – DSCR/Asset hybrid loan. For example, $60,000 in eligible assets can count as $1,000/month in additional income – helping you meet DSCR requirements more easily. A DSCR/Asset hybrid loan is a game-changer for investors with significant liquid assets or those transitioning between income sources.

No Cash-Out Seasoning Requirements

Griffin Funding allows cash-out refinances with no seasoning period – even on recently purchased or recently listed properties. With this loan, you can cash out based on today’s value and not the purchase price.

This feature is ideal for investors who purchase below market at foreclosure auctions, wholesale deals, or renovate properties and want to recycle their capital quickly to move onto the next investment.

SOFR DSCR ARM loans

Griffin Funding offers 6-month and 1-year SOFR-based adjustable-rate mortgages (ARMs) for DSCR loans with no prepayment penalties. These non-traditional mortgage options are ideal for investors who want flexible financing aligned with market interest rate trends. Because these loans are tied to the Secured Overnight Financing Rate (SOFR) – the industry standard replacing LIBOR – they typically offer lower introductory rates and transparent market-based adjustments. Investors benefit from greater flexibility, shorter fixed periods, and the ability to sell or refinance without penalty if rates drop or new opportunities arise. This program is especially advantageous for real estate investors seeking short to mid-term holds, bridge-to-permanent strategies, or portfolio repositioning, giving you the freedom to adapt as your investment goals evolve.

Sara J.

Sara J.

“Great team to work with from application through closing and afterwards for follow up needs. Very fast turnaround on rental property cash out mortgage. Have used them twice for this product and will again if I need to. Highly recommend for rental real estate investors!”

Other Non-QM Mortgage Products

Frequently Asked Questions

DSCR Loan Definition

A DSCR loan is a non-traditional mortgage that measures the gross rental income against the current debt obligations of an investment property. These loans are alternative mortgages used by real estate investors to qualify for financing based on the property’s income, without personal income verification.

You can use a DSCR loan for rental property investments, including single-family homes, multifamily units, and short-term rentals. Lenders approve financing based on how much income the property generates, so you can focus on properties that strengthen your investment strategy and help you grow your portfolio.

Your DSCR changes as income and expenses shift. Rental rates, vacancies, and operating costs all affect the ratio. A strong DSCR signals a lower risk to lenders, while a weaker ratio can limit financing options.

Lenders often use market rent projections or appraisals to calculate DSCR, though some may also consider actual rental income. This flexibility helps investors secure financing for both established properties and those expected to generate strong income after purchase or renovation.

DSCR Loan Requirements

Most DSCR loans require a down payment of at least 20 to 25 percent. The exact amount depends on the property, lender, and your overall financial profile. A higher down payment may improve your loan terms and lower DSCR loan interest rates. Griffin Funding allows for down-payments as low as 15%.

Lenders typically look for a credit score of 620 or higher for DSCR loans. A stronger credit score may help you secure better terms and lower DSCR loan interest rates. Even if your score is lower, Griffin Funding can review your options to see what works best.

Yes, although qualifying may be more difficult. A DSCR below 1.0 means your rental income does not fully cover the debt, which increases lender risk. Some lenders still approve loans with lower ratios, but often at higher rates or stricter terms.

No, DSCR loans are only for investment properties. They are designed to help you purchase or refinance rental properties based on income potential. If you want financing for a primary residence, you’ll need to explore other mortgage options.

No, a DSCR loan is not a hard money loan. Hard money loans are short-term and come with very high rates. DSCR loans are structured like traditional mortgages, with longer terms and more favorable interest rates for investors.

PITIA stands for principal, interest, taxes, insurance, and association fees. Lenders compare your rental income to PITIA to calculate DSCR. The lower your PITIA compared to rental income, the stronger your ratio and the easier it is to qualify for financing.

Some lenders allow gift funds toward the down payment or closing costs on a DSCR loan, but requirements vary. Griffin Funding can help you review your options and determine whether gift funds are acceptable for your specific situation.

You can connect directly with a Griffin Funding loan specialist. They’ll walk you through DSCR loan pros and cons, current DSCR loan interest rates, and specific requirements. This personalized guidance helps you choose the best loan for your investment goals.

DSCR Loan Use Cases

A DSCR loan is perfect for real estate investors who want to qualify using property income instead of personal income. This is especially useful if you are self-employed, own multiple properties, or want to scale your portfolio quickly.

Yes, first-time investors can qualify for DSCR loans. As long as the property meets income requirements, you can use this financing to get started in real estate investing.

Yes, DSCR loans are one of the best ways to build a rental property portfolio. Since approval focuses on property income rather than your personal income, you can keep growing your investments even as you add more properties.

Yes, you can refinance investment properties using a DSCR loan. Refinancing can help you lock in better interest rates, access equity, or restructure debt to improve cash flow.

Getting a DSCR Loan

The best place is with a lender who specializes in DSCR loans, like Griffin Funding. You’ll benefit from competitive rates, flexible terms, and a team that understands how to tailor financing to your investment strategy.

Griffin Funding is the #1 direct-to-consumer DSCR lender in the United States, helping real estate investors access non-traditional mortgage solutions nationwide. Founded in 2013, Griffin has grown into a trusted leader in DSCR loans, specializing in helping clients qualify based on rental income and property cash flow, not tax returns or W-2s.

Our proprietary Loan Intelligence Assistant (LIA), recently featured by HousingWire, uses AI-driven underwriting to streamline the approval process, reduce manual errors, and fund loans faster. In 2025, Griffin Funding has closed DSCR loans in as little as six calendar days, with an average of just 34 calendar days from application to funding.

Backed by an A+ BBB rating and thousands of 5-star reviews across Google, Yelp, and the BBB, Griffin Funding is proud to serve investors in all 50 states with transparent terms, expert guidance, and exceptional client service.

“Our mission is to empower real estate investors to grow wealth through smarter financing – by combining technology, transparency, speed, expertise, and a client-first approach,” says Bill Lyons, CEO of Griffin Funding.

Whether you’re buying your first rental or expanding a multimillion-dollar portfolio, our team of experienced mortgage advisors is here to help you structure the DSCR loan that fits your investment strategy – and your goals.

Your DSCR directly impacts loan approval, interest rates, and terms. A higher ratio shows lenders that your rental income covers debt easily, which can lead to better rates. A lower ratio may limit options or increase costs.

Some lenders offer temporary rate buydowns on DSCR loans. This option lowers your initial interest rate, making early payments more manageable. Griffin Funding can help you explore whether a rate buydown fits your investment strategy.

DSCR loans are widely available, but not every lender operates in all states. Griffin Funding offers DSCR loans in all 50 states and the District of Columbia.

At Griffin Funding, qualified and organized borrowers can close on a DSCR loan in as little as six calendar days. Thanks to our AI-powered Loan Intelligence Assistant (LIA) and streamlined underwriting process, most DSCR mortgages close within 30 days or less from application to funding.

This efficiency gives real estate investors a competitive advantage – allowing them to secure financing, lock in rates, and close on properties faster than with traditional lenders.