VA Funding Fee Guide: How Much Is the VA Funding Fee in 2026?

VA Funding Fee Guide: How Much Is the VA Funding Fee in 2026?

KEY TAKEAWAYS

- The VA funding fee in 2026 ranges from 1.25% to 3.3% of the loan amount for purchase loans depending on factors like your down payment size, loan type, and whether it’s your first VA loan use.

- The funding fee for VA cash-out refinance loans is 2.15% for your first use and 3.3% for each subsequent use. For VA IRRRLs, the VA funding fee is a flat 0.5%.

- Certain borrowers can have the VA funding fee waived, including those with service-connected disabilities, recipients of the Purple Heart, and surviving spouses receiving VA compensation.

- The VA funding fee is not the same as private mortgage insurance (PMI). It’s a one-time fee paid at closing to help sustain the VA loan program, while PMI typically involves ongoing monthly payments.

If you’re considering a VA loan in 2026, it’s essential to understand the VA funding fee, a one-time charge that helps sustain the VA home loan program. This fee varies based on factors such as your loan type, down payment amount, and whether it’s your first time using a VA loan benefit. Knowing how the funding fee works can help you plan your finances and potentially save thousands at closing.

VA loans are available to active-duty members of the military and veterans. With a VA loan, you can secure a home loan with a relatively low interest rate without supplying a down payment or paying private mortgage insurance (PMI).

While these benefits are certainly nice, there is a price attached to them. That is where the VA loan funding fee enters the picture. A VA loan funding fee is a cost associated with virtually every VA loan. Borrowers are required to pay the funding fee in order to support the VA loan program and enable other veterans to take out loans as well.

In this post, we explain what the VA funding fee is, why the fee is required, and how much a VA funding fee is. Read on to learn about the VA funding fee or navigate the article using the links below.

- What Is a VA Funding Fee?

- Why Do VA Loans Include a Funding Fee?

- How Much Is the VA Funding Fee?

- Can I Get the VA Funding Fee Waived?

- VA Funding Fee vs Private Mortgage Insurance

- Explore VA Loans Available From Griffin Funding

What Is a VA Funding Fee?

While VA loans extend several significant benefits to borrowers, they also come with a unique cost known as the VA funding fee. The VA funding fee refers to a one-time fee that a borrower will pay to the Department of Veterans Affairs. The exact size of the funding fee will vary depending on a number of factors, but essentially everyone taking out a VA loan is required to pay it. Keep in mind, however, that in certain cases the VA funding fee can be waived—we’ll go into more detail about that in a later section.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Why Do VA Loans Include a Funding Fee?

The VA funding fee can be significant, so why do VA loans ask you to pay a funding fee? The biggest reason why you are required to pay a VA funding fee is that the program needs to remain sustainable. By paying the VA funding fee, you are supporting the VA loan program and giving other service members and veterans access to these government-backed home loans

Taking out a loan through the VA gives you access to numerous VA loan benefits that are not available to the traditional borrower. The funding for all of these benefits has to come from somewhere, and much of it comes from the government. That means that these benefits are also coming from various taxpayers.

While this is a generous piece of legislation, the program cannot survive on taxpayer dollars alone. Therefore, the government has created a funding fee as a way to keep the program sustainable and to continue offering benefits to borrowers who have served the country.

How Much Is the VA Funding Fee?

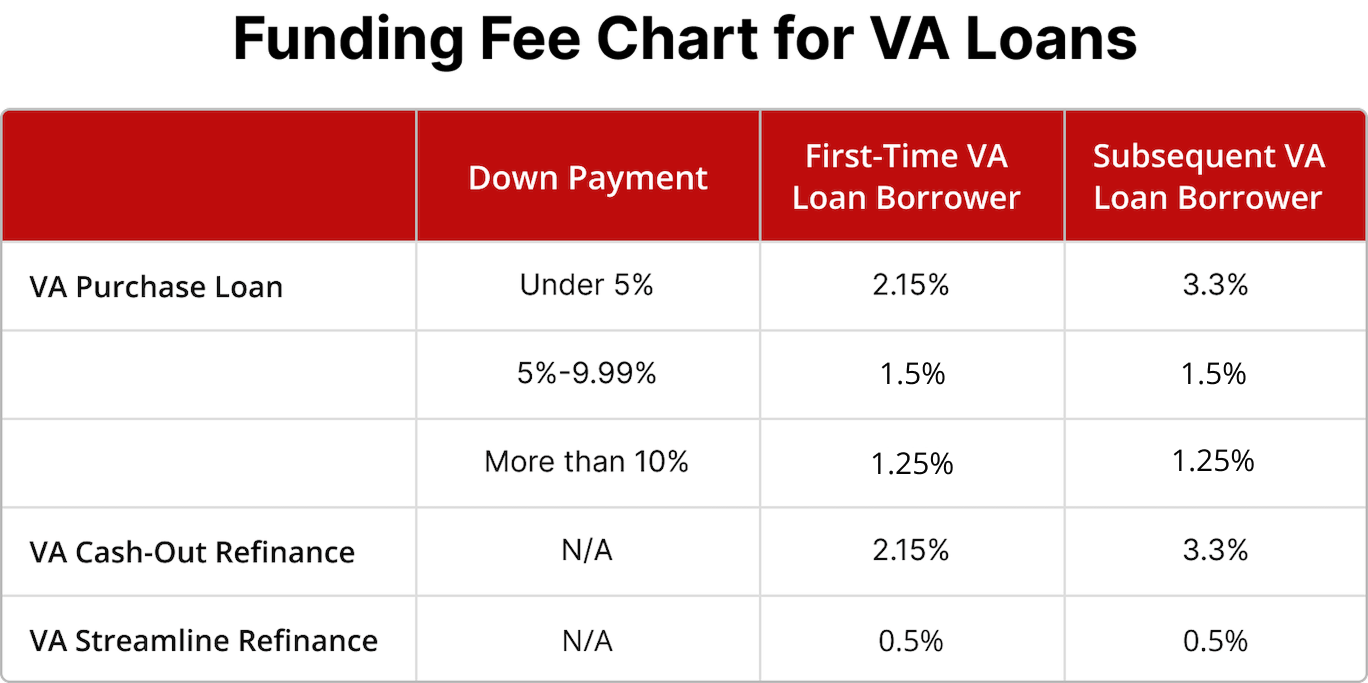

So how much is the VA funding fee? If you are purchasing a home for the first time, you will have to pay 2.15 percent of the loan amount when you close on your house. If you are taking out a subsequent VA loan to purchase a house, you will have to pay a funding fee of 3.3 percent.

For purchase loans, those using their VA loan benefit for the first time will have to pay a funding fee that ranges between 1.25% to 2.15% of the loan amount. After your first use, you will pay a VA funding fee between 1.25% and 3.3%.

For VA cash-out refinance loans, borrowers will pay a VA funding fee of 2.15% on their first use and 3.3% for every subsequent use. VA Interest Rate Reduction Refinance Loans (IRRRLs) come with a flat VA funding fee of 0.5% regardless of your down payment or how many times you’ve used the loan.

If you would like an easy chart that will explain the VA funding fee to you, take a look at the chart below:

Keep in mind that the funding fee can change from time to time depending on changes in legislation. You need to make sure you understand exactly how much money you might have to pay when you close on a house, so consider reaching out to a professional who can help you. It might be difficult to keep up with changes in funding fee legislation, but an expert can point you in the right direction.

VA Funding Fee Exemptions

If you are interested in taking out a VA home loan to repair, improve, build, or purchase a house, you will typically be required to pay a VA funding fee. The VA funding fee will also apply to you if you are refinancing a mortgage.

On the other hand, there are a few specific situations in which you might be able to get your VA funding fee waived. Some of the most important examples include:

- Disability: If you can prove that you are receiving VA compensation for a disability that is related to your time serving in the armed forces, you may be eligible to have the funding fee waived.

- Active Pay: If you are eligible to receive VA compensation for a disability that you sustain during your time serving the military, but you are still receiving pay related to active duty service or retirement, you may be eligible to have the funding fee waived.

- Surviving Spouse: If you are receiving dependency and indemnity compensation as a surviving spouse, you might be eligible to have the funding fee waived.

- Pre-Discharge Claim: If you have received a proposed or memorandum rating before the closing date of your loan, and that memorandum says that you are eligible for compensation because of a claim prior to discharge, you might be able to get the funding fee waived.

- Purple Heart: If you have received a Purple Heart prior to the closing date of your loan, you may be able to get your funding fee waived.

If you have to pay the funding fee now but certain factors change going forward, you may be able to get a refund. There might be a way for you to apply for a VA funding fee refund down the road if your circumstances change.

For example, you might be applying for compensation related to a disability you sustained while serving in the armed forces. If your disability claim has not been approved by the time you close on your loan, you might not be able to get the funding for you waived. However, if you can show proof that the claim was approved later, and you can show that the disability was sustained before you closed on your house, you might be able to get your funding fee refunded to you.

VA Funding Fee vs Private Mortgage Insurance

You may have heard that if you put less than 20% down on your house, you might be required to pay private mortgage insurance, also known as PMI. Some people believe that the VA funding fee is simply VA loan private mortgage insurance or VA loan mortgage insurance. But, in reality, that is not the case.

First, when you pay your VA funding fee, you have to pay it all at closing. With mortgage insurance, you typically pay a monthly premium, similar to other insurance policies. Even though the VA funding fee is designed to keep the mortgage program sustainable, which is also the purpose of traditional mortgage insurance, it is not identical to traditional mortgage insurance.

A few important differences to note include:

- With a conventional loan, you are required to pay PMI monthly if your down payment is less than 20%.

- If you decide to take out an FHA loan, you are required to pay a mortgage insurance premium (MIP) as well. This includes an upfront mortgage insurance payment and a monthly premium.

Therefore, you need to understand exactly what type of insurance you are paying, how often you have to pay it, and how much you need to pay. The process can be confusing, and that is why you need to reach out to a professional who has an in-depth understanding of VA loan rates and insurance premiums. We can help you with that.

Explore VA Loans Available From Griffin Funding

If you are interested in applying for a VA loan, consider working with a professional who can help you find the right loan to meet your needs. At Griffin Funding, we have plenty of loan options available, whether you’re looking for a VA loan, a conventional mortgage, or a non-QM mortgage. We understand that everyone comes from a slightly different background, and it would be our pleasure to help you find the right loan package for your upcoming real estate purchase.

Apply for a VA loan with our team today. We can help you qualify for competitive interest rates, get to the closing table at a time that is convenient for you, and finance the home of your dreams. We also offer free tools like the VA loan calculator and VA loan affordability calculator to help you estimate how much home you can afford and what a VA loan may look like for you.

Reach out to us today to start the process.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Do you pay the VA funding fee if you assume a VA loan?

Is the VA funding fee tax deductible?

Can I get the VA funding fee refunded?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Why vacation rental investors are spending more time on market research before buying

For investors already holding properties or considering new purchases, miscalculating revenue in this environm...

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...