VA Certificate of Eligibility: A Complete Guide

VA Certificate of Eligibility: A Complete Guide

KEY TAKEAWAYS

- All eligible veterans, service members, and surviving spouses must obtain a Certificate of Eligibility (COE) from the VA to qualify for a VA loan.

- The COE determines your VA loan eligibility and contains crucial information about your entitlement. There are several ways to request your COE. Either the lender can do it for you, or you can do it before applying for your loan.

If you’re interested in applying for a VA loan, you’ll need your Certificate of Eligibility (COE). This form is crucial for helping lenders determine your eligibility and remaining entitlement to ensure you not only qualify for a VA loan but can afford one with zero down payment required.

VA home loans help eligible active duty service members, veterans, and surviving spouses become homeowners by providing them with more flexible lending criteria, including benefits like competitive VA loan rates, zero percent down payments, lower credit score requirements, and higher maximum debt-to-income (DTI) ratios allowed.

Unfortunately, not everyone who has served in the military qualifies for a VA loan. The VA requires you to meet certain eligibility criteria. The VA COE can help borrowers determine their eligibility and provide them with more information, such as their remaining entitlement if they’ve already used their VA loan. Keep reading to learn more about the VA Certificate of Eligibility.

KEY TAKEAWAYS

- All eligible veterans, service members, and surviving spouses must obtain a Certificate of Eligibility (COE) from the VA to qualify for a VA loan.

- The COE determines your VA loan eligibility and contains crucial information about your entitlement. There are several ways to request your COE. Either the lender can do it for you, or you can do it before applying for your loan.

What Is a Certificate of Eligibility?

To qualify for a VA loan, lenders must determine your eligibility by requesting your Certificate of Eligibility. The VA Certificate of Eligibility is proof that a borrower has met the VA’s service requirements and is eligible to receive a VA loan.

The Certificate of Eligibility for a VA loan is provided by the US Department of Veterans Affairs (VA). This government agency doesn’t service the loan, but they guarantee it, which is why lenders can make the requirements much more flexible. The VA guarantees 25% of the loan, so if you fail to repay or default, the VA will cover part of the cost, making it less risky for lenders.

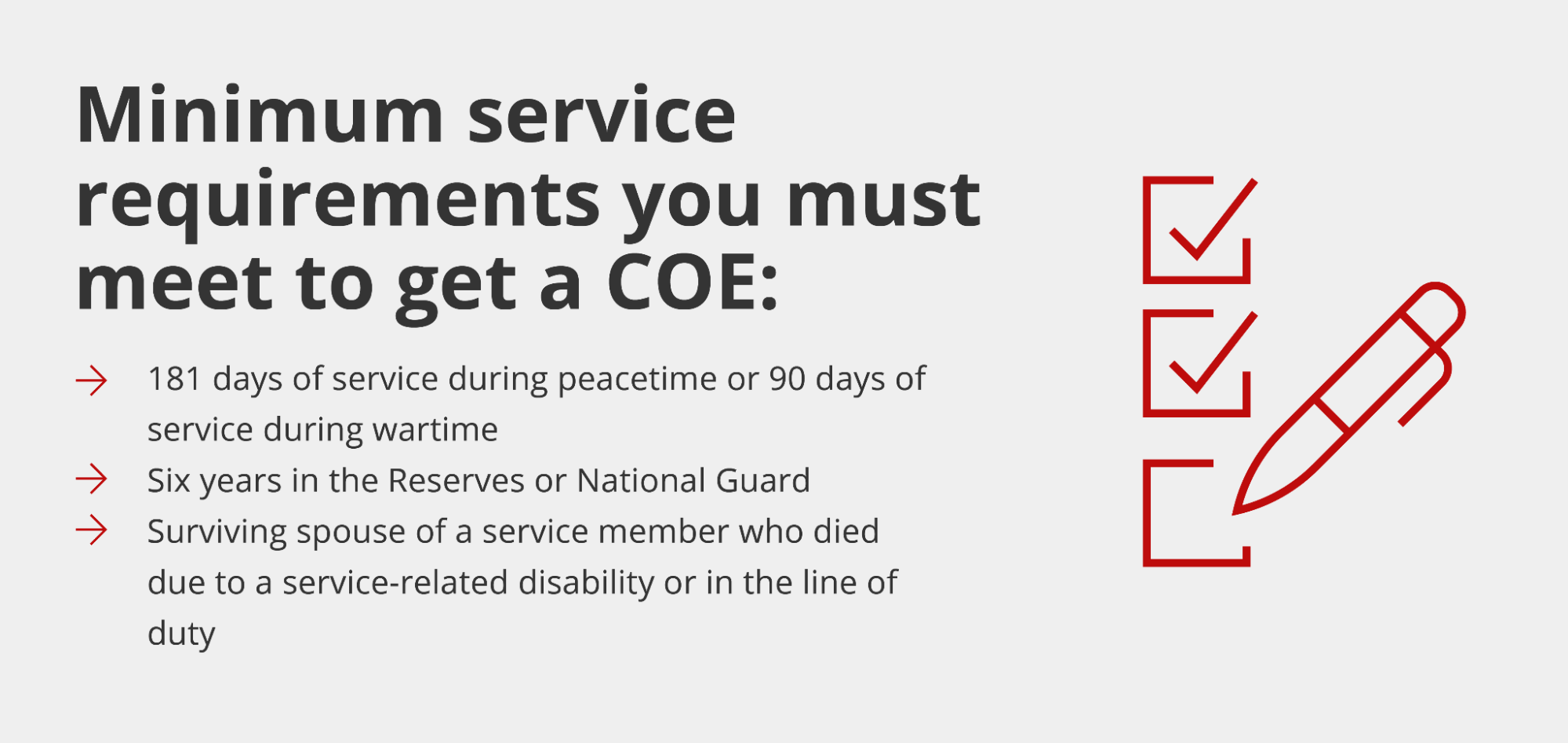

However, to be eligible for a VA loan, borrowers must meet the minimum service requirements, which include the following:

- 181 days of service during peacetime or 90 days of service during wartime

- Six years in the Reserves or National Guard

- Are a surviving spouse of a service member who died due to service-related disability complications or in the line of duty

The VA loan Certificate of Eligibility confirms this information for lenders, allowing them to proceed with the loan application process. However, it also provides information for VA loan borrowers who have already used their loans.

VA entitlement is the maximum amount of the loan the VA will guarantee. There are currently no loan limits for first-time VA loan borrowers. However, if you’ve already used your loan, you’ll have a remaining entitlement, which is equal to 25% of the conforming loan limits in the county where the home is located.

If you have a remaining entitlement that doesn’t cover the VA’s guarantee (25% of the loan), you’ll be responsible for providing a down payment. Let’s take a look at an example in which you’ve used your VA loan once and have already used $90,000 of your entitlement but want to take out a home loan for $500,000.

As mentioned, when a borrower has remaining entitlement (rather than full entitlement), the VA uses the conforming loan limit to calculate how much it will guarantee. For 2026, the baseline conforming loan limit in most US counties is $832,750. In this calculation, the VA would guarantee $208,187.50 ($832,750 x 0.25). However, remember, you’ve already used $90,000 of your entitlement. Therefore, you must subtract $90,000 from that amount, giving you a total of $118,187.50 in remaining entitlement.

The VA guarantees 25% of the total loan amount. In this case, the loan amount is $500,000. Therefore, they’d need to guarantee $125,000 ($500,000 x 0.25).

Now, we have two amounts: your remaining entitlement of $118,187.50 and the $125,000 needed to cover 25% of the loan. Since your remaining entitlement is less than $125,000, you’ll have to pay the difference. Therefore, on this particular $500,000 loan, you’ll need to make a down payment of $6,812.50.

Note: Borrowers with full entitlement — meaning they’ve never used a VA loan or have had a previous VA loan fully paid off and the entitlement restored — are not subject to loan limits and can borrow with no down payment regardless of the purchase price.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Why Do You Need a VA Certificate of Eligibility?

You need a COE to be eligible for the VA loan from a private lender. Without it, you’re not eligible because the lender must verify you meet the VA’s service requirements and have enough remaining entitlement to secure a VA loan with zero percent down.

Without this document, lenders can’t approve you for a VA loan or its benefits, so it’s crucial to obtain your COE if you believe you’re entitled to this benefit. However, even if you’re unsure if you qualify, you can request a COE from the VA to help you understand whether you qualify for a VA loan before applying with a lender.

Additionally, your COE is crucial for helping lenders understand how much the VA is willing to guarantee if you default on your loan. If you’ve already used your VA loan, you may be required to make a down payment to cover the 25% guarantee and continue to take advantage of at least some of the benefits of the loan.

This document also determines whether you have to pay the VA funding fee. Most borrowers will have to pay this fee, which funds the program and helps other eligible borrowers secure a VA loan.

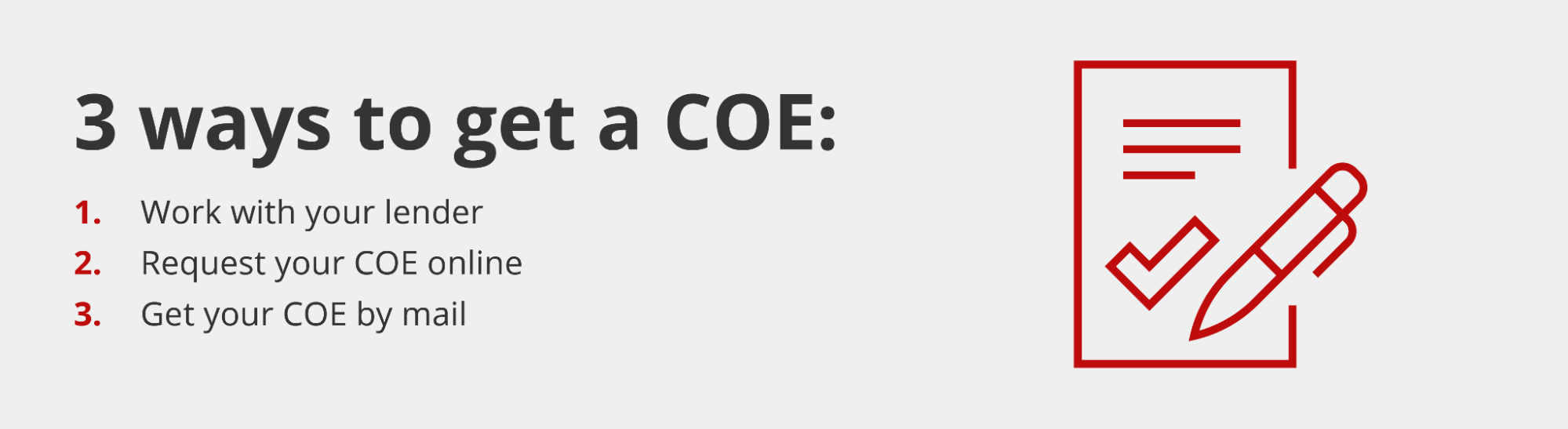

How to get a Certificate of Eligibility

Obtaining your VA loan Certificate of Eligibility is crucial if you want to take out a VA loan. Once you’ve received your COE, you can start searching for a home and apply for a VA loan. Of course, it’s important to note that your COE doesn’t guarantee loan approval. Instead, it simply tells lenders that you’re eligible for the VA loan and how much of your entitlement you have left.

There are several ways to obtain your COE, and some are faster than others. For example, if you request your COE directly with the VA, it can take up to six weeks to receive it by mail. However, there are several other options, which include the following:

Speak with your lender

One of the easiest ways to obtain your COE to be approved for a VA loan is to ask your lender. VA-approved lenders can often access an online system to quickly obtain your COE. This is usually the best option if you’ve already put in an offer on a home and want to streamline the application process.

Request COE online

The VA allows you to request your COE online using the eBenefits portal. Instead of providing a lender with your Social Security number and other personal information, you can simply log in or create a new account.

Get your COE by mail

Another option is to print off Form 26-1880 and mail it to the VA. However, if you request your COE by mail, it can take up to six weeks or longer, depending on your status. Therefore, this is the least efficient method and probably not the right option if you’ve already put an offer in on a house and want to move forward with a streamlined application process.

Instead, you might choose this option if you’re considering purchasing a house and want to learn if you’re eligible. In addition, you’ll need a new COE every time you use your VA loan, so if you’ve already used your loan, you’ll need another one before applying for another loan.

What Do I Need Before Requesting a VA Certificate of Eligibility?

The type of information you need to request your VA COE varies depending on the method. However, it’s usually quite simple as long as you can provide the lender or the VA with the necessary information. Here’s how to obtain your VA Certificate of Eligibility based on your current situation:

Veterans

The easiest way for veterans to obtain their COE is to ask the lender to do it for them. Since they have access to the database of COEs, they can usually pull yours up using your Social Security number and birth date. However, they may require additional information depending on various factors, like the type of discharge.

Veterans are required to provide Form DD-214, Certificate of Release or Discharge From Active Duty, to ensure they’ve met the VA’s active duty requirements. In addition, the type of discharge can factor into eligibility.

Active service members

Active duty military members don’t have discharge paperwork, so they may need to submit a statement of their service to the VA to receive their COE. Usually, they’ll need to provide the following information:

- Full name

- Social Security number

- Date of birth

- Date of entry

- Duration of lost time

- Name of the command providing the information

Members of the National Guard or Reserves

Members of the National Guard and Reserves must also provide a DD-214 and other discharge documents. However, if you’re a current member with at least 90 days of active duty service, you’ll need one of several documents, including:

- A DD-214

- Annual point statement

- DD-220 with accompanying orders

If you’re a current member and have never been activated, you’ll need a statement of service signed by the commander, adjutant, or personnel offer with the following information:

- Full name

- Social Security number

- Date of birth

- Date of entry

- Number of creditable years of service

- Duration of lost time

- Name of the command providing the information

Discharged members of the national guard who were never activated need their Report of Separation and Record of Service NGB Form 22 for each period of service and your Retirement Points Statement NGB Form 23 with proof of honorable service.

Military spouses

Eligible military spouses must also obtain a COE. However, the process is slightly different because they’re not veterans or active duty service members. In addition to providing their own personal information, they’ll need to receive Dependency and Indemnity Compensation (DIC) benefits to qualify. Otherwise, they’ll need Survivors Pension and/or Accrued Benefits VA Form 21P-534EZ.

Eligible borrowers who receive DIC benefits must fill out a Request for Determination of Loan Guarantee Eligibility and receive a copy of the veteran’s DD-214.

Military spouses not receiving DIC benefits, you’ll need to provide the VA with the following documents:

- A completed application for DIC

- A copy of your marriage license

- The veteran’s death certificate

We Can Help You Get a COE for a VA Loan

Obtaining your COE from the VA by mail can take up to six weeks or more, depending on the types of documentation and information you’ve provided. However, Griffin Funding can help you obtain your Certificate of Eligibility for a VA loan quickly to help you verify that you’re eligible for a VA loan and determine whether or not you’ll owe a funding fee or down payment.

Ready to apply for a VA loan? Talk to a Griffin Funding mortgage specialist today. We can help you ensure you qualify for a VA loan and walk you through the process to streamline your journey of becoming a homeowner.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Why vacation rental investors are spending more time on market research before buying

For investors already holding properties or considering new purchases, miscalculating revenue in this environm...

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...