No-Income Verification Mortgage: Can You Get a Mortgage Without Tax Returns?

No-Income Verification Mortgage: Can You Get a Mortgage Without Tax Returns?

KEY TAKEAWAYS

- No-income verification mortgages allow borrowers to qualify with alternative methods.

- Bank statements, assets, and signed statements can be used to qualify for no-income verification loans, among other options.

- No-income verification mortgages may be a beneficial option for retirees, business owners, and others whose true income is not reflected on their tax returns.

Getting approved for a mortgage doesn’t always mean showing years of W-2s and tax returns. A no-income verification mortgage might be your path to homeownership if you’re self-employed, a business owner, or someone with non-traditional income.

Purchasing a home is the most significant and fulfilling transaction most people will make in their lifetimes. But first, you have to qualify for a mortgage.

And if you have unsteady income, non-traditional sources of income, less-than-perfect credit, job instability, or any potential problems verifying your income, it can seem all but impossible.

Fortunately, no-income verification mortgage loans are tailor-made for unconventional financial situations. Read on to learn more about no-income verification mortgages and how you can qualify.

KEY TAKEAWAYS

- No-income verification mortgages allow borrowers to qualify with alternative methods.

- Bank statements, assets, and signed statements can be used to qualify for no-income verification loans, among other options.

- No-income verification mortgages may be a beneficial option for retirees, business owners, and others whose true income is not reflected on their tax returns.

What Are No-Income Verification Mortgages?

No-income verification mortgages, also known as stated income or low-documentation mortgages, are popular types of non-qualified (non-QM) home loans. These types of home loans allow you to qualify your income based on alternative methods.

A few key advantages of mortgages with no-income verification offered by Griffin Funding include:

- You do not need tax returns or tax transcripts to qualify.

- Lenders can use 12 or 24-month bank statements.

- Businesses can show 12-24 months of P&L statements.

- You can get a no-income verification mortgage with as little as 10% down.

- You can borrow up to $5 million.

- Our no-income verification mortgages will allow a higher debt-to-income ratio than traditional lending products.

- You can choose a fixed-rate, adjustable-rate, or an interest-only no-income verification mortgage.

Traditional mortgages require extensive income verification documentation, such as:

- W-2 statements

- Pay stubs

- Tax returns

- Other financial documents

However, if you’re a real estate agent, freelancer, business owner, or consultant, these documents may not be readily available. Fortunately, lenders often accept the following as income instead:

- Bank statements

- Signed statements

- Using assets as income

Depending on the lender and your financial circumstances, other non-traditional income verification methods may also be applicable.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Are No-Income Verification Mortgages The Same as No Doc Loans?

In the early 2000s, “no-doc” loans earned a reputation as mortgages where you could simply state your income without proving it. Today’s no-income verification mortgages are different. While they’re a type of no-doc/low-doc mortgage loan and offer flexibility in how you prove your income, you’ll still need to provide documentation — just not the traditional W-2s and tax returns. Instead, you might show bank statements, proof of assets, or other financial records that demonstrate your ability to repay the loan.

There are no truly no-doc or no-income mortgage loans anymore. Whichever mortgage loan type you choose, the lender must ensure you can pay your mortgage every month. It’s more accurate to call no-income verification mortgages “alternative documentation” loans. The lender still needs to verify you can afford the mortgage; they’re just more flexible about how you prove it.

How Can I Get Approved for a Mortgage Without a Source of Income?

In general, it can be very difficult—and for some, almost impossible—to get approved for a traditional mortgage without a steady and verifiable source of income.

This is because your income determines your ability to repay the loan. However, if that’s not an option based on your circumstances, you may be eligible for a no-income verification mortgage.

Some of the notable criteria for our no-income verification mortgage loans include:

- Acting as a business owner or being self-employed for at least two years.

- Note: If you have two years of experience in the same field, you may qualify with one year of owning a business.

- Have a credit score of 620 or above.

- At least 10% down payment, depending on your credit score.

- You’ll need at least 10% down (90% loan to value, w/ a 720+ credit score).

- You’ll need at least 15% down (85% loan to value w/ a 700+ credit score).

- You’ll need at least 20% down (80% loan to value w/ a 660+ credit score).

- You’ll need at least 25% down (75% loan to value w/ a 620+ credit score).

- Several months of reserves.

- You’ll need three months of reserves in the bank for loan amounts under $1 million.

- You’ll need at least six months of reserves in the bank if your loan is over $1 million.

- You’ll need at least 12 months of reserves if your loan is over $1.5 million.

- You may qualify with as little as 12 months of bank statement deposits.

- The minimum loan amount is $100,000, and the maximum loan is $5,000,000.

Types of No-Income Verification Mortgages

There are many different types of no-income verification mortgages for borrowers with limited or non-traditional sources of income. Some of our most popular loan types include:

- Asset-Based Loans and Mortgages: As the name suggests, these types of no-income verification mortgage loans — also known as asset depletion mortgages— use assets to qualify for a loan. Whether you are a new business, a retiree on a fixed income, or an established company that needs to maintain a high cash flow, asset-based loans and mortgages are a flexible solution.

- Bank Statement Loans: Bank statement loans are a type of no-income verification mortgage that uses your bank statements instead of tax returns. To qualify, you’ll need to provide a specific number of bank statements, which will depend on lender requirements. Bank statement mortgage programs are ideal for business owners, freelancers, self-employed individuals, and retirees who need an alternative income verification option. Try our bank statement loan calculator to see how much you might qualify to borrow.

- Debt Service Coverage Ratio Loans: Debt Service Coverage Ratio (DSCR) loans are a no-income verification mortgage designed to help real estate investors. The DSCR is the ratio of a property’s annual gross rental income and its annual mortgage. The DSCR determines how much of a loan can be supported by the income generated from the property. Use our DSCR loan calculator to see if you qualify for this investment property loan.

Types of No-Income Verification Refinance Loans

Already have a mortgage but looking to refinance? There’s good news — some refinancing options truly require no income verification at all. Unlike other mortgage programs that ask for alternative proof of income, these streamline programs skip the income check completely. The two main options are:

- FHA streamline refinance: The FHA streamline refinance is available if you already have an FHA loan. This program focuses mainly on whether you’ve made your payments on time. They won’t ask for pay stubs, tax returns, or even bank statements to verify income.

- VA streamline refinance: This option is for veterans with existing VA loans. Like its FHA counterpart, it skips the income verification entirely, making the refinancing process quick and straightforward.

What Credit Score is Needed for a No-Income Verification Mortgage?

At Griffin Funding, our no-income verification mortgage program has significantly lower credit score requirements than a traditional loan.

While most customers have at least 620, we have issued mortgages for customers with credit scores as low as 580—as long as other compensating factors were present. Our no-income verification mortgages are among the best home loans for bad credit.

Pros and Cons of a No-Income Verification Mortgage

Determining whether a no-income verification mortgage is right for you requires you to carefully consider the potential advantages and disadvantages it may present for you. Below, we’ve outlined some of the most notable pros and cons of a no-income verification mortgage.

Pros of a No-Income Verification Mortgage

- Simplified Application Process: No-income verification mortgages usually require less documentation than traditional mortgages, which can make the application process faster and more straightforward.

- Less Restrictive Qualification Requirements: Because there are more flexible underwriting requirements, we define our criteria, which means an easier, less-restrictive qualification process.

- Higher Loan Amounts: With no-income verification mortgages, borrowers can potentially qualify for higher loan amounts since the lender is not relying solely on income to determine eligibility.

- Flexibility: Borrowers who may not meet traditional income and employment requirements may still be able to qualify for a mortgage with a no-income verification loan, allowing them more flexibility in their home financing options.

Cons of a No-Income Verification Mortgage

- Higher Interest Rates and Fees: Since no-income verification mortgages are considered riskier for lenders, they may come with higher interest rates and fees than traditional mortgages.

- Risk of Default: As with any loan, the risk of default is always present.

Why Apply for a No-Income Verification Mortgage With Griffin Funding?

Griffin Funding is the premier no-income verification mortgage lender. We specialize in offering an array of no-income verification mortgages and other types of non-QM loans and are a fully-digital direct lender.

Our experienced team employs cutting-edge technology to originate loans efficiently. Most importantly, we will guide you through the process. We will suggest the best lending solution for your circumstances to help you achieve your goals. Learn more about our customer-focused application process.

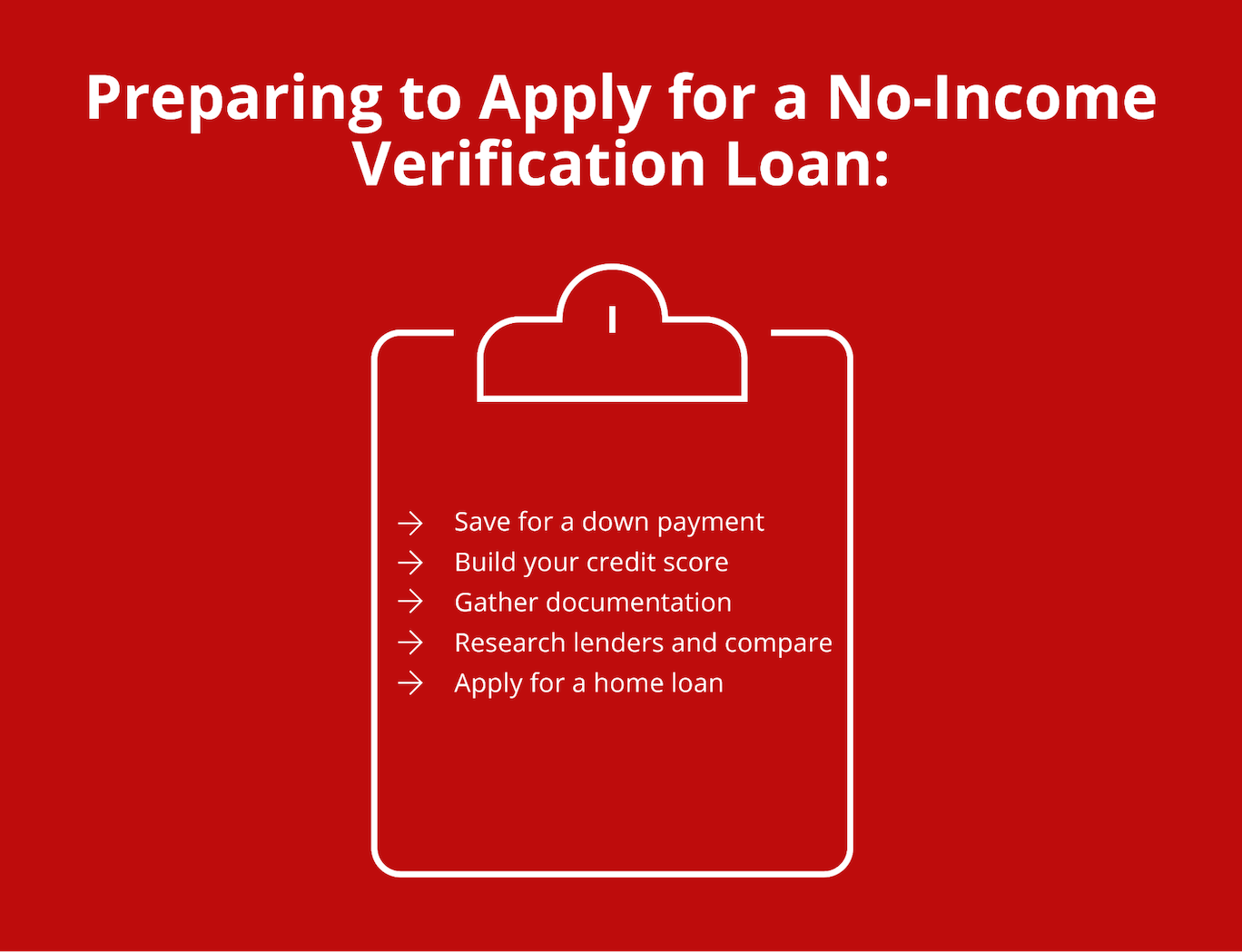

How to Apply for a No-Income Verification Loan

Applying for a home loan can be cumbersome. That’s why we have streamlined our mortgage process into 10 simple steps:

- Discovery Meeting: We will get to know you, understand your unique situation, and guide you to the type of no-income verification mortgage best suited to help you achieve your goals. We will also walk you through all of your options, so you can confidently make the best decision.

- Loan Application: In most instances, you can use our secure digital mortgage platform. However, if you need assistance, we can complete the application over the phone to ensure accuracy.

- Secure Your Rate: Once we have your authorization, we will lock in your interest rates to maximize your savings.

- Application and Disclosures: We’ll securely send you all applications and disclosures. You will sign and return all documents with an electronic signature via email in a secure PDF, through our digital mortgage platform, or via overnight delivery. We can accommodate whichever method you prefer.

- Supporting Documentation: Based on your needs and situation, we will explain the documents you’ll need to fax, scan, use our digital mortgage platform, or overnight the documents to us.

- Mortgage Loan Process: Once all information has been received, our processors and loan processing assistants will submit your file to underwriting. The underwriting team will pay special attention to a few key factors:

- Capacity—Do you have the capacity to repay your loan?

- Credit—Does your credit history suggest you’ll pay on time?

- Collateral—Are the home value and purchase price aligned?

- Appraisal and Pest Inspection: During this step, our independent property appraiser will determine the value of your new home. You will be responsible for ordering a pest inspection by a local termite company (if applicable).

- Loan Approval: We will contact you to discuss the terms of approval and any outstanding criteria.

- Final Loan Document Signing: After your loan specialists review your closing disclosure with you, a mobile notary will schedule a time for the signing. We will be available to answer any questions during this time.

- Loan Funding Recording: As the final step in the process, your funds will be released after the 3-day waiting period for refinancing. Escrow will then wire the funds to you as soon as the County confirms the recording for cash-out. Note that, for purchase loans, there is no 3-day waiting period.

Apply for a No-Income Verification Loan with Griffin Funding

Whether you’re a real estate investor, freelancer, business owner, retiree, or anyone facing difficulty verifying your income with traditional methods, Griffin Funding’s no-income verification mortgage loans can help you achieve your goals of purchasing property.

Ready to learn more? Get started online or speak directly with one of our loan specialists by calling 855-698-1098.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Who should apply for a no-income verification loan?

- Real estate investors

- Gig economy workers

- Sole proprietors

- Home flippers

- Freelancers

- Realtors

- Consultants

- Independent contractors

- Self-employed individuals

- Business owners

- Entrepreneurs

- Retirees

Additionally, if you have a low credit score or a high debt-to-income ratio preventing you from qualifying for a traditional mortgage, Griffin Funding's no-income verification mortgage loans may be a potential solution for you as well.

Do no-income verification loans have higher interest rates?

However, interest rates can vary based on several financial factors as well as market conditions. Additionally, the specific rate you qualify for will depend on the type of no-income verification mortgage loan you choose.

Do no-income verification loans require a larger down payment?

How do I find mortgage lenders that don’t require tax returns?

At Griffin Funding, we specialize in exactly these types of loans and can walk you through your options. Our team has years of experience helping self-employed borrowers and business owners get the mortgages they need.

Can I get a home equity loan without proof of income?

- Bank statement home equity loans: These loans let you prove your income using your banking history instead of tax returns or W-2s. They’re ideal for self-employed individuals or those with variable income but maintain healthy bank balances.

- DSCR home equity loans: These investment property loans focus on your property’s rental income rather than your personal income. If you’re an investor with rental properties, the rental income itself can qualify you for the loan.

- Reverse mortgages (for those who qualify): These mortgages offer a way for homeowners 62 and older to access their equity without any income verification. Since these loans are based on your home’s value and age, not your income, they can be a good option for retirees. We also offer reverse second mortgage loans for older homeowners looking to convert their home equity into cash.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...