Inflation & Housing: How Does Inflation Affect House Prices?

Inflation & Housing: How Does Inflation Affect House Prices?

KEY TAKEAWAYS

- Inflation doesn’t directly influence mortgage rates, but mortgage interest rates tend to rise with inflation.

- In addition to rising interest rates, higher house prices make purchasing a home during inflation more expensive.

- While inflation affects home prices, you shouldn’t let it deter you from purchasing a home because rising inflation means home prices and interest rates will continue to rise, making homeownership more expensive in the future.

Inflation is one of the many concerns on borrowers’ minds today. Unfortunately, when inflation rises, home prices tend to rise with it. However, purchasing a house now may be more affordable than purchasing one in the future as long as inflation is expected to continue increasing.

Rising inflation means higher home prices, but it also means that you can purchase a home for cheaper now than in the near future. Whether you should purchase a home during rising inflation depends on factors such as your current spending power, savings, employment, income, and credit history.

Is rising inflation a good or bad time to purchase a home? Ultimately, it could mean it’s a good or bad time depending on the particular buyer. Unfortunately, we can’t always predict when inflation will slow, so if you want to buy a house right now, you shouldn’t let higher home prices deter you. However, if you can wait to purchase a home, you might find that inflation will ease, making homes significantly less expensive.

So what happens to house prices during inflation? Keep reading to learn more about the housing market and inflation to help you determine whether to buy a house now or later.

KEY TAKEAWAYS

What Is Inflation?

Inflation describes the rising of prices for goods and services over time. As inflation increases, consumer purchasing power decreases because their money doesn’t take them as far. For instance, someone who used to be able to purchase one gallon of milk for $2 years ago may now have to pay $2.75. Their purchasing power decreased, forcing them to buy less for more.

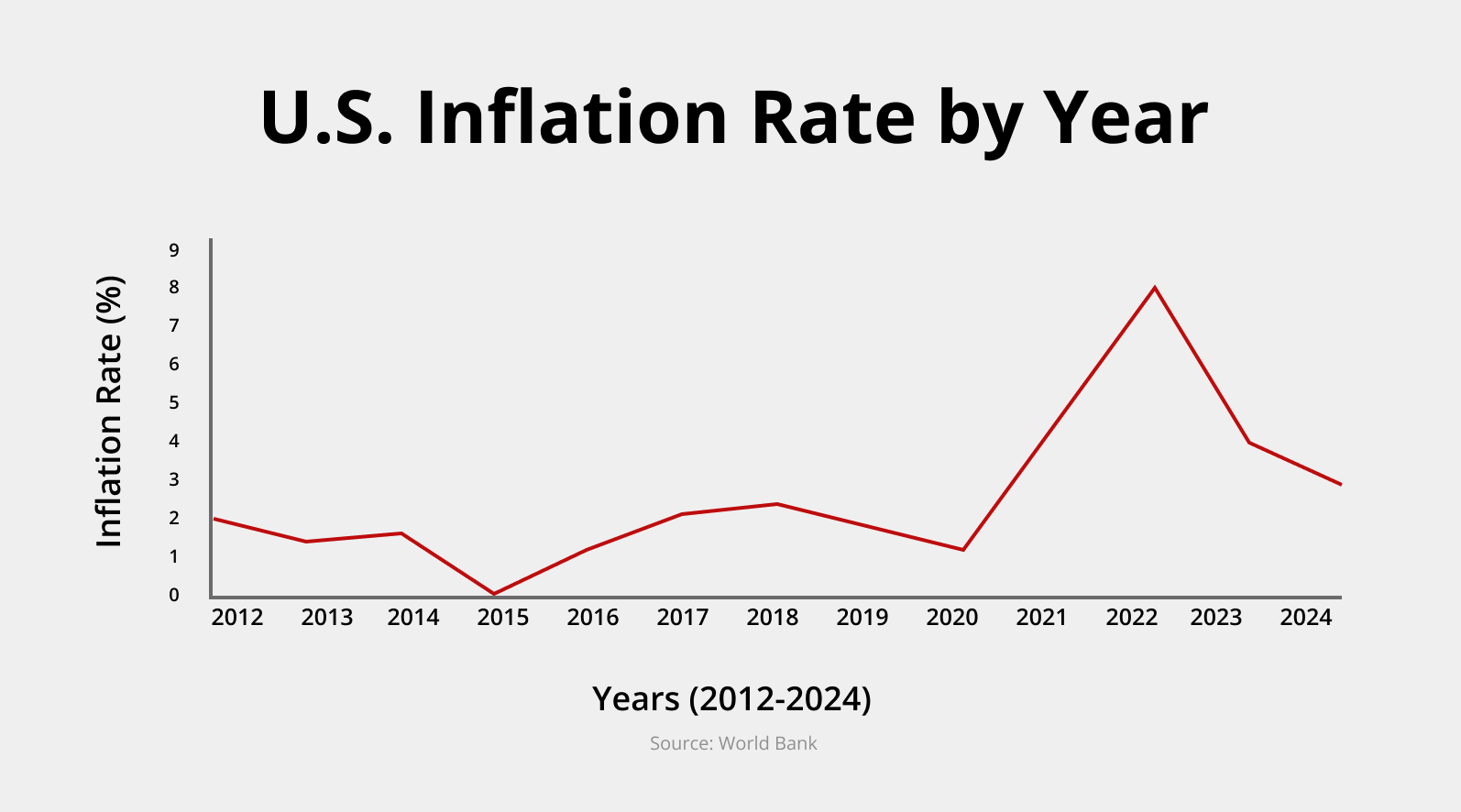

While inflation rates are typically small percentages, the expenses add up quickly. For instance, in 2021, the inflation rate was 4.7%. Let’s say your total grocery cost for one week was $500 before that. In 2021, your groceries would cost $523.50. Most of us buy groceries every week, so if you multiply the additional 23.50 by 4 (the number of weeks in a month), you’ve spent almost an additional $100 just on groceries.

Simply put, inflation measures the increase in pricing for various products and services to help consumers understand how much more they’re paying for everything from toilet paper to haircuts. Of course, prices rise for various products over time, and that’s not necessarily the result of inflation. Inflation occurs only when prices increase throughout the economy, affecting products and services from all industries.

What Causes Inflation?

When consumers have more money to spend or the government prints more money or lowers interest rates, there’s too much money floating around the economy for the number of goods available.

The main cause of inflation is an increase in money throughout an economy, which loses purchasing power for various reasons ranging from the government distributing more money to citizens to loaning new money by purchasing government bonds. Economists categorize the causes of inflation in three ways:

- Demand-pull effect: The demand-pull effect is when the amount of money and credit increases the demand for goods and services too rapidly. When the supply of money increases, the demand for products and services increases because consumers have more to spend. However, since production can’t keep up, the supply of products and services is much lower than demand, leading to price hikes. When consumers spend more, businesses increase prices because there’s more demand and less supply.

- Cost-push effect: The cost-push effect occurs when prices increase due to an increase in cost for production. For instance, a home builder may increase their prices when there’s less building material available or their cost for raw goods increases. Since homes cost more to produce, the supply decreases. However, the overall demand hasn’t changed, so the builder passes the price increases onto the customers.

- Built-in inflation: Built-in inflation relates to consumer expectations during inflation. For instance, workers expect their salaries to increase alongside the cost of goods to maintain their living costs. However, when workers earn more money, the employers that produce goods increase the cost of those goods, further increasing the cost of living.

Understanding inflation is complicated because the cost of everything, such as labor and raw materials, impacts the cost to the consumer. And when the consumer has more money to spend, businesses may increase their prices because their supply can’t keep up with the demand.

How Does Inflation Impact the Housing Market?

Inflation impacts the cost of everything from the socks on your feet to the home you live in, whether you’re a renter or a homeowner. As a result, inflation and the housing market typically have an indirect relationship. Of course, rising inflation doesn’t always impact housing prices, but it usually does. The Federal Reserve Board (the Fed) is responsible for regulating financial activities to combat inflation, and one of the most common ways they do this is by increasing interest rates.

Mortgage interest rates aren’t directly influenced by inflation or the Fed’s interest rates, but mortgage rates typically follow the same path. Unfortunately, this means that when inflation is rising, mortgage rates are likely also rising, making purchasing a home more expensive.

How Does Inflation Affect House Prices?

Understanding the relationship between inflation and house prices can help you determine whether now is the right time to apply for a mortgage. Ultimately, as inflation rises, sales prices of homes increase, but so do mortgage interest rates, making getting approved for a mortgage challenging. That said, short-term inflation typically does not impact mortgage rates. However, inflation doesn’t just impact buyers.

As we’ve mentioned, sellers typically increase their asking price because their money doesn’t go as far as it once did. However, with the combination of increased home prices and interest rates, fewer borrowers can afford these price hikes, so sellers may not be able to find a buyer unless they reduce their asking prices.

In any case, investing in real estate at any point is still considered a good investment because it appreciates in value over time. If you expect inflation to keep rising, purchasing a home now can help you save thousands of dollars over the life of your loan.

Additionally, inflation may reduce the supply of available homes on the market. For instance, construction materials are typically more expensive during rising inflation, and homeowners may want to avoid selling their homes because purchasing a new one is more expensive. When there’s less supply to keep up with demand, homeowners can increase their asking prices.

On the flip side, since consumers have less purchasing power during times of rising inflation, they may not be looking to purchase a home yet, leaving sellers with no choice but to reduce their asking prices because there’s not enough demand.

Inflation and Real Estate: 3 Perspectives

We’ve already discussed the relationship between the housing market and inflation. First, however, it’s crucial to understand how it affects the different types of people involved in the housing market: buyers, sellers, and investors.

Buyers

Inflation and real estate have a complicated relationship that buyers should be aware of before purchasing a home during rising inflation. Buying homes is less affordable during inflation because you have less purchasing power; a dollar doesn’t go as far. A house once worth $250,000 may now be worth $300,000, and since your everyday purchases are more expensive, you’ll have less money to spend on a home.

House price inflation may cause some types of buyers to take a step back and wait for inflation to slow, while others may try to take advantage of home prices being lower now than in the future. For example, instead of purchasing a smaller, less expensive house now, you may be able to wait and purchase a larger house for the same budget later. Unfortunately, there are no guarantees when it comes to inflation and house prices. It’s possible that inflation in the housing market may not slow, leaving you with no other option than to spend more on a smaller home.

Inflation can reduce the overall demand for homes. Increased interest rates and home prices can make many buyers think twice about whether now is the right time to purchase a home. With less demand for housing, it’s possible that inflation can actually force sellers to reduce their asking prices if they want to sell their homes quickly.

So should you buy a home during rising inflation? It depends on your financial situation, employment, debts, income, and how much you have saved for a down payment. Home prices may decrease as many buyers get cold feet around high interest rates and higher home prices, and less demand with more supply means savings for buyers who can stick it out.

Sellers

During housing inflation, home values increase, allowing you to increase your asking price because, like goods and services, your home is worth more. However, you should keep in mind that selling your home means buying or renting a new one, which will also be more expensive during inflation.

Buyers tend to be more hesitant as inflation increases because home prices and interest rates make getting a mortgage and owning a home more expensive. Therefore, even though your home value increases, the lack of overall demand may mean you have to reduce your overall asking price.

Many sellers choose not to sell their homes during periods when inflation is rising drastically because there will be fewer buyers. However, when this happens, fewer homes are available on the market, so the buyers planning to purchase a home during this time will have to compete for the short supply. Again, you must consider supply and demand. When fewer homes are available, and there is more demand for those homes, sellers can increase their asking prices and ask buyers to compete.

However, you should never choose to sell your home based on the simple fact that it’s worth more at certain points. Instead, you should consider other factors like your overall financial goals and housing situation for the future. If you sell your home and hope to use that money to buy a new one, you may be disappointed with what’s available because your money won’t go as far.

Investors

Real estate investing is one of the best ways to grow wealth over time because people will always need housing regardless of inflation. So whether you purchase a single-family home or an entire apartment complex, you can still build wealth when inflation rises.

Like house prices, rents tend to rise with inflation, meaning you can charge more for the same unit without upgrading it. As we’ve mentioned several times throughout this article, consumer purchasing power decreases during inflation.

This means that individuals may be unable to afford mortgage loans or payments, forcing them to put off their dreams of homeownership or selling their homes to save money and avoid foreclosure. However, these individuals still need homes, so they often turn to rentals.

When home prices and interest rates are high, many people choose to wait to purchase homes and instead rent apartments, houses, and condos because purchasing a home is too expensive. When someone is spending more money on groceries, they’re saving less for down payments, so they may turn to renting, which means now is an excellent time to purchase an investment property.

Of course, there are several factors to consider before purchasing an investment property. For instance, buildings and building costs are typically more costly during periods of rising inflation. Like home loans, investment property loans may be more challenging to get, and the properties themselves will cost more. While you can combat this with increasing rental rates, you should calculate your ROI on a property before buying it to ensure you can turn a profit.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Should I Buy Real Estate During Inflation?

Whether you should buy real estate during inflation depends on several factors, such as your budget, financial goals, economic forecasts, and location. You should only ever purchase a home when it’s the right time for you, whether or not inflation is rising.

Sometimes you don’t have a choice and have to either buy or sell a home during inflation. However, if you have a choice, you might consider waiting until prices flatten out. Still, there’s no guarantee, and inflation never just stops. Instead, the rate of inflation (how fast prices increase) slows. Taking advantage of lower prices today and waiting it out to see if inflation slows and home prices begin to fall both have their pros and cons.

For instance, if inflation continues to rise, purchasing a home now means spending less because you won’t need to borrow as much, and you can take advantage of lower interest rates. Conversely, if you purchase a home now and inflation does slow, you could end up spending much more on your monthly mortgage premium than if you waited.

However, it’s also possible that other buyers want to take advantage of today’s home prices and interest rates, which means much more competition. However, there’s no way to predict inflation, home prices, and how other buyers will respond.

That said, purchasing a home during inflation is still a good opportunity if it makes financial sense. As a homeowner, you save money on rent and instead spend it on your mortgage until you officially own your home. When you pay rent, you never get a return on your investment; that money is gone.

However, when you purchase a home, your home appreciates in value over time, so a home worth $350,000 today might be worth $600,000 in 20 years, depending on various factors. Therefore, your house, condo, or manufactured home is an investment, whereas your apartment or rental home is not.

Tips for Navigating the Housing Market During Inflation

You shouldn’t let inflation deter you from purchasing a home. Interest rates and home prices are typically higher during inflation, and you have less purchasing power. Still, inflation shouldn’t stop you if now is the right time to purchase a home based on your needs and financial situation.

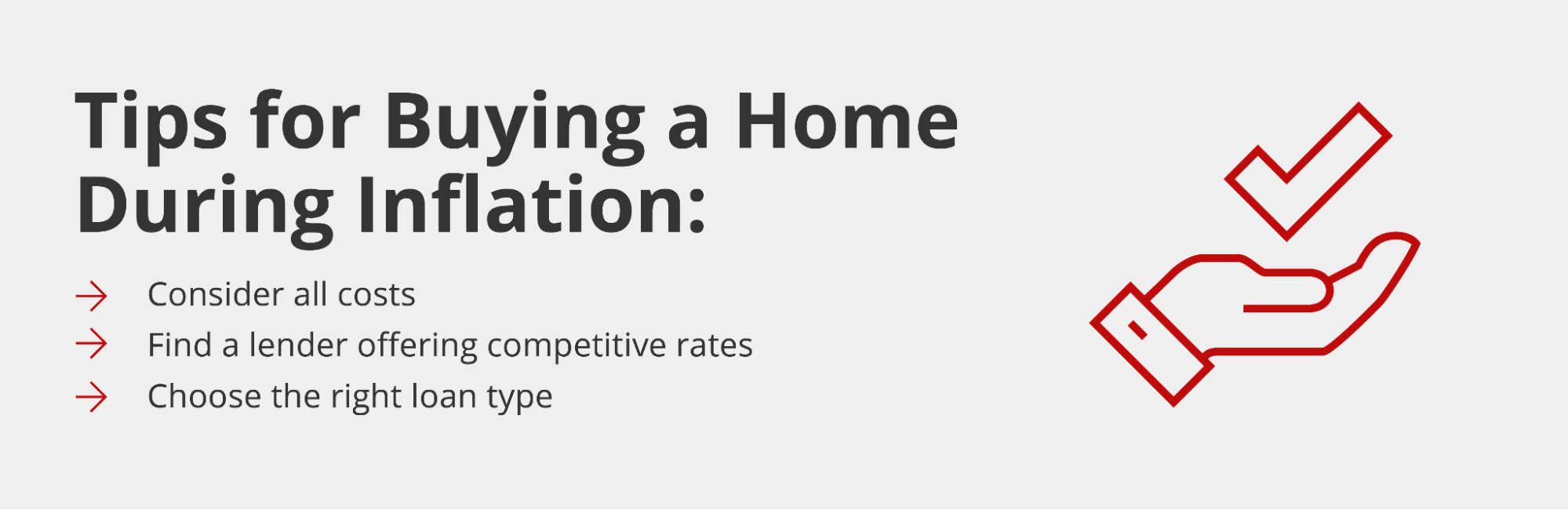

That said, inflation causes various shifts in the housing market, affecting house prices for better or worse. Since inflation can cause home prices to rise or fall depending on supply and demand, navigating the housing market during this time can be complicated. Here are a few tips to help if you’re considering purchasing a home during inflation.

Consider all costs

While inflation typically results in increased house prices and mortgage interest rates, there are other costs to consider when purchasing a home, such as closing costs, mortgage insurance, and moving costs. Additionally, costs for homes vary by location. For instance, a three-bedroom house in California typically costs much more than the same house in Ohio.

Before looking for homes, you should look at local housing markets where you’re interested in purchasing a home to find the average sales prices to see if they match your budget. You should also compare costs not associated with purchasing a home, such as groceries, electricity, entertainment, clothing, and so forth, which are more expensive during inflation.

Once you understand your budget, including your income versus expenses, you can determine how much money you have left over each month for your monthly mortgage payments. Of course, you should also include money saved for your down payment, closing costs, and any reserves the lender requires.

Find a lender with competitive rates

Your interest rate on a mortgage loan depends on various factors like your down payment amount, credit score, and loan terms. Still, inflation often leads to significantly increased costs of everything, including mortgage interest rates.

The Fed doesn’t set mortgage interest rates, but they do set federal interest rates for banks, and mortgage loans tend to follow suit. Simply put, when interest rates rise, mortgage rates rise with them.

If you want to purchase a home during inflation, you should always find a lender that offers competitive interest rates and get pre-approved as soon as possible before home prices rise higher. When you get pre-approved, you can lock in your interest rate while telling you the loan amount you may qualify for.

Choose the right type of loan

Knowing what happens to house prices during inflation can help you choose the right loan, depending on your unique financial situation. Luckily, there are many types of mortgage loans available. For instance, if you’re self-employed, you might benefit from a bank statement loan that allows you to qualify using alternative income verification methods. Meanwhile, you may still qualify for FHA loans, USDA loans, and VA loans if you have a low credit score.

Additionally, you can choose between a fixed-rate or adjustable-rate mortgage (ARM). A fixed-rate mortgage has an interest rate that stays the same throughout the life of the loan. Every month, you’ll pay the same amount. Conversely, an adjustable-rate mortgage is variable, with the initial mortgage rate similar to or lower than a fixed-rate mortgage. However, the interest rate changes based on market conditions after a set period.

Adjustable–rate mortgages usually cost more than a fixed rate mortgage during times of inflation. However, ARMs are fairly popular during inflation because they can be less expensive short-term. To avoid paying more interest during inflationary periods, many borrowers refinance to fixed-rate mortgages, allowing them to take advantage of lower rates during the initial period.

In addition to the type of loan you choose, the length of the loan can also impact your home buying power. For instance, interest rates tend to be lower if you have a shorter loan term, so you might choose a 15-year mortgage over a 30-year mortgage if you can afford the more expensive monthly payments.

Successfully Navigate the Housing Market During Inflation

Inflation and house prices can be tricky if you’re a buyer. While inflation doesn’t make buying a home impossible, it can affect your purchasing power and influence the type of home loan you choose. While home prices tend to rise with inflation, inflation doesn’t last forever, so it’s crucial to determine if now is the right time to purchase a home based on your goals and needs.

Wondering how inflation affects your home loan? Discuss your mortgage options with Griffin Funding today. We can help you understand the various costs associated with purchasing a home and help you get pre-approved so you can lock in your interest rate.

Take the first step and get started today!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Why is housing so expensive right now?

- Slow wage growth: In recent years, house prices have increased at a rate that has outpaced wage growth. This has played a role in pushing homeownership out of reach for those whose income can’t keep up with home appreciation, especially in big cities.

- Supply shortage: A key reason for high home prices is a supply shortage that has been growing for years. As metro areas continue to grow their populations, builders and developers are unable to keep up. This is due to things like restrictive zoning laws, the rising costs of building materials, high rates, and supply chain disruptions.

- High interest rates: Beginning in 2022, the Federal Reserve began raising rates to combat growing inflation. While this helped cool inflation, it has made it more expensive to get a mortgage. Additionally, the increase in rates has disincentivized current homeowners from selling, as they are reluctant to give up their low, locked in rate.

Will house prices go down?

Is inflation good or bad for the housing market?

A balanced housing market is typically best for both buyers and sellers, giving buyers the freedom to choose the house they want and sellers the ability to get a fair price for their home.

Is it best to buy a home when inflation is higher or lower?

That said, buying during higher inflation isn't necessarily a bad decision, it just requires more strategic planning. While interest rates may be higher, locking in a fixed-rate mortgage can help protect you from future rate increases. Keep in mind if rates drop in the future, you can always refinance your mortgage and secure a better rate.

Ultimately, the best time to buy depends on your personal financial situation, not just economic conditions. A strong credit profile, stable income, and long-term goals should guide your decision as much as the market.

Is real estate an inflation hedge?

For homeowners with a fixed-rate mortgage, inflation can actually work in your favor: your monthly payment stays the same while the value of your property and potential rental income may rise. This combination of stable debt and appreciating assets makes real estate a popular long-term strategy for protecting wealth against inflationary conditions.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...