Tax Benefits of Real Estate Investing

Tax Benefits of Real Estate Investing

KEY TAKEAWAYS

- Investing in real estate can help diversify your portfolio and build wealth over time, and it has several tax advantages other types of investments don’t.

- Tax deductions for properties you hold, whether rental properties or fix and flip properties, can help you reduce your tax burden.

- If you want to take advantage of the tax benefits of real estate investing without holding property, you may prefer a REIT or tax-advantaged retirement account.

Investing in real estate can help you build wealth over time while expanding your portfolio with new opportunities. Some of the key benefits of real estate investing include depreciation, investment property tax deductions, and advantageous capital gain tax rates. Read on to learn more about the tax benefits of rental property and how to start investing in real estate.

Does Investing in Real Estate Reduce Taxes?

Investing in real estate can sometimes reduce taxes, especially compared to other types of investments. However, situations vary, and investing in real estate isn’t necessarily a way to reduce your tax burden. When you invest in real estate, you earn an income, and that income is subject to taxation, so investing in real estate may increase your tax burden.

However, there are several tax benefits of investing in real estate that might help reduce your tax burdens, whether you’re a house flipper, landlord, or full-time investor.

Let’s take a look at the top benefits of real estate investing to help you understand how it works and how real estate investments may reduce your tax burden.

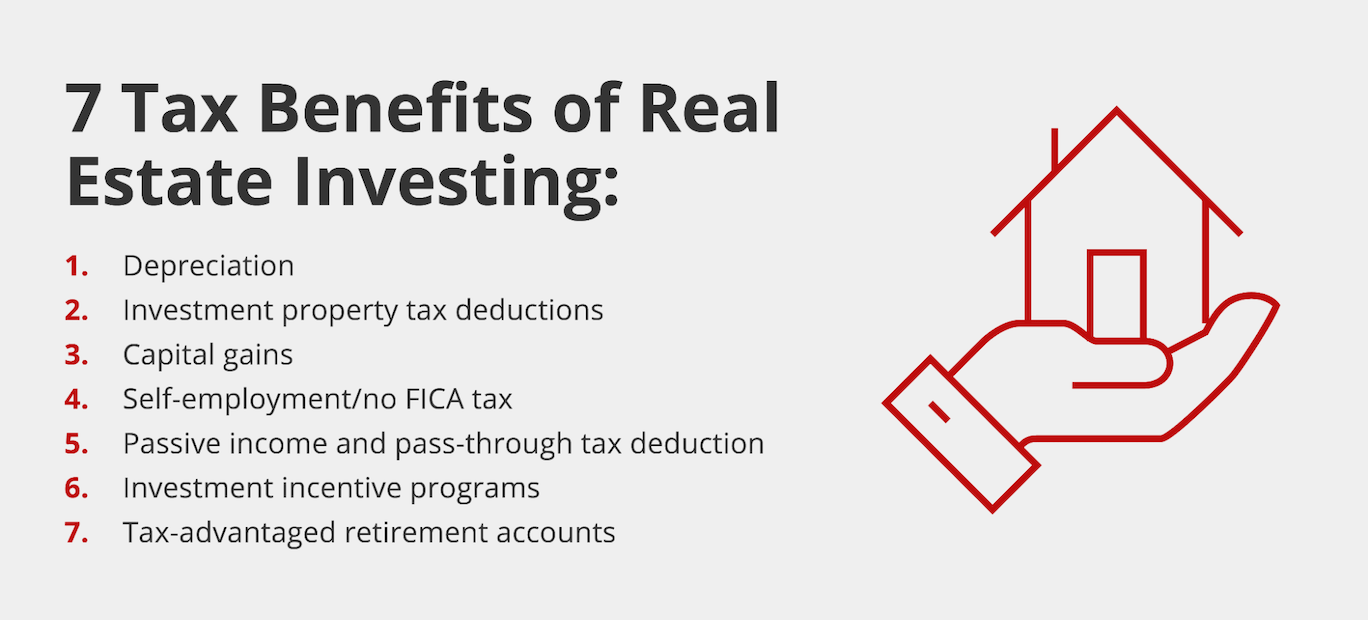

1. Depreciation

Depreciation is the loss of value for a property or another type of asset. Depreciation in real estate allows investors to deduct the cost of a property over time due to general wear and tear. This is one of the top tax benefits for real estate investors because you can claim a depreciation deduction on a rental property even if the market value has increased.

- Residential real estate properties are typically depreciated over a period of 27.5 years. This means that you can claim a depreciation deduction on the property every year for those 27.5 years, provided the property continues to meet the minimum requirements to be considered depreciable.

- Only the physical structure is depreciated (not the land itself).

- Depreciation begins when a property is ready to rent (i.e. when it’s placed in service).

- Once you sell your property, you’ll pay income tax on any claimed depreciation because the IRS calculates capital gains based on your profits.

Why this matters:

Investment property tax deductions like depreciation reduce your taxable income, so you’ll pay less in taxes for that year while maintaining cash flow.

Bonus depreciation

Using the bonus depreciation deduction, real estate investors can deduct up to 100% of qualifying property costs in the first year of service instead of spreading the deductions over decades.

- Bonus depreciation can apply to items like appliances, fixtures, and qualifying home improvements.

- The 2025 One Big Beautiful Bill Act (OBBBA) permanently reinstated 100% bonus depreciation, so assets placed in service after January 19, 2025, can qualify for this deduction.

Why this matters:

100% bonus depreciation can significantly lower your tax burden in the early years of ownership and make it easier to maintain positive cash flow.

2. Investment property tax deductions

As an investor, you’re a business owner, so you can deduct business expenses from your taxable income. You’re allowed to deduct expenses related to the management or maintenance of your rental property, which may include the following:

- Property taxes

- Insurance

- Management costs

- Maintenance

- Utilities

- Repairs

- Advertising

- Legal and accounting fees

- Business operations equipment

Why it matters:

Owning a rental property provides investors with a wide range of deductions related to operating expenses and maintenance, which can directly lower taxable income.

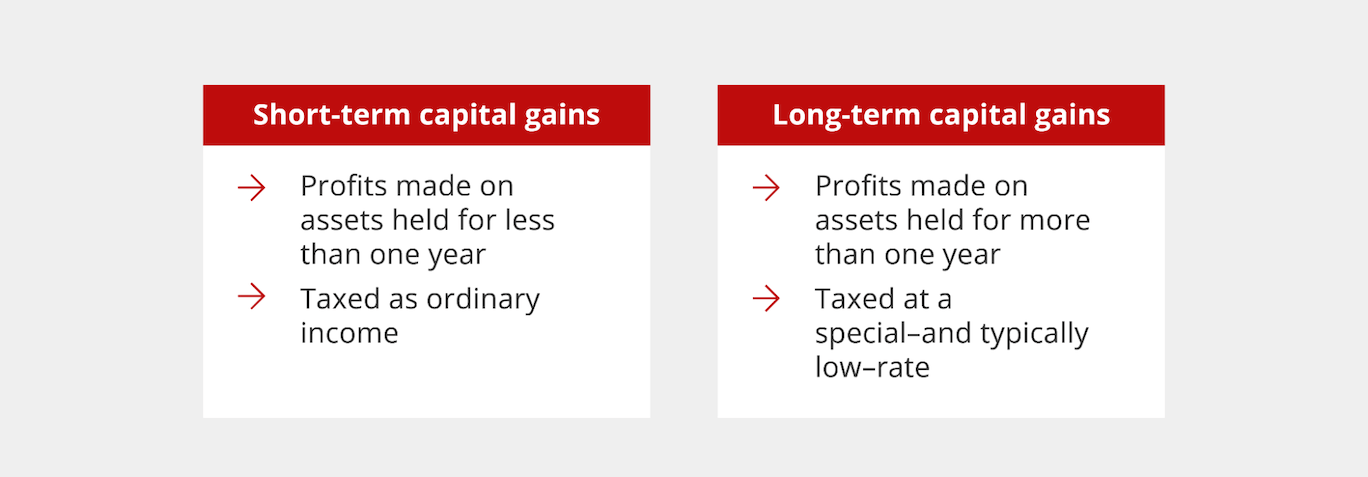

3. Capital gains

Whenever you sell an investment property that grows in value, you’ll be required to pay taxes on your capital gains, which are applied to the appreciation — or increase in value — of the property. However, the rate at which you’re taxed depends on how long you’ve held onto the asset.

Short-Term Capital Gains

- Short-term capital gains refer to the profit earned on an asset you’ve held for less than 12 months.

- Taxed as ordinary income, which means you’ll pay a higher rate.

Long-Term Capital Gains

- Assets that you’ve held for more than 12 months are taxed as long-term capital gains.

- Long-term capital gains rates are lower than short-term capital gains rates.

Why it matters:

Short vs. long-term gains aren’t necessarily a tax benefit, but it’s important to keep in mind that you can benefit from longer-term investments if you can keep them for more than a year.

4. Rental income not subject to FICA tax

Rental income is not subject to Federal Insurance Contributions Act (FICA) taxes like regular self-employment income.

- The self-employment tax rate is 15.3%. Many types of traditional self-employment income are taxed at this rate.

- Rental income is typically exempt from FICA taxes.

Why it matters:

An exemption from FICA taxes is a significant tax advantage compared to other self-employed income streams. Investors can also buy investment property in an LLC to reduce self-employment tax and protect personal assets.

5. Passive income and the pass-through tax deduction

Your rental income can be considered a passive qualified business income (QBI). A pass-through deduction allows you to deduct up to 20% of your QBI on your personal taxes when you own a rental property.

- Example: If you make $100,000 from rental income, you may be able to deduct up to $20,000 from your taxable income.

- Though this tax benefit was set to expire in 2025, the OBBBA made this permanent for 2026 and expanded phase-in thresholds.

Why it matters:

The pass-through deduction can significantly reduce taxable income for rental property owners.

6. Investment incentive programs

Investors may be able to take advantage of investment incentive programs depending on the structure of their business. Investment incentive programs are designed to provide additional tax savings on several types of investments and income.

Opportunity zones

- The government created opportunity zones to encourage investment in lower-income communities.

- Real estate investors can invest in designated areas through Qualified Opportunity Funds and enjoy tax benefits such as:

- Deferred capital gains taxes.

- Potential tax-free gains after 10 years.

- Growing your gains by 10% for holding the fund for five years, or holding the fund for seven years and growing your gains by 15%.

1031 exchanges

- Enables investors to defer capital gains taxes when they reinvest in a property of greater or equal value than the one sold.

- 1031 exchanges don’t reduce your tax bill, but you can defer paying capital gains taxes until you decide to cash out.

Why it matters:

These tax-advantaged strategies make it possible for real estate investors to defer or reduce their taxes over time.

7. Tax-advantaged retirement accounts

Retirement accounts like Roth IRAs, SDIRAs and 401(k) plans allow you to invest in real estate without purchasing property. For instance, you can invest in stocks, bonds, private and commercial real estate, real estate investment trusts (REITs), and other real estate holdings.

- With a tax-advantaged retirement plan, your gains are tax-deferred, meaning anything you earn won’t be taxed until you decide to pull money out of your retirement account.

- There are also tax-advantaged retirement accounts like Roth IRAs that aren’t subject to taxes when withdrawn because you pay taxes on the money deposited in them.

Why it matters:

Tax-advantaged retirement accounts allow investors to grow their wealth without dealing with an immediate tax liability. Additionally, investing in real estate via retirement accounts can present a more affordable entry point than actually purchasing property.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

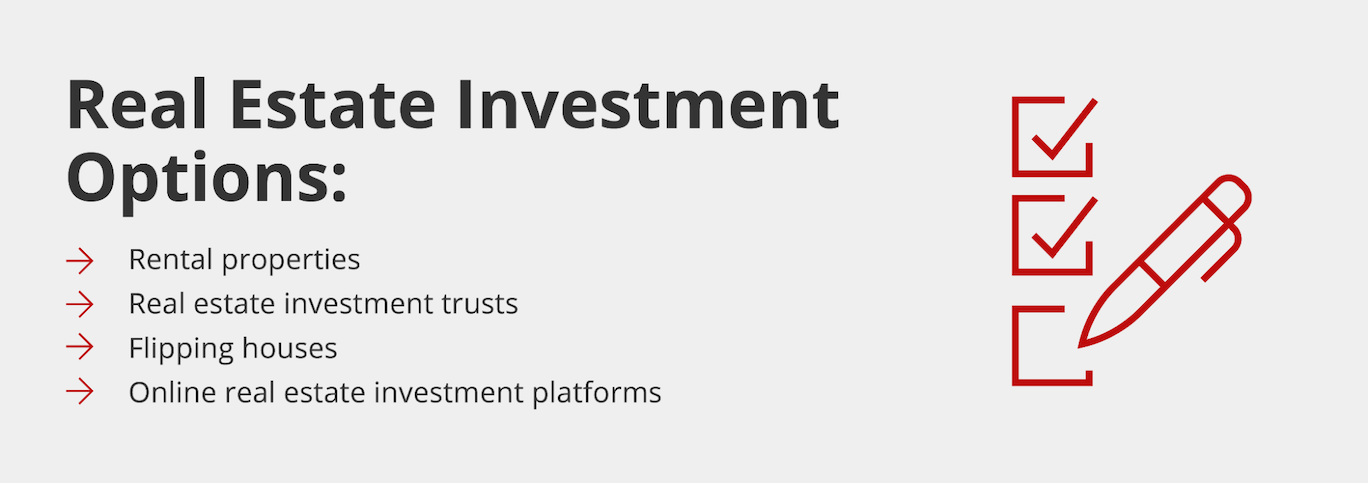

Real Estate Investment Options

Let’s take a closer look at a few ways you can invest in real estate and their tax benefits.

Rental property

When you invest in rental property, you become a landlord. You can purchase a single or multi-family property, condo, apartment, residential and commercial properties, or even a manufactured home and earn rental income.

Investing in a rental property is one of the most common ways to build wealth and create a passive income stream. You can purchase a single or multi-family property, condo, apartment, residential and commercial properties, or even a manufactured home and earn rental income.

Key tax benefits of rental properties include:

- Pass-through deduction: Deduct up to 20% of qualified rental income with the pass-through deduction.

- Depreciation: Claim the depreciation deduction over 27.5 years.

- Mortgage interest deduction: Mortgage interest on a rental property is often tax deductible.

- Operating expense deductions: Deduct expenses for maintaining the property and operating the business, which may include property taxes, insurance, repairs and maintenance, utilities, and marketing costs.

- 1031 exchange: Use a 1031 exchange to defer capital gains if you sell your rental property and buy another one of equal or lesser value.

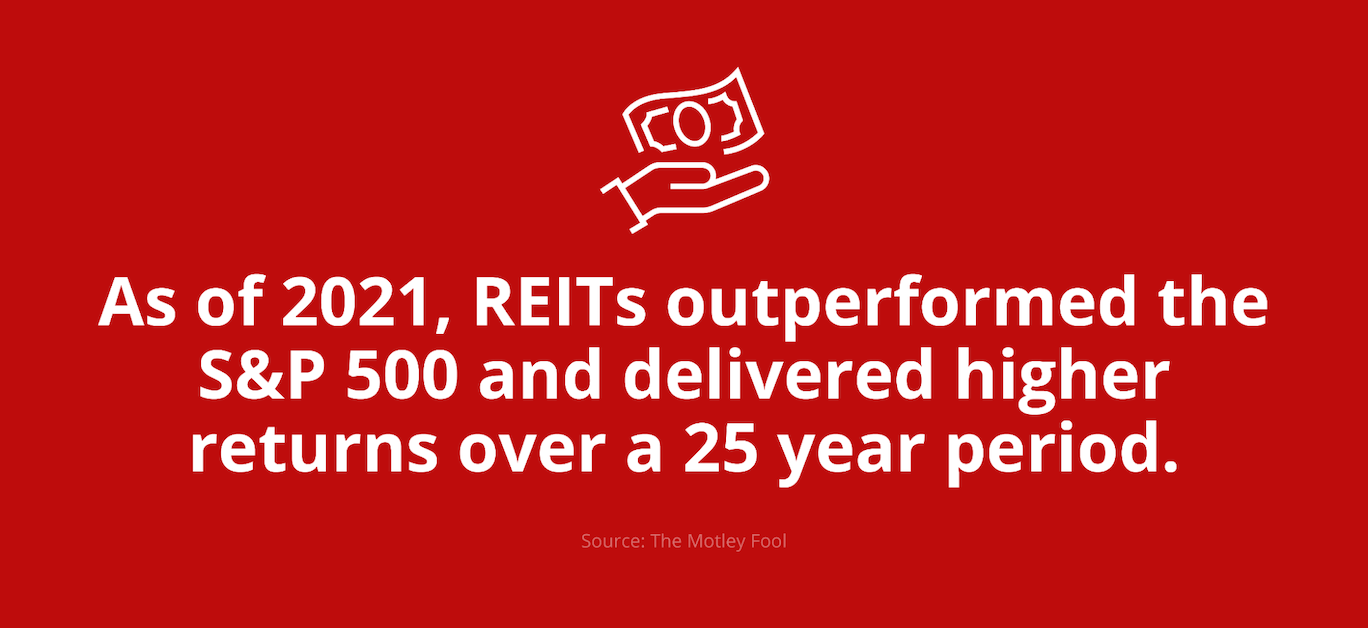

Real estate investment trusts

A real estate investment trust (REIT) is a company that owns or finances real estate. When you invest in a trust, you can get the returns of real estate investment without actually owning the property. Instead, it’s similar to owning a stock that you can sell at any point. REITs are liquid, giving you more flexibility and control of your gains, and they have several advantages over other types of investments.

Key benefits of REITs include:

- Earn profits without a mortgage: No property management or mortgage requirements.

- Invest in real estate with less money: Accessible entry point with low upfront costs.

- High liquidity: Buy or sell REITs like stocks.

- Pass-through deduction: Deduct up to 20% of qualified REIT income.

- No corporate-level taxation: Avoid double taxation at the company level.

House flipping

House flipping is another popular real estate investment method. However, because the goal is to fix and flip as many houses as possible to increase your profits, flippers are often subject to short-term capital gain taxes.

House flipping involves purchasing properties at a lower price, renovating them, and then turning around and selling them for a profit. This real estate investment strategy focuses on generating short-term profits rather than long-term gains. In this case, properties are often held for under a year, meaning investors will be subject to higher short-term capital gains rates.

Key benefits of house flipping include:

- Short-term profits: Real estate is typically a long game, but house flipping allows investors the opportunity to quickly turn a profit.

- Operating expense deductions: You may be able to deduct costs related to property renovation, labor, and business expenses.

- 1031 exchange: Potentially defer capital gains when you use a 1031 exchange to reinvest in another property.

Online real estate investment platforms

Online real estate investment platforms allow you to invest in real estate without holding property, making them more convenient and flexible if house flipping or becoming a landlord don’t interest you. These platforms enable groups of investors to pool money and invest in large-scale real estate projects without owning the property directly.

Key benefits of online real estate investment platforms include:

- Earn passive income: Once you’ve invested, you won’t be responsible for managing the project or the property.

- Diversify your portfolio: Access commercial real estate opportunities and diversify your investment portfolio with larger-scale development projects.

- Pass-through deduction: You may benefit from pass-through tax advantages in some cases.

Start Reaping the Tax Benefits of Real Estate Investing

The tax benefits of investing in real estate can help you determine when is the right time to purchase property and what type of investment is right for you. Of course, you shouldn’t base your decision on tax advantages alone. Even though some real estate investments come with higher or more taxes, they could also come with higher profits.

Don’t forget that purchasing a primary residence is a type of real estate investment because your property is likely to appreciate in value over time. There are many tax benefits to purchasing a home, whether for your family or as an investment property.

Ready to become a real estate investor or fund your next investment? Get started online with Griffin Funding today or contact us to learn more about the tax advantages of rental property. We can help you find the best investment property loan based on your goals, property type, and financial situation.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What is a cost segregation study in real estate?

What is Real Estate Professional Status (REPS)?

- Spend more than 750 hours per year in real estate activities.

- Spend more time in real estate than in any other profession.

- Materially participate (spend more than 50% of their working time over the tax year) in trades or business involving their investment properties.

What is Schedule E and how do landlords use it?

- Rental income

- Mortgage interest

- Property taxes

- Insurance

- Repairs and maintenance

- Utilities

- Depreciation

- Property management fees

- Other operating expenses

What is the difference between repairs and capital improvements?

- Fixing leaks

- Repainting walls

- Replacing broken fixtures

- Minor plumbing repairs

- Roof replacements

- HVAC installations

- Room additions

- Major kitchen remodels

Do I owe self-employment tax on rental income?

How can real estate investors legally pay little to no taxes?

- Depreciation

- Bonus depreciation

- Cost segregation studies

- 1031 exchanges

- Operating expense deductions

- Pass-through deductions

Can rental property losses offset ordinary income?

Is depreciation mandatory for rental properties?

Are short-term rentals taxed differently than long-term rentals?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Why vacation rental investors are spending more time on market research before buying

For investors already holding properties or considering new purchases, miscalculating revenue in this environm...

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...