Non-Conforming Loans: What They Are and How They Work

KEY TAKEAWAYS

- Non-conforming loans are home loans that don’t adhere to Fannie Mae and Freddie Mac guidelines for resale.

- These loans are ideal for individuals with low credit scores and down payment amounts or those wanting to purchase a home in an expensive area.

- There are several types of non-conforming loans with different requirements, and understanding your options can help you find the right mortgage.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformUnderstanding the difference between conforming and non-conforming loans is key to finding the right mortgage. While conforming loans follow strict guidelines, non-conforming loans offer more flexibility for buyers with unique financial situations. In this post, we explain what a non-conforming loan is and the differences between conforming vs non-conforming loans. Using this information, you can determine if a non-conforming loan could be the solution to securing your dream home.

When you’re ready to buy a house and learn about the mortgage process, you’ll come across mortgage terms that seem intimidating and confusing. Terms like “conforming” and “non-conforming loans” can make applying for a home loan even more confusing and daunting. However, knowing the difference between these types of loans can ensure you make the right decision for your family and wallet.

Loans fall under several categories, including non-conforming and conforming loans. Conforming loans are your typical conventional home loan with strict lending criteria, which make it challenging for many people to be eligible. Luckily, for individuals who don’t meet conforming loan requirements, there are non-conforming loans, also referred to as non-agency loans.

But what are non-conforming loans, and how do they differ from conforming loans? Keep reading to learn more about non-conforming mortgage loans, including what they are, how they work, and their pros and cons.

KEY TAKEAWAYS

- Non-conforming loans are home loans that don’t adhere to Fannie Mae and Freddie Mac guidelines for resale.

- These loans are ideal for individuals with low credit scores and down payment amounts or those wanting to purchase a home in an expensive area.

- There are several types of non-conforming loans with different requirements, and understanding your options can help you find the right mortgage.

What Is a Non-Conforming Loan?

The non-conforming loan definition is a little complex if you don’t understand how the mortgage process works behind the scenes. To understand what a non-conforming loan is, you must understand how the mortgage market works.

Fannie Mae and Freddie Mac are entities that have guidelines for loan limits and qualifications because they buy mortgages from lenders and sell them on the secondary mortgage market. These companies guarantee most of the mortgages in the United States but don’t originate or service the loans. Instead, they purchase and guarantee loans through the secondary mortgage market.

These companies are federally backed and provide stability to the mortgage market, making homeownership more affordable for borrowers by purchasing mortgages from lenders and reselling them to investors. Ultimately, purchasing mortgages frees up a lender’s capital, allowing them to service more loans. To do this, government-sponsored enterprises (GSEs) like Fannie Mae and Freddie Mac have specific requirements for borrowers and loans set by the Federal Housing Finance Agency (FHFA), including maximum loan limits and lending criteria, such as maximum debt-to-income (DTI) ratios, minimum credit scores, and down payments.

Borrowers won’t have any contact with these entities, but they’ll know when their mortgage is sold when they get a letter in the mail.

Non-conforming loans are any loans that don’t meet — or conform to — Fannie Mae and Freddie Mac guidelines. Loans may not conform if they don’t meet any one of the FHFA requirements or if the loan amount exceeds specific limits. Unfortunately, this means they’re more difficult for lenders to sell, forcing them to keep them in their investment portfolios. That said, there are several non-conforming loans backed by the government instead of GSEs, making them easier to sell on the secondary mortgage market.

How Do Non-Conforming Loans Work?

Non-conforming loans typically work best for individuals who want to purchase a home without putting down a hefty down payment, have lower credit scores, or want to purchase a home in a competitive market.

How a non-conforming loan works depends on the specific type. For example, VA loans don’t require a down payment, while FHA loans do. Conversely, some individuals will choose a jumbo loan if they need to purchase a more expensive home that exceeds the Fannie Mae and Freddie Mac loan limits.

Non-conforming loans work similarly to conforming loans. You’ll still complete an application to qualify and provide proof of income and other documents for the lender to verify. Each type of non-conforming loan has different lending criteria, benefits, and use cases. Many non-conforming loans offer a greater degree of flexibility when it comes to things like:

- Proof of income: Some non-conforming loans are able to accommodate borrowers who can’t prove income via tax returns, and instead accept bank statements, asset statements, and other alternative income documentation.

- Credit score: Many non-conforming loans are more lenient when it comes to minimum credit score requirements.

- Down payment amount: While some non-conforming loans require a down payment, others do not. Additionally, the minimum down payment requirement can vary depending on the specific type of loan you’re interested in.

- Loan amount: Non-conforming loans are able to provide borrowers with larger loan amounts. With these types of loans, borrowers may also be able to secure an unconventional loan term that is longer or shorter than is typical.

Non-Conforming Loan Qualification Requirements

Conforming loans become non-conforming loans when they don’t meet the guidelines set forth by GSEs like Freddie Mae and Freddie Mac. Qualifying for a non-conforming loan is usually easier because of the more flexible lending criteria. Some of the key qualifications for non-confirming loans include the following:

- Credit score: Non-conforming loans are ideal for borrowers with a credit score lower than the minimum requirement for conforming loans. Therefore, individuals with credit scores lower than 620 can still qualify for a non-conforming mortgage loan.

- Loan size: Non-conforming mortgage loans can exceed the loan limits set by GSEs. The conforming loan limit is $806,500 in 2025 for most of the country. Any loan amounts higher than that are considered non-conforming.

- DTI ratio: Conforming loans typically have a maximum DTI of 43%, while non-conforming loans often allow a DTI as high as 55%.

- Down payment required: Different types of loans have different down payment requirements. If you put down less than the required amount, it makes your loan non-conforming.

It’s important to note that the requirements vary for non-conforming loans. However, non-conforming loans generally are ideal for borrowers who can’t meet the requirements of conforming loans.

Conforming vs. Non-Conforming Loans

The main difference between conforming and non-conforming loans is that conforming loans adhere to strict standards, allowing Fannie Mae and Freddie Mac to purchase and resell them on the secondary mortgage market. On the other hand, non-conforming loans are much more difficult to sell since they can’t be sold to the two largest mortgage buyers in the country. Here are a few other key differences to consider:

- Cost: The loan amount you receive from a lender isn’t your total cost of the loan. Every mortgage loan, whether conforming or non-conforming, comes with interest. Non-conforming loan rates are typically higher because they carry more risk for the lender. They’re not easily sold to another company or investor, which lenders may view as a risk because it means they can’t sell them to increase cash flow to service more loans.

- Limits: Non-conforming loans can exceed the conforming loan limits, making them jumbo loans. If a home loan amount exceeds conforming loan limits, it can’t be purchased by Freddie Mac or Fannie Mae, making it non-conforming.

- Lending criteria flexibility: Conforming loans have strict guidelines for borrowers, so they can be purchased and resold on the secondary mortgage market. Any home loans given to borrowers that don’t meet these requirements are considered non-conforming mortgages. For example, to qualify for a conforming loan, you must meet the specific credit score guideline of 620 or higher. Conversely, you may qualify for a non-conforming loan with a much lower score. Other flexible requirements include higher DTI ratios and lower down payment requirements.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

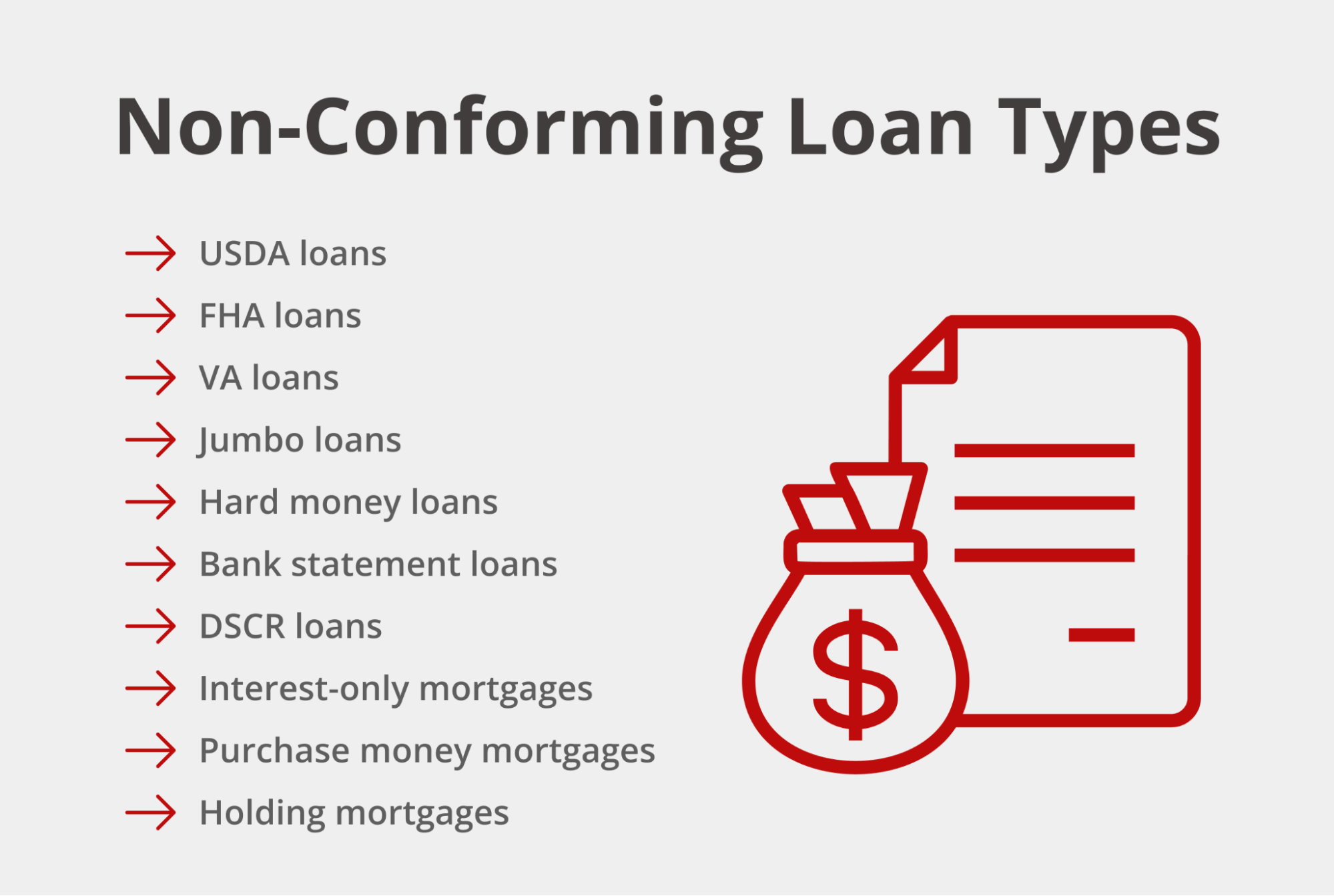

The Different Types of Non-Conforming Loans

There are several types of non-conforming loans to choose from. Remember, any loan that doesn’t meet the strict lending criteria of GSEs is considered a non-conforming loan. The most common types of non-conforming mortgages include the following:

Government-Backed Loans

Government-backed loans are technically non-conforming because they don’t meet Fannie Mae and Freddie Mac’s lending requirements. However, they’re not defined this way in the mortgage industry because they’re not conventional mortgages. Conventional mortgages are those that aren’t backed or guaranteed by the government. Since these loans are, they’re non-conventional and non-conforming. Below are three types of non-conforming government-backed loans:

USDA Loans

USDA loans are guaranteed by the Rural Development Guaranteed Housing Loan Program from the United States Department of Agriculture (USDA) and offer 0% down payment options, low-interest rates, and a more lenient minimum credit score requirement. The caveat is that these loans are only available for properties in eligible rural areas.

Besides the option to put 0% down on a home, the most significant benefit of these loans is that they typically come with more competitive interest rates because the government is taking on more risk. Additionally, these loans don’t require borrowers to pay traditional private mortgage insurance (PMI).

These loans can be difficult to qualify for because a borrower’s income can’t exceed 115% of the median income of the area where the property is located. In addition to this rule, borrowers must have a dependable income and a credit score of at least 640.

FHA Loans

FHA loans are backed by the Federal Housing Administration (FHA) and available for anyone, including first- and second-time homebuyers. This mortgage program allows for down payments as low as 3.5% and credit scores as low as 580. However, the requirements vary. For instance, you’ll need a down payment of at least 10% if you have a low credit score.

While FHA loans don’t require private mortgage insurance (PMI) for down payments of less than 20%, you will be required to pay an upfront mortgage insurance premium (MIP), which can increase the total cost of the loan. This premium is paid at closing and can be financed into the loan. You’ll have to pay it all at once and upfront as an on-time additional charge.

So what makes an FHA loan non-conforming? Ultimately, an FHA loan is non-conforming when it exceeds loan limits. However, their lending criteria differ from conventional loans, which typically require higher down payments and credit scores.

VA Loans

VA loans are backed by the Department of Veterans Affairs and are only available for eligible active duty service members, veterans, and surviving spouses. However, if you qualify for a VA loan, there’s no reason not to take advantage of it because it doesn’t require a down payment. However, putting down more than 0% can help you get better terms and lower non-conforming rates. VA loans also have more lenient credit score requirements and no loan limits.

In addition, if you choose to put down 0%, you won’t have to worry about mortgage insurance. VA loans are sold to Ginnie Mae. Ginnie Mae is not a GSE but rather a wholly-owned government corporation under the HUD umbrella.

Jumbo Loans

Jumbo loans are a type of non-conforming conventional loan. A conventional loan is one that the government does not back. Since jumbo loans aren’t backed by the government and exceed the conforming loan limits, they’re conventional, non-conforming loans. These loans are ideal for individuals who want to purchase a home in a high-cost area. However, lenders consider jumbo loans riskier because they’re available in higher amounts. Typically, borrowers need lower DTI ratios and higher credit scores to qualify. Additionally, they’ll need income that proves their ability to repay the loan.

Other Types of Non-Conforming Loans

Apart from government-backed non-conforming loans and jumbo loans, there are several other types of home loans that qualify as non-conforming, such as:

- Hard money loans: Hard money loans are a type of asset-based loan. However, instead of converting your assets into income to qualify, they’re short-term loans that use assets or property as collateral for the loan. They’re most commonly used by real estate investors or house flippers who may not qualify for other types of investment property loans. These private money loans have higher interest rates and carry more risk for the lender and the borrower.

- DSCR loans: Debt service coverage ratio (DSCR) loans help real estate investors qualify for mortgages based on their property’s income rather than personal earnings. Lenders calculate DSCR by dividing a property’s net operating income by its mortgage payment, ensuring rental income covers the loan. These loans are ideal for investors in rental properties, short-term rentals, or fix-and-flip projects who may not have traditional income documentation. While DSCR loans offer flexibility, they often come with higher interest rates and down payment requirements.

- Bank statement loans: Bank statement loans cater to self-employed individuals, freelancers, and small business owners who lack W-2 income but have strong cash flow. Instead of tax returns, lenders use 12 to 24 months of bank statements to verify income. These loans work well for those with fluctuating earnings but steady deposits. While they provide flexibility, they often require higher credit scores, larger down payments, and slightly higher interest rates. Borrowers can use them for primary homes, second homes, or investment properties.

- Interest-only mortgages: Interest-only mortgages allow borrowers to save money on the first portion of their loan by paying towards the interest instead of the principal balance. There are two types of interest-only mortgages: adjustable-rate and fixed-rate, and whichever one you choose can impact your total loan amount. Interest-only mortgages are ideal if you want to keep your monthly payments low for the first portion of the loan, allowing you to save money to pay higher amounts later.

- Purchase money mortgages: A purchase money mortgage, also known as seller financing, is a type of mortgage that the seller gives directly to the buyer. This can happen if a buyer doesn’t qualify for traditional banking, allowing the seller to set the down payment, interest rate, and closing fee requirements. These non-conforming loans typically only occur when the buyer has a poor credit score or high DTI and doesn’t qualify for another type of loan. However, they’re difficult to come by because it means the seller has to put in extra work to ensure that the buyer can afford the home and pay for it.

- Holding mortgages: A holding mortgage is another type of non-conforming loan where the seller acts as the lender or bank. Under this type of mortgage, the homeowner is the lender and gives the buyer a loan to finance the home. With a holding mortgage, the seller retains the property title until the loan is fully paid off in monthly installments.

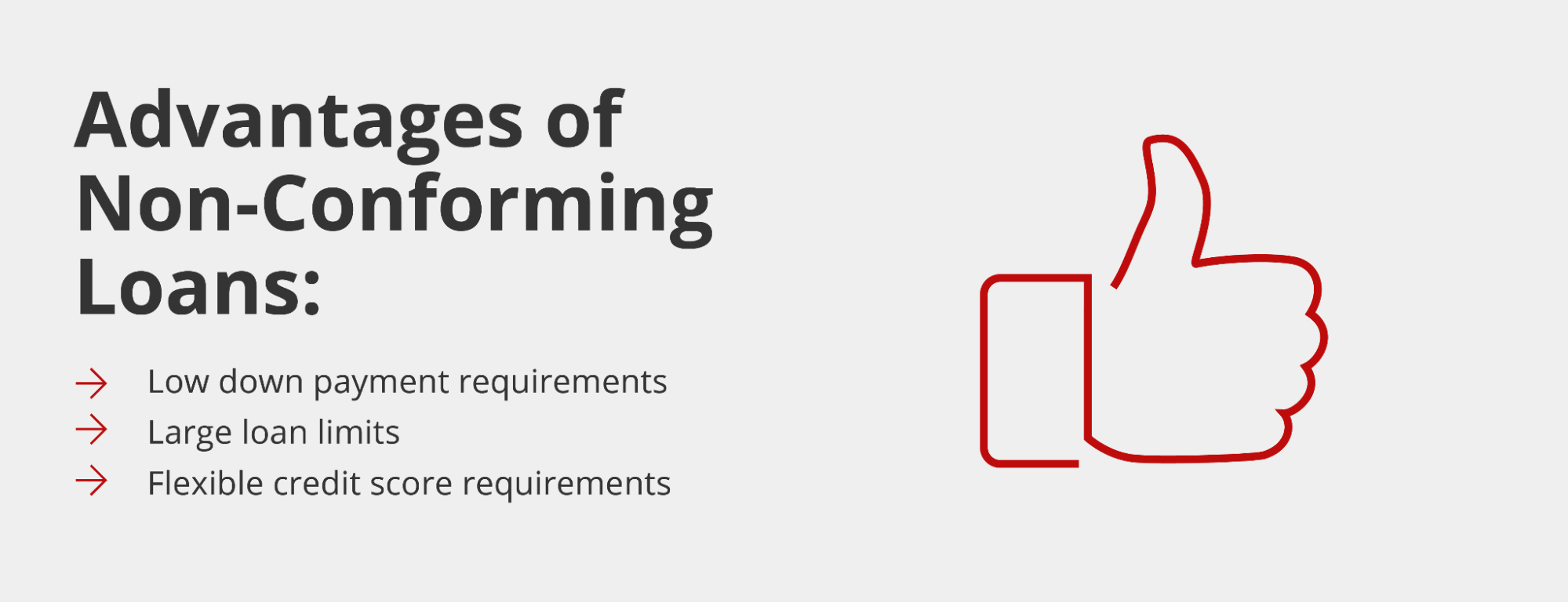

Pros and Cons of Non-Conforming Loans

Compare the pros and cons of non-conforming mortgage loans to see if this financing option aligns with your needs and goals.

Advantages Of Non-Conforming Mortgages

Non-confirming mortgages allow more borrowers to qualify for a home loan because they have more flexible lending requirements. A few advantages of non-conforming mortgages include the following;

Lower down payment requirements

Non-conforming loans typically have lower down payment requirements, with some allowing you to purchase a home with a 0% down payment. For example, USDA and VA loans allow borrowers to put down as little as they want on a home. However, both loan programs have strict requirements for borrowers to be eligible for these benefits. In addition, a higher down payment can help you get lower non-conforming rates to reduce the total cost of the loan.

Larger loan limits

Some non-conforming mortgages have larger loan limits. For example, jumbo loans allow borrowers to purchase properties with loans that exceed the Fannie Mae and Freddie Mac conforming loan limits, allowing them to become homeowners in high-cost cities or competitive markets.

Lower credit score requirements

Non-conforming loans allow individuals with credit scores lower than 620 to qualify for a loan. However, the credit score requirements vary by loan program and lender, so you should do your research and know your credit score before applying.

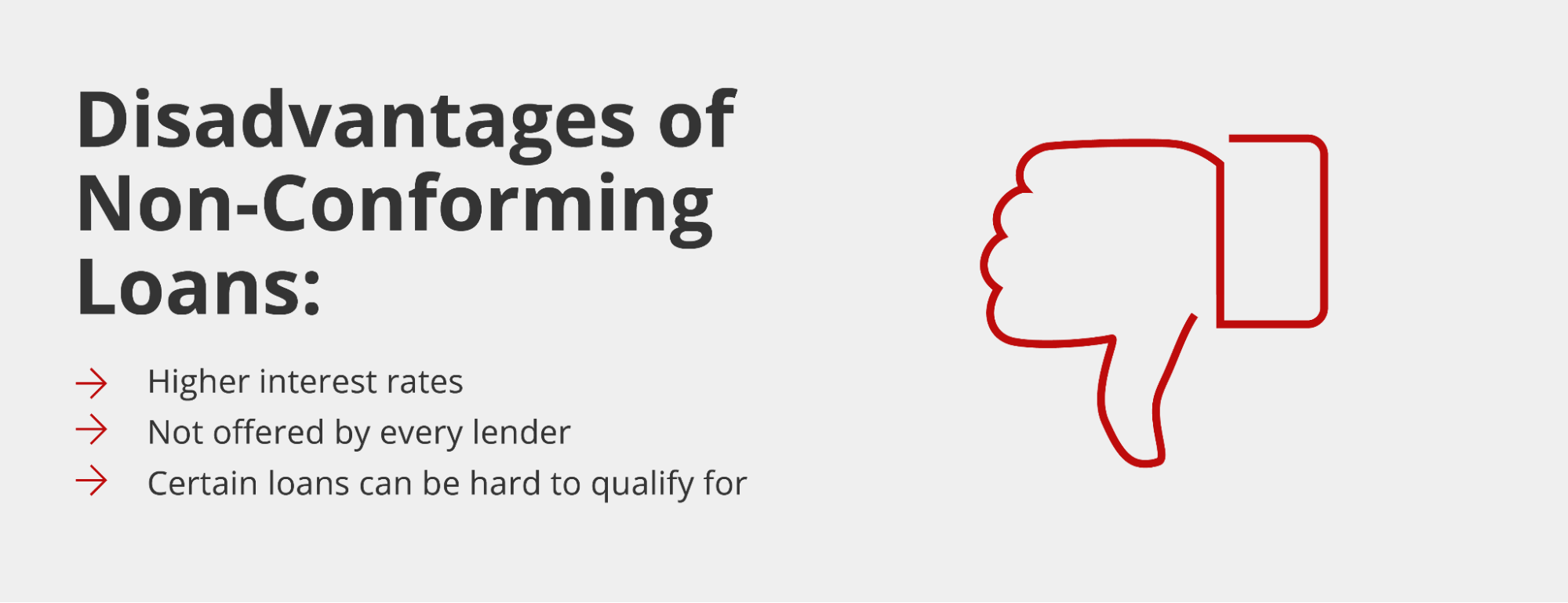

Disadvantages of Non-Conforming Mortgages

No mortgage is perfect. Some loans are better suited for particular borrowers than others. There are a few drawbacks to non-conforming mortgages, such as:

Higher interest rates

Non-conforming loan rates are usually higher than conforming ones because they carry more risk to the lender. Since the lender can’t sell them to Fannie Mae or Freddie Mac, they’re harder to sell and can stay in a lender’s portfolio for many years, making it more challenging for them to free up the cash flow to service other loans. This risk for the lender typically translates to higher interest rates for the borrower. A higher interest rate means paying more over the life of the loan, so it’s crucial to determine whether this type of loan is worth it. In addition, since it increases your monthly mortgage payments, some borrowers may not be able to afford it.

That said, some non-conforming loans are backed by the federal government, making them less risky for the lender. For example, VA loans are sold to Ginnie Mae and typically come with competitive or lower interest rates than traditional conforming loans.

Accessibility

Not all lenders offer non-conforming loans, so you may have to do your research to find one in your area. Since these loans are more challenging to sell on the secondary mortgage market, your local bank may not offer them.

May be harder to qualify for

In most cases, non-conforming loans are easier to qualify for because they have more flexible lending requirements, such as lower down payments and credit scores accepted. However, some non-conforming loans can be harder to qualify for. For example, jumbo loans typically require a lower DTI, higher credit score, and hefty down payment because they offer large loan limits that exceed those of conforming loans.

Non-Conforming Mortgage Rates

Non-conforming mortgage rates can vary depending on the type of loan and borrower qualifications. In many cases, non-conforming loans tend to have higher interest rates than conforming loans because they carry more risk for lenders. This is especially true for jumbo loans, hard money loans, and certain alternative mortgage products, which lack the backing of government agencies and involve larger loan amounts or unconventional borrower profiles.

However, government-backed non-conforming loans — such as VA loans, USDA loans, and FHA loans — actually offer highly competitive rates. Because these loans are insured by the government, lenders face less risk, allowing them to offer lower interest rates to eligible borrowers.

Interest rates are partially influenced by the type of loan you choose, but other factors play a role as well:

- Income level: Lenders look at your income stability, consistency, and debt-to-income (DTI) ratio to determine your ability to repay the loan. A lower DTI ratio (below 43%) is preferred, as it indicates that your monthly debt obligations are manageable compared to your income.

- Credit score: Your credit score is one of the most significant factors in determining your mortgage rate. Higher scores (typically 700 or above) qualify for better rates, while lower scores may result in higher interest rates due to increased lender risk.

- Loan type: The type of non-conforming loan you choose impacts your interest rate. Government-backed loans (VA, FHA, USDA) generally offer lower rates because they are insured by the government.

- Loan amount: Larger loan amounts, such as jumbo loans, often come with higher interest rates because they exceed conforming loan limits and cannot be sold to Fannie Mae or Freddie Mac.

- Down payment amount: A larger down payment reduces the lender’s risk, which can lead to a lower interest rate. Borrowers who put down 20% or more typically receive better rates.

- Market conditions: Interest rates fluctuate based on economic factors like inflation, Federal Reserve policies, and housing market trends.

See If a Non-Conforming Loan Is Right For You

A non-conforming mortgage might be right if you want a lower down payment, have a low credit score, or need a loan that exceeds conforming loan limits. However, these loans typically come with higher interest rates that can hurt your eligibility or make your loan more expensive if you choose to move forward.

Talk to a Griffin Funding mortgage specialist today to learn more about non-conforming loans and see if you qualify. If you don’t qualify, don’t worry. We have many loan programs designed with different types of borrowers in mind, including conventional, FHA, and non-QM loans, to help you secure a loan to purchase your dream home. In fact, you can use our free Griffin Gold app to explore and compare mortgage options while also leveraging smart financial management tools.

Reach out to Griffin Funding today to learn more about non-conforming mortgages and see what non-conforming mortgage rate you qualify for.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Is a conforming loan better than a non-conforming loan?

Non-conforming loans are a good option for individuals with low credit scores, recent bankruptcies, or less saved for down payments. In addition, non-conforming loans allow your loan to exceed conforming loan limits to purchase property in expensive cities with competitive markets.

That said, non-conforming loans typically come with higher interest rates because they carry more risk for the lender. Even government-backed and guaranteed loans can be more expensive than conforming loans. For example, if you choose an FHA loan, you’ll need to pay a one-time upfront mortgage insurance premium, which increases your total loan amount.

Non-conforming loans have less stringent requirements but can make your loan more expensive. On the other hand, the strict requirements of conforming loans make it challenging for many people to secure financing for a home. Talk to a lender to determine which loan option is right for you based on your unique circumstances.

Is a non-conforming loan a conventional loan?

Is it possible to refinance a non-conforming loan?

Is it hard to get a non-conforming loan?

Who are non-conforming loans best for?

Non-conforming loans tend to be best for borrowers who don’t qualify for a conventional loan or don’t want to abide by the rigid requirements of a conventional loan. Borrowers who may seek out non-conforming loans include:

- Self-employed borrowers

- Real estate investors

- Freelancers and contractors

- Retirees

- Those with poor credit

- Those with limited savings

- Those looking for a loan amount exceeding the conforming loan limit

Why work with Griffin Funding?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

HELOC Draw vs Repayment Period

A home equity line of credit is a revolving credit line secured by your home that allows you to borrow money a...

What Is a Non-Traditional Mortgage and When Should I Use One?

What Is a Non-Traditional Mortgage? A non-traditional mortgage, also known as a non-QM loan, is a home loan th...

Griffin Funding vs United Wholesale Mortgage (UWM): Mortgage Lender Comparison

Company Overview: Griffin Funding vs United Wholesale Mortgage (UWM) Let’s look at each company in turn: who...