Retirement Mortgages: A Guide to Mortgage Loans for Seniors

KEY TAKEAWAYS

- Most housing loans for seniors accept non-traditional income sources like Social Security, pensions, and retirement accounts instead of requiring W-2s or pay stubs.

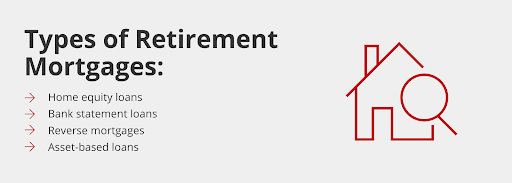

- Whether you’re buying a house in retirement or tapping into existing equity, options include reverse mortgages, home equity loans, bank statement loans, and asset-based mortgages.

- While reverse mortgages require you to be at least 62, most mortgage loans for seniors have no age restrictions.

- Lenders focus on your overall financial picture, including retirement accounts, investments, and equity, rather than traditional employment income.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformAre you interested in taking out a mortgage in retirement? Getting a traditional mortgage can often pose a challenge for retired individuals who may not earn a regular income. However, retirement mortgages can make it easier for retirees to secure a home loan. There are plenty of retirement mortgages available, but you need to figure out which one is right for your needs.

Ready to find the right retirement mortgage? Learn more about mortgages in retirement, government home loans for senior citizens, and the various options you have at your disposal.

What Is a Retirement Mortgage?

A retirement mortgage is a home loan designed to work with non-traditional sources like Social Security, pensions, and retirement accounts. These loans recognize that retirees often have substantial assets and reliable income streams even without a regular paycheck.

Traditional mortgages typically require proof of employment through W-2 forms and pay stubs. Retirement mortgages take a different approach. Instead of focusing solely on job-based income, lenders evaluate your overall financial stability using retirement distributions, investment income, and asset holdings. This means you can qualify for a mortgage based on monthly Social Security payments, pension distributions, or even the assets in your IRA or 401(k) without needing to make a 401(k) withdrawal.

How does a retirement mortgage work? Here are the basics:

- Lenders verify your income through documents like Social Security award letters, pension statements, and retirement account balances.

- If you’re using assets to qualify, they’ll review your investment accounts and calculate how much monthly income those assets could generate.

- Some lenders, like Griffin Funding, offer non-QM loans that provide even more flexibility.

Most retirement mortgages don’t have age requirements. The one exception is reverse mortgages, which require borrowers to be at least 62 years old and have significant equity in their home. All other mortgage options are available regardless of your age, as long as you meet the lender’s income and credit requirements.

Retirement Mortgage Options

Some of the most popular retirement mortgage options include:

- Home equity loans: If you are interested in taking out a loan, one of the first options could be a home equity loan. This is a great option if you own your property right now. Many seniors have been in one place for a while, and you could have a significant amount of equity built up. You may be able to tap into that equity using a home equity loan, which can provide you with a quick source of cash that you can use for various purposes.

- Bank statement loans: Another loan that you might be interested in taking out is called a bank statement loan. If you are looking for a loan option that does not require you to produce any proof of income, a bank statement loan could be the way to go. This type of loan will allow you to qualify for a mortgage using only your bank statements.

- Reverse mortgage: You can qualify for a reverse mortgage if you are at least 62 years of age and have at least 50 percent equity in your home. You can tap into the equity in your home to convert that equity into a regular income stream. While you will be responsible for monthly property tax payments and insurance payments, you can pay off your existing mortgage and eliminate monthly mortgage payments.

- Asset-based loans: You might also want to explore asset-based loans. These are loans that will allow you to qualify for a home loan using the assets you have instead of the income you generate. You may want to work with a professional who can help you identify assets that can allow you to qualify for the best mortgage with the lowest possible interest rate. You are still in control of the assets that you use to qualify for a home loan.

Keep in mind that there are plenty of other mortgages for seniors on Social Security as well. As a senior citizen, you are certainly welcome to apply for a traditional or conventional mortgage. You may also be eligible to apply for a VA loan if you meet the eligibility requirements.

How to Qualify for a Mortgage in Retirement

As you weigh your loan options, some of the most important factors you need to keep in mind include:

Income

While you do not necessarily need to have a traditional job to qualify for a mortgage, you may need to show that you have consistent sources of income if you are interested in retirement mortgages.

There are different sources of income that could help you qualify for a mortgage in retirement. A few of the options you may want to consider include:

- Social Security payments

- Your 401(k) account

- Your IRA account

- Pension payments

You will need to collect the necessary documentation to increase your chances of being approved.

| Type of Income | Documents Required | Relevant Guidelines |

|---|---|---|

| Social Security |

|

|

| Pension |

|

|

| 401(k), IRA, or Keogh retirement income |

|

|

| Investment income |

|

|

| Annuity income |

|

|

| Rental property income |

|

|

| Disability income |

|

|

Credit Score

You need to maximize your credit score if you want to put yourself in the best position possible to be approved for a retirement mortgage. There are different ways you can improve your credit score, such as paying down existing sources of debt and correcting mistakes on your credit report.

While a credit score of 620 will allow you to qualify for most loan types, try to get your credit score as high as possible. An excellent credit score will make it possible to qualify for a low interest rate and favorable loan terms.

Debt-to-Income Ratio

You should also try to improve your debt-to-income (DTI) ratio as you consider applying for a retirement mortgage. The best way to do that is to try to pay down existing sources of debt, such as any car loans or personal loans you might have. You should also try to avoid carrying a balance on your credit card.

Consider Your Assets

As a retiree, you may have significant assets that you can tap into to help you get ready to apply for a mortgage in retirement.

For example, you may want to consider your investment accounts and any equity that you might have in your current home. If you have substantial assets, you could increase your chances of getting approved for a loan.

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

Find the Best Retirement Mortgage for You

If you want to take out a mortgage in retirement, there are plenty of options available. By working with a real estate professional, you can review retirement mortgage options and find the loan that best aligns with your needs.

At Griffin Funding, we have a variety of loan packages available, including non-traditional options. Get started online and find the retirement mortgage that best aligns with your needs.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What is the best loan for retired people with a good credit score?

The most important thing that you need to remember is that there are multiple choices, so consider reaching out to a professional who can help you compare the benefits and drawbacks of each option before you make a decision.

Are there government home loans for senior citizens?

There are other options available as well. For example, you may want to see if you qualify for FHA first-time home buyer loans and VA loans, as these programs can make it easier to obtain financing.

Can I get a mortgage using Social Security income?

Can retirees qualify for a mortgage without any employment income?

A self-directed IRA is another way to invest in real estate after retirement by purchasing rental properties through your retirement account. The property must be used strictly for investment, and any rental income grows tax-deferred within the IRA.

Do retirement mortgages have higher interest rates than traditional mortgages?

Check out our current mortgage rates to compare rates across different loans. You can also use our home affordability calculator or bank statement loan calculator to estimate what you might qualify for.

Is there a maximum age limit for getting a mortgage?

What matters most to lenders is whether or not you can repay the loan. They'll consider your income, assets, and creditworthiness. You can even refinance your mortgage later in retirement if it makes financial sense.

Can I use retirement account funds to qualify without withdrawing them?

If you're considering investment property loans, retirement account assets can help you qualify for those, too.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

Amortization Calculator

How well do you understand your mortgage loan? If you’re like most people, you pay your mortgage loan monthl...

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...