Grantor vs Grantee in Real Estate: What’s the Difference?

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the terms “grantor” and “grantee.” These two parties appear on nearly every real estate transaction. Whether you’re buying your first home, inheriting property, or transferring a title within your family, knowing the difference between a grantor and grantee helps you read mortgage terms and legal documents with confidence.

- What Is a Grantor in Real Estate?

- What Is a Grantee in Real Estate?

- Grantor vs Grantee: Key Differences Explained

- How Different Deeds Impact Grantor vs Grantee Responsibilities

- Grantor vs Grantee in a Mortgage

- Examples of Grantor vs Grantee Scenarios

- Why Understanding the Difference Between Grantor vs Grantee Matters

- Final Notes

- Frequently Asked Questions

Key Takeaways

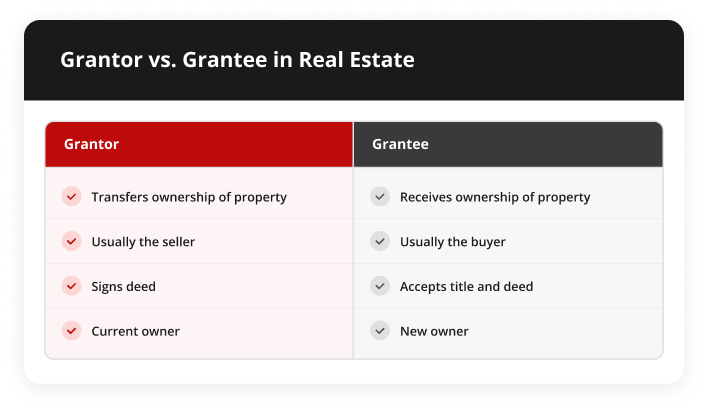

- The grantor is the party transferring ownership rights and the grantee is the party receiving them.

- Both parties appear on the property deed, which is the foundational document in any real estate ownership transfer.

- The type of deed determines how much protection the grantee receives and how much liability the grantor carries.

- In mortgage documents, the borrower often acts as the grantor of a security interest while the lender or trustee acts as the grantee.

What Is a Grantor in Real Estate?

A grantor is the person or entity that transfers ownership rights to real property. In plain terms, the grantor is the giver, or the party who currently holds the title and is conveying it to someone else.

The suffix “-or” in grantor signals the one performing the action. The grantor signs the deed, legally initiating the transfer of title.

Common examples of a grantor include:

- A home seller transferring title to a buyer at closing

- A parent gifting a property to a child

- A trust distributing real estate to a beneficiary

- A divorced spouse signing a quitclaim deed to remove their interest from shared property

Legal responsibilities of a grantor vary depending on the type of deed used. In a general warranty deed, the grantor makes broad promises, called covenants, guaranteeing clear title and agreeing to defend the grantee against any future claims. In a quitclaim deed, the grantor transfers only whatever interest they currently hold, with no warranties whatsoever.

On a property deed or title document, the grantor appears as the “transferring party.” You’ll typically see language like: “John Smith, Grantor, hereby conveys and warrants to Jane Doe, Grantee…”

What is a Grantee in Real Estate?

A grantee is the person or entity that receives ownership rights to real property. The grantee is the receiver, or the party who walks away from the transaction holding title.

Common examples of a grantee include:

- A homebuyer acquiring a property through a standard purchase

- A child or family member receiving gifted property

- A trust receiving real estate as part of an estate plan

- A new spouse being added to an existing title

Once the deed is signed, delivered, and recorded with the local county recorder’s office, the grantee becomes the legal owner of record. Recording the deed is the step that makes the transfer official and protects the grantee’s ownership rights in the public record.

Understanding your rights as a grantee matters because they vary depending on what kind of deed you receive. A grantee who accepts a general warranty deed has strong legal protections if title issues arise later. A grantee who accepts a quitclaim deed takes the property “as is” with no guarantees about the title’s history.

Grantor vs Grantee: Key Differences Explained

How Different Deeds Impact Grantor vs Grantee Responsibilities

A deed is the legal document that formally transfers ownership of real property from one party to another. Every deed identifies the grantor and grantee, describes the property, and must be signed, notarized, and recorded to be legally effective.

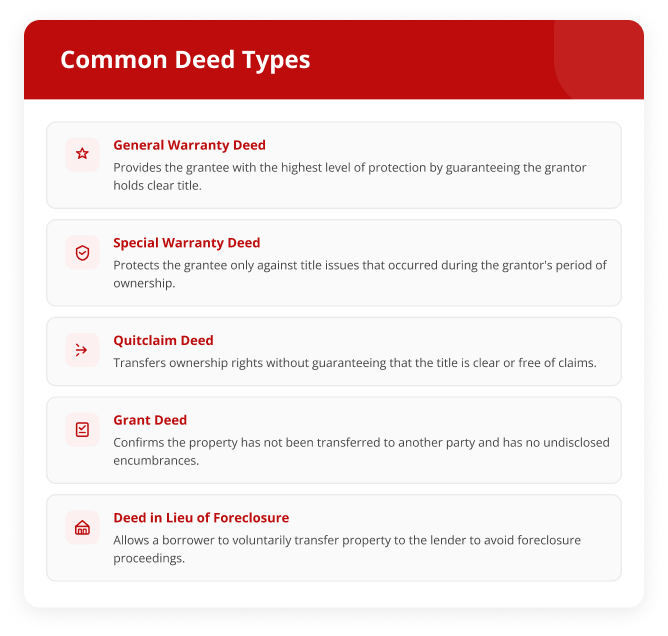

The type of deed used determines what the grantor promises and what protections the grantee receives. If you’re unsure what type of deed you received, review your house title documentation. Here are the most common deed types:

- General Warranty Deed: The grantor provides the highest level of protection, guaranteeing clear title against any claims, even those that arose before the grantor owned the property. This is the most common deed type in residential real estate sales and is heavily favored by grantees because of its broad protections.

- Special Warranty Deed: The grantor only warrants the title against claims arising during their period of ownership. Issues predating their ownership are not covered. This deed is common in commercial transactions and estate sales.

- Quitclaim Deed: The grantor transfers whatever ownership interest they have, with zero warranties about the title’s quality. Quitclaim deeds are common in divorces, family transfers, or when adding or removing a spouse from a title. The grantee takes on significant risk since no title guarantee exists.

- Grant Deed: Used primarily in California, the grant deed implies that the grantor hasn’t already sold the property to someone else and that the property is free from encumbrances made by the grantor (though not prior owners).

Grantor vs Grantee in a Mortgage

It’s easy to confuse how these terms apply in mortgage transactions because a mortgage and a deed are two separate legal documents.

When you take out a mortgage, you’re not transferring ownership of your home to the lender. However, in many states, particularly those using a deed of trust instead of a traditional mortgage, the borrower (you) actually conveys a security interest to a trustee on behalf of the lender. In that context:

- The borrower acts as the grantor, granting a security interest in the property

- The lender or trustee acts as the grantee, receiving that security interest as collateral for the loan

In states using a traditional mortgage structure, the borrower is called the mortgagor and the lender is the mortgagee.

When a mortgage is paid off, the lender releases the lien by recording a lien release or reconveyance deed. At that point, the lender (acting as grantor of the release) conveys its interest back to you as the grantee, restoring your full, unencumbered title.

Terminology also varies by state. Texas, California, and most western states use deed-of-trust structures, so the home buying process in those states looks a little different on paper from states that use a traditional mortgage. It’s also worth noting that if a property ever goes into foreclosure, the transfer of title from the homeowner to the bank or new buyer will again use grantor and grantee language on the relevant deed.

Examples of Grantor vs Grantee Scenarios

Example 1: Traditional Home Sale

In a standard home sale, the seller is the grantor and the buyer is the grantee. At closing, the seller signs a warranty deed, formally acting as the grantor, and conveys title to the buyer. Once the deed is recorded, the buyer becomes the new owner of record.

Example 2: Parent Transfers Property to Child

A parent who wants to gift their home to an adult child will execute a deed naming themselves as the grantor and their child as the grantee. This can be done via a gift deed or a quitclaim deed. The transfer may have gift tax implications, so it’s wise to consult a tax professional. Tools like the Griffin Gold app can help you track your finances as ownership responsibilities shift.

Example 3: Quitclaim Deed Transfer

A quitclaim deed is often used when ownership interests need to be quickly clarified or removed, like during a divorce. Say one spouse wants to transfer their interest in the family home to the other. The departing spouse becomes the grantor, signing over their interest with no warranties. The remaining spouse is the grantee, receiving whatever interest the grantor held.

Why Understanding the Difference Between Grantor vs Grantee Matters

These roles have real consequences at every stage of a real estate transaction. At closing, buyers and sellers sign multiple documents. Confirming which party you are helps you verify that your name is listed correctly, the property description is accurate, and the deed type matches what was negotiated. A recording error like a misspelled grantee name can cloud the title and create problems when you try to sell or refinance later.

The distinction also matters beyond a standard sale. When you refinance, a new deed of trust is recorded. In estate planning, property is often transferred into a trust, with the property owner as grantor and the trust as grantee. And in any transaction, confirming who the grantor is helps you verify chain of title, the unbroken sequence of ownership transfers from the original owner to you. Any gap in that chain can signal a fraudulent transfer or an unresolved lien.

Final Notes

The difference between a grantor and grantee in real estate comes down to the transfer. The grantor transfers; the grantee receives. That distinction flows through every deed type, every mortgage document, and every title record.

The clearer you are on these roles before you get to the closing table, the better positioned you are to catch errors, ask the right questions, and protect your investment. There are real benefits of homeownership on the other side of that process, and Griffin Funding is here to help you get there.

Frequently Asked Questions

Can a grantor also be a grantee?

Yes. It’s possible for the same person to appear as both grantor and grantee on different transactions, or even the same document in certain cases.

For example, a homeowner who sells their current home (acting as grantor) and simultaneously buys a new home (acting as grantee) occupies both roles across two separate transactions.

In some trust-related transactions, a person might also transfer property to themselves in a new capacity. For example, from individual ownership into a revocable living trust where they remain the beneficiary.

Is the grantor always the seller?

Not always. While the grantor is typically the seller in a standard home sale, a grantor can be anyone transferring property rights, including a parent gifting a home, an executor distributing an estate, a divorcing spouse removing their interest from a shared property, or a trust distributing real estate to a beneficiary.

What happens if a deed lists the wrong grantee?

If a deed contains an error, like a misspelled name or incorrect legal entity, it can create a cloud on the title. The fix is typically a corrective deed, sometimes called a confirmatory deed, which is prepared and recorded to correct the error.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Why vacation rental investors are spending more time on market research before buying

For investors already holding properties or considering new purchases, miscalculating revenue in this environm...

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...