Best DSCR Lenders: Griffin Funding vs Angel Oak vs Kiavi vs Visio vs Lima One vs Easy Street

Best DSCR Lenders: Griffin Funding vs Angel Oak vs Kiavi vs Visio vs Lima One vs Easy Street

KEY TAKEAWAYS

- Griffin Funding leads in speed and flexibility with fast approvals, nationwide coverage, and flexible underwriting guidelines that make us a top choice for most investors.

- DSCR loans focus on property cash flow rather than personal income, making them more accessible for investors with complex financial situations or multiple income streams.

- Minimum DSCR requirements typically range from 1.0 to 1.25, but the best lenders offer flexible underwriting that considers the complete borrower profile beyond just the ratio.

- Rate shopping is essential since each DSCR mortgage company offers different rate structures, and comparing multiple lenders can save thousands over the loan term.

Finding the best DSCR lender is crucial for your real estate investment success. With rental property financing becoming increasingly competitive, investors need lenders who understand their unique needs and can deliver both competitive rates and reliable service. We’ve analyzed the top DSCR loan lenders in the market to help you make an informed decision for your investment property financing.

What to Look for in a DSCR Lender

Choosing the best DSCR lender for your unique situation means evaluating several critical factors that directly impact your investment returns and borrowing experience. Here’s what to look for in a DSCR loan lender:

- Interest rates and loan terms: Compare both fixed and adjustable rate options across different loan terms. Many lenders offer 30-year fixed rates, but some provide interest-only payment periods that can improve cash flow during the early years of ownership.

- Minimum DSCR requirements: Most lenders require a debt service coverage ratio between 1.0 and 1.25, but some flexible lenders will go to 0.75 or less for strong borrowers. Understanding these thresholds helps you target the right lender for your property’s income potential.

- Loan-to-value ratios: LTV ratios typically range from 70% to 80% for investment properties, but the best mortgage lenders for investors may offer higher ratios for exceptional borrowers or prime properties.

- Prepayment penalties: Some DSCR lenders charge penalties for early payoff, which can limit your exit strategies. Look for lenders with minimal or no prepayment restrictions.

- States serviced: Not all lenders operate nationwide, so verify coverage in your target investment markets before starting the application process.

- Customer support and loan speed: Investment opportunities often require quick action, making responsive customer service and fast closing times crucial factors in lender selection.

- Portfolio loan options vs traditional underwriting: Portfolio lenders keep loans in-house rather than selling them, often allowing more flexible underwriting standards compared to traditional mortgage companies.

As of mid-May 2026, DSCR loan rates have become increasingly competitive — in many cases matching or beating conventional investment property loan rates after Fannie Mae and Freddie Mac loan-level price adjustments (LLPAs) are factored in. With conventional rates climbing back above 6.50% due to rising oil prices and geopolitical uncertainty, investors are finding that DSCR loans offer not only a simpler qualification process but also better pricing for rental property financing. That makes choosing the right DSCR lender more important than ever.

Licensing and Regulatory Status: A Buying Criterion Most DSCR Investors Skip

DSCR loans are business-purpose loans secured by investment properties. Because they are business-purpose loans rather than consumer mortgages, DSCR lenders are exempt from consumer mortgage licensing requirements in most states. This is why most DSCR lenders and DSCR brokers operate without state mortgage licensure.

Some investors consider that exemption a feature. We consider it a gap.

Griffin Funding is fully state-licensed as a non-bank mortgage lender in 46 states plus DC, supervised by state mortgage regulators and the Consumer Financial Protection Bureau (CFPB). We also hold VA-Approved Lender status and HUD FHA Non-Supervised Lender authority, meaning we are authorized by the U.S. Department of Veterans Affairs and the U.S. Department of Housing and Urban Development to originate, underwrite, and close federal mortgage programs directly.

We hold these licenses and approvals because the same consumer-protection, fair-lending, and disclosure standards that protect a primary-residence borrower should protect an investor borrowing $500,000 against a rental property. Regulatory accountability is part of the product.

Here is how the six DSCR lenders covered on this page compare on licensing and regulatory status:

| Lender | State Mortgage Licensing | Federal Approvals | CFPB Supervised |

|---|---|---|---|

| Griffin Funding | 46 states + DC (operates in 49) | VA-Approved · HUD FHA Non-Supervised | Yes |

| Angel Oak Mortgage | Licensed nationally | None confirmed | Yes |

| Kiavi | Licensed in 13 states (operates in 45) | None confirmed | Limited |

| Lima One Capital | Licensed in 13 states (operates in 46) | None confirmed | Limited |

| Visio Lending | Licensed in 1 state (operates in 41) | None confirmed | Limited |

| Easy Street Capital | Limited state licensing | None confirmed | Limited |

Sources: NMLS Consumer Access database, verified May 2026. Licensing status changes over time; verify current status at NMLS Consumer Access before engaging any DSCR lender.

Griffin Funding Overview

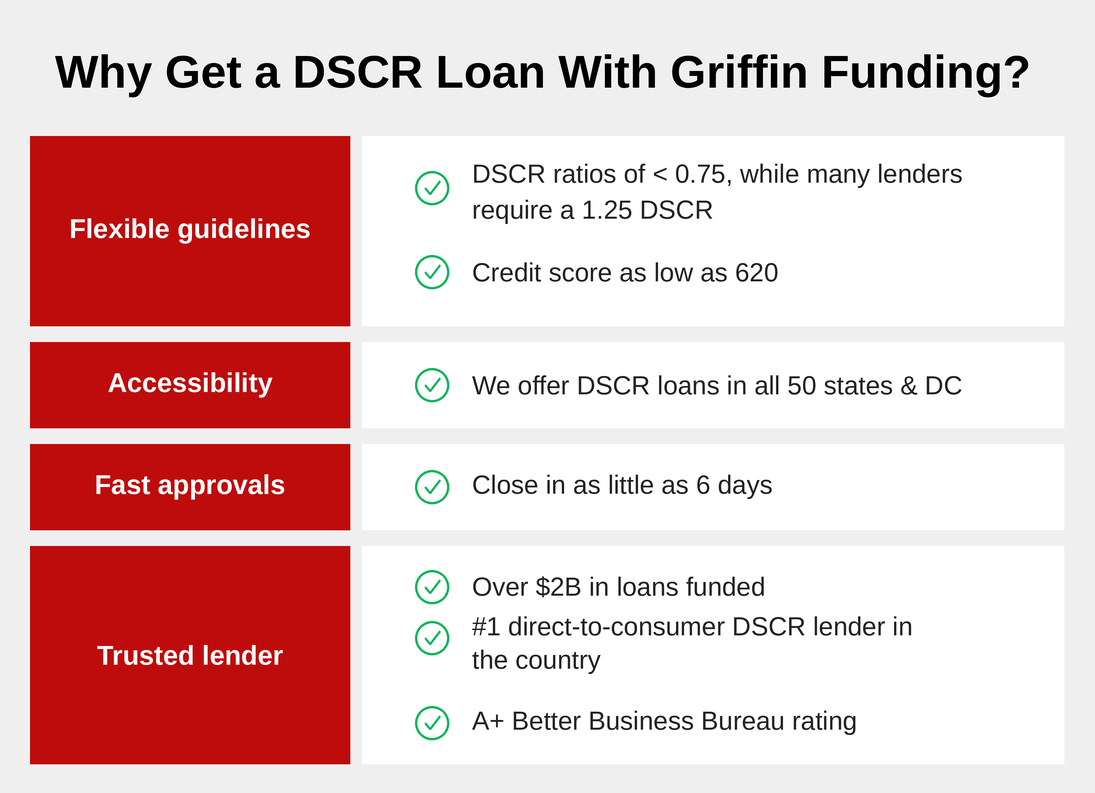

Griffin Funding has established itself as a leading DSCR lender by combining competitive rates with investor-friendly policies. Griffin Funding is the best DSCR lender for real estate investors who want competitive rates, fast closings, and flexible underwriting without tax returns. As one of the most active DSCR lenders in the country, Griffin offers no-ratio programs for investors who want to skip cash flow qualification entirely and close loans in as little as 6 days.

We offer both 30-year fixed and interest-only payment options with loan amounts up to $4,000,000. Our non-QM loans include specialized products like DSCR home equity loan options and DSCR cash-out refinance products.

Griffin requires a minimum 620 credit score and accepts DSCR ratios that are less than 0.75, making our loans accessible to newer investors and properties with modest cash flow.

Unlike many competitors, Griffin Funding originates DSCR loans nationwide and is fully state-licensed as a non-bank mortgage lender in 46 states plus DC, supervised by state mortgage regulators and the Consumer Financial Protection Bureau (CFPB). This nationwide reach, combined with VA-Approved Lender and HUD FHA Non-Supervised Lender authority, makes Griffin the most regulated lender in the DSCR space.

Pros:

- Fast approvals: Most applications receive approval decisions within 24-48 hours.

- Fast fundings: Fund in as little as 6 calendar days when your file is complete. Last year, Griffin averaged 34 days, and that timeline is drastically improving in 2026 with LIA, Griffin’s proprietary AI-powered non-QM underwriting agent.

- Flexible guidelines: Griffin’s underwriting team considers the complete investor profile rather than relying solely on rigid qualification boxes.

- 30-year fixed, ARM, and interest-only options: Multiple payment structures allow investors to optimize cash flow based on their investment strategy.

- Multiple prepayment penalty options: Griffin offers 6-month and 1-year ARMs with no prepayment penalties and 30 or 40-year fixed terms, ranging from zero to five-year prepayment penalties.

- No LLPA penalties: Unlike conventional investment property loans that carry Fannie Mae/Freddie Mac loan-level price adjustments adding 0.50%–1.50%+ to your rate, Griffin’s DSCR loans are not subject to the LLPA matrix — often resulting in lower all-in rates for investors. Learn more about LLPAs.

- Most regulated lender in this comparison: Griffin Funding is fully state-licensed in 46 states plus DC, CFPB-regulated, with VA-Approved Lender status and HUD FHA Non-Supervised Lender authority. Most DSCR competitors hold limited or no state mortgage licensing because business-purpose loans don’t require it. We hold the licenses anyway.

Cons:

- Limited commercial options: Griffin focuses primarily on residential investment properties, with fewer options for larger commercial deals.

The Griffin Gold app streamlines the application process, while our extensive testimonials demonstrate consistent customer satisfaction across different investor profiles.

Angel Oak Overview

Angel Oak has built a reputation as a specialized DSCR mortgage company with particular strength in non-qualified mortgage products and regional expertise.

This DSCR loan lender offers a comprehensive suite of investor loan products, including traditional investment property loans and specialized DSCR options. Their programs cater to both individual investors and those building larger portfolios.

Angel Oak offers DSCR loans up to $3 million with a $100,000 minimum, including purchase, cash-out refinance, rate-and-term refinance, and delayed financing options. They allow DSCR loans for short-term rentals with AirDNA reports and accept properties held in LLCs, corporations, or trusts.

Angel Oak requires a minimum 680 credit score with loan-to-value ratios up to 85%. They offer DSCR ratios below 1.0 and even no-DSCR options, making them accessible for properties with limited cash flow.

Pros:

- Strong presence in Southeast: Angel Oak’s regional focus allows it to provide specialized knowledge of local markets and faster processing in its primary service areas.

- Non-QM flexibility: Their extensive non-qualified mortgage experience translates to creative solutions for complex investment scenarios.

Cons:

- Slower funding process reported by users: Multiple borrowers report longer closing times compared to tech-forward competitors, potentially problematic in fast-moving markets.

Kiavi Overview

Kiavi differentiates itself through technology-driven lending processes designed for efficiency and speed in today’s competitive investment market. Its platform automates much of the underwriting process, allowing for faster decisions and reduced paperwork compared to traditional lenders.

Kiavi operates in 45 states (licensed in only 13), providing broad coverage while maintaining focus on its core markets with the strongest operational infrastructure.

Pros:

- Fast online applications: Their digital-first approach allows you to complete the application in just a few minutes and get approved quickly.

- Good for single-family rentals: Kiavi’s systems are optimized for the single-family rental market, making them ideal for investors focused on this property type.

Cons:

- Less flexible on DSCR ratios: Kiavi’s automated systems mean less flexibility for borderline deals that might benefit from human underwriter review.

- More geared toward experienced investors: Their streamlined process assumes familiarity with investment property financing, which can be challenging for newer investors.

Visio Overview

Visio Lending focuses exclusively on rental property financing, positioning itself as a specialist in the long-term rental investment space. This DSCR lender concentrates on long-term rental loans with programs designed specifically for buy-and-hold investors seeking stable, predictable financing.

Visio accepts properties with 1.0 DSCR ratios, making them competitive for properties with modest cash flow potential. Additionally, this lender operates across 41 states and is licensed in 1 state.

Pros:

- Transparent pricing: Visio provides clear, upfront pricing without hidden fees or last-minute surprises that can derail closing schedules.

- No personal income verification: Their focus on property cash flow rather than personal income makes them attractive to investors with complex personal financial situations.

Cons:

- Higher rates than competitors: Visio’s rates often run slightly higher than those of other top DSCR lenders, potentially impacting long-term investment returns.

Lima One Overview

Lima One targets serious real estate investors with a focus on scalability and portfolio growth support. The lender offers DSCR loans, fix-and-flip financing, and multifamily options, providing a complete suite of investment property financing solutions.

Operating in 46 states (licensed in only 13), Lima One sets minimum DSCR requirements at 1.0, though this can vary based on borrower qualifications and property characteristics. Properties with stronger cash flow potential often qualify for more competitive interest rates.

Lima One’s programs are designed to support investors as they scale from single properties to large portfolios, with systems built for volume lending.

Pros:

- Extensive lending network: Lima One’s broker network provides access to capital even in challenging markets or unique situations.

- Flexible terms: Their portfolio lending approach allows for creative structuring that traditional lenders cannot accommodate.

Cons:

- Can require more documentation: Lima One’s thorough underwriting process often demands additional documentation compared to streamlined competitors.

- Slower closing reported: Multiple investors report closing times extending beyond initial estimates, potentially problematic for time-sensitive acquisitions.

Easy Street Capital Overview

Easy Street Capital is a business-purpose investment property lender. They offer financing geared towards purchasing rentals, fix-and-flip properties, and building homes. They also allow borrowers to generate their own term sheets online. However, these term sheets can change after speaking with a loan officer or at a later point in the lending process.

Pros:

- Generate term sheets online: Borrowers can generate their own term sheets online, facilitating a quick and efficient experience.

- Business-purpose mortgage solutions: Easy Street Capital offers a variety of specialized loan programs aimed at those investing in real estate.

Cons:

- Term sheet changes: While borrowers can generate their own term sheets online, these terms can be changed after the borrower meets with a loan officer or moves further along in the process.

- Investment property loans only: Easy Street Capital only offers investment property loan products. They do not offer mortgages for those looking to finance a primary residence or a vacation home for personal use.

Which DSCR Lender Is Right for You?

The best DSCR lender depends on your investor profile, credit score, property type, and portfolio goals. Use this table to match your situation to the right lender.

| Investor Situation | Best DSCR Lender | Why |

|---|---|---|

| Speed-focused investors (quick close needed) | Griffin Funding or Kiavi | Griffin closed in as few as 6 days in 2025 using AI-driven underwriting (LIA); Kiavi uses algorithmic underwriting for fast SFR approvals. |

| Southeast market investors | Angel Oak | Regional expertise and market knowledge in Southeast core markets; specialized non-QM experience. |

| Portfolio investors planning significant expansion | Lima One | Scalability focus and extensive broker network; systems built for volume lending across large portfolios. |

| Investors who prioritize transparent, predictable pricing | Visio Lending | Upfront pricing with no last-minute surprises; long-term rental specialist with consistent underwriting. |

| Complex borrower profile needing flexible underwriting | Griffin Funding | Considers the complete investor profile rather than rigid qualification boxes; 620 minimum FICO; DSCR qualifies down to 0.75. |

| Rate-conscious investors (want lowest all-in cost) | Griffin Funding | No LLPA surcharges vs. conventional investment loans; DSCR rates often lower all-in than Fannie/Freddie investor pricing after LLPAs are factored in. |

| First-time real estate investors | Griffin Funding | 620 minimum FICO with no prior investment property experience required; 15% down; dedicated loan officer; 24 to 48 hour pre-approval. |

| Short-term rental / Airbnb property investors | Griffin Funding or Visio | Griffin accepts a comparable rent schedule or 12-month STR income history; no-ratio option if cash flow does not qualify. Visio uses AirDNA projections for Airbnb/VRBO underwriting. |

| Scaling a rental portfolio (BRRRR strategy) | Griffin Funding | No limit on financed properties; unlimited cash-out with no seasoning; each property underwritten on its own DSCR, not on total portfolio debt load. |

Your choice should align with your investment timeline, geographic focus, and financing complexity. Consider checking Griffin Funding mortgage rates and using our DSCR loan calculator to compare options before making your final decision.

Why Choose Griffin Funding for Your DSCR Loan?

Griffin Funding is among the best DSCR mortgage companies thanks to our combination of competitive rates and rapid closing timelines. Our nationwide coverage ensures consistent service quality whether you’re investing in your local market or expanding into new states.

What sets Griffin apart is our personalized approach to investor support. Each borrower works with dedicated loan officers who understand their unique challenges. This personalized service, combined with a streamlined pre-qualification process, helps investors move quickly in competitive markets. Griffin also has multiple products and programs and is not limited to one set of guidelines.

Ready to explore your financing options? Get pre-qualified today to understand your purchasing power and take advantage of Griffin’s investor-focused DSCR loan programs.

Explore DSCR Mortgage Solutions

The best DSCR lender for your situation combines competitive rates, reliable service, and programs that match your investment strategy. Griffin Funding’s comprehensive approach to investment property financing, combined with our nationwide coverage and investor-focused service, makes us a top choice for serious real estate investors.

Whether you’re purchasing your first short-term rental property or expanding an existing portfolio, working with experienced mortgage lenders for investors ensures access to the capital and expertise needed for successful real estate investment outcomes.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What is the best DSCR lender in 2026?

For most investors seeking reliable service, competitive rates, and fast closings, Griffin Funding provides the best combination of advantages. Consider getting pre-qualified with Griffin to compare our offering against other options.

What DSCR ratio do most lenders require?

Are DSCR loans hard to get?

The main advantage of these loans is that borrowers don't need to provide tax returns, pay stubs, or other personal income documentation. However, lenders do require detailed rent rolls, lease agreements, and property appraisals to verify the property's income potential. Working with experienced DSCR lenders like Griffin Funding can streamline the process.

What questions should I ask my DSCR mortgage lender?

- What are the interest rate, loan terms, and fees?

Understand the interest rate on the loan, whether it’s fixed or adjustable, and how it will impact your monthly payments and overall cost of borrowing. Additionally, you should inquire about the duration of the loan, repayment schedule, and any prepayment penalties or balloon payments that may apply.

To determine the total cost of borrowing, ask about:

- Origination fees

- Discount points

- Closing costs

- Any other fees associated with the loan

- What property types qualify?

Eligible property types can vary between lenders. Ask your lender about any restrictions on the types of properties that qualify for the loan, such as residential, commercial, rural, or multi-family properties.

- Are you experienced with DSCR loans and working with investors?

Working with lenders experienced in DSCR loans is crucial because they understand the unique aspects of investment properties. Key features of experienced DSCR lenders include:

- Understanding investors’ needs to offer financing solutions that align with their investment strategies.

- Expertise in property analysis to determine their income potential and accurately calculate DSCRs, evaluate property cash flow projections, and determine loan eligibility based on property performance.

- A streamlined approval process because the lender understands the documentation requirements, underwriting criteria, and due diligence process for investment properties to facilitate efficient loan approval and funding.

- There should be multiple money sources that have an appetite for all types of DSCR non-QM loans. The lender should not have one money source with one set of guidelines. Not all investment properties are equal; if the lender has access to funding from private equity, securitization, and large insurance companies, then your loan has a better chance of closing.

What is a good rate for a DSCR loan?

Rates with a 5-year prepayment penalty are typically 0.25%-0.75% lower than no-penalty options. Investors with a 740+ FICO and a DSCR of 1.25 or higher will qualify for the best pricing; rates increase as credit score or DSCR decreases.

One factor that makes DSCR rates competitive with conventional investment property loans: DSCR loans are not subject to Fannie Mae and Freddie Mac loan-level price adjustments (LLPAs), which can add 0.50%-1.50% to conventional investor loan rates. Griffin Funding's current DSCR loan rates are available on the rates page.

Do you need 20% down for a DSCR loan?

For borrowers with a credit score below 740 or a DSCR below 1.0, a 20-25% down payment is more typical. A larger down payment generally improves your DSCR ratio (by reducing monthly PITIA), lowers your interest rate, and makes it easier to qualify if the property's cash flow is thin. For DSCR loans with ratios below 0.75, additional reserves beyond the standard down payment may be required.

Who is the best DSCR lender for first-time real estate investors?

Which DSCR lender is best for investors with lower credit scores?

It is worth noting that most DSCR lenders price aggressively at 720+ FICO, so improving your score before applying can meaningfully lower your rate even with a DSCR-qualified loan.

Which DSCR lender is best for building a rental portfolio?

This structure is ideal for investors using the BRRRR strategy (buy, rehab, rent, refinance, repeat) because you can pull equity out of one property immediately after stabilization and deploy it into the next acquisition without waiting. Lima One is the secondary recommendation for investors working with broker networks or managing larger commercial portfolios.

What is the best DSCR lender for Airbnb and short-term rental properties?

Visio Lending specializes in STR underwriting using AirDNA projected revenue, making them a strong option for investors whose properties have a documented Airbnb or VRBO performance history.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...

How to Finance a Home Renovation

Whether you’re upgrading a dated kitchen, adding square footage, or tackling overdue repairs, figuring o...

Is Being a Landlord Still Worth It?

Owning rental property has long been one of the most reliable paths to building real wealth in America. But be...