Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

KEY TAKEAWAYS

- Bank statement loans let self-employed borrowers qualify on business or personal deposits instead of tax returns, which often understate real income after write-offs. This is the difference between an approval and a denial for many business owners.

- Griffin Funding leads on speed and flexibility, with expense ratios as low as 10% (with CPA verification), a 620 minimum credit score, coverage in 47 states plus DC, and a fastest 2026 close of 6 days.

- The number of months of statements required is a key differentiator. Some lenders qualify you on 12 months and accept personal accounts, while others require 24 months of business statements, so matching the program to your records matters.

- Lender oversight varies and affects your experience. Non-bank lenders like Griffin are state-licensed and CFPB-supervised, and their loan officers are individually licensed rather than only registered, which raises the floor on competency for a loan this judgment-intensive.

- Rates and terms differ widely between bank statement lenders, so comparing several on rate, expense ratio treatment, and loan limits can save thousands over the life of the loan.

Self-employed borrowers are routinely underserved by traditional mortgage lenders that still want two years of tax returns. This guide compares the top bank statement loan lenders of 2026 on rates, underwriting flexibility, speed, and licensing, so you can find the one built for how your income actually works.

What to Look for in a Bank Statement Loan Lender

Choosing the best bank statement loan lender for your situation means weighing several factors that directly affect your monthly payment, your approval odds, and how smoothly you get to closing. Here’s what to look for in a bank statement loan lender:

- Interest rates and loan terms:Compare both fixed and adjustable rate options across different terms. Many lenders offer 30-year fixed rates, but some provide interest-only payment periods and 40-year terms that lower payments during the early years.

- Maximum DTI requirements: Most lenders cap debt-to-income around 50%, though some flexible lenders will go to 55% for strong borrowers. Knowing these thresholds helps you target a lender that fits your income.

- Loan-to-value ratios: LTV ratios typically range from 70% to 80%, but the best mortgage lenders may offer higher ratios up to 90% for exceptional self-employed borrowers.

- Months of statements required. Some lenders qualify you based on 12 months of bank statements; others require 24; and some accept business or personal accounts. Fewer months and personal-account flexibility make qualifying easier.

- States serviced: Not all lenders operate nationwide, so verify coverage in your market before you apply.

- Customer support and loan speed: Self-employed buyers often need to move fast, which makes responsive service and quick closings a real factor in who you choose.

- Non-QM vs traditional underwriting: Non-QM lenders use more flexible underwriting than traditional mortgage companies, which is what lets them count deposits as income instead of tax returns.

Licensing and Regulatory Status: A Buying Criterion Most Bank Statement Loan Borrowers Skip

Bank statement loans are consumer mortgages secured by your home, which means the lender’s regulatory standing actually matters to you.

Griffin Funding is fully state-licensed as a non-bank mortgage lender in 46 states plus DC, supervised by state mortgage regulators and the Consumer Financial Protection Bureau (CFPB). We also hold VA-Approved Lender status and HUD FHA Non-Supervised Lender authority, meaning we are authorized by the U.S. Department of Veterans Affairs and the U.S. Department of Housing and Urban Development to originate, underwrite, and close federal mortgage programs directly.

We hold these licenses and approvals because they are required of non-bank lenders for consumer-protection, fair-lending, and disclosure standards. Regulatory accountability is part of the bank statement loan product.

Federally chartered banks are supervised by the OCC instead of obtaining state mortgage licenses, which exempts them from state-level mortgage oversight.

Some borrowers consider that exemption a feature. We consider it a gap.

The Person Handling Your Loan: Registered vs. Licensed Loan Officers

Not every loan officer carries the same credentials, and most borrowers never find out until something goes wrong. The SAFE Act sorts mortgage loan originators (MLOs) into two groups, and which group your loan officer falls into depends entirely on whether they work for a bank or a non-bank lender.

A loan officer at a non-bank lender like Griffin Funding must be individually licensed in each state. To get that license and keep it, they must:

- Pass the SAFE national mortgage exam with a qualifying score

- Complete 20 hours of pre-licensing education before they can originate a single loan

- Complete 8 hours of continuing education every year to stay licensed

- Pass an FBI fingerprint background check and a credit review

- Hold a unique NMLS number tied to an active state license in every state where they lend

A loan officer at a federally chartered bank does not have to do any of that. Under the SAFE Act, bank MLOs are registered rather than licensed. They submit fingerprints and receive an NMLS number, and that is essentially the requirement. No exam. No pre-licensing education. No mandatory annual continuing education. No individual license that a regulator can suspend or pull.

The practical effect is a lower floor on competency. A registered bank loan officer can originate your mortgage without ever having been tested on mortgage law, federal disclosure rules, or how to structure a complex file, and without any requirement to keep their knowledge current as the rules change. That does not make every bank loan officer unqualified, and it does not make every licensed loan officer an expert. It does mean the two credentials are not equal, and the gap matters most on exactly the kind of loan you are shopping for.

Bank statement loans are among the most judgment-intensive mortgages a borrower can get. Your income is built from deposits rather than tax returns, which means someone has to correctly identify qualifying deposits, separate business accounts from personal, apply the right expense factor, and document all of it to underwriting standards. A loan officer who was tested on this work and is required to stay current every year is better positioned to get that file structured right the first time. On a bank statement loan, getting it right the first time is often the difference between an approval and a denial.

This individual-level gap mirrors the institutional one. The table below shows how the six lenders compare at the company level, and the same pattern holds: the lenders supervised only at the federal bank level are also the ones whose loan officers are registered rather than licensed.

Here is how the six bank statement loan lenders covered on this page compare on licensing and regulatory status:

| Lender | State Mortgage Licensing | Federal Approvals | Loan Officers (MLOs) | Primary Regulator |

|---|---|---|---|---|

| Griffin Funding | 47 states + DC | VA-Approved · HUD FHA Non-Supervised | State-Licensed | CFPB |

| Farm Bureau Bank | None | VA-Approved · HUD FHA Supervised | Registered | OCC |

| CrossCountry Mortgage | 50 states + DC | VA-Approved · HUD FHA Non-Supervised | State-Licensed | CFPB |

| North American Savings Bank | None | VA-Approved · HUD FHA Supervised | Registered | OCC |

| Angel Oak | 46 states + DC | Verify against HUD/VA lender lists | State-Licensed | CFPB |

| Newfi | 48 states + DC | VA-Approved · HUD FHA Non-Supervised | State-Licensed | CFPB |

Licensing and approvals current as of June 2026, per the NMLS Consumer Access database, lender websites, and HUD definitions. This status can change, so always verify directly through NMLS Consumer Access, the lender’s website, or HUD and the VA before applying. “Supervised” applies to depository institutions such as banks and federal savings banks; “Non-Supervised” applies to independent mortgage companies.

Griffin Funding Overview

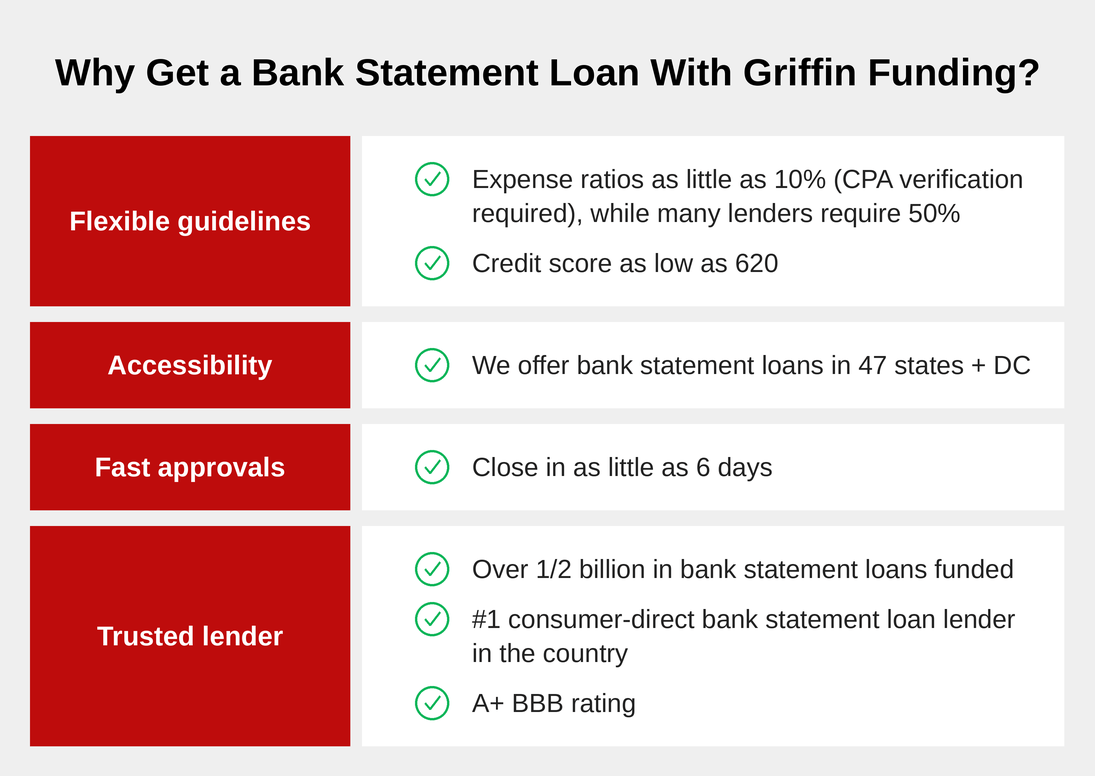

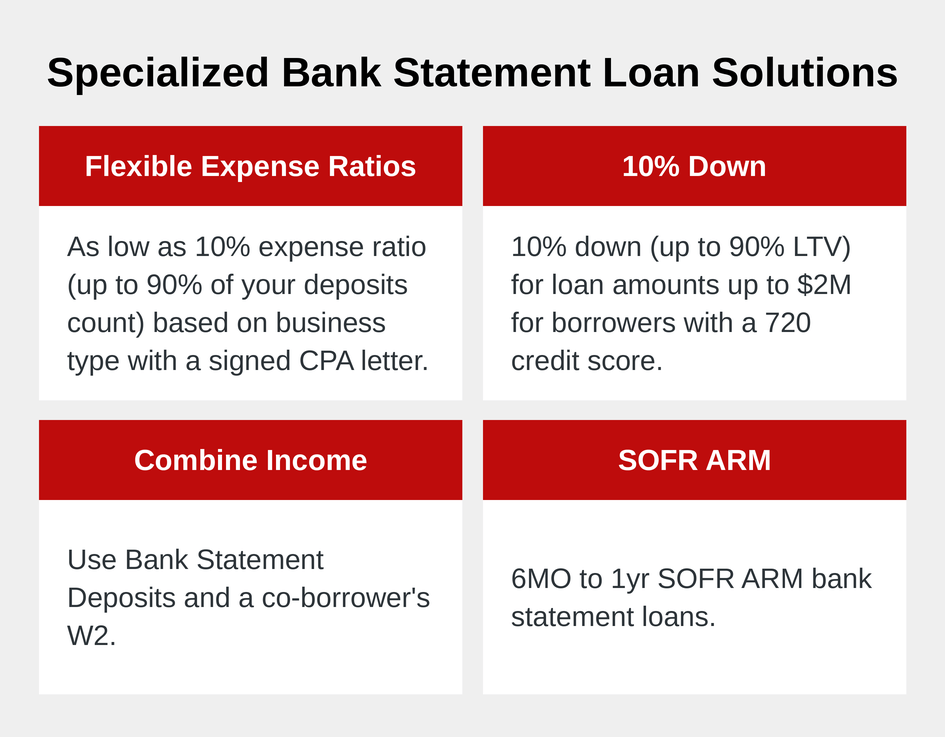

Griffin Funding is the best bank statement loan lender for self-employed business owners who want competitive rates, fast closings, and flexible underwriting without tax returns. As one of the most active bank statement lenders nationwide, Griffin qualifies borrowers using business bank statements with expense ratios as low as 10% (with CPA verification), maximizing buying power for entrepreneurs. One of Griffin’s fastest bank statement loans in 2026 closed in just 6 days.

The lender offers 30-year fixed, 40-year fixed, adjustable, and interest-only payment options with loan amounts up to $4,000,000. Our non-QM loans include specialized products like bank statement home equity and bank statement cash-out refinance. A minimum 620 credit score keeps these programs accessible to a broad range of business owners.

Unlike many competitors, Griffin originates bank statement loans nationwide and holds full state licenses as a non-bank mortgage lender in 47 states plus DC. It is supervised by state mortgage regulators and the CFPB, plus carries VA-Approved Lender and HUD FHA Non-Supervised Lender authority. This combination of reach and regulatory backing makes Griffin a reliable partner for borrowers almost anywhere in the country.

Pros:

- Fast approvals and fundings: Most applications receive decisions within 24-48 hours; fundings as quick as 6 calendar days for complete files. Year-to-date in 2026, Griffin averaged 38 days, with timelines improving rapidly thanks to LIA—its proprietary AI-powered non-QM underwriting agent and bank statement income calculator – no more PDFs.

- Flexible guidelines: Underwriting considers the full business profile rather than rigid boxes.

- Diverse terms: 30-year fixed, 40-year fixed, ARM, and interest-only options help optimize payments.

Cons:

- Limited availability: Not licensed for bank statement loans in Alaska, Missouri, and New York.

The Griffin Gold app streamlines the application process, while our extensive testimonials demonstrate consistent customer satisfaction across different investor profiles.

Farm Bureau Bank Overview

Farm Bureau Bank offers a strong bank statement loan program tailored for self-employed borrowers and 1099 contractors who want to qualify based on actual cash flow without tax returns. As a federal savings bank, it provides portfolio flexibility with competitive options for owner-occupied, second homes, and investment properties.

Borrowers can use 12- or 24-months of personal or business bank statements (as little as 50% business ownership for business statements or 25% for personal). Default expense factor is 50%, with lower factors possible via CPA/tax preparer verification (higher for certain industries like restaurants). P&L statements and 1099 options are also available. Loan amounts reach up to $4 million with various term structures.

Pros:

- Flexible cash-flow qualification: Reviews real deposits and supports lower expense ratios with documentation, helping self-employed borrowers maximize qualifying income.

- Broad property eligibility: Supports owner-occupied, second homes, and investment properties alongside strong government loan options (FHA/VA as a Supervised Mortgagee).

- Efficient for members: Digital tools and bank integration streamline the process for Farm Bureau members across participating states.

Cons:

- Expense factor defaults: Starts at a more conservative 50% (vs. more aggressive lenders), requiring extra CPA support for the lowest ratios.

- MLO licensing limitations: Individual Mortgage Loan Officers operate primarily under the bank’s federal charter and NMLS registration rather than holding traditional state-specific mortgage originator licenses in every jurisdiction, which some borrowers may see as a difference in direct individual-level oversight compared to non-bank lenders.

- Membership/availability focus: Best for those in participating states; operates under federal charter with NMLS registration (ID 2214437) rather than broad state-by-state mortgage licensing.

CrossCounty Mortgage Overview

CrossCountry Mortgage provides accessible bank statement loans for self-employed borrowers and business owners who need to document income through deposits rather than traditional tax returns or W-2s. As a large national non-bank lender, it emphasizes speed and flexibility in its Non-QM programs.

Its Signature Expanded Bank Statement loan reviews 12- or 24-months of personal or business bank statements to calculate qualifying income based on cash flow. Borrowers can reach up to 90% LTV in some cases, with DTI up to 50%. Loan amounts go into the millions with competitive terms for purchase, rate-and-term, and cash-out scenarios. FastTrack underwriting often enables quick decisions and closings (as fast as 10 days reported in some cases).

Pros:

- Fast processing: Digital tools and streamlined review deliver quick approvals, ideal for self-employed borrowers needing speed.

- Higher LTV/DTI flexibility: Supports borrowers with solid cash flow but less conventional documentation.

- Nationwide reach: Licensed in 50 states + DC with CFPB oversight and VA/FHA Non-Supervised approvals for added options.

Cons:

- Credit and documentation thresholds: While accessible, minimum credit and statement quality requirements can still exclude some edge cases compared to more aggressive specialists.

- Rate variability: Non-QM pricing (including bank statement) may be higher than prime conventional loans, though competitive within the space.

CrossCountry’s broad licensing (50 states + DC) and full Non-QM suite make it a reliable, scalable option for self-employed borrowers across most of the country.

North American Savings Bank Overview

North American Savings Bank (NASB) excels in bank statement loans for self-employed borrowers, 1099 contractors, and entrepreneurs who qualify via real cash flow from personal or business bank statements instead of tax returns or pay stubs. As a federally chartered savings bank with portfolio lending capabilities, it offers strong flexibility for non-traditional income.

Programs typically review 12- or 24-months of statements to assess deposits and cash flow. NASB supports a range of Non-QM products alongside bank statement options, with nationwide availability through its bank charter. It combines this with FHA/VA approvals (as a Supervised Mortgagee) for borrowers who may layer programs.

Pros:

- Portfolio flexibility: As a bank, NASB can accommodate unique self-employed scenarios with in-house underwriting and creative structuring.

- Strong Non-QM focus: Dedicated bank statement support for entrepreneurs, plus complementary options like 1099 and DSCR for investors.

- Nationwide service: Operates without heavy reliance on state-by-state mortgage licenses, backed by OCC regulation and explicit FHA approval.

Cons:

- Underwriting depth: May request additional documentation for thorough review, which can extend timelines compared to fully automated lenders.

- MLO licensing limitations: Individual Mortgage Loan Officers operate primarily under the bank’s federal charter and NMLS registration rather than holding traditional state-specific mortgage originator licenses in every jurisdiction, which some borrowers may see as a difference in direct individual-level oversight compared to non-bank lenders.

- Closing variability: Some borrowers report longer-than-expected closings depending on file complexity, though bank resources help mitigate this.

NASB’s combination of bank statement expertise, federal oversight (OCC, Supervised Mortgagee for FHA/VA), and portfolio approach makes it appealing for self-employed borrowers seeking reliable, scalable financing.

Angel Oak Overview

Angel Oak Mortgage Solutions is a leading Non-QM specialist with robust bank statement loan programs designed for self-employed borrowers, investors, and those with complex income who don’t fit traditional guidelines. As a wholesale-focused lender, it emphasizes flexible documentation and strong tech tools.

Bank statement loans typically require a minimum 640 credit score and review 12- or 24-months of statements (personal or business). Loans up to $4 million are available (minimum ~$150k), with LTVs up to 90% for certain scenarios. It supports purchase, cash-out refinance, rate-and-term, and delayed financing on owner-occupied, second homes, and investment properties. QuickQuote pricing engine speeds pre-qualification.

Pros:

- Non-QM expertise: Deep experience with bank statement and alternative documentation leads to creative solutions for self-employed and underserved borrowers.

- Competitive LTV and amounts: High loan limits and strong LTV options help maximize borrowing power.

- Tech efficiency: Tools like QuickQuote provide fast insights, backed by licensing in 46 states + DC.

Cons:

- Wholesale model: Primarily works through brokers, which may add a layer for direct-to-consumer borrowers.

- Limited government options: Focuses on Non-QM; no prominent FHA/VA approvals identified, so best for pure alternative documentation needs.

Angel Oak’s specialization in bank statement and Non-QM lending, combined with broad state licensing (46 states + DC) and CFPB oversight, positions it as a go-to for self-employed borrowers seeking flexible, high-LTV solutions.

Newfi Overview

Newfi Lending delivers flexible bank statement loans for self-employed borrowers and business owners, leveraging technology like its Income IQ automated bank statement analysis tool to streamline income verification and underwriting.

Programs accept 12- or 24-months of business or personal bank statements (along with 1099 or P&L options), with credit scores starting around 640. Loan amounts range from $100,000 to $5 million, supporting purchase, refinance, and cash-out with LTVs up to 90% (purchase/rate-term) or 80% (cash-out). It focuses on real deposit activity rather than taxable income for stronger qualifying power.

Pros:

- Tech-driven efficiency: Income IQ tool automates bank statement analysis for faster, more accurate reviews and quicker decisions.

- High loan limits and flexibility: Up to $5M with multiple documentation options tailored to self-employed cash flow.

- Strong regulatory backing: Licensed in 48 states + DC with explicit HUD FHA Non-Supervised (ID 0038900004) and VA approvals.

Cons:

- Process nuances: While online tools are powerful, final terms may adjust after full review or loan officer consultation.

- Wholesale-focused model: Newfi primarily operates as a wholesale lender through mortgage brokers, which can introduce intermediary (middleman) fees or additional costs/layers compared to direct-to-consumer lenders.

- Primary focus: Strong on self-employed/Non-QM but may not suit every primary residence scenario as seamlessly as dedicated consumer-direct lenders.

Newfi’s blend of technology (Income IQ), high limits, and solid licensing makes it a competitive choice for self-employed borrowers prioritizing speed and documentation flexibility.

Which Bank Statement Loan Lender Is Right for You?

The best bank statement loan lender depends on your qualified deposits, expense ratio, credit score, property type, down payment, and assets. Use this table to match your situation to the right lender.

| Self-Employed Borrower Situation | Best Bank Statement Loan Lender(s) | Why |

|---|---|---|

| Speed-focused (quick close needed) | Griffin Funding or CrossCountry Mortgage | Griffin closed some bank statement loans in as few as 6 days in 2026 using its AI-driven LIA underwriting and income calculator; CrossCountry’s FastTrack process often enables decisions in 24-48 hours and closings as fast as ~10 days. |

| Southeast market | Angel Oak | Strong regional expertise and Non-QM focus in Southeast core markets; flexible bank statement programs with QuickQuote tech for fast pre-qualification. |

| Self-employed with a growing business | North American Savings Bank (NASB) or Newfi | NASB’s portfolio lending as a bank allows creative structuring for growing self-employed borrowers; Newfi offers high loan limits (up to $5M) and Income IQ automation for efficient scaling. |

| Borrowers who prioritize transparent, predictable pricing | CrossCountry Mortgage | Clear upfront pricing and streamlined Non-QM bank statement review with fewer surprises; consistent underwriting across its 50-state footprint. |

| Complex borrower profile needing flexible underwriting | Griffin Funding or Angel Oak | Griffin considers the full business profile with aggressive expense ratios (as low as 10% with CPA) and 620 min FICO; Angel Oak excels in Non-QM flexibility for unique self-employed cash-flow situations. |

| Rate-conscious (want lowest all-in cost) | Griffin Funding or Farm Bureau Bank | Griffin avoids certain surcharges and offers competitive Non-QM rates with flexible terms; Farm Bureau Bank (as an OCC-regulated FSB) provides stable bank pricing plus access to government programs where applicable. |

| First-time self-employed buyers | Griffin Funding or CrossCountry Mortgage | Griffin’s 620 min FICO, no prior investment experience required in many cases, and fast 24-48 hour pre-approvals; CrossCountry offers accessible bank statement qualification with broad support. |

| Investment Properties | Angel Oak or Griffin Funding | Angel Oak supports flexible Non-QM bank statement programs for investment properties; Griffin accepts strong bank statement history or comparable rent schedules with flexible underwriting. |

| Scaling a rental portfolio (BRRRR or self-employed cash-out strategy) | Griffin Funding or NASB | Griffin has no strict limits on financed properties and strong cash-out options underwritten on individual bank statement profiles; NASB’s portfolio approach as a bank supports volume and creative equity extraction. |

Your choice should align with your timeline, geographic focus, and financing complexity. Consider checking Griffin Funding mortgage rates and using our Bank statement loan calculator to compare options before making your final decision.

Why Choose Griffin Funding for Your Bank Statement Loan?

Griffin Funding pairs competitive rates with fast closings, and our coverage across 47 states plus DC means consistent service whether you’re buying close to home or relocating for work.

We built our process around how self-employed business owners actually qualify. Each borrower works with a dedicated, individually licensed mortgage loan officer who knows how to read deposits, separate business from personal accounts, and structure a file that gets approved. That hands-on work, plus a streamlined pre-qualification, helps self-employed buyers move quickly when they’re competing for a home. And because Griffin runs multiple bank statement programs rather than one rigid set of guidelines, there’s usually a path that fits your business.

Ready to see your options? Get pre-qualified today to understand your purchasing power and put Griffin’s self-employed-focused bank statement programs to work.

Explore Bank Statement Mortgage Solutions

The right bank statement lender combines competitive rates, dependable service, and a program that fits how your income actually works. For self-employed borrowers, that last part is what separates an approval from a denial, and it’s where Griffin’s underwriting is built to help.

Whether you’re buying your first home, moving up, or downsizing, working with a lender experienced in self-employed income gives you the qualification expertise and the speed that competitive markets demand.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What is the best bank statement lender in 2026?

For most self-employed business owners who want competitive rates, individually licensed loan officers, and fast closings, Griffin Funding offers the strongest combination. Our fastest bank statement loan in 2026 closed in 6 days. Get pre-qualified with Griffin to compare our terms against other lenders.

What expense ratio do most lenders require?

Are bank statement loans hard to get?

The main advantage is that you skip the documentation that trips up business owners: no tax returns, no pay stubs, no profit-and-loss gymnastics. Instead, lenders review 12 or 24 months of business or personal bank statements to establish your income, and may ask for a signed CPA letter to confirm your expense ratio. Working with a lender experienced in self-employed income, like Griffin Funding, keeps the process straightforward and fast.

What questions should I ask my bank statement loan mortgage lender?

- What are the interest rate, loan terms, and fees?

Understand the interest rate on the loan, whether it's fixed or adjustable, and how it will affect your monthly payment and the overall cost of borrowing. Ask about the loan term, the repayment schedule, and whether any interest-only, 40-year, prepayment penalty, or balloon options apply, since self-employed borrowers often benefit from the flexibility these terms provide.

To determine the total cost of borrowing, ask about:

- Origination fees

- Discount points

- Closing costs

- Any other fees associated with the loan

- How do you calculate my income, and how many months of statements do you need?

This is the question that matters most on a bank statement loan, because the answer determines how much home you qualify for. Ask your lender:

- Whether they require 12 or 24 months of statements, and whether they accept personal accounts, business accounts, or both.

- What expense ratio they apply, and whether a signed CPA letter can lower it so more of your deposits count as income.

- Whether you can combine bank statement income with a co-borrower's W-2 income to strengthen the file.

- What property types and occupancy options qualify?

Eligible property types and occupancy can vary between lenders. Ask whether the loan can be used for a primary residence, second home, or investment property, and confirm any restrictions on condos, townhomes, or multi-unit properties. Also confirm which loan purposes are allowed, such as purchase, rate-and-term refinance, and cash-out refinance.

- Are you experienced with bank statement loans and self-employed borrowers?

Working with a lender experienced in bank statement loans matters because qualifying self-employed income is judgment-intensive work. Key features of an experienced bank statement lender include:

- Understanding self-employed borrowers' needs and structuring financing around how business owners actually earn and document income.

- Expertise in reviewing deposits to accurately calculate qualifying income, separate business from personal accounts, and apply the right expense ratio for your business type.

- A streamlined approval process because the lender understands the documentation, underwriting criteria, and verification steps specific to self-employed income, which speeds up approval and funding.

- Multiple funding sources with an appetite for all types of bank statement Non-QM loans. The lender should not rely on a single money source with one rigid set of guidelines. Not all self-employed borrowers look the same on paper, so when a lender has access to funding from private equity, securitization, and large insurance companies, your loan has a better chance of closing.

What is a good rate for a bank statement loan?

For most self-employed borrowers, the more useful comparison isn't the conventional rate they could get, it's the conventional loan they can't qualify for at all, because their tax returns understate their real income after write-offs. A bank statement loan trades a modest rate premium for an approval. Griffin Funding's current bank statement loan rates are available on the rates page.

Do you need 20% down for a bank statement loan?

For borrowers with a lower credit score, a higher down payment is more typical. A larger down payment generally lowers your interest rate, reduces your monthly payment, and strengthens your file when your documented income is closer to the qualifying minimum. Lenders may also ask for cash reserves on top of the down payment, with the amount depending on your credit profile, loan size, and the strength of your deposits.

Who is the best bank statement lender for first-time home buyers?

Which bank statement loan lender is best for borrowers with lower credit scores?

It is worth noting that most bank statement lenders price most aggressively at 720+ FICO, so raising your score before you apply can meaningfully lower your rate, even on a bank statement loan.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...