VA Loan Requirements Explained: Who Qualifies for a VA Loan?

KEY TAKEAWAYS

- If you meet the VA’s minimum service requirements, you can use a home loan after getting out of the military.

- The VA and your lender have various requirements you and the property must meet to qualify for the VA loan.

- Griffin Funding can help you determine your VA loan eligibility and walk you through the application process to secure financing for a home.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformIf you qualify for a VA loan, you can access lower interest rates, minimal closing costs, no down payment requirement, and more favorable loan terms. Learn more about the VA loan requirements to see if you’re eligible for this type of financing.

One of the most significant benefits of becoming a member of the military is being able to get a VA loan. The VA loan comes with flexible lending requirements that make it easier for active duty service members, veterans, and surviving spouses to secure financing for their dream homes.

Can you use a VA loan after getting out of the military? Absolutely! However, you must meet certain VA and lender requirements. The VA loan is intended to help active or veteran military members purchase a home with benefits like zero percent down payments, so you can use it whether you’re still in the military or retiring from your military duties.

KEY TAKEAWAYS

- If you meet the VA’s minimum service requirements, you can use a home loan after getting out of the military.

- The VA and your lender have various requirements you and the property must meet to qualify for the VA loan.

- Griffin Funding can help you determine your VA loan eligibility and walk you through the application process to secure financing for a home.

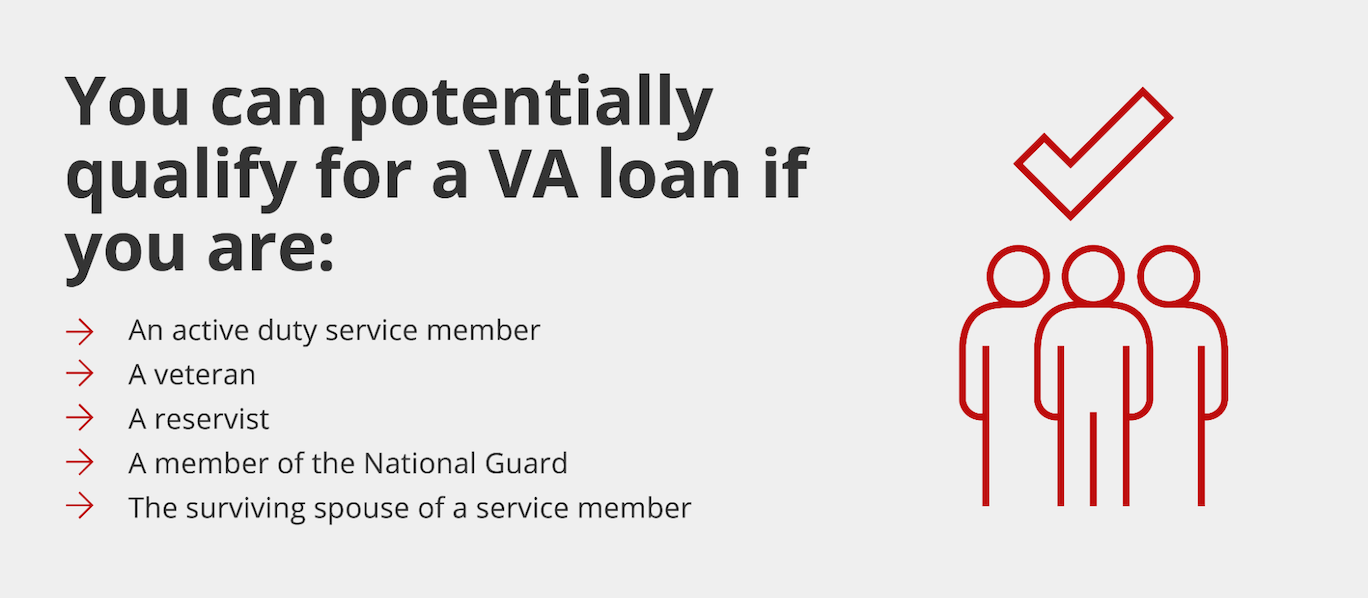

Can You Use a VA Loan After You Get Out of the Military?

While there are several types of VA loan borrowers, the two most common are:

- Individuals on active duty who want to purchase a home where they’re stationed

- Veterans who have retired from the military

So can you use a VA loan after you get out of the military? Of course, as that’s usually when most military members begin settling down. However, as we’ve mentioned, you can also use your VA loan while in the military.

To be eligible for a VA loan, whether in the military or as a retired veteran, you must meet the US Department of Veterans Affairs (VA) minimum service requirements. Ultimately, your eligibility depends on when you served, the length of service, and the branch you served in. In general, the minimum service eligibility requirements are as follows:

- 90 consecutive days of active service during wartime

- 181 days of active service during peacetime

- Six years in the National Guard or Reserves (or 90 days under Title 32 orders)

- Spouse of a service member who died in service or from a service-related disability

In addition to your length of service, your eligibility may be determined by the type of discharge you received. If you receive an honorable or general discharge, you will likely meet the VA loan requirements. However, you may not be eligible if you received an other-than-honorable or dishonorable discharge.

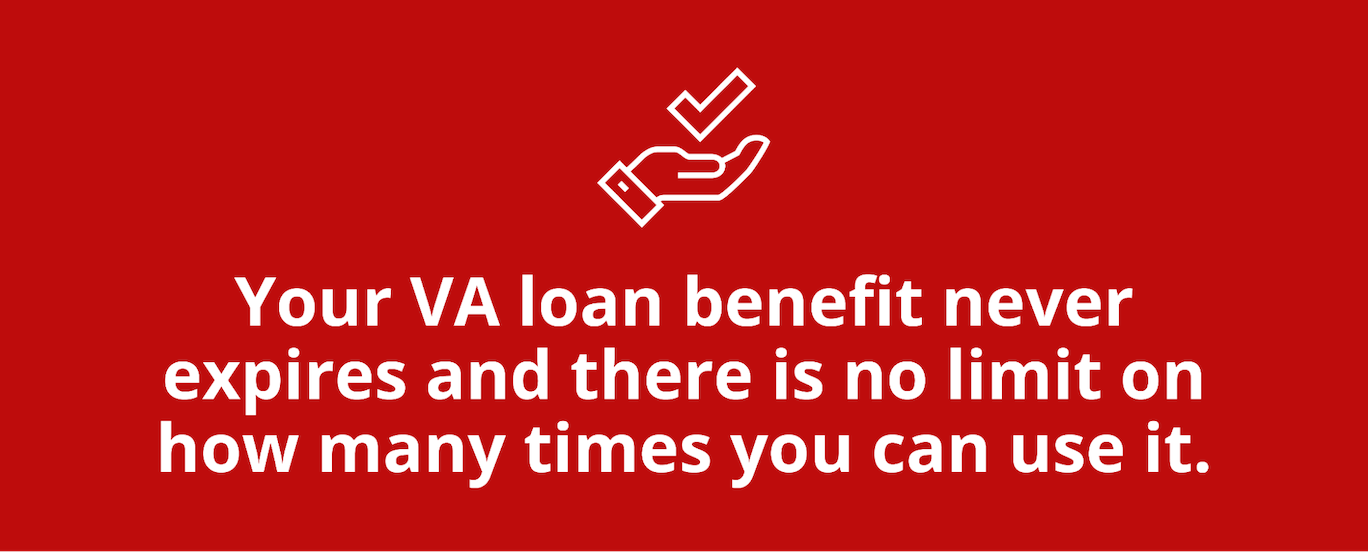

Do VA Loan Benefits Expire?

VA loan benefits don’t expire, so you can use them at any point after getting out of the military. Additionally, you can use this benefit as many times as you want as long as you have remaining entitlement. Your VA entitlement is the amount of your loan the VA will guarantee, meaning the amount they’ll pay the lender if you default on the loan. The VA guarantees up to 25% of the VA home loan, allowing you to multiply your remaining entitlement by four to determine the maximum amount you can borrow based on whether you have full or partial entitlement.

If you have your full entitlement, your Certificate of Eligibility (COE) will list $36,000 as your remaining entitlement. This number isn’t how much you can borrow. Instead, it tells lenders that you have your full entitlement. The VA loan doesn’t have loan limits to how much you can borrow if you have your full entitlement; they will guarantee 25% of the loan.

If you’ve used your VA loan prior to getting out of the military and haven’t restored your entitlement, you have a partial entitlement, which may require you to make a down payment on your next VA loan to cover the VA’s 25% guarantee to the lender. Your remaining entitlement is based on how much of your entitlement you’ve already used and current conforming loan limits.

VA Home Loan Requirements

If you meet the VA’s minimum service requirements, you’re eligible for a VA loan. However, the VA has other requirements you must meet before a lender can accept your application. In addition, you must meet the lender’s criteria to be eligible for the loan. A few of the most important VA loan requirements include the following:

VA Minimum Property Requirements

The VA’s minimum property requirements (MPRs) protect borrowers, lenders, and the VA by ensuring the safety and structural integrity of the home by looking for potential issues like lead-based paint and pests and ensuring the property has things like:

- Working heating, cooling, and electrical systems

- Adequate roofing

- Clean water supply

- Sanitary sewage disposal

- Accessibility from public and private streets

- Sufficient living space

- Accessible attics and crawl spaces with ventilation

If, for some reason, the home doesn’t meet these requirements, it’s not eligible for the VA loan, even though you, as the borrower, are. In these cases, you have a few options, such as finding a new home to purchase or asking the current homeowner to fix the issues and have the VA perform another inspection to approve the property for the loan.

Property Type

The VA requires that the property you purchase will serve as your primary residence. Most lenders allow you to secure a VA loan for a single-family home, condo, or townhome. However, some lenders might not allow manufactured homes.

VA loans can only be used for primary residences. Therefore, they cannot be used to explicitly purchase vacation homes, rentals, or investment properties. However, there are several caveats.

For example, if you own a home and have met the VA loan occupancy requirements, you may be able to purchase another home and rent your previous home out for an additional income. You can also buy a multi-unit property with your VA loan and live in one of the units while renting the other ones out.

Credit Score

The VA doesn’t have a minimum credit score requirement, but lenders do. The minimum credit score to qualify for a VA loan varies by lender, but most like to see a credit score of at least 500. Some lenders may be more lenient than others, depending on your financial situation. Therefore, you can get a VA loan with poor credit, but they typically come with higher interest rates.

Income

You need income to qualify for a home loan because lenders must be able to assess your ability to afford monthly mortgage payments. Lenders will also use your income to calculate your debt-to-income (DTI) ratio. Your DTI tells lenders what percentage of your income goes toward paying debts, and they typically prefer DTIs at or below 43%.

Loan Limits

As we mentioned earlier, VA loan limits don’t apply if you have your full entitlement. However, if you have partial entitlement, the amount you can borrow for a VA loan before making a down payment will be based on conventional conforming loan limits.

High-cost living areas have higher loan limits, but your remaining entitlement will determine how much you’ll have to pay out of pocket to reach the 25% guarantee necessary for the lender to approve your VA loan application.

Down payment

Comparing VA loans vs. conventional loans, you’ll find that the most significant benefit of VA loans is that they don’t have a down payment requirement as long as you have your full entitlement. However, some lenders may choose to require a down payment if you have a low credit score.

How to Determine Your VA Loan Eligibility

The easiest way to determine if you’re eligible for a VA loan is to obtain your Certificate of Eligibility (COE). This document tells you if you qualify and how much of your entitlement you have remaining. You must also ensure that you’re eligible for a VA loan through a lender by meeting all of their requirements. Requesting your COE by mail from the VA can take six months. Since time is of the essence when you’re purchasing a home, Griffin Funding can help you streamline the process of obtaining your COE.

However, if you’re not quite ready to begin the application process, you can request your COE from the VA online or by mail.

After you obtain your COE and have determined your eligibility, you can work directly with your lender to ensure you meet their lending requirements. The lender will request the VA appraisal of the property and review all of your financial information to determine whether to accept your application.

Why Take Out a VA Loan?

The VA loan was designed to help eligible borrowers who have served our country secure financing for a home. A few benefits of this program include the following:

- Competitive VA rates

- No down payment required

- No private mortgage insurance (PMI) required

- Flexible lending requirements

Download the Griffin Gold app today!

Take charge of your financial wellness and achieve your homeownership goals

Use invitation code: GRIFGOLD to register.

How to Apply for a VA Home Loan

When you’re ready to begin the VA loan application process, Griffin Funding can help. You can apply online or contact us to begin the application via phone. Our VA loan process looks something like this:

- Discovery meeting: Our loan officers review your VA loan eligibility to provide you with a quote and details about your options.

- Lock in your rate: With your quote, you can lock in your interest rate.

- Apply for a loan: Complete the application process online or via the phone with a loan officer.

- Underwriting: We’ll request the necessary documentation and begin the underwriting process

- Appraisal and inspection: You schedule a VA appraisal to evaluate the safety, sanitation, and structural integrity of the property.

- Approval: We’ll review your final loan documents and determine whether to approve your application.

See If You Are Eligible for a VA Loan

If you meet VA loan qualification requirements, this opens the door to great opportunities when it comes to buying and refinancing. Qualifying for a VA loan can be a pathway to affordable homeownership and a streamlined mortgage process.

You’re eligible for a VA loan after retiring from the military as long as you meet the VA loan requirements. However, you must meet the VA’s and your lender’s requirements to qualify for a VA loan.

Wondering if you fulfill the VA’s home loan requirements? Contact Griffin Funding today. We can request your COE to determine your eligibility and proceed with the pre-approval process. Reach out to get started!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What can disqualify you from getting a VA loan?

If your loan is denied, your loan officer should provide a reason for your denial so you can make the necessary changes before you apply again.

Is it hard to qualify for a VA loan?

If you don’t meet the minimum requirements to qualify for a VA loan, it can be harder to get approved. However, you can reapply for a loan if your application was denied. Make sure you find out why your application was denied and work on solving those problems before you apply for a loan again.

What are the requirements to assume a VA loan?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

HELOC Draw vs Repayment Period

A home equity line of credit is a revolving credit line secured by your home that allows you to borrow money a...

What Is a Non-Traditional Mortgage and When Should I Use One?

What Is a Non-Traditional Mortgage? A non-traditional mortgage, also known as a non-QM loan, is a home loan th...

Griffin Funding vs United Wholesale Mortgage (UWM): Mortgage Lender Comparison

Company Overview: Griffin Funding vs United Wholesale Mortgage (UWM) Let’s look at each company in turn: who...