What Is a Non-Traditional Mortgage and When Should I Use One?

What Is a Non-Traditional Mortgage and When Should I Use One?

KEY TAKEAWAYS

- Non-traditional mortgages offer alternative qualification methods for borrowers who don’t meet conventional lending standards.

- These loans use bank statements, assets, or rental income instead of tax returns to verify your ability to pay.

- Self-employed individuals, real estate investors, and high-net-worth borrowers benefit most from non-traditional mortgage options.

- While interest rates may be higher, the flexibility often makes these loans worth considering when traditional financing isn’t available.

Getting turned down for a traditional mortgage doesn’t mean homeownership is out of reach. If you’re self-employed, have irregular income, or don’t fit standard lending criteria, non-traditional mortgage financing could be your solution. So, what is a non-traditional mortgage? These alternative mortgage loans look beyond your W-2s and tax returns to assess your true ability to repay.

Keep reading to learn the non-traditional mortgage definition, which loan types might work for your situation, and when using alternative financing makes sense for your homeownership or investment goals.

What Is a Non-Traditional Mortgage?

A non-traditional mortgage, also known as a non-QM loan, is a home loan that doesn’t follow the strict guidelines set by Fannie Mae, Freddie Mac, or the Federal Housing Administration (FHA). These loans center on flexibility in how lenders verify your income and assess your creditworthiness.

Unlike traditional mortgages that require W-2s, two years of tax returns, and consistent employment history, non-traditional loans look at alternative documentation. So, what are non-traditional mortgages really about? They give lenders freedom to evaluate borrowers based on actual cash flow, assets, or property performance rather than just tax returns.

Types of Non-Traditional Mortgage Products

Non-traditional mortgages come in several forms, each designed for different borrower situations. Each type has unique qualification criteria that can help you secure financing when conventional loans won’t work. The types of non-traditional mortgage products include:

DSCR Loans

DSCR Loans

Debt service coverage ratio (DSCR) loans are investment property loans that qualify you based on a property’s rental income. The lender calculates whether the property’s rent will cover the mortgage payment. These loans work well for real estate investors who want to expand their portfolio. Many people purchasing rental properties use DSCR loans because they can purchase multiple properties without debt-to-income ratio concerns.

Bank Statement Loans

Bank statement loans let you use 12 to 24 months of bank statements to document income instead of tax returns. Lenders analyze your deposits to determine your average monthly income. Business owners and self-employed professionals who write off significant expenses benefit most from this approach since bank statements show the actual money flowing through their accounts.

1099 Mortgage Loans

Independent contractors and freelancers who receive 1099 forms can qualify for a mortgage with their 1099 income documentation. Lenders review your 1099s from the past one or two years to establish consistent earnings. This option serves the growing gig economy workforce that traditional lenders often struggle to evaluate.

Asset-Based Loans

Asset-based loans qualify you using your liquid assets — stocks, bonds, retirement accounts, or cash reserves — rather than your monthly income. The lender calculates a hypothetical income by dividing your total qualifying assets by the loan term. Retirees and individuals with significant wealth but limited traditional income find these loans particularly useful.

Interest-Only Mortgages

Interest-only loans let you pay just the interest portion for a set period (usually 5-10 years) before the loan converts to principal and interest payments. Real estate investors and high-income professionals who expect income growth often choose this structure since the lower initial payments improve cash flow.

Foreign National Loans

Foreign national loans allow non-U.S. citizens without Social Security numbers to purchase U.S. property. These loans typically require more substantial down payments and use international credit reports. International investors and foreign nationals relocating to the United States can access U.S. real estate without citizenship.

Non-Traditional Mortgage Financing vs Traditional Lending

Non-traditional and conventional financing differ in more ways than just the paperwork you submit. Let’s take a look at how these home loan options compare:

- Approval process differences: Traditional loans follow strict guidelines with less flexibility for exceptions. Non-traditional mortgage loans use manual, common sense underwriting, where experienced underwriters evaluate your complete financial picture. This human element means your unique circumstances get proper consideration.

- Documentation required: Traditional lenders need W-2s, pay stubs, tax returns, and employment verification. Non-traditional products accept bank statements, 1099 forms, asset statements, or rental income documentation.

- How lenders assess risk: Conventional underwriting relies heavily on debt-to-income ratios calculated using income verified through tax returns. Non-QM lenders consider factors like property performance, asset depth, and overall financial profile. Additionally, non-QM loans are considered higher risk because they don’t meet standard qualified mortgage guidelines.

Who Should Consider a Non-Traditional Mortgage?

Non-traditional loans work best for borrowers with non-standard financial profiles. Several groups benefit most from these alternative lending options, including:

- Self-employed: Business owners who write off substantial expenses show lower taxable income than their actual cash flow. Self-employed mortgages let you qualify based on bank deposits rather than tax returns, accurately reflecting your true earning power.

- Freelancers and gig workers: Independent contractors juggling multiple clients often struggle with traditional lending requirements. Non-traditional mortgages recognize that stable income doesn’t always come from a single employer.

- Real estate investors: Experienced investors who own multiple properties often can’t qualify for more conventional loans because their debt-to-income ratio is too high. DSCR loans remove personal income from the equation entirely, letting the property’s rental income qualify you.

- Retirees with significant assets but low income: Living off savings means your tax returns show minimal income. Asset-based loans convert your wealth into qualifying income, letting you purchase a home or refinance a non-traditional mortgage without employment income.

- Foreign nationals: Buying U.S. property as a non-citizen creates unique challenges with traditional lenders who require Social Security numbers. Foreign national programs provide a clear path to ownership for international buyers.

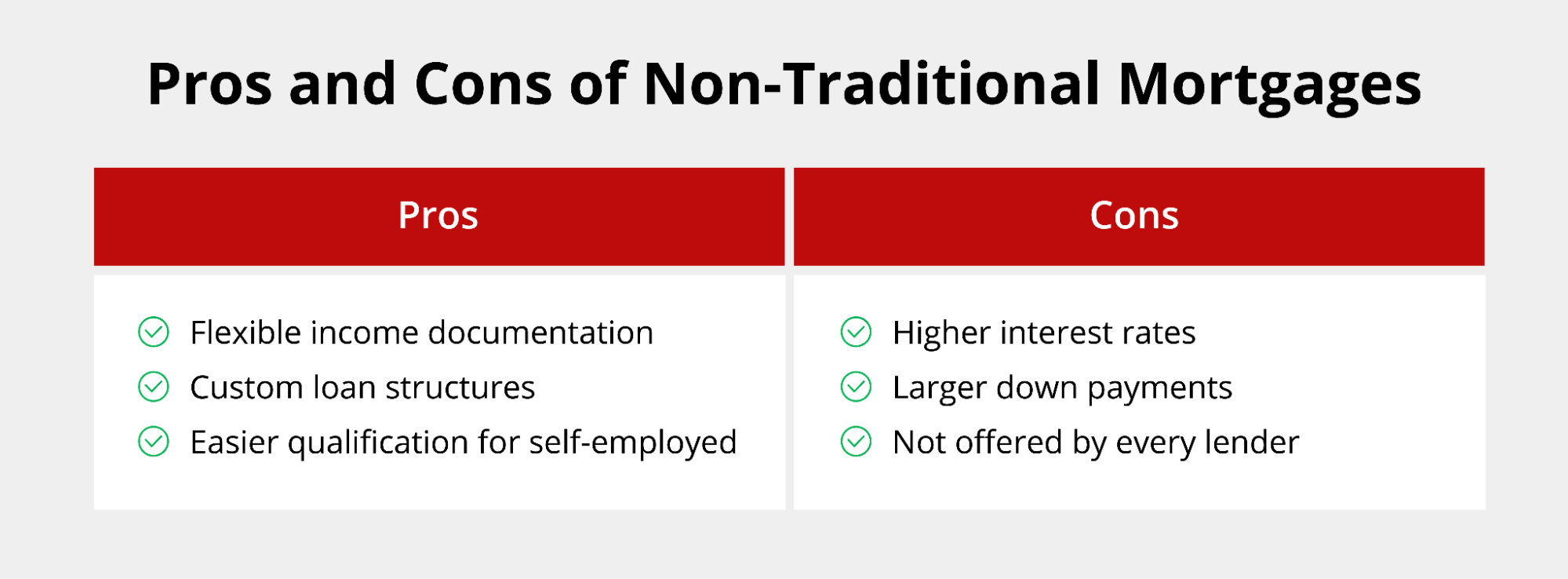

Pros and Cons of Non-Traditional Mortgages

Like any borrowing, non-traditional loans come with advantages and drawbacks.

Like any borrowing, non-traditional loans come with advantages and drawbacks.

The benefits of non-traditional mortgage loans include:

- Flexibility in documentation: With these loans, you’re not locked into rigid conventional lending requirements. Whether you’re self-employed, have irregular income, or receive compensation in non-traditional ways, there’s likely a documentation method that works for your situation.

- Customized loan structures: From interest-only payments to unique amortization schedules, non-traditional lenders can tailor loan terms to your needs. This customization simply isn’t available with conventional products.

- Easier qualification for non-W2 income earners: If you’ve struggled to qualify for a mortgage through traditional channels, non-QM loans level the playing field. You’re judged on your ability to repay the mortgage, not just your ability to produce specific documents.

While non-traditional mortgages offer flexibility, they come with some trade-offs you should consider. The potential cons of non-traditional mortgages include:

- Interest rates and pricing: In some cases, non-traditional mortgages can come with higher rates and fees. However, non-traditional mortgage rates are often competitive with, and in some cases lower than, conventional loan rates, especially for investment properties. While non-QM loans may appear higher on paper, traditional mortgages frequently include multiple Loan-Level Price Adjustments (LLPAs) for a variety of factors. These pricing hits can significantly increase the effective rate for conventional loans, sometimes making DSCR or bank statement programs more cost-effective overall.

- Stricter down payment requirements: Most non-QM loans require larger down payments than conventional loans. While this creates a higher barrier to entry, it also means you’re building equity faster.

- Limited availability: Not every lender offers non-traditional mortgages. You’ll need to work with specialized lenders who understand these loan types.

When Should You Use a Non-Traditional Mortgage?

Timing matters when choosing between traditional and alternative financing for your home or investment property purchase.

Non-traditional mortgages make sense if:

- You’ve been denied a conventional loan due to self-employment income, recent credit events, or documentation challenges.

- You’re a real estate investor who owns multiple properties and can’t qualify for more traditional loans because of debt-to-income ratios.

- You’re a foreign national without a U.S. credit history trying to purchase U.S. property.

- Your tax returns show low income, but you have significant assets or strong cash flow.

The question of whether to act now or wait to qualify for a traditional mortgage typically comes down to opportunity cost. Real estate opportunities don’t wait around while you spend years building the documentation profile traditional lenders want. Property values may rise, interest rates could change, or the perfect investment property might sell to someone else. If you can qualify for a non-traditional loan now, moving forward lets you start building equity and generating returns immediately rather than sitting on the sidelines.

Your timeframe also matters when deciding on non-traditional financing. These loans work well as short-term bridge financing if you plan to refinance once you can meet conventional requirements. Maybe you’re growing your business and expect your tax returns to reflect higher income in a couple of years. Or perhaps you’re using a non-traditional loan as part of your long-term investment strategy.

Active real estate investors often prefer non-QM loans permanently because DSCR and other programs don’t limit buying power based on personal income, making portfolio growth much easier.

Explore Your Non-Traditional Mortgage Options Today

Your mortgage approval shouldn’t depend on whether you fit into a narrow set of lending requirements. If your financial situation involves self-employment, investment properties, significant assets, or any other non-traditional aspect, you have options.

At Griffin Funding, we understand that real financial strength doesn’t always show up on tax returns. Our team evaluates your complete financial picture to find the non-traditional mortgage solution that fits your needs. Download the Griffin Gold app to explore your mortgage options or speak to a specialist who can guide you through your options.

Get started online today and take the first step towards pre-approval!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Is it hard to get a non-traditional mortgage?

How do I apply for a non-traditional mortgage?

Are non-traditional mortgages safe?

What is the best alternative financing option if I don’t qualify for a traditional mortgage?

- Bank statement loans for self-employed borrowers who want to use business deposits instead of tax returns.

- DSCR loans for real estate investors who qualify based on property cash flow rather than personal income.

- Asset-based mortgages for borrowers with significant savings, investments, or retirement accounts.

- 1099 and foreign national programs for freelancers or international buyers.

Are alternative mortgages safe and legitimate?

Unlike the “no-doc” loans from the early 2000s, today’s alternative home loans emphasize transparency, responsible underwriting, and sustainable payment structures. Reputable lenders like Griffin Funding specialize in alternative mortgage financing designed to help creditworthy borrowers achieve homeownership or expand investment portfolios safely.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...