Do HELOCs Have Closing Costs?

Do HELOCs Have Closing Costs?

KEY TAKEAWAYS

- Most HELOCs have closing costs, which can be structured as either a percentage of the total credit limit or a flat fee, depending on the lender.

- “No closing cost” HELOCs often offset fees through higher interest rates or early closure penalties.

- Comparing lenders, improving your credit profile, and reviewing your Loan Estimate carefully can help reduce total borrowing costs.

- Understanding when and how fees are paid helps you choose the most cost-effective home equity strategy.

A HELOC can be a flexible home equity solution that lets you borrow against your home as needed, but it’s important to understand the closing costs associated with a HELOC before applying. While these expenses are often lower than those associated with traditional mortgages, they can still impact your total borrowing costs. Here’s what to know about HELOC closing fees and what you might expect to pay.

Are There Closing Costs on a HELOC?

Yes, most lenders charge closing costs on a home equity line of credit, though they’re typically lower than the closing costs for a primary mortgage. In many cases, HELOC closing costs range from 2% to 5% of your total credit limit, or they may be structured as flat fees depending on the lender.

By comparison, traditional mortgage closing costs often range from 2% to 6% of the full loan amount, which can result in higher total fees due to larger balances.

Some lenders also offer “no closing cost HELOC” options, but these may come with higher interest rates or require you to keep the line open for a minimum period. Reviewing all fees carefully helps you determine the true cost of borrowing.

Common HELOC Closing Costs

Some of the most common HELOC closing costs include:

- Application fee: Some lenders charge a one-time application or origination fee to process your request. This may cover administrative and underwriting costs.

- Appraisal fee: An appraisal determines your home’s current market value and helps establish your available equity. Costs vary, but typically range from a few hundred dollars to over $500, depending on property type and location.

- Credit report fee: Lenders review your credit profile to assess risk, and this fee covers the cost of pulling your credit reports.

- Title search and title insurance: A title search confirms legal ownership and checks for liens. In some cases, lenders require title insurance to protect against claims or ownership disputes.

- Attorney or closing fees: Certain states require an attorney to oversee the closing process. Even where not required, administrative closing services may result in additional fees.

- Recording fees: Local governments charge fees to record the new lien against your property in public records.

- Annual fee (sometimes): Some HELOCs include an ongoing annual maintenance fee to keep the line of credit open, even after initial closing.

How Much Are Closing Costs for a HELOC?

In total, HELOC closing costs often range from $500 to $5,000, depending on your lender, loan size, and location. Some lenders use percentage-based pricing tied to your credit limit, while others charge mostly flat fees.

Because HELOC closing costs can vary significantly, using a closing cost calculator can help estimate your total expenses before applying. It’s also helpful to compare HELOC closing costs vs home equity loan fees, since home equity loans may have different fee structures and interest rate considerations.

Factors that impact HELOC closing costs include:

- Loan amount: Higher credit limits may increase percentage-based fees or require more comprehensive underwriting.

- Property value: Higher-value properties may involve more detailed appraisals or higher title-related costs.

- State regulations: Some states require attorney involvement or have higher recording fees, which can increase total costs.

- Lender policies: Fee structures vary widely. Some lenders bundle costs, while others itemize each charge.

- Whether an appraisal is required: If a full in-person appraisal is necessary, costs are typically higher than automated or drive-by valuation methods.

Does Every Lender Require HELOC Closing Costs?

Not always. While many lenders charge upfront fees, some choose to absorb certain costs as a competitive incentive. In these cases, the lender may cover appraisal, title, or application fees, but often with conditions attached. For example, you might be required to keep the line open for a set period or repay those costs if you close the account early. It’s also common for borrowers to ask, “are HELOC annual fees negotiable?”—and in some cases, they are, especially if you have strong credit or an existing relationship with the lender. Reviewing your official Loan Estimate carefully is essential, as it outlines all projected fees, repayment terms, and potential penalties.

What Is a No Closing Cost HELOC?

A no closing cost HELOC is a home equity line of credit where the lender advertises little to no upfront fees at closing. Instead of charging you out of pocket, lenders typically structure these products by rolling fees into the line of credit, offsetting them with a slightly higher interest rate, or adding an early closure penalty (often if the account is closed within the first 2–3 years). In some cases, the structure may resemble a fixed-rate HELOC option, where part of your balance converts to a fixed rate but pricing adjustments compensate for waived fees.

While avoiding upfront costs can be attractive, it’s important to evaluate the long-term expense. A higher rate or repayment penalty could cost more over time than paying closing costs upfront.

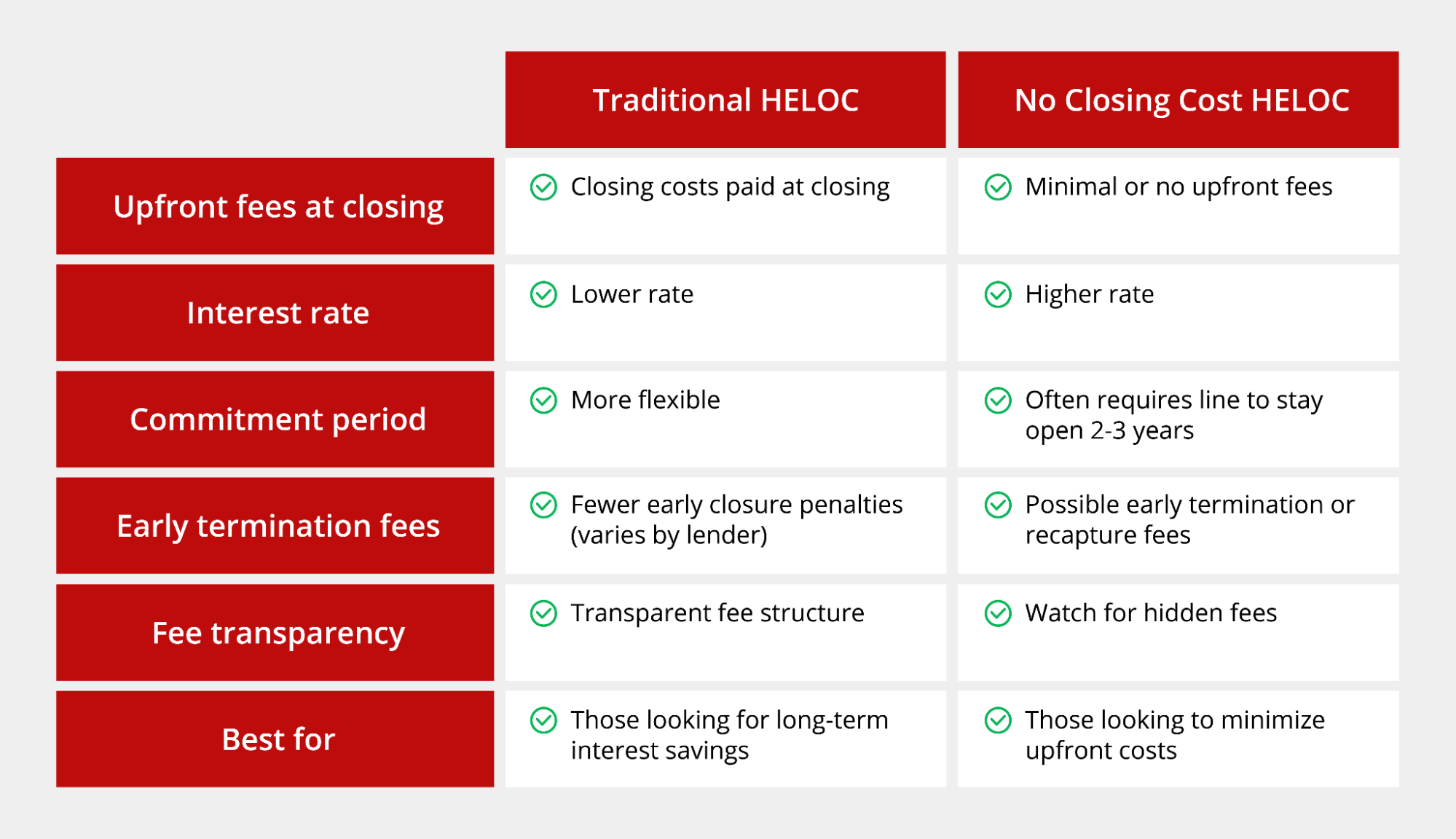

No Closing Cost HELOC vs Traditional HELOC

If you’re comparing options, especially as lenders promote HELOCs with zero closing fees in 2026, it’s helpful to understand the key differences.

No Closing Cost HELOC:

No Closing Cost HELOC:

- Minimal or no upfront fees at closing

- May include higher interest rate

- Often requires keeping the line open for 2–3 years

- Possible early termination or recapture fees

- Important to watch for hidden fees on no cost HELOCs

Traditional HELOC:

- Upfront closing costs paid at closing

- Typically lower interest rate compared to closing cost HELOC

- Fewer early closure penalties (varies by lender)

- More transparent fee structure

Both options still have similar HELOC requirements, such as credit score minimums, combined loan-to-value (CLTV) limits, and income verification standards. The right choice depends on how long you plan to keep the line open and whether paying upfront costs saves you more in long-term interest.

When Do You Pay HELOC Closing Costs?

HELOC closing costs are typically paid at closing, similar to a primary mortgage or home equity loan. Depending on the lender, you may pay fees out of pocket, have them deducted from your initial draw, or finance them into your available credit line.

In no-closing-cost structures, the lender may technically cover the fees upfront but recapture them through higher rates or early closure penalties.

Understanding how and when you pay is an important part of weighing the no closing cost HELOC vs traditional HELOC pros and cons before moving forward.

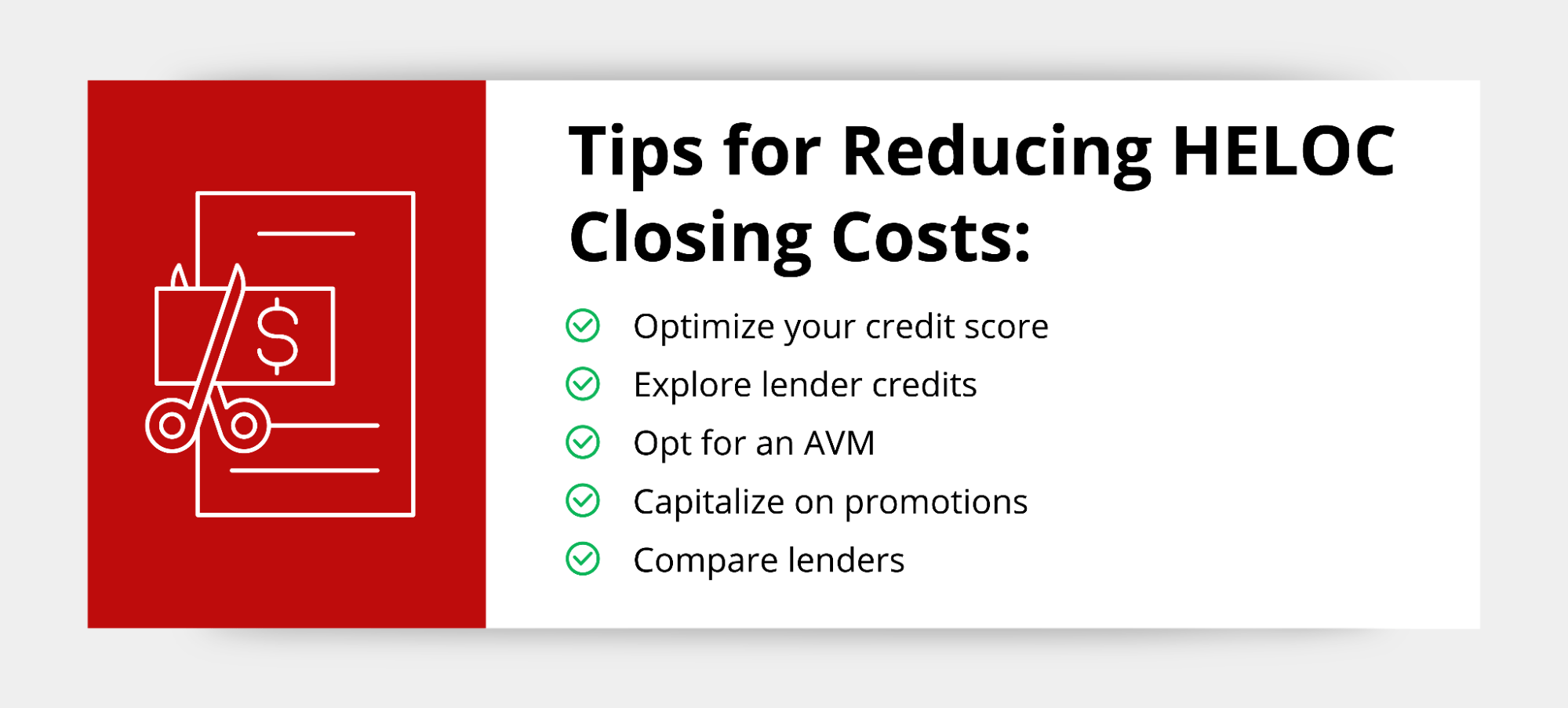

How to Reduce Closing Costs for a HELOC

There are several ways to potentially lower your HELOC expenses.

- Optimize your credit score: Improving your credit score before applying can help you qualify for better pricing and possibly reduced fees.

- Explore lender credits: You can also request lender credits or ask whether certain fees (like annual charges) can be waived.

- Opt for an AVM: If eligible, choosing an automated valuation model (AVM) instead of a full in-person appraisal may reduce appraisal costs.

- Shop around for promotional deals: Shopping promotional offers or limited-time lender incentives can also lower upfront expenses.

- Compare lenders: Comparing multiple lenders and using a HELOC closing cost calculator in 2026 can help you estimate total costs and identify the most competitive option.

See If a HELOC Is Right for You

A HELOC can be a flexible way to tap into your home’s equity, but it’s important to understand the average cost to open a HELOC in 2026, compare fee structures, and evaluate long-term repayment terms.

A HELOC can be a flexible way to tap into your home’s equity, but it’s important to understand the average cost to open a HELOC in 2026, compare fee structures, and evaluate long-term repayment terms.

At Griffin Funding, we help borrowers explore HELOCs, home equity loans, and even specialty products like a DSCR HELOAN for investment-focused strategies. If you’re considering alternatives to a HELOC for home improvement, refinancing or fixed-rate equity products may also be worth reviewing.

With tools like the Griffin Gold app, you can monitor your mortgage profile, evaluate equity opportunities, and make informed decisions about leveraging your home’s value. Whether you’re consolidating debt, funding renovations, or planning for future investments, our team can help you compare options. Get started online and find the right solution for your goals.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can HELOC closing costs be negotiated?

Are HELOC closing costs tax deductible?

Is a HELOC worth it if there are closing costs?

Can I roll HELOC closing costs into the loan?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

America’s Self-Employment Boom is Creating a New Class of Real Estate Investors

Self-employed investors are reshaping the real estate market, fueling record-high rental property investment t...

Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

What to Look for in a Bank Statement Loan Lender Choosing the best bank statement loan lender for your situati...

Housing Market Data Tool: Access Local Housing Market Insights

Housing Market Insights Tool Access comprehensive local housing market data for any address or neighborhood in...