Mortgage Commitment Letter: What It Is & How to Get One

KEY TAKEAWAYS

- Mortgage commitment letters are formal promises from your lender to fund your home loan and represent a stronger indication of approval than pre-qualification or pre-approval documents.

- There are two types of commitment letters: conditional ones that have remaining requirements and final ones that indicate complete approval with all conditions satisfied.

- A commitment letter strengthens your position as a buyer and is typically required by a specific date in most purchase agreements.

- The commitment letter process takes 2-3 weeks after documentation submission, during which maintaining financial stability is essential to avoid approval issues.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformGetting a home loan involves several important steps, and one of the most critical milestones is receiving your mortgage commitment letter. This document is your lender’s formal promise to finance your home purchase, bringing you one big step closer to closing day.

If you’re going through the home-buying process, understanding what a mortgage loan commitment letter is and how to get one can make a huge difference in your experience. Let’s break down everything you need to know about this essential document.

What Is a Mortgage Commitment Letter?

A mortgage loan commitment letter is a formal document from a lender stating they’ve approved your mortgage application and are committed to providing the loan under specific terms. This document is one of the final stages in the mortgage approval process and indicates that the lender has thoroughly reviewed your financial information and property details.

Unlike mortgage pre-qualification, which is based on self-reported financial information, or mortgage pre-approval, which involves credit checks but not full underwriting, a home loan commitment letter comes after the lender’s underwriting team has evaluated your application, credit history, income verification, and often the property appraisal. This makes it a much stronger indication that your financing will go through.

When a lender issues this letter, they’re committing to lend you the money for the property as long as you meet specific conditions. It’s an important milestone that gives both you and the seller confidence that the deal will close successfully.

Types of Mortgage Commitment Letters

Not all commitment letters are created equal. Understanding the difference between the two main mortgage commitment types can help you know exactly where you stand in the mortgage process.

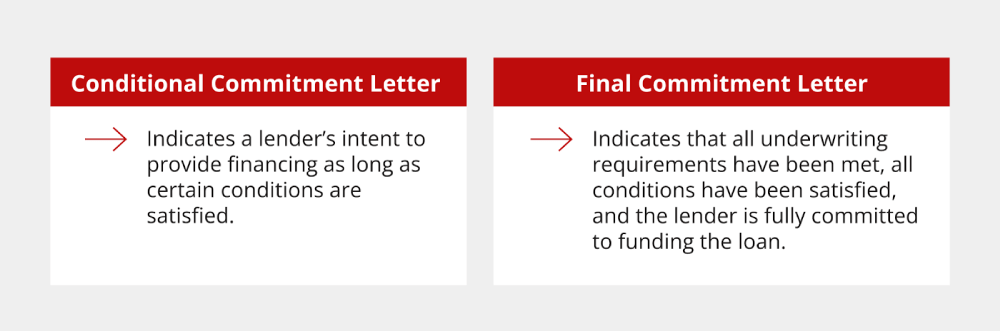

Conditional Commitment Letter

A conditional commitment letter is the most common type you’ll encounter first. As the name suggests, this document indicates the lender’s intent to provide financing but includes certain conditions that must still be satisfied.

These conditions might include:

- A satisfactory property appraisal that meets or exceeds the purchase price

- Final verification of employment just before closing

- Proof that you’ve obtained proper insurance coverage

- Resolution of any title issues discovered during the title search

- Satisfactory completion of any required home repairs

Think of a conditional commitment as your lender saying, “We’re prepared to give you this loan, provided these few remaining items check out.” Most homebuyers receive a conditional commitment initially, with conditions that are cleared one by one as you move toward closing.

Final Commitment Letter

The final mortgage commitment letter is the highest level of lender commitment. This document indicates that all underwriting requirements have been met, all conditions have been satisfied, and the lender is fully committed to funding your loan.

When you receive a final commitment letter, it means your loan is essentially ready to close. The only remaining steps typically involve scheduling the closing and signing the final paperwork. This is the document that gives both you and the seller maximum confidence that the financing is secure.

Some lenders may not issue a separate final commitment letter but will instead provide documentation that all conditions from your conditional commitment have been cleared.

Why a Mortgage Commitment Letter Is Important

Beyond simply being another step in the mortgage process, there are several reasons why securing a mortgage commitment letter is crucial:

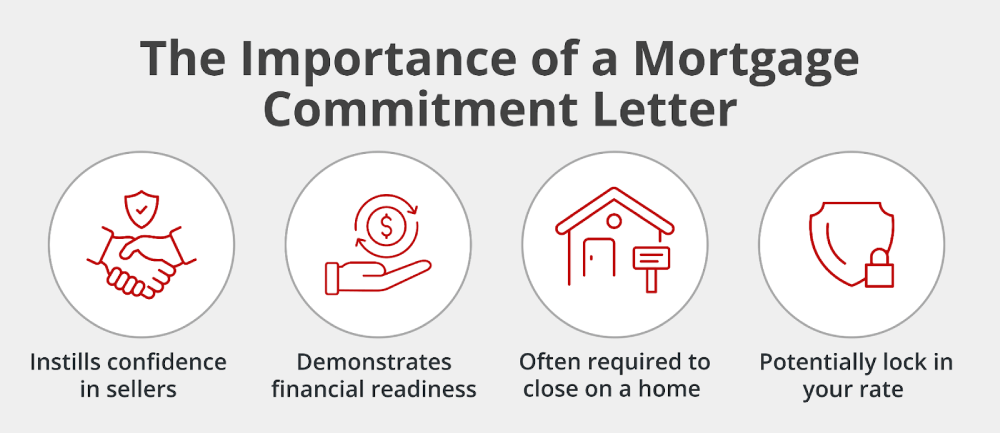

- Strengthens your offer to sellers: In competitive housing markets, having a commitment letter can give you an edge over other buyers who only have pre-approval. Sellers and their agents understand that a commitment letter represents a higher level of lender confidence, which reduces the risk of financing problems derailing the sale.

- Signals financial readiness: The commitment letter demonstrates that a lender has thoroughly evaluated your financial situation and found you creditworthy for the specific loan amount. This level of scrutiny goes beyond the preliminary checks done during pre-qualification or pre-approval.

- Required to move toward closing: Most purchase agreements include a mortgage commitment contingency, which requires you to obtain a commitment letter by a specific date. Without meeting this requirement, the seller could potentially terminate the contract, or you might lose your earnest money deposit.

- May be used to lock in interest rates: Depending on your lender and the terms in your commitment letter, this document may include a rate lock guarantee. This can protect you from interest rate increases that might occur between commitment and closing.

If this is your first time getting a mortgage, we recommend using a first-time home buyer checklist to help you understand the entire process, from pre-approval to closing.

How to Get a Mortgage Commitment Letter

Securing a mortgage loan commitment letter follows a specific process. Here’s how to handle each step:

- Step 1 – Get pre-approved by a lender: Before you can get a commitment letter, you’ll need to be pre-approved for a mortgage. This involves submitting preliminary financial information and having your credit checked. Organizing these documents for mortgage pre-approval can significantly speed up the process. Your lender may also provide a proof of funds letter that you can use to make your offer stronger.

- Step 2 – Submit required documentation: Once you’ve found a home and your offer is accepted, you’ll need to provide comprehensive documentation to your lender, which typically includes recent paystubs and W-2 forms, tax returns from the past two years, bank statements showing your assets, details about debts you have, and information about the property you’re purchasing. Using the Griffin Gold app can help streamline this process and ensure you submit all required documents.

- Step 3 – Undergo the underwriting process: The underwriting process is where your lender thoroughly reviews your financial situation and the property details. During this time, the property will be appraised to confirm its value, your credit, income, and assets will be verified, the title will be searched to ensure there are no issues, and your debt-to-income ratio will be calculated. Sometimes, the underwriter may request additional documentation, such as a letter of explanation for any unusual financial activities or verification of the source of your down payment funds.

- Step 4 – Receive conditional or final commitment letter: After completing the underwriting process, your lender will issue a conditional commitment letter outlining any remaining requirements. As you satisfy these conditions, you’ll move toward receiving a final commitment letter.

You can expect to receive your mortgage commitment letter in about 2-3 weeks after you’ve submitted all required documentation, though this can vary based on:

- The complexity of your financial situation

- Current lender workloads

- The type of loan you’re applying for

- Any issues discovered during underwriting

It’s crucial to maintain financial stability throughout this process. Avoid making major purchases, changing jobs, or taking on new debt, as these actions could affect your approval status. Even after receiving a commitment letter, these changes could potentially cause problems before closing.

Start Your Home Buying Journey Today

Getting a home loan commitment from a lender is a huge milestone in your path to homeownership. It provides peace of mind that your financing is secure and puts you in a stronger position with sellers.

If you’re ready to begin the home-buying process, Griffin Funding can guide you through every step. Our approach and personalized service make getting through the mortgage process easier.

Get started online and start your homeownership journey today!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What's included in a mortgage commitment letter?

Is a mortgage commitment letter the same as a pre-approval letter?

Can you be denied a loan after getting a loan commitment letter?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

Net Operating Income: Definition, Formula, & Examples

What Is Net Operating Income (NOI)? Net operating income measures how much money your investment property gene...

Best DSCR Lenders: Griffin Funding vs Angel Oak vs Kiavi vs Visio vs Lima One vs Easy Street

What to Look for in a DSCR Lender Choosing the best DSCR lender for your unique situation means evaluating sev...

Cash on Cash Return in Real Estate: Definition, Formula, & Examples

What Is Cash on Cash Return? Cash on cash return (CoC) is a metric that measures the annual income you generat...