What Is Mortgage Amortization?

What Is Mortgage Amortization?

KEY TAKEAWAYS

- Mortgage amortization determines how your monthly payment is divided between principal and interest and how quickly you build equity over the loan’s lifespan.

- Understanding your amortization schedule helps you forecast your payoff timeline, identify interest-saving opportunities, and decide when refinancing may be beneficial.

- Extra principal payments, biweekly payment strategies, or a shorter mortgage term can significantly reduce total interest paid.

Mortgage amortization is the built-in repayment plan that gradually pays off your home loan over time. Even though your monthly payment often stays the same, what that payment does changes as the years pass. Early on, you’re mostly covering interest on the loan, while later on you’re mostly paying down the balance. Knowing how amortization works makes it easier to understand your payoff path, total loan cost, and equity growth.

Mortgage Amortization Definition

Amortization means paying off a loan in regular, scheduled payments. With a mortgage, it’s the system that spreads your repayment across many years so the loan balance steadily declines to zero. Each payment is split between interest (the cost of borrowing charged by the lender) and principal (the amount you actually borrowed).

The amortization schedule is the map that shows that split for every payment you’ll make. Because amortization follows a predictable pattern, homeowners can clearly see how their balance will change over time. It also helps borrowers understand how much interest they’re really paying and how their equity will grow month by month.

How Mortgage Amortization Works

Here are the basics of how mortgage amortization works:

- Every payment is part interest, part principal. Interest is calculated on your remaining balance, and whatever is left from your payment goes toward principal.

- Early payments are interest-heavy. Because your balance is highest at the start, the interest portion takes up most of your payment, so principal falls slowly at first.

- Later payments shift toward principal. As the balance drops, interest charges shrink, and more of your payment goes toward reducing what you owe.

- The amortization schedule evolves as the loan matures. Month by month, the principal share rises and the interest share falls, speeding up payoff in the back half of the loan.

- Mortgage rate amortization and rate changes matter. For a fixed-rate loan, the split changes predictably. For adjustable-rate loans, a rate increase bumps up the interest share and can slow principal payoff; a rate drop does the opposite. Your mortgage term is also a crucial element since longer terms lower monthly payments but stretch interest costs over more time.

Why Amortization Matters for Homeowners

Understanding how mortgage amortization works is important for homeowners because it provides the following:

- A predictable loan payoff timeline: Amortization shows exactly when your mortgage will be paid off if you follow the amortization schedule, helping you plan long-range goals.

- Interest savings opportunities: Since interest is front-loaded, extra principal payments early in the loan can cut total interest dramatically and shorten the payoff window.

- Financial planning advantages: Understanding amortization helps you decide when refinancing makes sense, how much equity you’ll have as time goes on, and how payment changes fit your budget, especially as current mortgage rates rise or fall.

Amortization also plays a direct role in house amortization and equity growth. Every principal dollar you pay increases your ownership stake in the property, and that equity can grow faster if your home’s value appreciates over time.

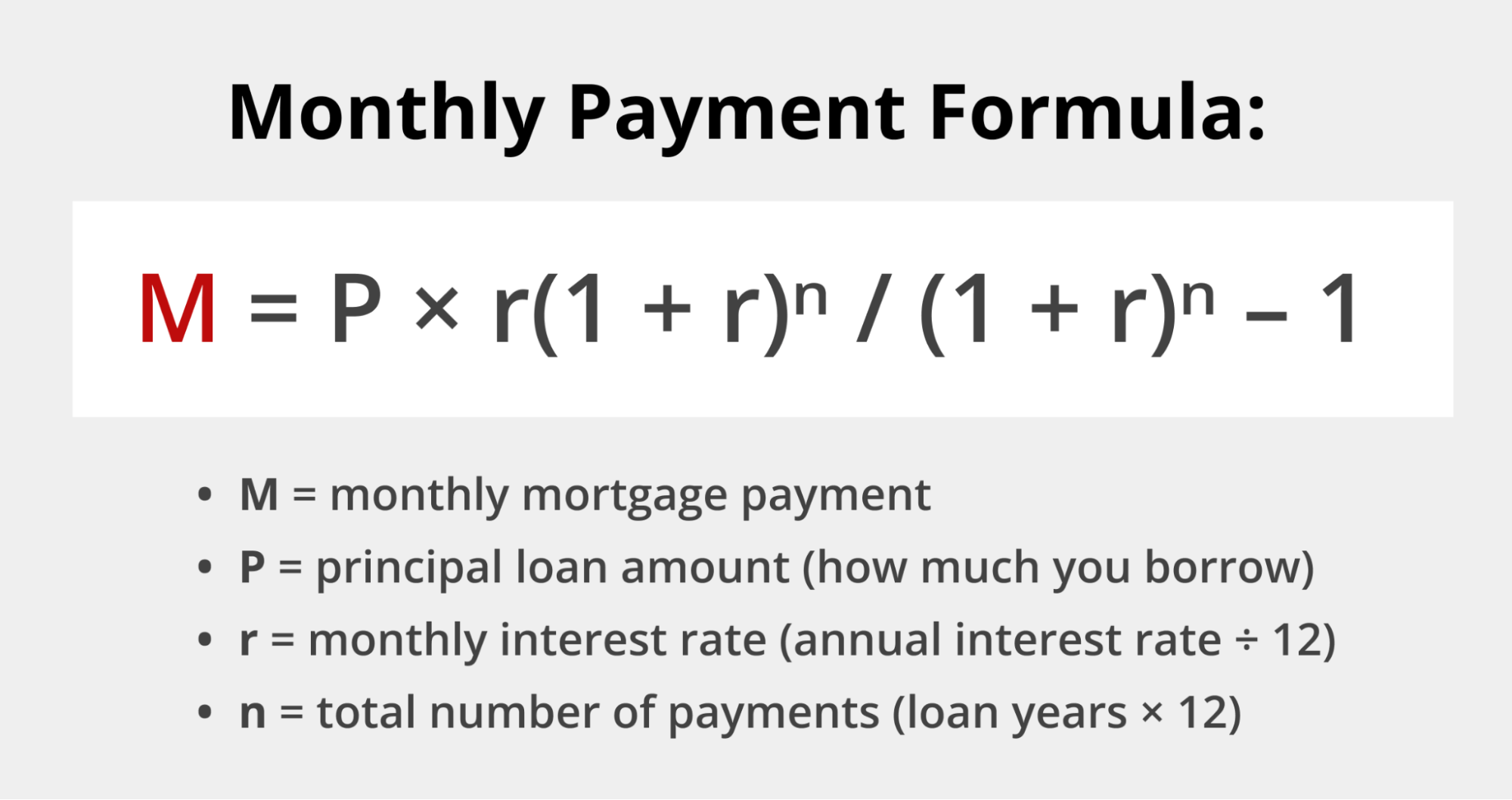

Amortization Formula for Mortgage Loans

Follow these steps to calculate mortgage amortization:

Follow these steps to calculate mortgage amortization:

- Use the monthly payment formula

M = P r(1+r)n(1+r)n-1

- Define the variables

- M = monthly mortgage payment

- P = principal loan amount (how much you borrow)

- r = monthly interest rate (annual interest rate / 12)

- n = total number of payments (loan years × 12)

This formula calculates a level monthly payment that fully pays off both interest and principal by the end of the mortgage term.

Mortgage Amortization Schedule

A mortgage amortization schedule is a breakdown of every payment you’ll make over the life of the loan, showing exactly how much goes toward principal, how much goes toward interest, and how your balance decreases over time. You can read it month-by-month for detailed insight or year-by-year if you prefer a big-picture view of how quickly you’re gaining equity.

Reviewing your amortization schedule helps you understand how long it will take to pay off your mortgage, how much interest you’ll pay at different stages, and how your balance changes as the loan matures. It’s especially useful before refinancing or planning extra payments, since biweekly mortgage payment schedules can accelerate payoff and reduce total interest.

How Extra Payments Affect Mortgage Amortization

When you make extra payments toward the principal, you immediately reduce the balance on which mortgage interest is calculated. This means more of your future payments go toward principal rather than interest, speeding up your payoff timeline.

Even small additional payments can shorten the mortgage term and lower total interest costs dramatically, especially in the early years when interest makes up most of each payment.

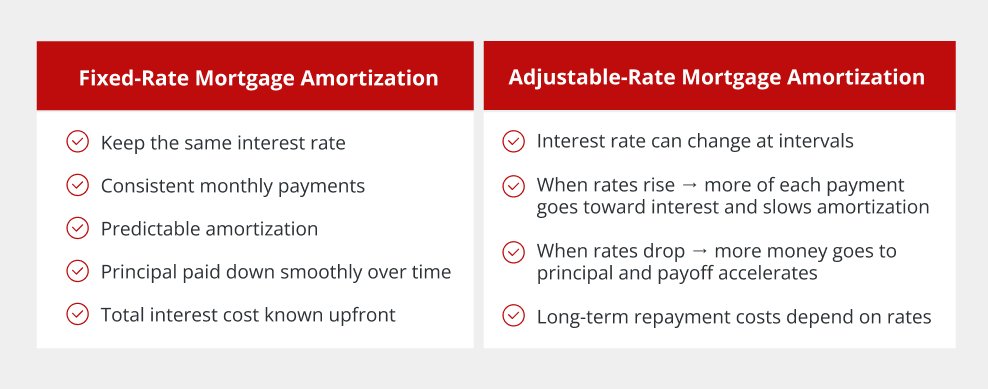

Fixed-Rate vs Adjustable-Rate Amortization

Mortgage amortization differs in a few key ways when it comes to fixed-rate vs adjustable-rate mortgages.

Fixed-Rate Mortgage Amortization:

Fixed-Rate Mortgage Amortization:

- Your interest rate stays the same throughout the entire mortgage term.

- Monthly payments are the same month-to-month, making amortization predictable.

- Principal is paid down steadily, with interest declining as the balance shrinks.

- Extra principal payments always have a clear, predictable impact.

Adjustable-Rate Mortgage (ARM) Amortization:

- The interest rate can change at preset intervals, causing your monthly mortgage payment to rise or fall.

- When rates increase, more of each payment goes toward interest, slowing amortization.

- When rates decrease, more money goes to principal, accelerating payoff and building equity faster.

- Long-term repayment costs depend heavily on how interest rates move over time.

Interest rate fluctuations affect how quickly you pay down your balance. A higher rate increases interest costs and slows principal reduction, while a lower rate speeds it up. This makes understanding your amortization schedule crucial when deciding whether to refinance, change payment strategies, or make extra principal payments.

Tools to Calculate Mortgage Amortization

Online mortgage amortization calculators make it easy to see how your payments are allocated and how quickly your balance will drop over time. These tools help you test different interest rates, loan terms, or extra payment strategies to understand how they affect your payoff timeline.

Griffin Funding offers several helpful free tools, including:

- A mortgage payoff calculator for estimating how extra payments shorten your term

- A home affordability calculator to help determine how much house you can comfortably afford based on income and debt.

- A biweekly mortgage payment calculator that helps illustrate how making biweekly payments can impact mortgage amortization.

While calculators are great for initial planning, borrowers with complex income, investment properties, or future refinancing goals should consider consulting with a mortgage professional to get personalized guidance.

When to Consider Refinancing Based on Amortization

Your amortization schedule can reveal the ideal time to refinance, especially if you’re still early in the loan and most of your payment is going toward interest. Refinancing may make sense if it:

- Lowers your monthly payment

- Reduces your total interest costs

- Shortens your loan payoff date

Homeowners often review their home mortgage amortization progress to compare their current payoff trajectory with what a new loan could offer. If shifting to a lower rate, a shorter term, or a different loan structure aligns better with your financial goals, refinancing could be a strategic move.

Wrapping Up

Understanding mortgage amortization empowers homeowners to plan ahead and identify opportunities to save money or build equity faster. Whether you’re reviewing your amortization schedule or exploring refinancing options, having clarity makes decision-making much easier.

Griffin Funding offers personalized mortgage guidance along with digital tools, supported by features like the Griffin Gold app, to help you track your loan and stay informed throughout the process. Get started online today and work with a mortgage professional to find a mortgage product that aligns with your needs and goals.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

What is negative amortization?

This is a type of repayment structure offered with some loan types, and the upside is that negative amortization provides some short-term flexibility by allowing borrowers to reduce their mortgage payment. The downside is that this initial flexibility results in larger payments down the line due to the increasing principal balance.

Is mortgage amortization different for investment properties?

How long should I amortize my mortgage?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

America’s Self-Employment Boom is Creating a New Class of Real Estate Investors

Self-employed investors are reshaping the real estate market, fueling record-high rental property investment t...

Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

What to Look for in a Bank Statement Loan Lender Choosing the best bank statement loan lender for your situati...

Housing Market Data Tool: Access Local Housing Market Insights

Housing Market Insights Tool Access comprehensive local housing market data for any address or neighborhood in...