USDA Loans vs FHA Loans

USDA Loans vs FHA Loans

KEY TAKEAWAYS

- USDA loans offer 0% down payment options but restrict purchases to rural and suburban areas, while FHA loans require 3.5% down but work anywhere.

- FHA loans accommodate lower credit scores (starting at 500) compared to USDA loans (typically 640+).

- USDA loans have income limits but feature lower mortgage insurance costs than FHA loans.

- Your location, credit score, and down payment savings should drive your USDA vs FHA decision.

Are you wishing to achieve homeownership but are short on cash for a down payment? You’re not alone. The secret weapon many successful homebuyers leverage isn’t family money or years of aggressive saving—it’s government-backed mortgages like USDA and FHA loans. These two programs open doors to homeownership through different paths, each with their own advantages that could save you thousands. Discover the differences between USDA vs FHA loans and unlock your own path to owning a home.

KEY TAKEAWAYS

- USDA loans offer 0% down payment options but restrict purchases to rural and suburban areas, while FHA loans require 3.5% down but work anywhere.

- FHA loans accommodate lower credit scores (starting at 500) compared to USDA loans (typically 640+).

- USDA loans have income limits but feature lower mortgage insurance costs than FHA loans.

- Your location, credit score, and down payment savings should drive your USDA vs FHA decision.

What Is a USDA Loan?

A USDA loan is a mortgage backed by the United States Department of Agriculture designed to boost homeownership in rural and some suburban communities. These loans support low-to-moderate income borrowers who might struggle to qualify for conventional financing.

The standout feature of USDA loans is the 0% down payment requirement, allowing eligible buyers to finance 100% of their home purchase. This makes homeownership accessible to families who lack substantial savings but maintain steady income and decent credit.

USDA loans come with two types of restrictions: geographic and income-based. The property must sit in a USDA-eligible area (typically rural or suburban communities with populations under 35,000). Additionally, household income cannot exceed 115% of the area’s median income.

Instead of traditional mortgage insurance, USDA loans charge a guarantee fee (1% of the loan amount upfront) and an annual fee of 0.35% of the remaining balance.

One of the most appealing aspects of USDA guaranteed loans is that they don’t have predetermined loan limits. Instead, the maximum loan amount is determined by the borrower’s household income and ability to repay the loan.

This differs from USDA direct loans, which do have regional USDA loan limits. As of January 2025, USDA direct loan limits range from $398,600 in standard-cost areas to $970,800 in high-cost regions.

Pros of USDA loans:

- No down payment required

- Lower mortgage insurance costs

- Competitive interest rates

- Ability to finance closing costs

Cons of USDA loans:

- Geographic restrictions limit property options

- Income limits exclude some households

- Stricter credit requirements than FHA loans

- Potentially longer processing times

What Is an FHA Loan?

An FHA loan is a mortgage insured by the Federal Housing Administration, designed to help borrowers who might not qualify for conventional loans. These government-backed mortgages particularly benefit first-time homebuyers and those with limited credit history or lower credit scores.

FHA loans require a minimum 3.5% down payment for borrowers with credit scores of 580 or higher. Those with scores between 500-579 need 10% down.

The flexible credit requirements make FHA loans accessible to many borrowers. While conventional loans often require scores of 620+, FHA loans accept scores as low as 500, though most lenders prefer scores of at least 580 for the lowest down payment option.

FHA loans charge two types of Mortgage Insurance Premiums (MIP): an upfront premium of 1.75% of the loan amount, which can be financed into the loan, and an annual premium between 0.55-1.05% of the loan amount, paid monthly. Unlike with conventional loans, FHA mortgage insurance typically remains for the life of the loan unless you refinance.

FHA loan limits vary by location, ranging from $524,225 in standard-cost counties to $1,209,750 in high-cost areas for single-family homes as of 2025. These limits are recalculated annually to reflect changing housing markets.

The FHA program also offers several loan types to meet diverse needs. For example, FHA purchase loans help buyers acquire their primary residence, FHA cash-out refinance allows homeowners to tap into home equity, and FHA streamline refinance offers simplified refinancing with reduced paperwork for existing FHA borrowers.

Pros of FHA loans:

- Low down payment requirements

- Accommodates lower credit scores

- Available for properties nationwide

- Allows gift funds for down payment and closing costs

Cons of FHA loans:

- Higher mortgage insurance costs than USDA loans

- Mortgage insurance typically lasts the loan’s lifetime

- Property must meet FHA standards

- Loan limits may restrict buying in high-cost areas

Key Differences Between USDA and FHA Loans

As you evaluate USDA vs FHA financing options, understand their fundamental differences to help you make the right choice. Let’s take a look:

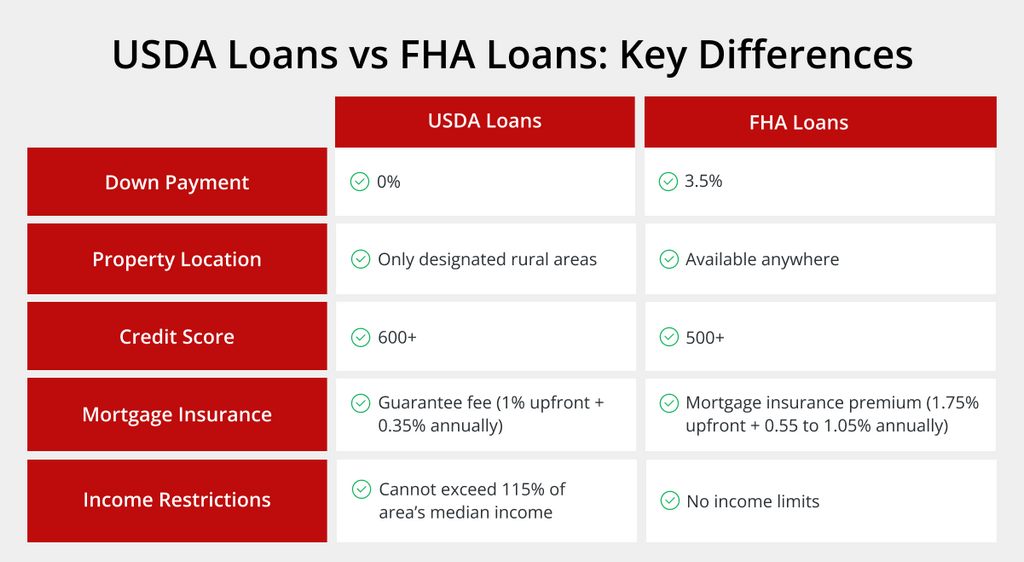

- Down payment requirements: USDA loans provide a 0% down payment while FHA loans have a minimum requirement of 3.5% down.

- Property location restrictions: USDA loans are limited to designated rural and suburban areas and FHA loans are available for properties anywhere in the US.

- Credit score minimums: To apply for a USDA loan, you typically need a credit score of 640+ (though technically there is no minimum in the program). You can achieve an FHA loan with a credit score as low as 500.

- Mortgage insurance: USDA loans require a 1% upfront guarantee fee and 0.35% annual fee and FHA loans require a 1.75% upfront MIP and 0.55-1.05% annual MIP.

- Income restrictions: With a USDA loan your income cannot exceed 115% of area median income. FHA loans have no income limits.

Eligibility Requirements

To qualify for either loan program, you’ll need to meet specific criteria. Here’s what you need to know about eligibility for both USDA and FHA loans:

USDA Loan Eligibility:

- Credit score: While no official minimum exists, most lenders require 640+

- Income limits: Household income cannot exceed 115% of the area median income

- Debt-to-Income (DTI) ratio: Typically 41% maximum, though exceptions exist

- Property location: Must be in a USDA-eligible rural or suburban area

- Occupancy: Must be your primary residence

- US Citizenship: Must be a US citizen, permanent resident, or qualified alien

- Stable income: Must demonstrate reliable income for at least 24 months

FHA Loan Eligibility:

- Credit score: Minimum 500 (requires 10% down), or 580+ (for 3.5% down)

- Income: No maximum limits, but must demonstrate steady employment

- DTI ratio: Typically 43% maximum, though exceptions can reach 50%

- Property: Must meet FHA minimum property standards

- Occupancy: Must be your primary residence

- Mortgage history: No FHA foreclosure in past 3 years

- Bankruptcy: At least 2 years since Chapter 7 discharge or 1 year of Chapter 13 payments

USDA Loan vs FHA Loan: Which Is Better for You?

The USDA vs FHA decision depends on your specific circumstances. Here are scenarios to help you determine which might work better for you:

Consider a USDA loan if:

- You have limited or no money for a down payment

- You want to buy in a rural or qualifying suburban area

- Your household income falls under the local USDA limits

- You have a credit score of 640 or higher

- You want lower mortgage insurance costs

Take a young couple earning a combined amount of $65,000. They each have a decent credit (660), but minimal savings. They found a $200,000 home in a small town 30 minutes from the city. With a USDA loan, they purchased with $0 down and are saving on their monthly mortgage insurance compared to FHA options.

Consider an FHA loan if:

- You have some money saved for a down payment (at least 3.5%)

- You want to buy in an urban area (ineligible for USDA)

- Your income exceeds USDA limits

- Your credit score falls between 500-639

- You need a property with 2-4 units

Let’s look at another example. Say you have a credit score of 605, $10,000 saved, and are looking to purchase a $275,000 duplex in the city where you work. The property’s location ruled out USDA financing, but an FHA loan allowed you to buy with 3.5% down and rent the second unit to help cover your mortgage.

For buyers with good credit who qualify for both loan types, USDA loans typically offer the better financial deal if the property location works. However, FHA loans provide more flexibility in location and property type, plus accommodate lower credit scores.

Ultimately, the FHA vs USDA comparison isn’t about which program is necessarily “better.” They both offer different tradeoffs so it’s more about which loan better suits your unique situation.

Get Expert Help Comparing USDA vs FHA Loans

Choosing between USDA and FHA loans involves weighing multiple factors that impact both your short-term costs and long-term financial health. Working with mortgage professionals who specialize in government-backed loans can help ensure you make the optimal choice.

Griffin Funding specializes in both USDA and FHA loans, offering personalized guidance to help you navigate these complex programs. Our loan specialists can analyze your specific situation to determine which loan type provides the most benefits for your circumstances.

For added convenience, download the Griffin Gold app to explore loan options, check your potential eligibility, and compare estimated costs between USDA and FHA programs—all from your smartphone.

Don’t navigate the USDA loan vs FHA loan decision alone. Contact Griffin Funding today to speak with a government loan specialist who can help you find the most affordable path to homeownership based on your unique needs and qualifications.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...