Tips for Buying a House on a Single Income

Tips for Buying a House on a Single Income

KEY TAKEAWAYS

- Buying a home on a single income is achievable with proper financial planning, budgeting, and credit management.

- Improving your credit score and lowering your debt-to-income (DTI) ratio can significantly increase your chances of loan approval and better mortgage terms.

- Exploring government-backed loans, such as FHA, VA, or USDA programs, can help reduce upfront costs and make homeownership more accessible.

- Staying within the 28/36 rule and choosing a home that aligns with your financial comfort zone helps prevent becoming “house poor” and supports long-term stability.

Buying a home on a single income can feel like a daunting challenge, but it’s absolutely possible with the right preparation and financial strategy. From setting a realistic budget to exploring flexible loan options, there are many ways to make homeownership attainable for solo buyers.

Whether you’re a first-time homebuyer or re-entering the market, these practical tips can help you navigate the process with confidence and make smart, sustainable decisions for your future.

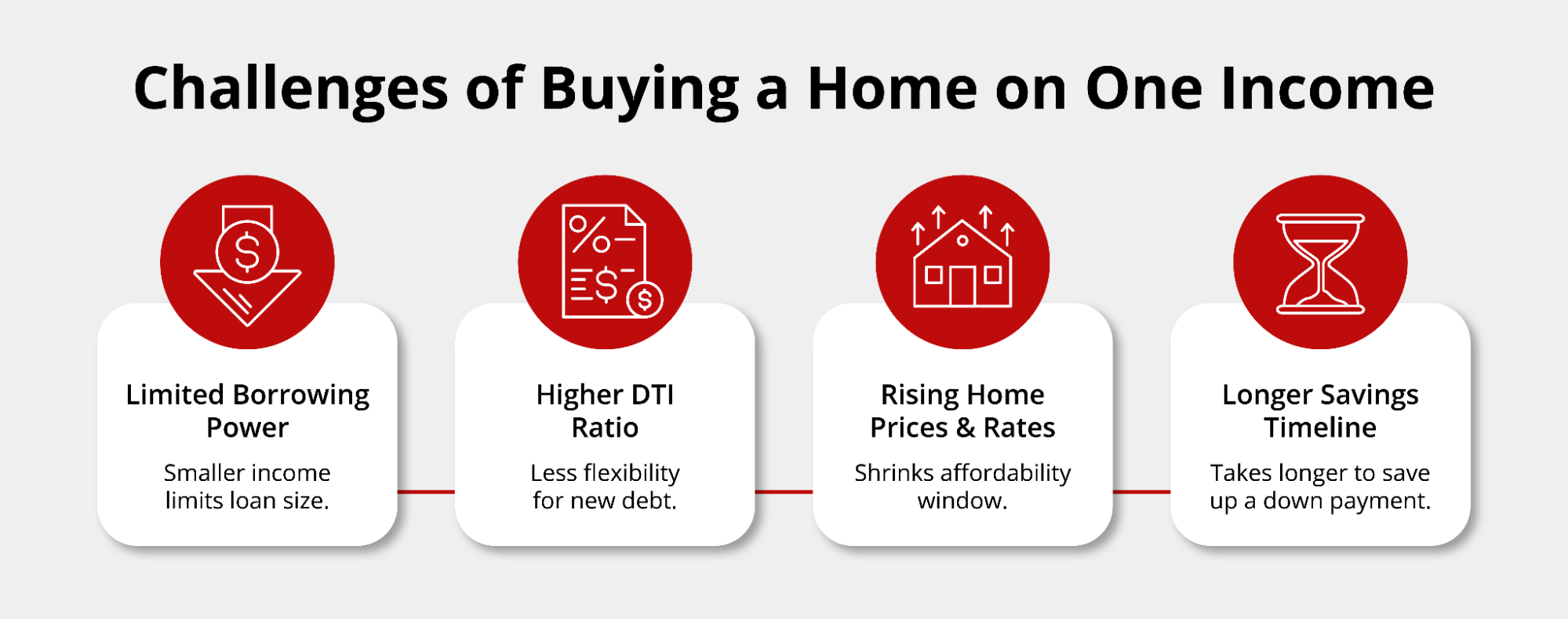

The Challenges of Buying a Home on One Income

Purchasing a home on a single income can present several financial hurdles that make the process more complex. One of the biggest challenges is limited borrowing power. Lenders often qualify buyers based on income and existing debts, so a single-income household may be approved for a smaller loan amount. This can make it harder to compete in markets with rising home prices and limited inventory.

Another major factor is the higher debt-to-income (DTI) ratio that can come with managing all financial obligations alone. Even with a strong credit score, a higher DTI can restrict your loan options or impact your interest rate. Additionally, with today’s elevated mortgage rates, monthly payments can quickly add up, further straining affordability.

Understanding these challenges early on allows you to plan strategically: by strengthening your financial profile, improving credit, and budgeting carefully, you can increase your chances of qualifying for a mortgage that fits your goals and lifestyle.

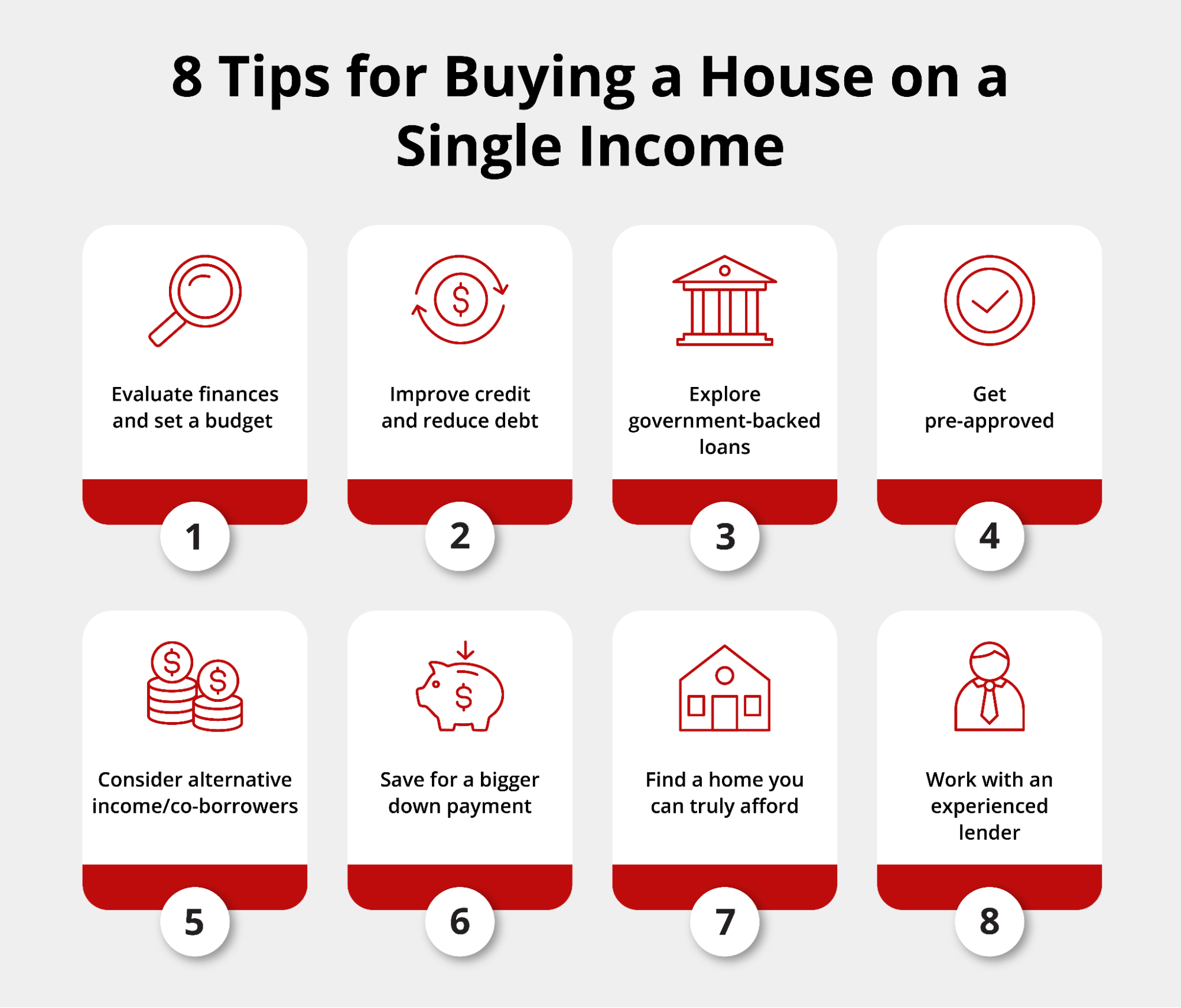

8 Tips for Buying a House on a Single Income

While buying a home on one income comes with unique challenges, careful planning and the right financial strategies can make it completely achievable. The key is to understand your financial position, explore flexible loan options, and make informed decisions every step of the way.

Below are eight practical tips to help you navigate the process and position yourself for success as a single-income homebuyer.

-

1. Evaluate Your Financial Health and Set a Budget

Before you start house hunting, it’s essential to take a clear, honest look at your overall financial picture. Start by assessing your income stability, outstanding debts, and available savings—these will form the foundation for determining what you can comfortably afford.

Lenders will review your financial health closely, focusing on your income consistency, credit score, and debt-to-income (DTI) ratio to decide how much you qualify for and at what mortgage rates. A lower DTI and higher credit score can improve your chances of approval and help you secure more favorable loan terms.

Setting a realistic budget based on these factors ensures you’re not overextending yourself. Tools like Griffin Funding’s prequalification form and home affordability calculator can give you a personalized estimate of your purchasing power, helping you understand how much home you can afford before you even apply for a loan.

-

2. Improve Your Credit and Lower Debt

Your credit score plays a major role in determining your loan approval, the types of mortgage programs you qualify for, and the interest rates you’ll receive. A higher score signals to lenders that you’re a reliable borrower, which can lead to better loan terms and lower monthly payments.

To strengthen your credit, start by paying down revolving debt like credit cards to reduce your credit utilization ratio. Review your credit report for errors and dispute any inaccuracies that could be dragging your score down. It’s also wise to avoid opening new credit accounts or taking on additional loans in the months leading up to your mortgage application.

At the same time, focus on lowering your debt-to-income (DTI) ratio: a key factor lenders use to assess your ability to manage new debt. Paying off existing obligations or increasing your income can help bring your DTI within an acceptable range, improving your overall mortgage eligibility and helping you secure more favorable loan terms.

-

3. Explore Government-Backed Loan Programs

Government-backed loans can make homeownership more accessible for single-income buyers by offering flexible requirements and lower upfront costs. Here are some key options to consider:

- FHA Loans: Designed for buyers with moderate incomes, FHA loans allow for lower down payments (as little as 3.5%) and more flexible credit requirements, making them a great option if you’re still building your financial profile.

- VA Loans: Available to eligible veterans, active-duty service members, and certain surviving spouses, VA loans offer significant benefits such as zero down payment, no private mortgage insurance (PMI), and competitive interest rates.

- USDA Loans: Ideal for rural and some suburban homebuyers, USDA loans provide 100% financing with no down payment required, as long as you meet income and location eligibility guidelines.

In addition to these programs, many states and local agencies offer first-time home buyer programs and grants that can help cover down payment or closing costs. These initiatives are particularly valuable for individuals or families purchasing their first home, including those seeking single parent home loans designed to make homeownership more attainable on a single income.

-

4. Get Pre-Approved to Bolster Your Buying Power

Getting pre-approved for a mortgage is one of the smartest steps you can take before starting your home search. A pre-approval shows sellers that you’re a serious and qualified buyer, giving you credibility in competitive markets. It also helps you set realistic expectations about your price range and monthly payments, ensuring you stay within your financial comfort zone.

To get pre-approved, lenders will need documentation to verify your financial health, including:

- Recent pay stubs: to confirm your income and employment.

- Tax returns and W-2s: typically for the past two years.

- Bank statements: showing assets and savings for down payment and reserves.

- Credit report: to evaluate your credit score and payment history.

- Identification documents: such as a driver’s license or Social Security card.

Being prepared with these documents can speed up the pre-approval process and give you a competitive edge once you begin making offers.

-

5. Consider Alternative Income or Co-Borrowers

If you’re trying to buy a house with low income, consider exploring ways to supplement your earnings to strengthen your mortgage application. Additional income streams, such as side hustles, freelance work, or rental income from an accessory dwelling or roommate, can increase your qualifying income and make homeownership more attainable.

Another option is adding a co-borrower, such as a family member or partner, to your loan application. Combining incomes can help you qualify for a larger loan or better terms, as lenders evaluate the total household income and debt profile. However, co-borrowing comes with shared legal and financial responsibility: both parties are equally accountable for the mortgage payments and credit impact.

Carefully consider these options to determine what best fits your long-term financial goals and comfort level before committing.

-

6. Save for a Bigger Down Payment

Saving for a down payment is one of the most impactful steps you can take as a single-income homebuyer. A larger down payment not only reduces the amount you need to borrow but can also help you qualify for better loan terms and a lower interest rate—saving you thousands over the life of your mortgage.

If you’re struggling to save, look into down payment assistance programs, employer housing benefits, or even financial gifts from family members. These options can help you reach your goal faster. While some loan programs offer no money down options, contributing even a modest amount upfront can make your offer more competitive and reduce long-term costs.

-

7. Find a Home You Can Comfortably Afford

It’s important to find a home that fits comfortably within your financial means. A good rule of thumb is the 28/36 rule, which suggests spending no more than 28% of your gross monthly income on housing costs and no more than 36% on total debt payments.

By keeping your income spent on a mortgage within these limits, you’ll reduce financial stress and avoid becoming “house poor”—a situation where too much of your income goes toward your home, leaving little for savings or other expenses. Consider exploring affordable or emerging neighborhoods that offer strong value and growth potential without stretching your budget too thin.

-

8. Work With an Experienced Mortgage Lender

Partnering with the right lender can make all the difference when buying a home on a single income. An experienced mortgage professional provides personalized guidance, helping you understand your options and navigate the complexities of the lending process with confidence.

At Griffin Funding, we specialize in helping single-income buyers achieve their homeownership goals through flexible loan programs, competitive rates, and tailored support. Our team can guide you from prequalification to closing, making sure you find the right financing solution that aligns with your income, budget, and long-term financial plans.

Find an Affordable Pathway to Homeownership

Buying a home on a single income is absolutely possible—with the right strategy, smart budgeting, and the right lending partner. At Griffin Funding, we’re committed to helping single-income buyers find flexible, affordable financing solutions tailored to their unique financial situations. From low down payment options to personalized loan guidance, our team is here to support you every step of the way.

You can also simplify your homebuying journey with the Griffin Gold app, which allows you to track your loan application, upload documents securely, and manage your progress all in one place. Whether you’re planning your first purchase or looking to upgrade, Griffin Funding can help you make homeownership a reality.

Get started online today!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can I buy a house with only one income?

What salary does a single person need to buy a house?

What’s the best loan for a single-income home buyer?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

What Is a Homestead Exemption?

Most homeowners pay more property taxes than they have to simply because they never filed a homestead exemptio...

Top Secondary Cities for Real Estate Investors 2026

Major metros like New York, Los Angeles, and San Francisco still dominate the headlines, but savvy real estate...

Grantor vs Grantee in Real Estate: What’s the Difference?

If you’ve ever reviewed a property deed or mortgage document, you’ve probably come across the term...