Does a HELOC Require an Appraisal?

Does a HELOC Require an Appraisal?

KEY TAKEAWAYS

- Most lenders require some form of appraisal for a HELOC to determine your home’s current market value and calculate your available equity.

- The type of valuation (full appraisal, desktop, drive-by, or AVM) depends on your loan amount, CLTV ratio, and overall borrower profile.

- Appraisal results directly impact your borrowing power, as lenders use your home’s value to set HELOC loan limits.

- In certain lower-risk scenarios, lenders may waive a full appraisal or reduce fees, but some form of property valuation is typically required.

Tapping into your home’s value can be a smart way to fund renovations, consolidate debt, or cover major expenses. But before you move forward, it’s important to understand how lenders evaluate your property. If you’re exploring home equity solutions, one of the most common questions is whether an appraisal is required.

Does a HELOC Loan Require an Appraisal?

Yes. In most cases, a lender will require an appraisal for a home equity line of credit to determine your home’s current market value. Because your property serves as collateral, lenders need an accurate valuation before approving your credit limit. The appraisal helps confirm how much equity you’ve built and ensures the loan amount aligns with current market conditions.

While some lenders may offer alternatives, such as automated valuation models (AVMs) or desktop appraisals, a full or hybrid appraisal is still the standard for most borrowers.

Why Lenders Require a HELOC Appraisal

Lenders require an appraisal to verify your home’s market value and accurately calculate how much equity is available to borrow against. This protects both the borrower and the lender when issuing a HELOC or home equity loan. Here’s how each factor matters:

- Loan-to-value (LTV) ratio. Your LTV compares your existing mortgage balance to your home’s appraised value. Lenders use this percentage to determine how much you can borrow and whether you meet their eligibility guidelines.

- Combined loan-to-value (CLTV). CLTV factors in your primary mortgage plus the new HELOC amount. This calculation ensures your total debt against the property stays within acceptable risk limits.

- Risk mitigation. An appraisal helps lenders avoid over-lending if property values decline. It reduces financial risk by confirming the home is worth the amount being borrowed against.

- Market fluctuations. Real estate values can shift based on local market trends. A current appraisal reflects today’s conditions rather than relying on outdated purchase prices.

- Borrower equity protection. Accurate valuation can prevent homeowners from overextending themselves. By confirming available equity, lenders help ensure you’re borrowing within sustainable limits.

Types of HELOC Appraisals

Not all home appraisals for home equity loans look the same. The type required often depends on your loan amount, equity position, and lender guidelines – and it can impact the cost of a HELOC appraisal in 2026.

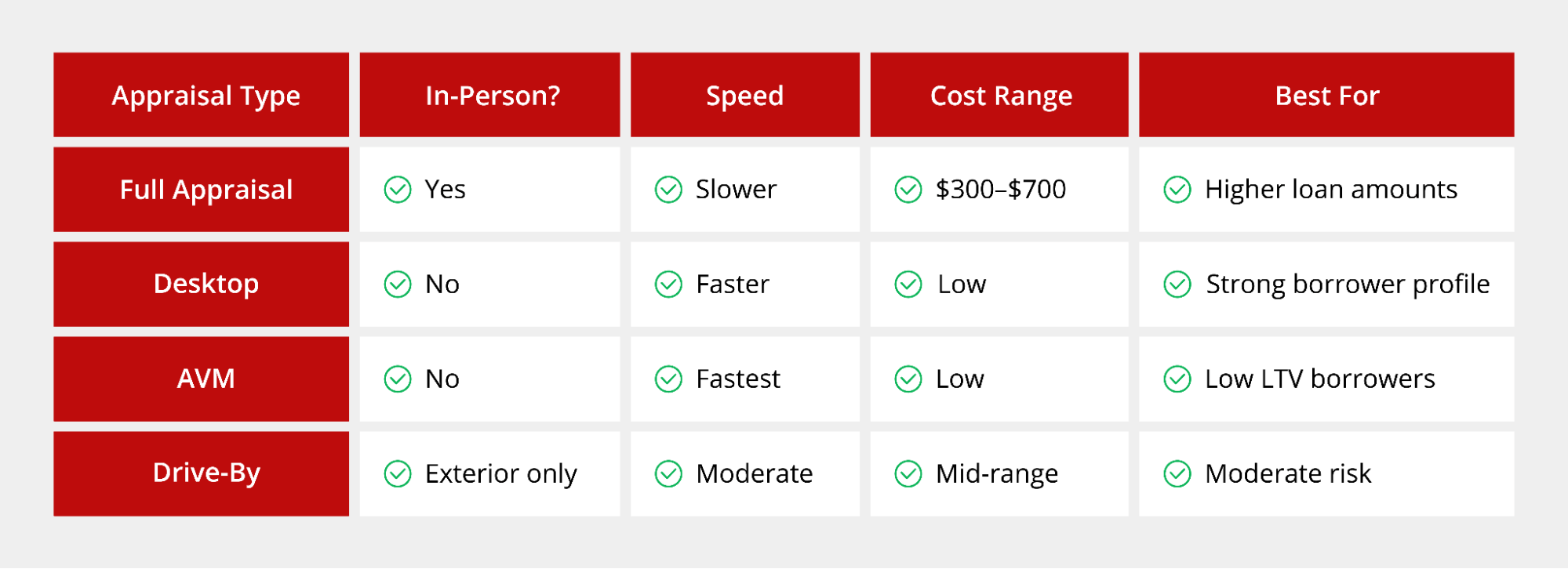

Full In-Person Appraisal

Full In-Person Appraisal

A full in-person appraisal is the most traditional and comprehensive option. A licensed appraiser visits your home, evaluates its condition, measures square footage, and compares it to similar properties in your area. This type is often required for higher loan amounts or when the lender needs a more detailed valuation. The typical cost ranges from $300 to $700, depending on your location and property size.

Desktop Appraisal

A desktop appraisal is completed remotely without an in-person visit. Instead, the appraiser reviews public records, MLS data, tax assessments, and recent comparable sales to estimate your home’s value. This option is generally faster and may cost less than a full appraisal, but it’s typically used when the risk profile is lower.

Automated Valuation Model (AVM)

An Automated Valuation Model, also known as AVM, uses algorithm-based technology to estimate your home’s value based on large data sets, recent sales, and market trends.

AVMs offer faster approvals and are often sufficient for borrowers with lower LTV ratios. However, because they rely entirely on data rather than physical inspection, lenders may limit their use to lower-risk scenarios.

Drive-By Appraisal

A drive-by appraisal involves an exterior-only review of the property. The appraiser assesses curb appeal, neighborhood conditions, and visible features, then combines that information with market data.

When comparing a drive-by appraisal vs. a full appraisal for HELOC approval, the key difference is the level of detail. Drive-by appraisals are less comprehensive and typically used when a lender needs added reassurance beyond an AVM but not a full interior inspection.

When a HELOC Might Not Require a Full Appraisal

In some situations, a full in-person appraisal may not be necessary. Lenders evaluate overall risk, and borrowers with a low combined loan-to-value (CLTV) ratio – meaning they have significant equity – are often considered lower risk. A strong borrower profile, including high credit scores, stable income, and low debt-to-income ratios, can also make lenders more comfortable using a desktop appraisal or automated valuation model instead of sending an appraiser to the home.

A recent appraisal already on file (such as from a recent purchase or refinance) may also reduce the need for a new full valuation, especially if market conditions haven’t shifted dramatically. Smaller credit lines typically present less exposure for lenders, which can increase the likelihood of a streamlined approval. In competitive or fast-moving real estate markets, lenders may rely on updated sales data and automated tools to reflect current pricing trends more efficiently.

Certain products, including a fixed-rate HELOC, may qualify for alternative valuation methods depending on HELOC loan limits and the lender’s internal guidelines. Ultimately, each lender sets its own criteria, but homeowners with substantial equity and strong financials often have more flexibility when it comes to appraisal requirements.

How Much Does a HELOC Appraisal Cost?

Nationally, the average cost of a HELOC appraisal typically ranges from $300 to $700, depending on your location, property size, and the type of appraisal required. In most cases, the borrower pays this fee, either upfront or as part of closing costs. Some lenders allow appraisal fees to be rolled into closing, meaning you won’t pay out of pocket at the time of the valuation, though this can slightly increase your overall loan balance.

If you’re wondering how to get a HELOC without an appraisal fee, some lenders may waive the cost during promotional periods, for lower-risk borrowers, or when using automated valuation methods. Fee waivers are more common when CLTV ratios are low or when borrowers have strong credit profiles.

How a HELOC Appraisal Impacts Your Borrowing Power

Your appraisal directly impacts how much you can borrow because it determines your home’s current market value. Lenders use this value to calculate your combined loan-to-value (CLTV) ratio using the following formula:

(Current mortgage balance + Requested HELOC amount) ÷ Appraised home value

For example, if your home appraises at $500,000 and you owe $300,000 on your mortgage, a lender allowing an 85% CLTV may cap your total borrowing at $425,000. This means you could potentially access $125,000 through a HELOC.

If the appraisal comes in lower than expected, your available credit line may shrink, or you may need to adjust your requested amount. This is especially important if you’re planning to use funds for large expenses, such as renovations or debt consolidation, where borrowing power directly impacts your financial strategy.

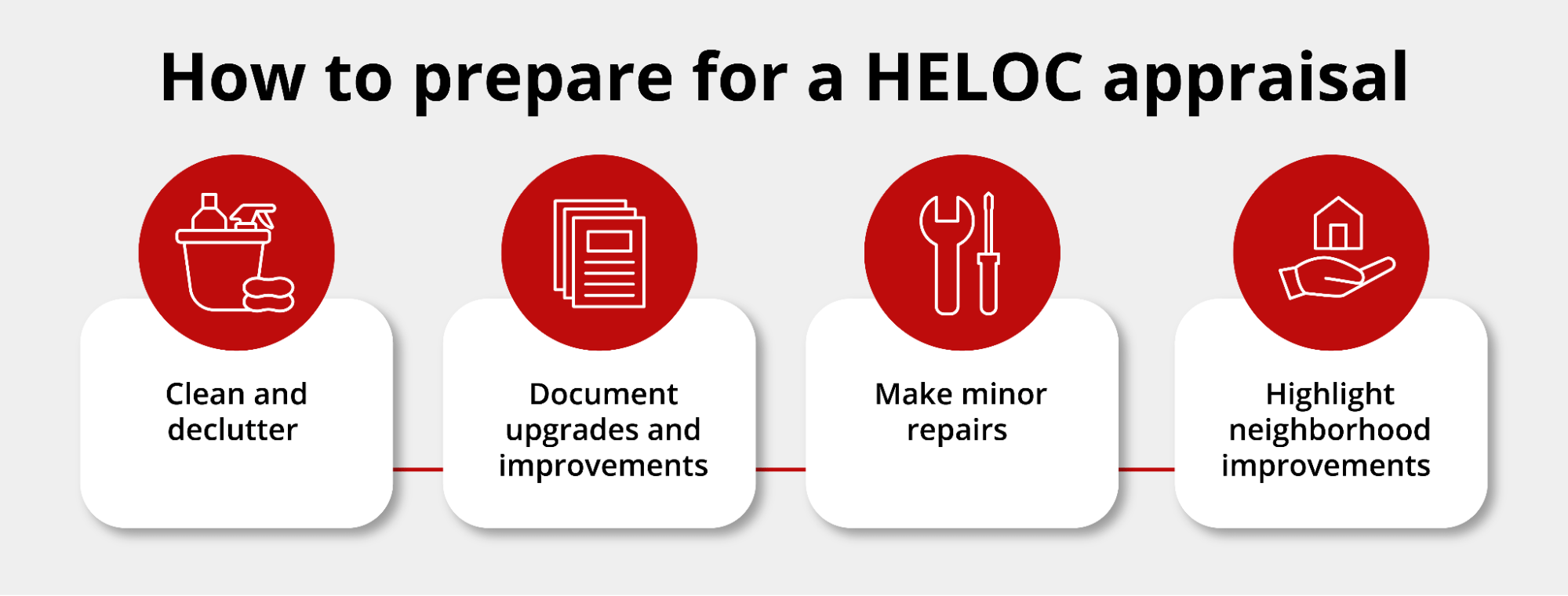

How to Prepare for a HELOC Appraisal

Preparing ahead of time can help ensure your home is valued accurately and meets common HELOC requirements. Here are some ways to prepare for your HELOC appraisal:

- Clean and declutter to present your home in its best condition.

- Document any recent upgrades, such as kitchen remodels, roof replacements, or energy-efficient improvements.

- Make minor repairs, including leaky faucets, chipped paint, or cracked fixtures, and gather any permits for completed renovations.

- Highlight neighborhood improvements, such as new schools, parks, or infrastructure, that may positively impact value.

Using a checklist for home equity loan appraisal preparation can help you stay organized and confident before the appraiser arrives.

Final Thoughts

A HELOC appraisal plays a key role in determining your borrowing power and ensuring you access your home equity responsibly. While most lenders require some form of valuation, the type of appraisal—and the cost—can vary based on your financial profile and property details. Understanding what to expect helps you plan ahead and avoid surprises during the process.

A HELOC appraisal plays a key role in determining your borrowing power and ensuring you access your home equity responsibly. While most lenders require some form of valuation, the type of appraisal—and the cost—can vary based on your financial profile and property details. Understanding what to expect helps you plan ahead and avoid surprises during the process.

At Griffin Funding, we’re committed to helping you explore flexible home equity options with transparent guidance every step of the way. You can also use the Griffin Gold app to track your loan progress, manage documents, and stay informed throughout your home equity journey.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Does a HELOC loan require an appraisal every time?

What happens if the HELOC appraisal comes in lower than expected?

Can I get a HELOC with no appraisal?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

America’s Self-Employment Boom is Creating a New Class of Real Estate Investors

Self-employed investors are reshaping the real estate market, fueling record-high rental property investment t...

Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

What to Look for in a Bank Statement Loan Lender Choosing the best bank statement loan lender for your situati...

Housing Market Data Tool: Access Local Housing Market Insights

Housing Market Insights Tool Access comprehensive local housing market data for any address or neighborhood in...