LLC for Rental Property Purchase: Pros & Cons

KEY TAKEAWAYS

- An LLC separates your personal assets from your rental property business, offering liability protection if tenants sue or creditors come after the property.

- Financing a rental property through an LLC can be more expensive and complicated than personal ownership.

- Creating an LLC for rental property involves state filing fees, ongoing costs, and stricter lending terms, but it can simplify partnerships and tax planning.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformIf you’re buying a rental property, you’ve probably heard that forming an LLC could protect your personal assets. But is setting up an LLC for rental property actually worth it? The answer depends on your situation, financing options, and long-term investment goals.

An LLC protects your personal assets and streamlines your business operations, but it also comes with extra costs and potential financing challenges. Keep reading to learn how LLCs work for rental properties, the real advantages and drawbacks, and how to decide if this structure fits your investment strategy.

What Is an LLC for Rental Property?

A limited liability company (LLC) is a type of business structure that gives your rental property business its own legal identity, separate from your personal finances. When you own real estate through an LLC, the company — not you personally — holds the title to the property.

In real estate ownership, an LLC acts as a protective barrier. If someone sues your rental property or if the business takes on debt, your personal bank accounts, home, and other assets typically stay protected.

The main difference between personal ownership and LLC ownership is the legal separation. When you own a rental property in your own name, a lawsuit against the property can reach your personal assets. With an LLC, the company is its own legal entity, offering protection that personal ownership doesn’t provide.

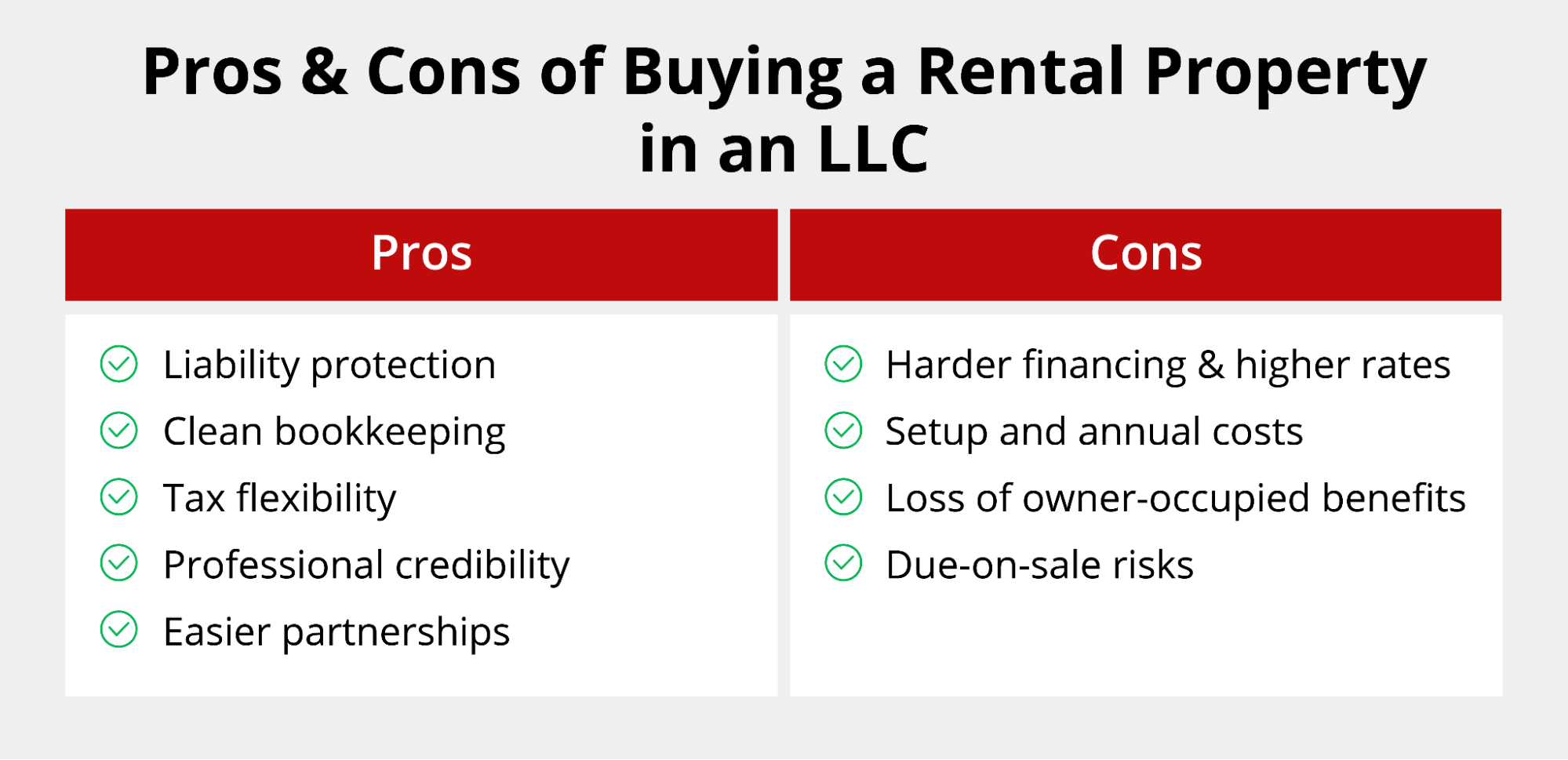

Pros of Buying a Rental Property in an LLC

Setting up an LLC for rental property offers several advantages. Here’s why many real estate investors choose this structure:

Limited Personal Liability Protection

Limited Personal Liability Protection

The biggest draw of a rental property LLC is protection for your personal assets. If a tenant or one of their guests is injured on your property and sues, or if a contractor files a claim, the lawsuit targets the LLC instead of you personally. This protection keeps your personal savings, home, and other investments safe from business-related claims.

Separation of Personal and Business Finances

An LLC creates a clear dividing line between your personal money and your rental income and expenses. You’ll maintain separate bank accounts and financial records for the business. This separation leads to cleaner bookkeeping throughout the year, and when tax season arrives, all your business activity is already organized in one place, which simplifies accounting and expense tracking.

Potential Tax Flexibility

Most LLCs use pass-through taxation, so rental earnings go straight to your individual tax filing rather than being taxed at the company level. This structure allows you to claim deductions for property expenses, mortgage interest, and depreciation.

Depending on your situation, you might choose for your LLC to be taxed as an S- or C-corporation, Partnership, or disregarded entity, which can offer different tax benefits in specific scenarios.

Professional Credibility

Operating under an LLC name rather than your personal name can boost your credibility with tenants, vendors, and potential business partners. It signals that you run a legitimate business operation rather than a casual side venture.

Easier Ownership Transfers and Partnerships

An LLC structure simplifies bringing in partners or investors down the line. You can add members to the LLC, sell partial ownership interest, or transfer shares without changing the property title.

For estate planning, you can transfer membership interests to heirs more smoothly than transferring real estate titles.

Cons of Creating an LLC for Rental Property

While LLCs offer protection and flexibility, they’re not always the best choice for every investor. Here are the downsides of creating an LLC for rental property:

Financing Can Be More Difficult

Getting a mortgage for a property owned by an LLC is tougher than financing in your personal name. Many traditional lenders don’t offer LLC loans at all, and those that do typically charge higher interest rates.

You’ll usually need a larger down payment — sometimes 25% to 30% instead of the 15% to 20% you might get with personal financing. Even with LLC financing, expect to sign a personal guarantee, putting you on the line for loan repayment if the business defaults.

Loss of Certain Tax Benefits

If you’re considering living in the property, you’ll lose access to owner-occupied financing options when the property is in an LLC. Owner-occupied mortgage loans typically offer lower interest rates and better terms than investment property loans.

You also can’t claim the capital gains exclusion that homeowners get when selling their primary residence. This exclusion allows homeowners to avoid paying taxes on up to $250,000 in profit (or $500,000 for married couples) from the sale if they’ve lived in the home for at least two of the past five years — a benefit that doesn’t apply to LLC-owned properties.

Setup and Ongoing Costs

Forming an LLC for rental property costs money upfront and every year after. You’ll pay state filing fees for Articles of Organization, and these vary depending on where you file. Annual report fees to maintain your LLC status also differ by state. Many states require LLCs to use a registered agent service, which adds to your yearly expenses.

Due-On-Sale Clause Risks

Most mortgages include a due-on-sale clause that lets the lender demand full loan repayment if you transfer the property to another owner, including an LLC. If you already own a rental property in your personal name and want to transfer it into an LLC, you risk triggering this clause.

This risk is why many investors choose to form the LLC first and purchase property through it rather than transferring ownership later.

How to Form an LLC for a Rental Property

Setting up an LLC for rental properties involves several administrative steps. Here’s what the process looks like:

Choose a State for Your LLC

You’ll need to decide whether to form your LLC in your home state or in another state. Most rental property investors form their LLC in the state where the property is located because that’s typically the most straightforward and cost-effective option.

Keep in mind that you’ll need to obtain foreign authority with the Secretary of State if the property you are purchasing is outside of the state that the LLC was formed in.

File Articles of Organization

Articles of Organization are the legal documents that officially create your LLC. You’ll file these with your state’s Secretary of State office, either online or by mail. The Articles typically require basic information, such as your LLC’s name, address, registered agent, and the names of members or managers.

Create an Operating Agreement

An Operating Agreement outlines how your LLC will operate, including ownership percentages, profit distribution, and decision-making procedures. Even if you’re the sole member, this document clarifies how the business runs and strengthens the legal separation between you and the LLC.

Obtain an EIN and Open a Business Bank Account

To open a bank account under your LLC, you need an employer identification number (EIN), which you get from the IRS. This free number works like a Social Security number for your business and is required for opening business bank accounts and filing taxes. Opening a business bank account is necessary for maintaining the financial separation that makes your LLC effective.

Transfer or Purchase Property in the LLC

You can either purchase a new property directly in your LLC’s name or transfer an existing property into the LLC. Buying directly is cleaner and avoids the due-on-sale clause issues mentioned earlier.

How Does Financing Work for a Rental Property LLC?

Financing a rental property LLC works differently from traditional mortgages. Standard conforming loans typically aren’t available for LLC-owned properties, so you’ll need to explore specialized lending options.

DSCR loans are one of the most popular choices for LLC investors. These debt-service coverage ratio loans focus on the property’s rental income instead of your personal income or DTI ratio. Other options include portfolio loans from smaller banks and credit unions, or non-qualified mortgages designed specifically for real estate investors. These investor mortgages account for the unique needs of rental property owners and LLC structures.

Keep in mind that most lenders will still ask for a personal guarantee, which means you’re personally responsible for the loan even though the LLC owns the property. This limits some of the liability protection benefits, though your LLC still protects you from non-loan-related claims like tenant lawsuits.

Griffin Funding specializes in helping real estate investors finance properties through LLCs. As a leading DSCR mortgage lender, we understand the challenges LLC owners face and offer flexible terms based on property performance rather than just personal credit scores.

See If an LLC Is Right for Your Real Estate Investment Strategy

Whether you should buy a rental property in an LLC depends on your specific situation. If you’re acquiring multiple properties, forming partnerships, or want strong liability protection, an LLC often pays for itself. For investors buying their first property or those with limited capital, the added costs and financing challenges might outweigh the benefits of real estate investing through an LLC structure.

Griffin Funding offers financing solutions for real estate investors, whether you’re purchasing property in your own name or through an LLC. We work with both structures and can help you find the right loan product for your situation, whether you’re just learning how to create an LLC for real estate investing or expanding an existing portfolio.

Track your investment progress with the Griffin Gold app to stay organized and monitor your real estate goals.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Should I buy a rental property in an LLC or transfer it later?

What type of LLC do I need for a rental property?

Can I live in a rental property owned by my LLC?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...