How the OBBB Tax Bill Impacts Real Estate

KEY TAKEAWAYS

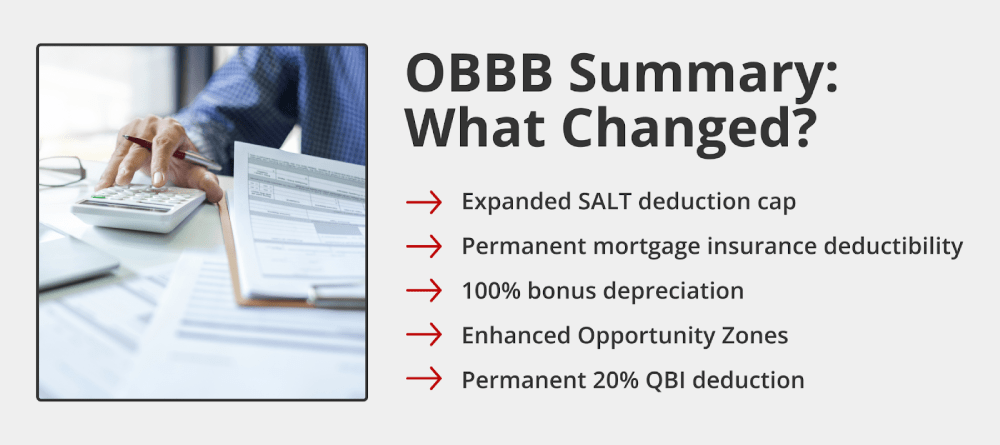

- Trump’s One Big Beautiful Bill Act will temporarily increase the state and local tax (SALT) deduction cap from $10,000 to $40,000 for households earning under $500,000, significantly benefiting homeowners in high-tax states.

- Real estate investors can take advantage of 100% bonus depreciation for qualifying property improvements and equipment, providing immediate tax benefits.

- Homeowners with FHA, VA, and conventional loans can now permanently deduct mortgage insurance premiums, reducing the effective cost of low-down-payment loans.

- The 20% qualified business income (QBI) deduction will become permanent, along with preserved 1031 exchanges and enhanced Opportunity Zone benefits.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformThe One Big Beautiful Bill Act (OBBB) is one of the most significant pieces of tax legislation in recent years. Enacted by President Trump in July 2025, this comprehensive bill makes permanent many tax provisions while introducing new incentives that directly benefit the real estate sector.

Understanding how these many tax changes affect your real estate investments, homeownership costs, and market opportunities is crucial for making the right decisions when buying, selling, or investing. Keep reading to learn more about how the OBBB will impact you.

KEY TAKEAWAYS

- Trump’s One Big Beautiful Bill Act will temporarily increase the state and local tax (SALT) deduction cap from $10,000 to $40,000 for households earning under $500,000, significantly benefiting homeowners in high-tax states.

- Real estate investors can take advantage of 100% bonus depreciation for qualifying property improvements and equipment, providing immediate tax benefits.

- Homeowners with FHA, VA, and conventional loans can now permanently deduct mortgage insurance premiums, reducing the effective cost of low-down-payment loans.

- The 20% qualified business income (QBI) deduction will become permanent, along with preserved 1031 exchanges and enhanced Opportunity Zone benefits.

What Is the One Big Beautiful Bill Act?

The One Big Beautiful Bill Act is a comprehensive tax overhaul designed to extend and enhance provisions from the 2017 Tax Cuts and Jobs Act while introducing new economic incentives. First, here’s a quick One Big Beautiful Bill Act summary: The legislation emerged from President Trump’s desire for “one big, beautiful bill” to address multiple policy priorities simultaneously, using the budget reconciliation process to bypass traditional Senate filibuster rules.

The One Big Beautiful Bill Act has a dual focus on individual tax relief and business growth incentives. The bill makes permanent many individual tax cuts that were set to expire at the end of 2025, while introducing new deductions for tips and overtime income. For real estate specifically, the legislation recognizes housing as a cornerstone of wealth building and economic stability.

The OBBB is fundamentally designed to stimulate economic growth through targeted tax incentives, with real estate playing a central role. By reducing tax burdens on property ownership, investment, and development, the bill aims to increase housing supply, improve affordability, and strengthen the overall housing market.

Key Tax Provisions That Impact Real Estate

The OBBB real estate changes introduce several important tax provisions for real estate investors and homeowners:

- Mortgage interest deduction cap: The bill makes permanent the mortgage interest deduction cap at $750,000 of acquisition debt, providing certainty for homeowners and buyers.

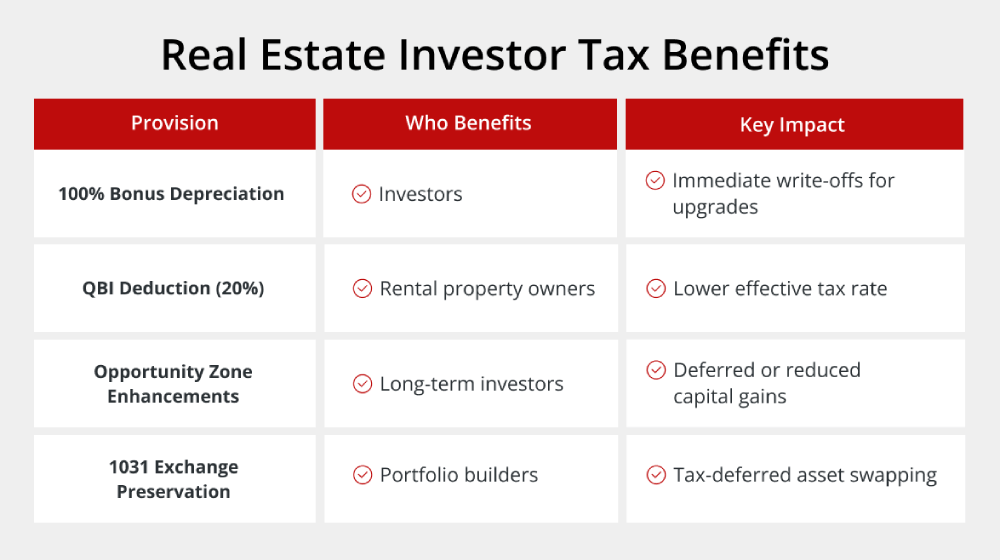

- 100% bonus depreciation: The return of full bonus depreciation allows investors to immediately deduct the entire cost of qualifying property improvements and equipment in the year of purchase.

- Section 1031 like-kind exchanges: These exchanges remain unchanged, so investors can defer capital gains taxes when selling real estate and reinvest the money earned in similar assets. With this capital gains tax calculator, you can determine the potential tax savings and plan more effective exchange strategies to maximize your investment returns.

- 20% qualified business income deduction: The legislation maintains this deduction for rental real estate activities permanently, applying to net rental income and effectively reducing the tax burden on real estate investment income while improving investment yields.

How the OBBB Could Shift the Housing Market

The OBBB housing market effects are expected to be substantial, particularly in high-tax states where the expanded SALT deduction creates new incentives for homeownership. The legislation raises the state and local tax deduction cap from $10,000 to $40,000 per household from 2025 to 2029, making homeownership more attractive for upper-middle-income borrowers in states like New York, New Jersey, and California.

This change could drive increased demand in high-cost areas, potentially pushing home values higher as more buyers seek to maximize their tax benefits. The expanded deduction makes previously expensive markets more affordable on an after-tax basis, which could intensify competition for property in these regions.

The bill’s impact on housing supply is equally important. The law increases funding for affordable housing development programs and makes it easier for developers to qualify for tax credits when building low-income housing. This change should stimulate affordable housing development, helping address supply shortages that have contributed to rising home prices.

Regional variations will be significant, with high-tax states seeing the most dramatic benefits from SALT deductions. Meanwhile, areas with lower property taxes may see less direct impact from these provisions, though they’ll still benefit from enhanced mortgage insurance deductibility and other homeowner incentives.

Impact on Real Estate Investors

Real estate investors will benefit from the OBBB’s investor-friendly provisions. The permanent extension of the 20% qualified business income deduction under Section 199A provides ongoing tax benefits for rental property income, effectively reducing the tax rate on investment returns.

The preservation of business interest deductions for real property trades ensures that investors using leverage can continue to deduct mortgage interest on investment properties. This is valuable for commercial real estate investors and those using debt service coverage ratio (DSCR) loans to finance their portfolios.

Opportunity Zone incentives receive strengthened support under the OBBB, renewing targeted benefits for investments in designated economically distressed areas. These enhanced incentives could drive increased capital flows into underserved communities while providing attractive tax benefits for patient investors.

The legislation also maintains flexibility for sophisticated investment strategies. With 1031 exchanges preserved and adjusted basis calculations unchanged, investors can continue to defer taxes while building real estate portfolios through acquisitions and dispositions.

Home Buyers and Homeowners: What to Expect

Current homeowners and prospective buyers will see several immediate benefits from the OBBB. The permanent deductibility of mortgage insurance premiums (PMI, FHA MIP, VA funding fees, and USDA guarantee fees) reduces the effective cost of low-down-payment loans.

This change benefits first-time buyers who often rely on FHA loans or conventional loans with less than 20% down payments. The ability to deduct these premiums permanently makes homeownership more affordable and predictable for budget-conscious buyers.

The expanded SALT deduction creates opportunities for homeowners in high-tax areas to reduce their overall tax burden significantly. However, the benefit phases out for higher-income earners, with households earning over $500,000 seeing reduced benefits.

For families, the increased Child Tax Credit of $2,200, indexed to inflation, helps ease housing costs for families, indirectly supporting housing affordability by freeing up income for mortgage payments.

Financing and Mortgage Considerations Under OBBB

The OBBB’s tax changes create new considerations for mortgage financing and lending standards. Enhanced tax benefits for homeowners and investors could increase demand for real estate financing, potentially affecting interest rates and lending practices.

Lenders may need to adjust their debt-to-income calculations to account for the permanent mortgage insurance premium deductions and expanded SALT benefits. These changes effectively reduce borrowers’ net housing costs, potentially qualifying more buyers for larger loan amounts.

The bill’s emphasis on business income deductions and investment incentives could also drive demand for investment property financing. Lenders specializing in rental property loans and commercial real estate may see increased activity as investors seek to capitalize on enhanced tax benefits.

For those looking to navigate these changing conditions, using tools like the Griffin Gold app can help track market conditions and identify optimal financing opportunities as the OBBB’s effects unfold.

Criticisms and Support of the OBBB Tax Bill

Supporters of the OBBB real estate changes argue that the legislation provides crucial economic stimulus through targeted tax relief. The National Association of Realtors praised the bill’s passage, with NAR’s executive vice president noting that the provisions “form the backbone of the real estate economy — from supporting first-time and first-generation buyers to strengthening investment in housing supply and protecting existing homeowners.”

Proponents emphasize that the bill’s real estate provisions will increase housing production, improve affordability through permanent tax benefits, and provide certainty for long-term investment planning. The permanent nature of many provisions removes uncertainty that has historically hampered investment decisions.

Critics, however, raise concerns about the bill’s fiscal impact and distributional effects. The Congressional Budget Office estimates that the bill will add $3.4 trillion to federal deficits over the next 10 years, raising questions about long-term fiscal sustainability.

Some analysts worry that enhanced tax benefits for higher-income homeowners and investors could exacerbate wealth inequality, particularly given that many benefits are concentrated in high-cost, high-income areas. There are also concerns that increased demand driven by tax incentives could push home prices higher, potentially offsetting affordability gains for some buyers.

Navigate the Market With Mortgage Experts

The OBBB real estate changes create opportunities and complexities. Whether you’re a first-time homebuyer looking to maximize mortgage interest deductions, an investor seeking to leverage enhanced depreciation benefits, or a current homeowner considering refinancing strategies, professional mortgage expertise is essential.

At Griffin Funding, our experienced loan officers understand how the OBBB’s provisions affect different borrower situations and can help you structure financing to maximize your tax benefits.

The changing regulatory environment and enhanced tax incentives create new opportunities for strategic real estate investment and homeownership. Contact Griffin Funding today to learn about our comprehensive range of home loans or get started online to find the right mortgage product for you.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Is mortgage insurance now tax deductible under the OBBB?

Yes. The OBBB makes mortgage insurance premiums (MIP) permanently tax-deductible. This includes:

- FHA Mortgage Insurance Premiums (MIP)

- VA Funding Fees (VA FF)

- USDA Guarantee Fees

- Private Mortgage Insurance (PMI) for conventional loans

This change lowers the effective cost of loans with lower down payments and makes homeownership more affordable, especially for first-time buyers and borrowers who put down less than 20%.

What is the new SALT deduction cap under the OBBB?

The State and Local Tax (SALT) deduction cap has been temporarily increased from $10,000 to $40,000 for households earning under $500,000. This change applies from 2025 through 2029, providing major tax relief for homeowners in high-tax states like California, New York, and New Jersey.

How does the OBBB benefit real estate investors?

The OBBB delivers several powerful benefits for investors:

- 100% Bonus Depreciation on qualifying improvements and equipment.

- Permanent 20% Qualified Business Income (QBI) Deduction for rental income.

- Preserved 1031 Exchanges for deferring capital gains taxes.

- Expanded Opportunity Zone Benefits to encourage investment in underserved communities.

- Deductible Mortgage Interest on Investment Properties, even when using leverage like DSCR loans.

What is the 100% bonus depreciation rule?

The 100% bonus depreciation provision allows real estate investors to deduct the entire cost of eligible property improvements and equipment in the year they’re placed into service rather than depreciating over time. This accelerates tax write-offs and can significantly reduce taxable income.

What happens to 1031 exchanges under the OBBB?

Section 1031 like-kind exchanges remain unchanged. Investors can still defer capital gains taxes when selling one investment property and purchasing another of “like kind.” This helps build portfolios more efficiently by preserving capital.

Can I still deduct mortgage interest on my home?

Yes. The OBBB makes the $750,000 mortgage interest deduction cap permanent. Homeowners with acquisition debt under this limit can continue to deduct interest on their primary and secondary homes.

Does the OBBB affect the Child Tax Credit?

Yes. The Child Tax Credit is increased to $2,200 and will now adjust for inflation, providing families with extra financial relief that can help offset housing costs.

Does the bill impact loan qualification?

Indirectly, yes. Since mortgage insurance is now deductible and the SALT cap is expanded, many borrowers will see lower net housing costs, which may:

- Improve debt-to-income (DTI) ratios

- Allow qualification for larger mortgage amounts

- Make low-down-payment loans more accessible

Lenders may adjust their underwriting calculations to reflect these improved affordability metrics.

Are there any income limits on these benefits?

Yes. The expanded SALT deduction phases out for households earning over $500,000. Other benefits, such as mortgage insurance deductibility, do not have income-based phaseouts under the OBBB, though taxpayers should consult with a tax advisor.

How can I track these changes and identify the best mortgage options?

You can use the Griffin Gold app to:

- Monitor real estate market trends

- Assess the impact of tax benefits like bonus depreciation

- Explore mortgage options tailored to your financial situation

- Get prequalified and connect with loan experts

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...