How Much House Can I Afford With a $100k Salary?

How Much House Can I Afford With a $100k Salary?

KEY TAKEAWAYS

- Your home affordability on a $100K salary depends on factors like debt, credit score, savings, loan type, and current mortgage rates.

- The 28/36 rule helps determine a comfortable mortgage payment, ensuring you don’t overextend financially.

- In addition to external factors, how much house you can afford depends on how much of your income you’re comfortable spending on a mortgage payment.

Earning a $100K salary opens up a range of possibilities when buying a home, but affordability isn’t just about income. Factors like your expenses, savings, and loan terms all play a role in determining how much house you can comfortably afford. Understanding these elements can help you set a realistic budget and find a home that fits your financial situation. Before jumping into the numbers, it’s essential to consider what impacts affordability and how to make the most of your home-buying budget.

KEY TAKEAWAYS

- Your home affordability on a $100K salary depends on factors like debt, credit score, savings, loan type, and current mortgage rates.

- The 28/36 rule helps determine a comfortable mortgage payment, ensuring you don’t overextend financially.

- In addition to external factors, how much house you can afford depends on how much of your income you’re comfortable spending on a mortgage payment.

How Much Home Can I Afford With a $100k Salary?

The answer largely depends on your financial situation and other key factors. While a $100K salary provides a solid foundation to buy a house, affordability is influenced by your monthly expenses, debt, savings, and loan terms. Lenders use these factors to determine how much you can borrow while ensuring your mortgage payments remain manageable. One common guideline for assessing affordability is the 28/36 rule.

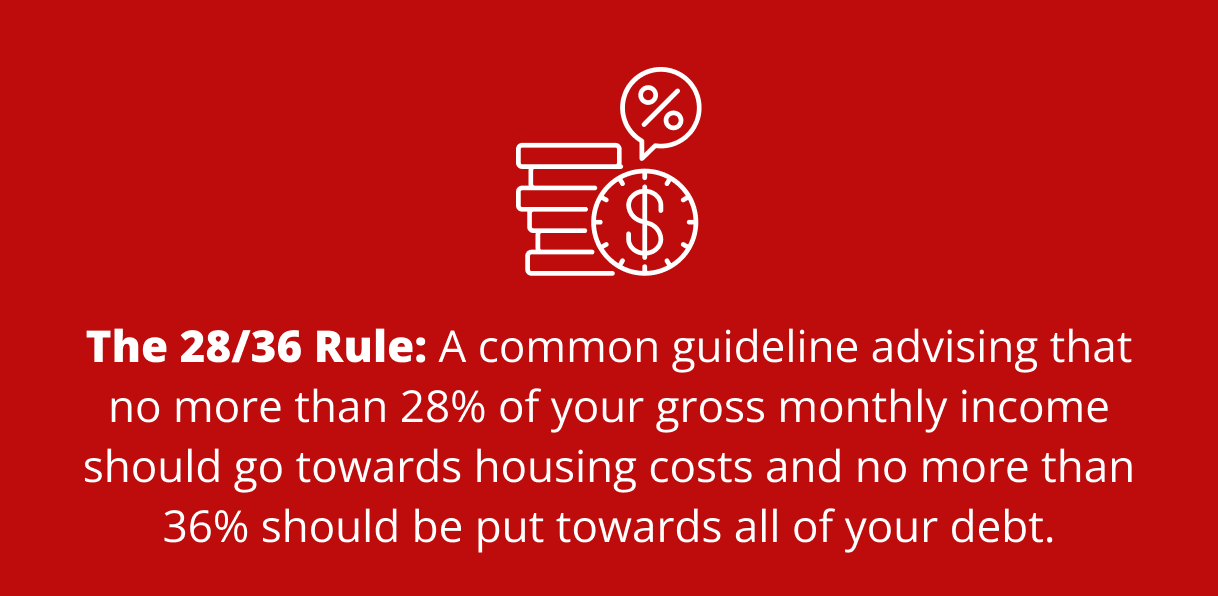

28/36 Rule

The 28/36 rule is a common guideline lenders use to evaluate how much home you can afford. It recommends that no more than 28% of your gross monthly income should go toward housing costs—including your mortgage, property taxes, and insurance—while no more than 36% should be allocated to total debt, including car loans, student loans, and credit cards.

For a $100K salary, this means your maximum monthly housing expense should be around $2,333, with total debt payments staying under $3,000. This rule will ensure you buy a house within a comfortable financial range without overextending your budget.

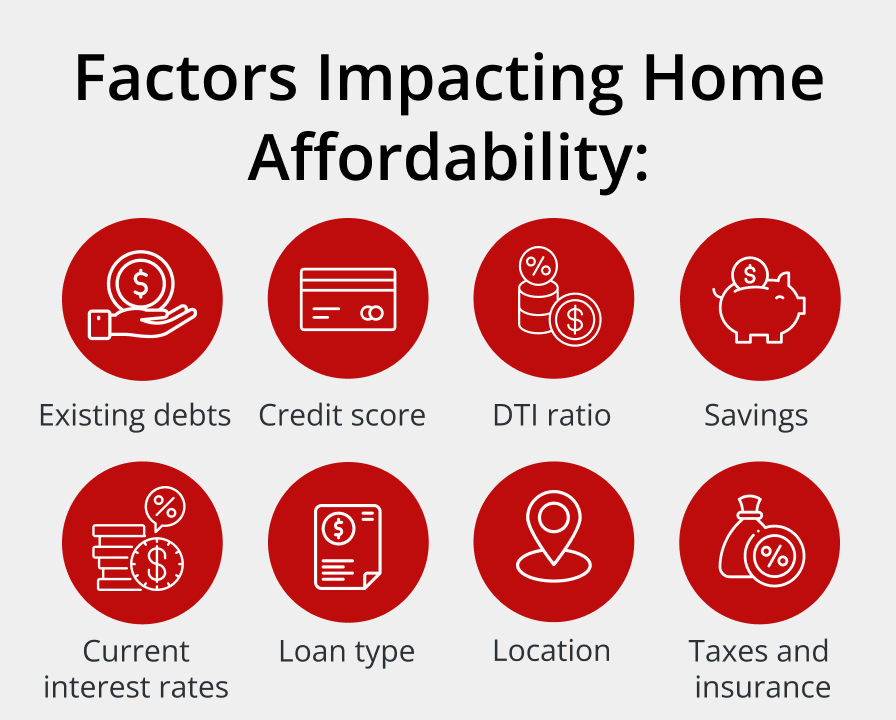

Factors Impacting Home Affordability

Your salary is just one component when figuring out how much home you can afford. Lenders consider several financial factors to assess what you can comfortably borrow and repay. Understanding these elements can help you set a realistic home-buying budget and avoid unexpected costs.

Existing Debts

Your current debt obligations significantly affect how much you can afford and if you qualify for a mortgage. To determine how much additional debt you can handle, lenders look at recurring payments such as student loans, car loans, credit card balances, and personal loans.

If you have significant monthly debt, it can limit the size of your mortgage and affect your loan terms. On the other hand, having little to no debt frees up more of your income for mortgage payments, potentially allowing you to qualify for a larger home loan with better interest rates. Reducing debt before applying for a mortgage can improve your borrowing power and affordability.

Credit Score

Your credit score directly impacts your mortgage options, as it determines the interest rates and loan terms available to you. A higher credit score usually leads to lower interest rates, reducing your monthly mortgage payment and making homeownership more affordable over the long term.

Borrowers with lower scores may face higher rates, which increase borrowing costs, or they may need to explore other financing options, such as a non-QM mortgage, which provides flexibility for those with unique financial circumstances. Improving your credit score before buying a home can help you secure better loan terms and save thousands over the life of your mortgage.

DTI Ratio

Your debt-to-income (DTI) ratio compares your total monthly debt payments to your gross monthly income, helping lenders assess whether you can comfortably take on a mortgage. A lower DTI ratio—typically under 36%—makes it easier to qualify for a mortgage and afford a higher-priced home.

If your DTI is too high, lenders may limit your borrowing limit or require you to pay down existing debts before approving your loan. Monitoring and lowering your DTI before applying for a mortgage can increase your home-buying options and improve your financial stability.

Keep in mind that with many non-QM loans, you can qualify for a mortgage with a higher DTI ratio. At Griffin Funding, we can approve borrowers with DTI ratios as high as 50% for non-QM loans.

Savings

Having enough savings is crucial when buying a home, not only for the down payment but also for closing costs and emergency reserves. A larger down payment can reduce your loan amount, lower your monthly mortgage payment, and even help you avoid private mortgage insurance (PMI) on conventional loans.

Additionally, some lenders require reserves—extra savings set aside after closing—to ensure you can continue making mortgage payments in case of financial hardship. Building your savings before purchasing a home can improve affordability and provide financial security once you become a homeowner.

Current Mortgage Rates

Mortgage rates fluctuate based on market conditions and can significantly impact how much home you can afford. Even a small difference in interest rates can add up to thousands of dollars over the life of a loan.

When rates are low, buyers can afford more expensive homes with the same monthly budget, while higher rates increase borrowing costs and may require buyers to adjust their price range. Monitoring market trends and securing a favorable rate can maximize affordability and reduce long-term housing expenses.

Loan Type

The type of loan you choose impacts your interest rate, down payment requirements, and overall affordability. Conventional loans often have lower rates and fewer restrictions for borrowers with strong credit, while a non-QM mortgage may be a better fit for those with non-traditional income sources like self-employed individuals.

Government-backed loans, like FHA or VA loans, also provide different advantages, such as lower down payment requirements or more flexible credit score standards. Comparing loan options and working with different lenders can help you find the best terms for your financial situation.

Location

Where you buy a house plays a major role in affordability, regardless of salary. Home prices vary widely based on the cost of living, demand, and local market conditions. A $100K salary may be sufficient to buy a spacious home in a smaller city or rural area, while the same income may barely cover a small condo in a high-cost metropolitan area.

Additionally, living expenses, property values, and access to amenities can all affect your long-term financial stability. Researching different housing markets can help you find a location where you get the most value for your budget.

Taxes and Insurance

Beyond the mortgage itself, property taxes and homeowners insurance add to your overall monthly housing costs and vary widely by location. Some states have significantly higher property taxes than others, making an otherwise affordable home more expensive in the long run.

Insurance costs also depend on where you buy—homes in high-risk areas, such as those prone to hurricanes, wildfires, or flooding, often require higher insurance premiums. While a house in a high-risk area may have a lower purchase price, the cost of insurance can quickly add up, making it less affordable over time. Considering these costs before buying a home gives you a clear picture of your total housing expenses.

Example: What House Can You Afford on $100k a Year?

Using a hypothetical scenario, let’s break down how much home someone earning $100,000 per year could afford.

- Income: $100,000 per year ($8,333 per month)

- Debt-to-Income (DTI) ratio: 36%

- Monthly debts: $500 (e.g., car payment, student loans, credit card minimums)

- Interest rate: 6.5%

- Loan term: 30 years

To determine affordability, lenders typically follow the 28/36 rule, meaning no more than 28% of your gross monthly income should go toward housing costs, and total debt payments (including your mortgage) should not exceed 36% of your income.

Step 1: Calculate Maximum Monthly Mortgage Payment

With a 36% DTI, the total allowable debt payments per month would be:

$8,333 × 36% = $3,000

Since the borrower already has $500 in monthly debt obligations, that leaves:

$3,000 – $500 = $2,500 available for the mortgage payment (including principal, interest, property taxes, and insurance).

Step 2: Determine Home Price

Assuming a 6.5% interest rate on a 30-year loan and factoring in an estimated amount for taxes and insurance, a borrower could afford a home priced up to approximately $353,319 with a 20% down payment.

If the borrower puts down less than 20%, the monthly payment will increase due to private mortgage insurance (PMI) and a higher loan amount, reducing the home price they can afford.

See How Much House You Can Afford on a $100k Salary

Understanding how much home you can afford on a $100K salary depends on several key factors, including your debt, credit score, savings, and mortgage rate. By considering these elements and following affordability guidelines like the 28/36 rule, you can set a realistic budget and move forward in your home-buying journey.

At Griffin Funding, we specialize in helping buyers secure the right mortgage for their financial situation. Whether you’re looking for a conventional loan or a non-QM mortgage, our expert team can guide you through the process and find the best loan options to fit your needs. We also offer the Griffin Gold app, which lets you easily track your mortgage, manage payments, and stay on top of your budget and finances—all in one convenient place.

Get started on your mortgage journey today!

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business. Follow his updates on LinkedIn.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFeatured In

Recent Posts

Landlord-Friendly States Ranked for 2026: A Scored Methodology

Search for landlord-friendly states, and you will find a dozen rankings that disagree with each other, none of...

America’s Self-Employment Boom is Creating a New Class of Real Estate Investors

Self-employed investors are reshaping the real estate market, fueling record-high rental property investment t...

Best Bank Statement Loan Lenders 2026: Griffin Funding vs Farm Bureau Bank vs CrossCountry Mortgage vs North American Savings Bank vs Angel Oak vs Newfi

What to Look for in a Bank Statement Loan Lender Choosing the best bank statement loan lender for your situati...