Loan Level Price Adjustments (LLPAs): What They Are & How They Impact Rates

KEY TAKEAWAYS

- Loan-level price adjustments (LLPAs) are risk-based fees charged by Fannie Mae and Freddie Mac that increase your mortgage rate based on credit score, down payment, and property type.

- Investment properties face higher LLPAs than primary residences, often adding 0.50% to 1.50% or more to your rate.

- DSCR loans don’t follow the Fannie Mae LLPA matrix, which can make them more competitive for investors.

- Understanding LLPAs helps you choose the right loan program and potentially save thousands.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformWhen you’re shopping for a mortgage, the rate you’re quoted includes hidden risk-based fees called loan-level price adjustments. Most borrowers don’t even know they exist, but for real estate investors, these fees can add thousands to financing costs.

What Is a Loan-Level Price Adjustment (LLPA)?

A loan-level price adjustment is a fee charged on conventional mortgages to account for specific risk factors in your loan application. The riskier your loan profile looks, the higher the LLPA.

These adjustments exist because not all borrowers present the same level of risk. Instead of denying loans to higher-risk borrowers, Fannie Mae and Freddie Mac use LLPAs to charge higher rates that reflect that risk.

Fannie Mae and Freddie Mac set the LLPA guidelines for conventional loans. LLPAs can be applied as an upfront fee you pay at closing or rolled into your loan amount. More commonly, lenders convert the loan-level price adjustment fee into a higher interest rate.

How Loan-Level Price Adjustment Fees Work

The LLPA fee is calculated as a percentage of your loan amount. For example, if your loan has a 1.5% LLPA and you’re borrowing $400,000, that’s a $6,000 fee. Most borrowers never see this fee explicitly broken out on their Loan Estimate.

Instead of charging you upfront, lenders typically convert that fee into a rate increase. They might bump your interest rate from 6.5% to 6.875% to cover the cost. From your perspective, you just see a higher rate.

This is why two borrowers getting quotes from the same lender on the same day can see wildly different rates based on their individual risk profiles.

Fannie Mae LLPAs Explained

Fannie Mae plays a central role in how conventional loans are priced. When a lender originates a conventional mortgage, they typically sell it to Fannie Mae or Freddie Mac. To protect themselves from losses, these entities use a detailed LLPA matrix that accounts for dozens of risk factors.

The Fannie Mae LLPA matrix cross-references your credit score, down payment percentage, property type, loan purpose, and other variables to determine how much extra you’ll pay. Fannie Mae cares most about factors that statistically predict default risk, such as credit score, loan-to-value ratio, and property type.

Investment properties get hit especially hard by Fannie Mae’s pricing. The LLPA for an investment property is typically several points higher than for a primary residence because historical data shows borrowers prioritize their primary home over rental properties during financial hardship.

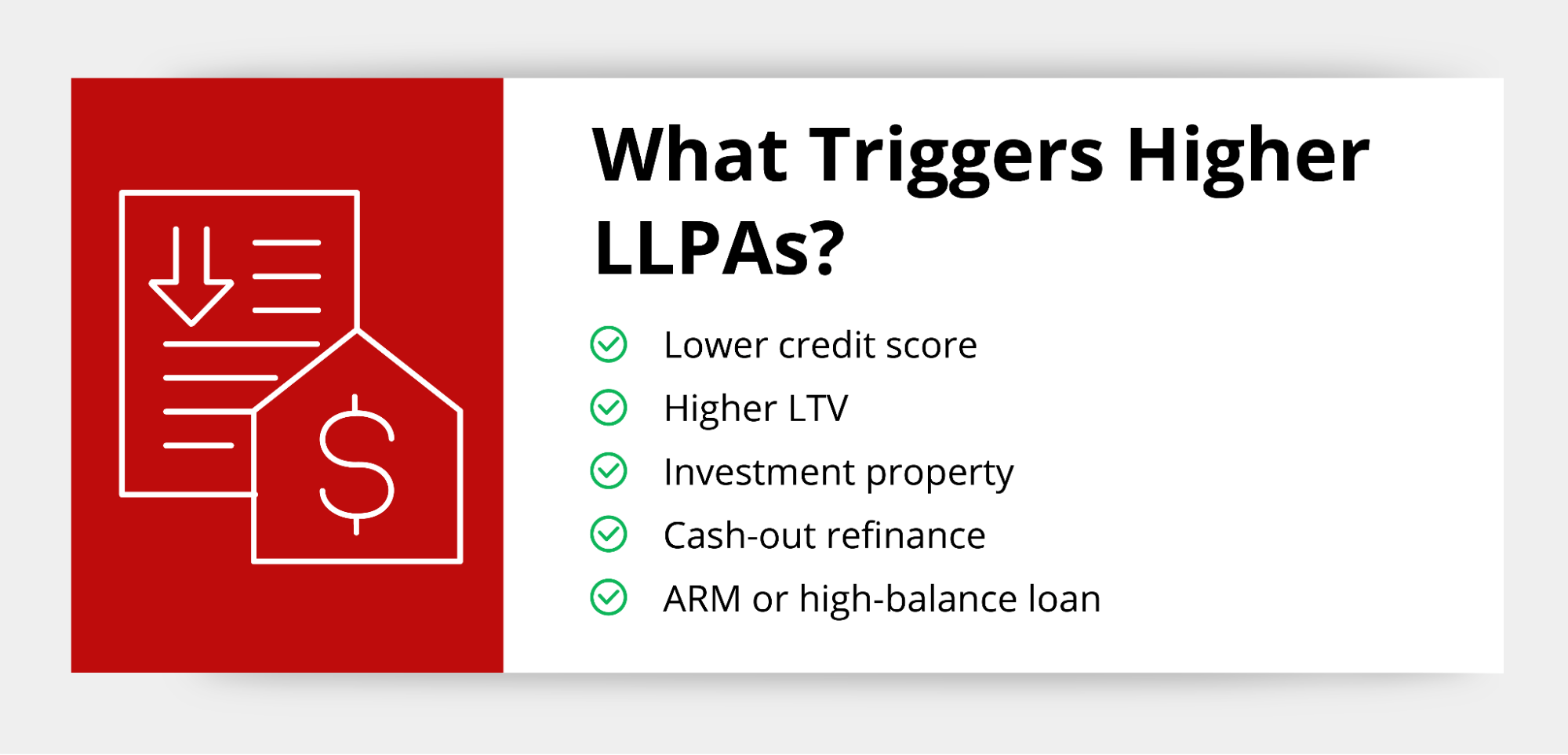

What Triggers Higher LLPAs?

Several factors influence your LLPA, and understanding them helps you see why your rate might be higher than expected. Here’s what lenders look at:

Credit Score

Credit Score

Your credit score has one of the biggest impacts on your loan-level price adjustment. Fannie Mae uses tiered pricing thresholds, where borrowers with scores of 740 or higher get the best pricing. Drop down to the 720-739 range, and your LLPA increases. The gap between credit tiers can be substantial. For example, a borrower with a 750 score might pay 0.25% in LLPAs while someone with a 690 score on the same loan could pay 2.0% or more.

Loan-to-Value (LTV)

Your down payment size directly affects your LLPA. Higher leverage means higher risk. Even putting 20-25% down on an investment property still triggers meaningful LLPAs. The LLPA pricing isn’t linear. The biggest reductions typically happen when you cross major thresholds like moving from 75% LTV to 70% LTV.

Property Type

Investment properties and second homes carry substantially higher LLPAs than primary residences. Even within investment property loans, the type of property matters. A single-family rental might have a lower LLPA than a 2-4 unit property.

Loan Characteristics

Certain loan features trigger additional LLPAs. Cash-out refinances carry higher LLPAs than rate-and-term refinances. Adjustable-rate mortgages sometimes have their own LLPA adjustments. High-balance loans that exceed conforming limits face additional pricing hits.

How LLPAs Impact Interest Rates on Investment Property Loans

For real estate investors, LLPAs stack. You might have an LLPA for your credit score, another for your LTV ratio, another for the property being an investment property, and potentially more. On a conventional investment property loan, combined LLPAs often raise your rate by 0.50% to 1.50% or more.

An investor with a 720 credit score putting 20% down on a single-family rental might see multiple LLPAs applied. By the time the lender converts all those adjustments to an interest rate, what started as a 6.0% base rate might end up at 7.25%. This is why the belief that conventional is always cheaper often doesn’t hold true for investors.

The 2022-2023 LLPA Overhaul: What Changed for Investors

LLPAs aren’t static. The Federal Housing Finance Agency (FHFA) made sweeping changes to the LLPA framework in 2022 and 2023 that significantly increased costs for real estate investors using conventional financing.

The first major change took effect on April 1, 2022, when FHFA dramatically increased upfront fees on second home loans. Before this change, second homes had minimal LLPAs — in many scenarios, there was no additional pricing adjustment at all. Overnight, second home LLPAs jumped to between 1.125% and 3.875% depending on LTV, putting them in nearly the same pricing range as investment properties.

This affected short-term rental investors especially hard. Before April 2022, a popular strategy was to purchase a property as a second home with as little as 10% down and get a rate close to what you’d pay on a primary residence — then list it on Airbnb or VRBO. FHFA effectively shut down that pricing advantage.

Then on May 1, 2023, FHFA rolled out a comprehensive redesign of the entire LLPA matrix. The overhaul shifted credit score tiers, adjusted LTV buckets, increased fees on cash-out refinances, and moved the best pricing threshold from a 740 credit score to 780. While investment property LLPAs were already steep, the restructured matrix changed how all these fees stack together.

The result: conventional financing for investment properties and second homes became meaningfully more expensive. For investors who were already dealing with layered LLPAs, these changes made alternative loan programs like DSCR loans even more worth considering.

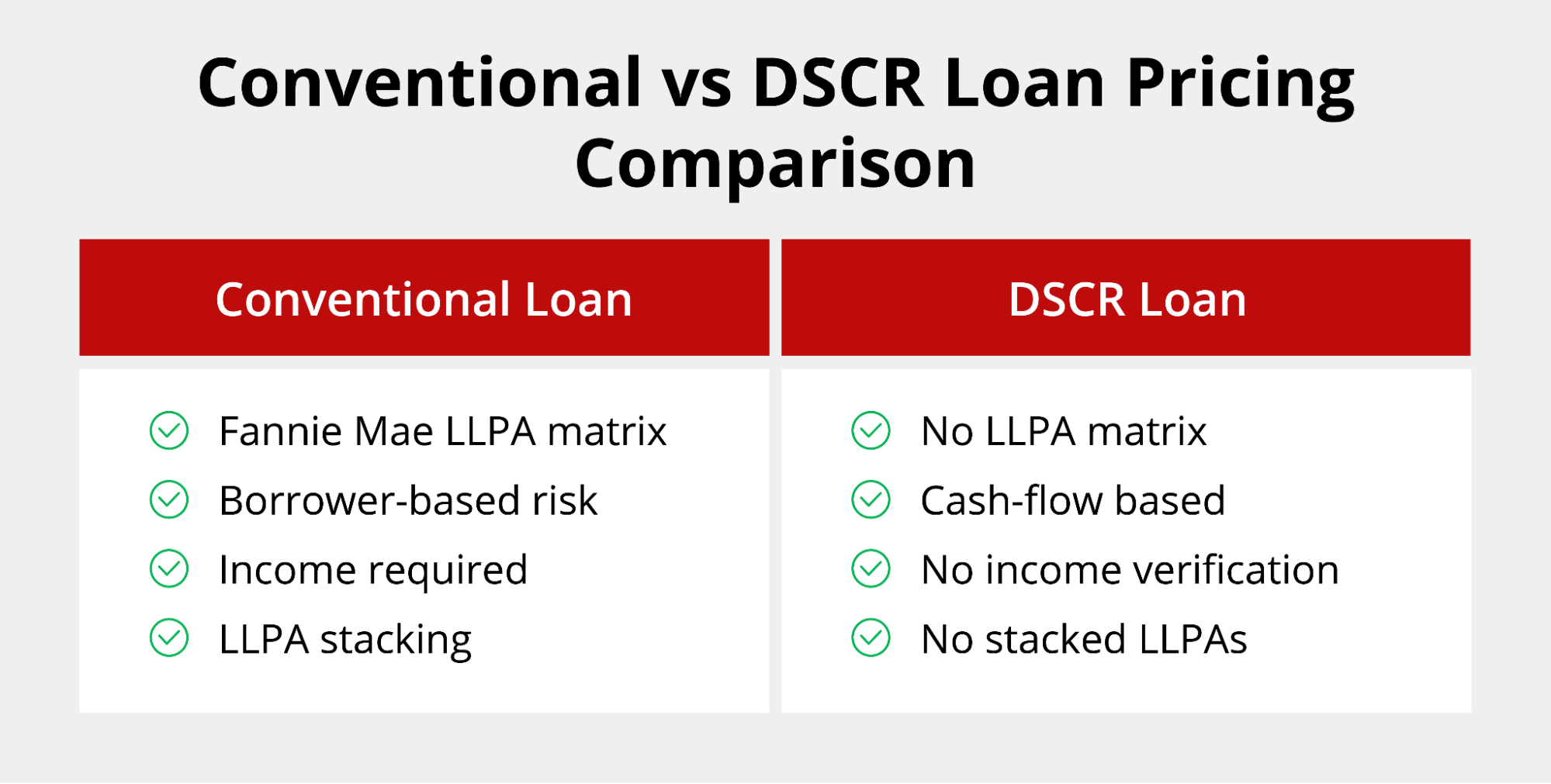

Why DSCR Loans Can Be More Competitive Than Conventional Loans

DSCR loans operate outside the Fannie Mae system, which means they’re not subject to the LLPA matrix. Instead, these loans are priced based on the property’s rental income.

DSCR loans operate outside the Fannie Mae system, which means they’re not subject to the LLPA matrix. Instead, these loans are priced based on the property’s rental income.

Because DSCR loans don’t use personal income-based underwriting, there’s no LLPA for your debt-to-income ratio or employment status. The lender focuses on whether the property’s rental income covers the mortgage payment.

Without the Fannie Mae LLPA matrix, DSCR lenders price loans more holistically. They look at the investment itself rather than layering on fee after fee. For investors who would face heavy LLPAs on a conventional loan, this can tip the scales in favor of DSCR. Comparing DSCR vs conventional loans helps you see which option saves you money.

When a DSCR Loan May Be the Better Option

Several situations make DSCR loans more attractive than conventional financing. Here are scenarios where DSCR pricing often beats conventional financing:

- Self-employed real estate investors: Your tax returns show minimal income due to write-offs. Conventional lenders may limit qualification or pricing flexibility due to income documentation requirements, but DSCR lenders don’t take your personal income into account.

- Portfolio growth strategies: You’re scaling quickly with multiple properties. Conventional loans cap borrowers at 10 financed properties, and pricing often worsens as risk factors stack.

- Short-term rental investors: Your property generates strong Airbnb or VRBO cash flow, but conventional underwriting doesn’t account for that properly.

- Borrowers affected by stacked LLPAs: Your credit is good but not great, and you’re putting 20-25% down. Those combined LLPAs push your conventional rate higher.

- Scaling beyond Fannie Mae loan limits: You’re building a substantial real estate portfolio and need financing that doesn’t get progressively more expensive.

How to Reduce the Impact of LLPAs

While you can’t eliminate LLPAs entirely on conventional loans, you can minimize their impact with these approaches:

- Improve credit score before applying: Even a small increase can move you into a better pricing tier. If you’re at 715, getting to 720 might save you significantly. Pushing from 735 to 740 could be worth thousands.

- Increase down payment strategically: Putting down 25% instead of 20% reduces your LLPA, but run the numbers to see if you’d earn a better return by keeping that money for another deal.

- Choose the right loan program: Don’t assume conventional is always best. Get quotes for both conventional and DSCR loans to see which offers better terms. The Griffin Gold app can help you track and compare options.

- Work with an investor-focused lender: A lender who specializes in investment properties understands the nuances and can help you learn about and compare your options.

- Compare DSCR vs conventional pricing: Get actual rate quotes for both programs. What looks more expensive on paper might be cheaper once all the LLPAs are factored in. Pay attention to current mortgage rates and the various factors impacting mortgage rates.

Understanding LLPAs Can Help You Save

Loan-level price adjustments might seem like an obscure detail, but they have real financial consequences. Don’t assume you know which loan program will be cheaper until you see actual quotes that account for all the fees and adjustments. The conventional loan that looks attractive at first might be loaded with LLPAs that push the rate above what you’d pay with a DSCR loan.

An investor-focused lender can compare conventional and DSCR pricing side by side so you see the real cost difference. Griffin Funding specializes in investment property financing. We work with real estate investors who need to understand the true cost of their financing options and want a lender who knows how to price DSCR loans against conventional products.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

How do LLPAs affect interest rates?

Do DSCR loans have loan-level price adjustments?

Why can DSCR loans have lower rates than conventional investment loans?

When did LLPAs increase for investment properties and second homes?

Then in May 2023, FHFA redesigned the entire LLPA matrix, adjusting credit score thresholds, LTV buckets, and cash-out refinance fees. Together, these changes made conventional financing significantly more expensive for investors, which is one reason DSCR loans have become an increasingly competitive alternative.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...

Mid-Term Rentals: Guide for Real Estate Investors

Mid-term rentals are furnished properties leased for 30 days to 12 months, targeting traveling professionals, ...