VA Waiting Periods: Seasoning for Foreclosure, Short Sale, & Bankruptcy

KEY TAKEAWAYS

- VA loan seasoning periods vary by event, with foreclosures typically requiring a 2-year wait, while short sales may have no waiting period if payments were current.

- Bankruptcy timing matters since Chapter 7 requires 2 years from discharge, but Chapter 13 allows qualification after just 12 months of on-time payments.

- Use the waiting period wisely by focusing on rebuilding credit, maintaining stable housing payments, and saving for closing costs.

- Extenuating circumstances can help since lenders will sometimes consider shorter waiting periods if the financial hardship was due to circumstances beyond your control.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFinancial hardships can happen to anyone, and sometimes circumstances beyond our control can lead to foreclosure, bankruptcy, or short sale. However, these events don’t permanently disqualify you from homeownership, especially if you’re a veteran eligible for VA loan benefits.

Understanding the waiting periods, also known as seasoning requirements, after these financial events is crucial for planning your path back to homeownership. Let’s break down what you need to know about VA loan waiting periods and how to make the most of this time.

What Is a VA Loan Seasoning Period?

VA loans offer incredible benefits that make homeownership more accessible for veterans and service members. They come with no down payment requirements, no private mortgage insurance, competitive interest rates, and the ability to reuse your benefit multiple times. These advantages make VA loans one of the best homebuying tools available.

A “seasoning period” is simply the amount of time you need to wait after a major financial event before you can qualify for a new mortgage. Lenders require these waiting periods because they want to see that you’ve recovered financially and are unlikely to face the same problems again. The good news is that you can get a VA loan after bankruptcy, foreclosure, and short sale.

The reasoning behind a seasoning period is simple: if someone just went through foreclosure or bankruptcy, there’s a higher risk they might struggle with mortgage payments again soon. Lenders require a waiting period so they can see evidence that you’ve stabilized your finances, rebuilt your credit, and developed better money management habits.

Waiting periods aren’t the same for every financial event. A foreclosure involves losing your home involuntarily, while a short sale is typically a more controlled exit from homeownership. Bankruptcy can actually be a fresh start that clears problematic debts. Each situation gets treated differently by lenders.

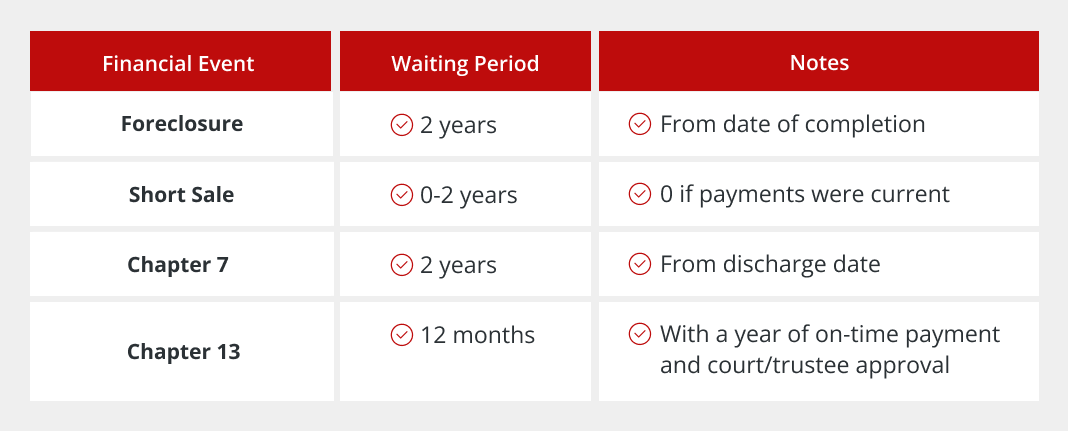

VA Loan Waiting Period After Foreclosure

The standard VA foreclosure waiting period is two years from the date the foreclosure is completed. This means two full years from when you officially lose ownership of the property, not from when you first missed payments or when the process started.

Understanding what “completion” means is important because foreclosure is a legal process that can take months or even years. The foreclosure is complete when the property is sold at auction, you deed the property back to the lender, or the lender takes full legal ownership. The waiting period clock starts ticking from that final date.

Foreclosure typically causes significant damage to your credit score. However, the impact lessens over time, and many people see substantial recovery within the two-year waiting period. This is part of why the waiting period exists — it gives your credit time to recover naturally.

There are exceptions for extenuating circumstances. If your foreclosure was caused by factors completely beyond your control — like a serious illness, military deployment complications, or natural disaster — some lenders might consider a shorter waiting period. You’ll need extensive documentation proving the circumstances were truly unavoidable.

VA Loan Waiting Period After Short Sale

Short sales are typically treated more favorably than foreclosures in most cases. If you completed a short sale while keeping your mortgage payments current up until the sale, many lenders don’t require a VA short sale waiting period at all. This is because a short sale, if you’re current on payments, shows financial responsibility and proactive problem-solving. However, if you were delinquent on mortgage payments at the time of the short sale, you might face up to a two-year waiting period.

From a lender’s perspective, there’s a big difference between someone who proactively addressed an underwater mortgage situation versus someone who stopped paying and then did a short sale as a last resort. The first scenario shows financial maturity, while the second looks more like someone who gave up on their obligations.

After a short sale, lenders will want documentation showing the circumstances that led to the sale, proof that you attempted to work with your previous lender, and evidence of your current financial stability. Being organized with this paperwork can speed up your application process.

VA Loan Waiting Period After Bankruptcy

VA Bankruptcy waiting periods depend on which type you filed and your current circumstances.

Chapter 7 Bankruptcy

Chapter 7 bankruptcy typically requires a two-year waiting period from the discharge date, not the filing date. The bankruptcy process can take several months, and the waiting period doesn’t start until the court officially discharges your debts.

Keep in mind there’s a difference between “discharged” and “dismissed”. A discharge means the court eliminated your qualifying debts, and you successfully completed the bankruptcy process. A dismissal means the case was thrown out for some reason, and you don’t get the benefits of debt elimination. Only a discharge starts the waiting period clock.

During your two-year wait after Chapter 7, focus on rebuilding credit responsibly. Consider a secured credit card, keep any remaining accounts current, and avoid taking on unnecessary debt. Many people are surprised by how much their credit can recover during this period with consistent effort.

Chapter 13 Bankruptcy

Chapter 13 has much more favorable timing for VA loans. You may be able to qualify for a VA loan just 12 months into your Chapter 13 repayment plan, provided you get court approval and meet specific requirements.

You’ll need to show 12 consecutive on-time payments to your bankruptcy trustee and get written permission from the court to take on new debt. The trustee will evaluate whether adding a mortgage payment fits within your approved budget and won’t jeopardize your ability to complete the bankruptcy plan.

The main advantage here is that you don’t need to wait for the final discharge. If you’re in good standing with your payment plan after 12 months, you can move forward with homebuying while still technically in bankruptcy.

Documentation is critical for Chapter 13 VA loans. You’ll need trustee approval letters, payment history records, and court permission.

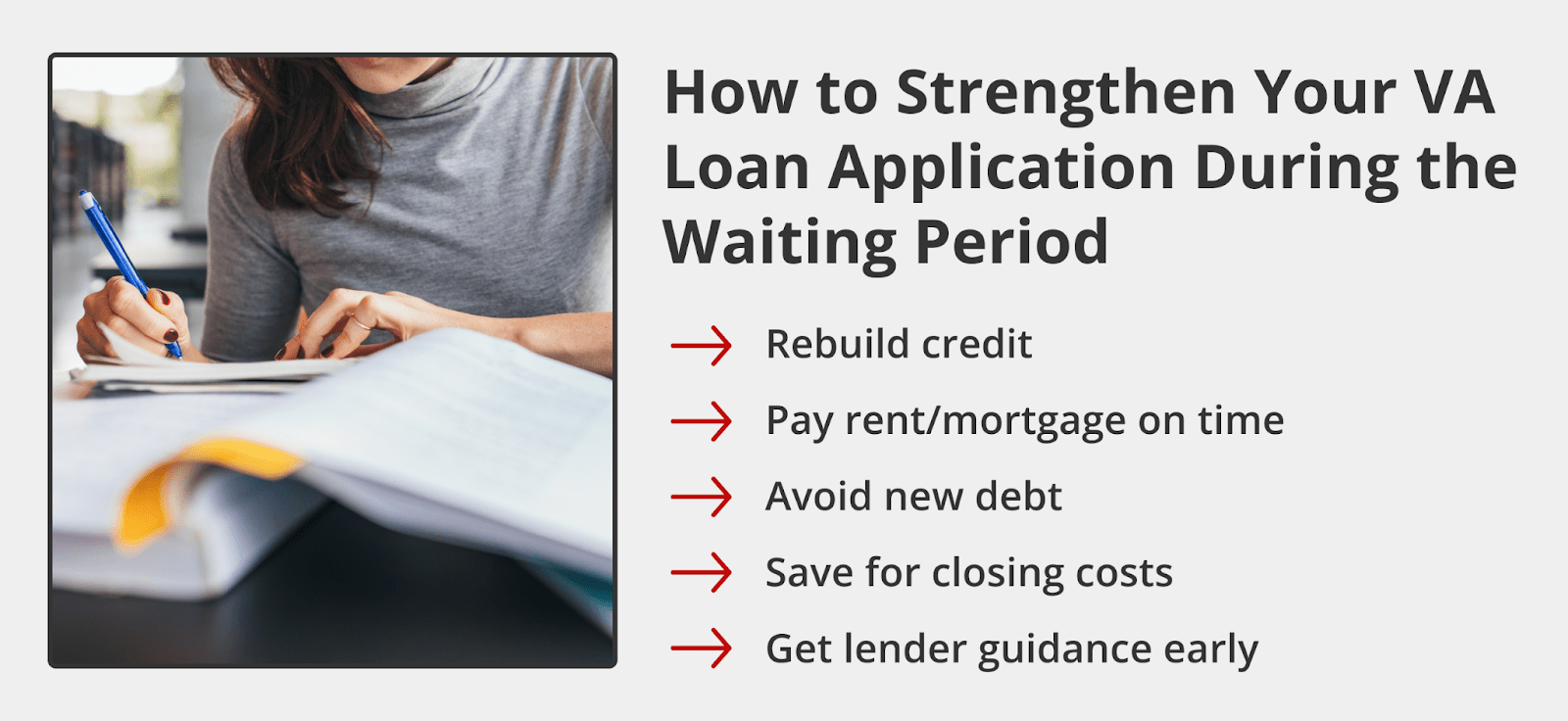

How to Strengthen Your VA Loan Application During the Waiting Period

The VA loan waiting period is an opportunity to position yourself for loan approval and better terms. Instead of simply counting down the days, start actively improving your financial profile. The difference between someone who uses this time strategically versus someone who doesn’t can mean the difference between approval and denial, or between getting a great rate and paying more over the life of the loan.

- Rebuilding credit: Get your credit reports from all three bureaus and dispute any errors immediately. It might be worth it to get a secured credit card to establish new credit, but keep balances under 10% of the limit and pay in full every month. Even small credit score improvements can significantly impact your interest rate and monthly payment amount.

- Maintaining on-time rent or mortgage payments: Lenders scrutinize your housing payment history more than anything else since it’s the best predictor of future mortgage performance. Set up automatic payments if possible and keep detailed records showing 12-24 months of perfect payment history, even if you’re staying with family and paying them directly.

- Avoiding new collections or major debt: Every new negative item on your credit report can extend your recovery timeline by months or even restart the clock entirely. If you’re struggling with bills, contact creditors immediately to work out payment plans rather than letting accounts go to collections.

- Saving for closing costs or reserves: While VA loans don’t require down payments, you’ll still need to cover closing costs, which vary depending on your loan amount and location. Our VA loan affordability calculator can help you determine your budget and find a monthly payment that fits comfortably with your income and existing debts. Having 2-3 months of mortgage payments saved also shows lenders you can handle unexpected expenses without missing payments.

- Working with a VA loan expert to prepare early: Connecting with a VA-experienced lender like Griffin Funding early in your waiting period can help you understand what lenders are looking for and avoid potential issues that could delay your approval.

Get a VA Loan With Griffin Funding

At Griffin Funding, we understand that financial hardships don’t define your future as a homeowner. We focus on guiding veterans through the journey back to homeownership following difficult financial situations.

We also offer helpful tools and can assist with complex situations like VA restoration of entitlement or VA debt consolidation loan options. Download the Griffin Gold app to compare mortgage options and access financial management tools, and get started online today.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

How long after bankruptcy can I get a VA loan?

The VA Chapter 7 bankruptcy waiting period generally requires two years from the discharge date. In contrast, the VA Chapter 13 bankruptcy waiting period is more flexible—you may qualify after 12 months of consistent, on-time payments to your trustee, provided you have court approval. It's important to show financial stability and meet all lender requirements during the waiting period.

Once you're eligible, use our VA loan calculator to estimate your potential monthly payments and see what you might qualify for.

Why do VA lenders require a waiting period after foreclosure or bankruptcy?

Waiting periods help lenders assess risk and give borrowers time to rebuild financial stability. These events often indicate temporary financial stress, and the waiting period allows time for credit recovery, income stabilization, and the development of better financial management habits. It's essentially a cooling-off period that benefits both borrowers and lenders.

Does the VA ever waive waiting periods due to extenuating circumstances?

While the VA itself doesn't set waiting periods (individual lenders do), many lenders will consider shorter waiting periods for extenuating circumstances. These might include serious illness, natural disasters, military deployment issues, or other events completely beyond your control. You'll need extensive documentation proving the circumstances were unavoidable.

Can I restore my VA loan entitlement after bankruptcy or foreclosure?

Bankruptcy or foreclosure doesn't permanently affect your VA loan entitlement. Once you meet the waiting period requirements and qualify for a new VA loan, you can use your benefits again. If you had a previous VA loan, you might need to go through the entitlement restoration process, but this is typically straightforward after satisfying the waiting requirements.

What counts as the start of the waiting period for VA loans?

The waiting period starts from specific completion dates:

- For foreclosure, it's when the property transfer is finalized

- For Chapter 7 bankruptcy, it's the discharge date

- For Chapter 13, it's typically 12 months into your payment plan

- For short sales, it might be immediate if the payments were current.

Working with a VA loan expert can help clarify these dates and get you ready to qualify as soon as possible.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...