What Is an Escalation Clause in Real Estate?

KEY TAKEAWAYS

- An escalation clause automatically raises your offer when competing bids come in, helping you stay competitive without starting with your highest price.

- Buyers should set a realistic cap and require proof of competing offers to avoid overpaying or getting manipulated.

- While escalation clauses work well in competitive markets with low inventory, they can backfire in slower markets or when appraisal gaps become an issue.

- Sellers may appreciate the transparency of escalation clauses, but some prefer the simplicity of a highest and best offer strategy.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformIn a competitive housing market, it’s not enough to simply find your dream home. You might put in a solid offer, only to lose out to another buyer who bid higher. If this keeps happening to you, an escalation clause might be the solution you’re looking for. So, what is an escalation clause?

An escalation clause in real estate is a provision in your purchase offer that automatically increases your bid if another buyer submits a competing offer. Instead of guessing what it’ll take to win or leaving money on the table, this clause lets you stay competitive without overpaying from the start. But like any strategy in real estate, it comes with both advantages and risks that buyers and sellers should understand.

Keep reading to learn how escalation clauses work, when to use them, and how to protect yourself in the process.

What Is an Escalation Clause?

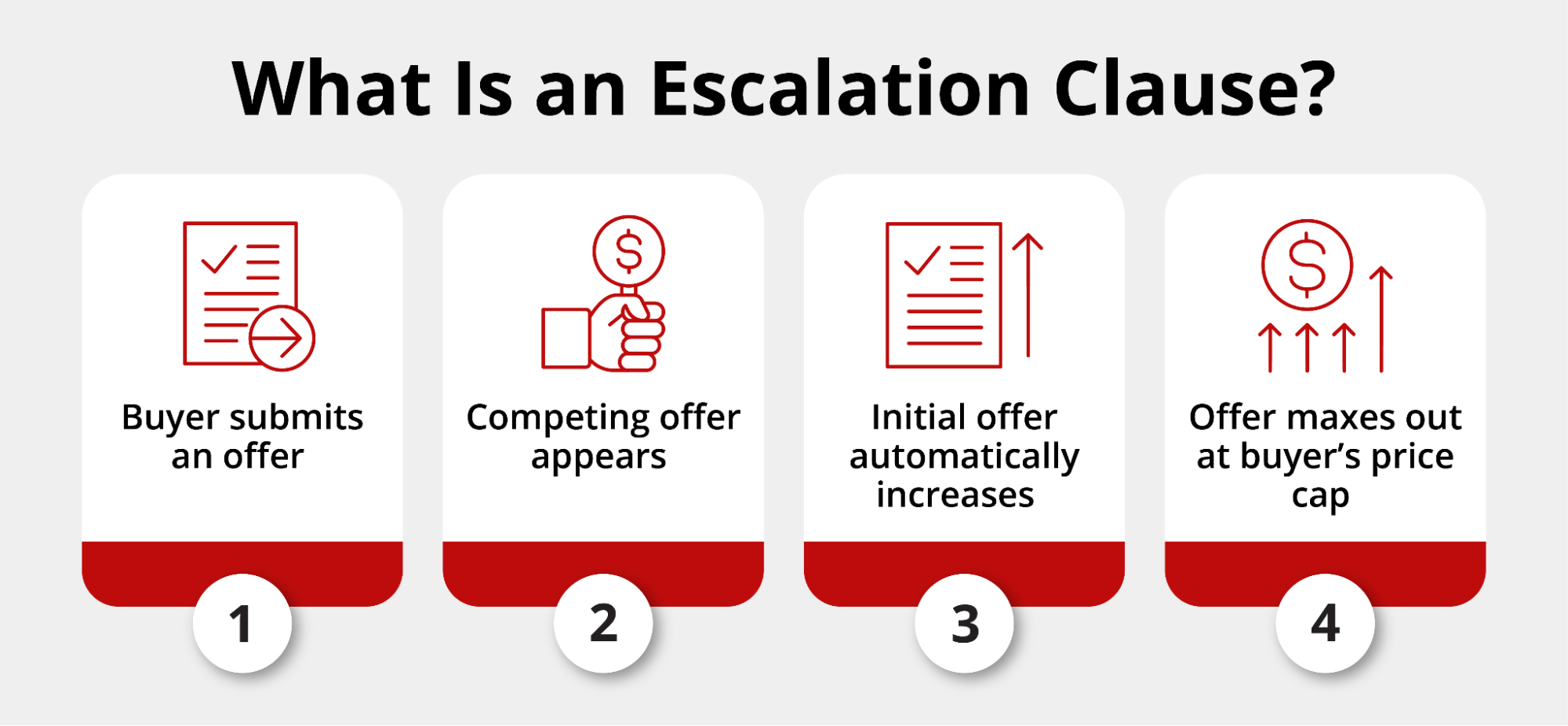

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automatically by a predetermined amount if another buyer submits a higher offer.

Here’s how it works in practice: You submit an initial offer on a home at $400,000, but you include an escalation clause that says you’ll beat any competing offer by $5,000, up to a maximum of $430,000. If another buyer offers $410,000, your offer automatically escalates to $415,000. If someone offers $427,000, you’d go up to $432,000, but since that exceeds your $430,000 cap, your offer maxes out at your predetermined limit.

The escalation clause only activates when the seller receives a bona fide competing offer and provides proof of that offer to your agent. This protection keeps sellers honest and prevents them from inflating fake bids just to drive up your price.

Key Components of an Escalation Clause

Every escalation clause should include four essential elements to protect both parties and create a clear framework for how the bidding process will unfold.

Original Offer Price

This is your starting bid — the amount you’re willing to pay if no other offers come in. Your original offer price should be competitive enough to get the seller’s attention but strategic enough to leave room for escalation.

Most buyers start with an offer that’s reasonable based on comparable sales in the area, then let the escalation clause do the heavy lifting if competition appears.

Escalation Amount

The escalation amount determines how much you’ll increase your bid above each competing offer. Common escalation increments range from $1,000 to $10,000, depending on the home’s price point and market conditions.

In hot markets where homes sell for $500,000 or more, escalation amounts of $5,000 to $10,000 are typical. For properties under $300,000, buyers often use smaller increments of $1,000 to $3,000.

Your escalation amount should be large enough to beat competitors but not so generous that you’re giving away money unnecessarily.

Maximum Price (Cap)

Your cap is the highest amount you’re willing to pay, no matter how many competing offers roll in. This is your absolute walk-away number and should reflect what you can genuinely afford and what the home is worth to you.

Setting a realistic cap is crucial. If you set it too high and win the bidding war, you might end up with an appraisal gap that leaves you scrambling for extra cash at closing.

Proof of Competing Offer Requirement

This component protects you from unethical practices. Your escalation clause should explicitly state that the seller must provide written proof of any competing offer before your bid increases.

Without this safeguard, a seller could claim they received a higher offer when they actually didn’t, manipulating you into paying more than necessary. The proof requirement keeps the process transparent and fair.

Escalation Clause Example

Let’s walk through a realistic scenario to see how an escalation clause works in practice:

Sarah is a first-time buyer looking at a house listed for $375,000 in a neighborhood where homes typically sell within days of hitting the market.

Sarah’s agent drafts an offer with these terms:

- Initial offer: $380,000

- Escalation amount: $3,000 above any competing offer

- Maximum cap: $405,000

- Proof of competing offer required

Here’s how different scenarios would play out:

- Scenario 1: Another buyer submits an offer at $385,000. Sarah’s escalation clause kicks in, and her offer automatically increases to $388,000 ($385,000 + $3,000).

- Scenario 2: A third buyer comes in at $400,000. Sarah’s offer escalates to $403,000 ($400,000 + $3,000), which is still within her $405,000 cap.

- Scenario 3: A competing offer hits $404,000. Sarah’s escalation would push her to $407,000, but that exceeds her $405,000 maximum. Her final offer stays at $405,000.

If Sarah wins at $403,000, she’s only paid $3,000 more than necessary to beat the competition. Without the escalation clause, she might have started at $405,000 and left $22,000 on the table unnecessarily.

Pros and Cons of an Escalation Clause

Before adding an escalation clause to your offer, you’ll want to weigh the advantages against the potential drawbacks. Here’s what buyers and sellers should consider:

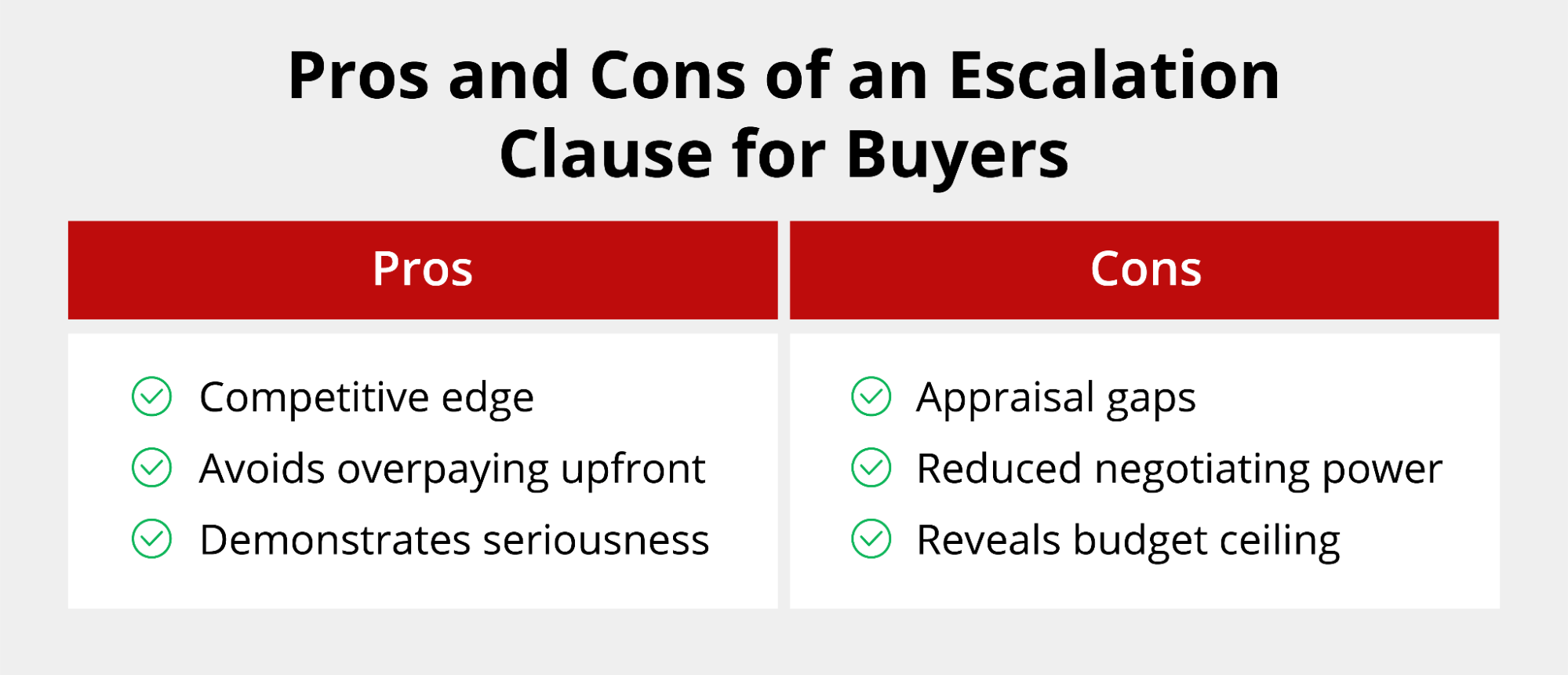

Pros for Buyers

Pros for Buyers

Understanding the benefits of using an escalation clause can help you decide if this option works for your situation. The pros of escalation clauses include:

- Competitive edge in bidding wars: You stay in the running without constantly revising and resubmitting offers, which can be exhausting in fast-moving markets where multiple offers are common.

- Avoids overpaying upfront: Instead of guessing what it’ll take to win and potentially offering too much, you only pay what’s necessary to beat the competition by your predetermined increment.

- Signals a strong intent to sellers: An escalation clause shows you’re serious about buying the property and willing to be flexible, which can make your offer more appealing even if it’s not the highest initially.

Risks for Buyers

While escalation clauses offer advantages, they also come with potential downsides that buyers need to understand, such as:

- Risk of overpaying beyond appraised value: If your escalation pushes you above what the home appraises for, you’ll need to cover the appraisal gap with cash or risk losing your financing. This is especially problematic if you’re using traditional mortgages that require the home to appraise at or above the purchase price.

- Less room for negotiation: Once you’ve revealed your maximum cap, you’ve essentially told the seller the most you’ll pay, leaving little wiggle room for other negotiations on repairs or closing costs.

- Can reveal buyer’s maximum budget: Savvy sellers and listing agents will see exactly how high you’re willing to go, which could influence their strategy in ways that don’t benefit you.

Seller Perspective

Sellers have mixed feelings about escalation clauses, and their preferences often depend on the specific situation.

- Why some sellers love escalation clauses: They appreciate the transparency and efficiency. Instead of playing games with multiple rounds of highest and best offers, the escalation clause streamlines the process. Sellers also know they’re getting the buyer’s true maximum, which can provide confidence that the deal won’t fall apart later due to buyer’s remorse.

- Why others prefer “highest and best” offers: Some sellers and their agents feel that asking for everyone’s best and final offer creates more competition and potentially yields a higher price. They may also worry that an escalation clause limits their negotiating power or that the proof requirement creates extra work.

When to Use an Escalation Clause

Knowing when to use an escalation clause can help you win your dream home. However, before using this approach, consider whether you’re in a buyer’s vs. seller’s market, as escalation clauses perform best when sellers have the upper hand.

Escalation clauses work best in competitive markets with low inventory and high demand. When homes receive multiple offers within hours of listing, this strategy gives you a fighting chance. If you’re trying to win a bidding war on a house and inventory remains tight, an escalation clause helps you stay competitive without constantly revising your offer.

Certain property types attract more competition and therefore benefit more from escalation clauses. For example:

- Move-in ready homes in popular neighborhoods: These tend to spark bidding wars, especially if they’re priced competitively and require minimal work.

- Starter homes and first-time buyer properties: Homes in the sweet spot for first-time buyers often see multiple offers due to high demand and limited supply in this price range.

- Unique or highly desirable properties: Houses in prime locations, properties with rare features, or homes in exceptional condition attract enough competition to make escalation clauses a smart strategy.

Keep in mind that not every buyer should use an escalation clause, but these profiles tend to benefit most:

- Buyers with flexibility in their budget: If you have some financial cushion and can handle potential appraisal gaps, escalation clauses give you room to compete.

- Motivated buyers on a timeline: Maybe you’re relocating for work or need to close quickly. In these cases, escalation clauses can speed up the process by reducing back-and-forth negotiations.

- Risk-tolerant buyers: If you’re comfortable revealing your maximum price in exchange for a competitive advantage, this strategy aligns with your approach.

- Well-financed buyers: Those with strong pre-approvals, significant down payments, or access to non-qualified mortgages that offer more flexibility can better absorb the risks that come with escalation clauses.

When to Avoid an Escalation Clause

Even though escalation clauses can be helpful for buyers, there are situations where they don’t make sense or could actually hurt your chances. Here’s when to skip this strategy:

- Slow or balanced markets: If homes are sitting on the market for weeks and you’re not seeing multiple offers, an escalation clause is overkill and reveals information you’d be better off keeping private.

- Homes priced above market value: If comparable sales suggest the property is already overpriced, adding an escalation clause could push you even further above what the home is worth, creating problems at appraisal.

- When appraisal gaps are likely: In markets where sale prices routinely exceed appraised values, escalation clauses amplify your risk of getting stuck with a gap you’ll need to cover in cash.

- If buyer finances are tight: When you’re stretching to afford the home and don’t have extra funds to cover potential appraisal shortfalls or higher closing costs, the risks of an escalation clause outweigh the benefits.

Final Thoughts

An escalation clause in real estate can give you an edge in competitive markets when used strategically. Whether you’re buying in a hot market or considering all your options, knowing what strategies are available to you can help you make the best decision.

Ready to experience the benefits of owning a home? At Griffin Funding, we can help you get pre-approved and find the right financing to make your offer competitive in any housing market. Download the Griffin Gold app to track your financial readiness and get personalized insights as you prepare for homeownership.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Are escalation clauses legally binding?

Do sellers have to accept an escalation clause?

Can sellers counter an escalation clause?

The escalation clause is simply one component of your offer, and like any other term, it’s negotiable until both parties reach an agreement.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...