How to Refinance a Non-QM Loan

KEY TAKEAWAYS

- You can refinance a non-QM loan to a new non-QM loan or a traditional mortgage.

- Non-QM refinance options include rate-and-term and cash-out refinancing.

- Common borrowers include self-employed individuals, investors, and applicants with credit challenges.

- Griffin Funding specializes in non-QM refinance solutions tailored to meet the unique needs of borrowers.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformNon-qualified mortgage (non-QM) loans offer flexible alternatives for borrowers who may not meet traditional loan standards. But what happens when you want to refinance a non-QM loan? Whether you’re looking to lower your rate, access equity, or shift to a conforming product, refinancing a non-QM loan can open new doors, as long as you know how to navigate the process.

In this guide, we’ll cover everything you need to know, from what a non-QM loan is to how to complete a non-QM refinance in five steps.

KEY TAKEAWAYS

- You can refinance a non-QM loan to a new non-QM loan or a traditional mortgage.

- Non-QM refinance options include rate-and-term and cash-out refinancing.

- Common borrowers include self-employed individuals, investors, and applicants with credit challenges.

- Griffin Funding specializes in non-QM refinance solutions tailored to meet the unique needs of borrowers.

What Is a Non-QM Loan?

A non-qualified mortgage (non-QM) loan is a type of mortgage that does not meet the Consumer Financial Protection Bureau’s criteria for a “qualified mortgage.” Qualified mortgages typically follow strict guidelines regarding debt-to-income ratios, documentation, and income verification.

In contrast, non-QM loans offer more flexible underwriting standards and are tailored for borrowers who may not qualify for conventional loans.

Common non-QM loan types include bank statement loans, which use 12–24 months of deposits instead of tax returns; asset-based loans, which qualify based on liquid assets; and DSCR loans, which rely on rental income rather than personal income.

Can You Refinance a Non-QM Loan?

Yes, you absolutely can refinance a non-QM loan. Despite some common misconceptions, borrowers with non-qualified mortgage (non-QM) loans are not locked into their original loan terms forever. In fact, refinancing a non-QM loan is not only possible, but it can also be a strategic financial move, depending on your circumstances.

Eligibility for a non-QM refinance typically depends on your current credit profile, the type of non-QM loan you have, and your long-term financial goals. These types of loans often come with lower interest rates and more favorable terms, potentially saving you thousands over the life of the loan.

There are several scenarios where refinancing makes sense. If interest rates have dropped significantly since your original loan, refinancing could lower your monthly payment and total interest paid. If your income documentation has become more conventional — for example if you switched from self-employment to a salaried position — you may now be eligible for a traditional QM loan.

It’s important to note that mortgage rates fluctuate based on several economic factors, including inflation, employment data, Federal Reserve policies, and market demand for mortgage-backed securities. Understanding these factors that affect mortgage rates can help you time your refinance for the best financial outcome.

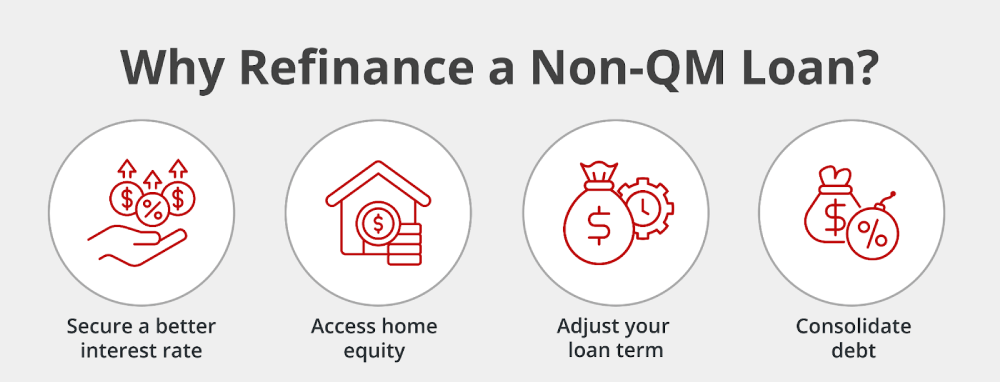

Why Refinance a Non-QM Loan?

One of the most compelling is the opportunity to secure a lower interest rate. If market conditions have shifted since you took out your original loan, or if your credit score has improved, you may qualify for more favorable terms that could significantly reduce your monthly mortgage payments and total interest paid over time.

Another key reason to refinance is the potential to transition into a conforming loan. Many borrowers initially choose a non-QM loan because they don’t meet the strict criteria required for conventional financing.

However, if your financial profile has since strengthened — for example, your income is now documented more traditionally, your debt-to-income ratio has improved, or past credit issues have been resolved — you might now be eligible for a QM loan. These loans typically come with lower interest rates, stronger protections, and more predictable terms.

For those looking to tap into their home equity, a non-QM cash-out refinance can provide quick access to funds. Homeowners can use this liquidity for home improvements, debt consolidation, or even new investment opportunities. Since non-QM lenders assess financial strength differently, this option is ideal for self-employed individuals, investors, or those with non-traditional income sources.

Ultimately, refinancing a non-QM loan is about aligning your mortgage with your current financial goals. Whether you’re seeking to save money, simplify your loan structure, or unlock the value of your home, the flexibility of non-QM refinance options, especially with lenders like Griffin Funding, can help you take the next step with confidence.

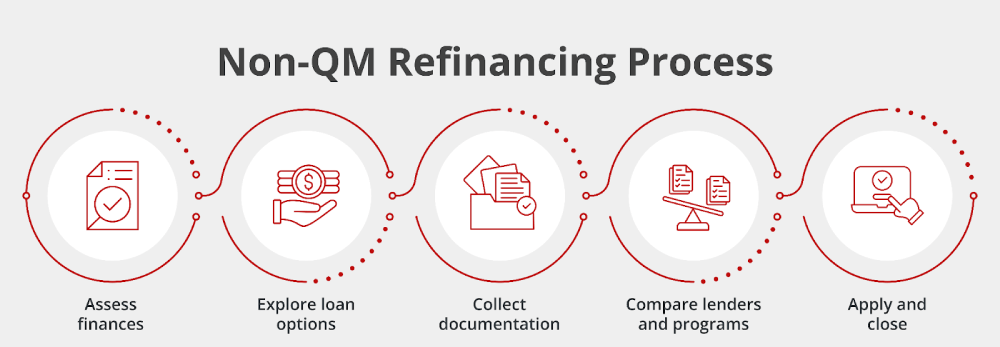

How to Refinance a Non-QM Loan in 5 Steps

Refinancing a non-QM loan may sound intimidating, but it’s manageable when broken down into clear steps. Here’s how to successfully refinance your non-QM loan from start to finish:

- Evaluate your current loan and finances: Start by reviewing your current mortgage terms closely. Review your existing interest rate and how much you still owe on the loan. Consider your monthly mortgage payment and the remaining time on the loan term. It’s also important to assess your current financial health, especially your credit score and debt-to-income (DTI) ratio. This foundational information will help you determine if refinancing is worthwhile and what kind of loan options you may qualify for.

- Explore your refinance options: Once you’ve evaluated your loan, explore your refinancing options. You may choose to refinance into another non-QM loan if you still don’t meet qualified mortgage (QM) standards. This option is ideal for borrowers with complex income streams or less-than-perfect credit. Alternatively, if your financial profile has improved, you might qualify for a QM or conforming loan with more favorable terms. Evaluating both options allows you to make a smart financial decision tailored to your current needs. You can compare offerings through our mortgage refinance limits.

- Gather documentation: Non-QM refinancing typically requires detailed documentation to verify your income, assets, and property details. Prepare to submit recent bank statements (usually 12–24 months), documentation of assets or alternative income (depending on your loan type), and property-related documents such as an appraisal report, homeowners insurance, and property tax information. The more organized and complete your paperwork is, the smoother your refinance will go.

- Compare lenders and loan programs: Not all lenders are equipped to handle non-QM loans, so you should work with a lender experienced in this space. Griffin Funding specializes in non-QM refinance solutions and offers flexible underwriting that caters to self-employed individuals, investors, and other non-traditional borrowers. Comparing different lenders and programs ensures that you receive competitive rates and the right loan structure for your unique situation.

- Apply and close: Once you’ve selected your lender and loan program, it’s time to apply and move through the closing process. Expect a custom underwriting experience that may differ from traditional mortgages, often requiring a more thorough review of your financial documents. Closing timelines for non-QM refinances typically mirror standard loans, ranging from 30 to 45 days.

Tips for a Smooth Non-QM Refinance Process

Whether you’re trying to lower your rate or get a non-QM cash-out refinance, keep these tips in mind to ensure the process goes smoothly:

- Work with an experienced lender: Non-QM loans require specialized underwriting.

- Improve your financial profile: Pay down debt and check your credit before applying.

- Get your documents ready: Be prepared with a detailed financial picture.

- Set realistic expectations: Non-QM refinancing may take slightly longer, but it’s well worth it.

Explore Your Non-QM Refinancing Options Today

Start exploring your options with mortgage refinance solutions. Refinancing a non-QM loan doesn’t have to be complicated. Whether you’re looking for better rates, improved loan terms, or access to cash, Griffin Funding can help you make a move that supports your financial goals.

Our team is here to guide you through the refinance process step by step, providing solutions tailored to your specific needs. This includes resources like the Griffin Gold app, which offers easy-to-use financial management tools, mortgage calculators, and private home search capabilities.

Ready to get started on your mortgage journey? Reach out online and take the first step towards homeownership.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Who should consider a non-QM refinance?

Borrowers who don’t fit into the traditional lending mold should strongly consider a non-QM refinance. This includes business owners, gig economy workers, and individuals with unconventional income streams or limited income documentation. Real estate investors who qualify based on rental income rather than personal income are also prime candidates.

In addition, borrowers who have experienced recent credit events such as foreclosures, bankruptcies, or late payments may find that refinancing into another non-QM loan offers better terms than their original loan.

What is a non-QM cash-out refinance?

A non-QM cash-out refinance enables borrowers to leverage the equity in their homes without sticking to the strict criteria of traditional mortgage products.

This type of refinance is ideal for individuals who don’t qualify for conventional loans due to irregular income, self-employment, or other non-traditional financial situations. With a non-QM cash-out refinance, you can replace your existing mortgage with a larger one and receive the difference in cash, which you can use for a wide variety of financial goals.

Why choose Griffin Funding for a non-QM refinance?

Griffin Funding is a leading expert in non-QM refinancing and stands out for its personalized approach and industry knowledge. We understand that every borrower’s situation is unique, which is why we offer a wide range of non-QM products tailored to various income types, asset structures, and credit profiles.

Our team works closely with you to evaluate your financial goals and recommend the best refinancing option, whether it’s staying within the non-QM space or transitioning to a qualified mortgage.

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...