How to Get Rid of PMI

KEY TAKEAWAYS

- You can request PMI removal once you reach 20% equity, or wait for automatic cancellation at 22% equity.

- Rising home values may qualify you for early PMI removal through a new appraisal, even if you haven’t paid down much principal.

- Making extra principal payments or refinancing when rates are favorable can help you eliminate PMI years faster than scheduled.

- FHA mortgage insurance cannot be removed without refinancing, unlike conventional PMI, which offers multiple removal options.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformPrivate mortgage insurance (PMI) can potentially add hundreds of dollars to your monthly home loan payment. If you put down less than 20% when you bought your home, you’re likely paying PMI right now. The good news is that PMI doesn’t last forever, and you have several options to eliminate this expense once you’ve built enough equity.

Keep reading to learn how to get rid of PMI and start saving money each month.

What Is PMI and Why Do Lenders Require It?

Private mortgage insurance is a monthly fee added to your mortgage payment when your loan-to-value ratio (LTV) exceeds 80%. Your LTV is simply the percentage of your home’s value that you’re borrowing. Lenders require PMI on conventional loans with down payments lower than 20% because these borrowers represent a higher risk.

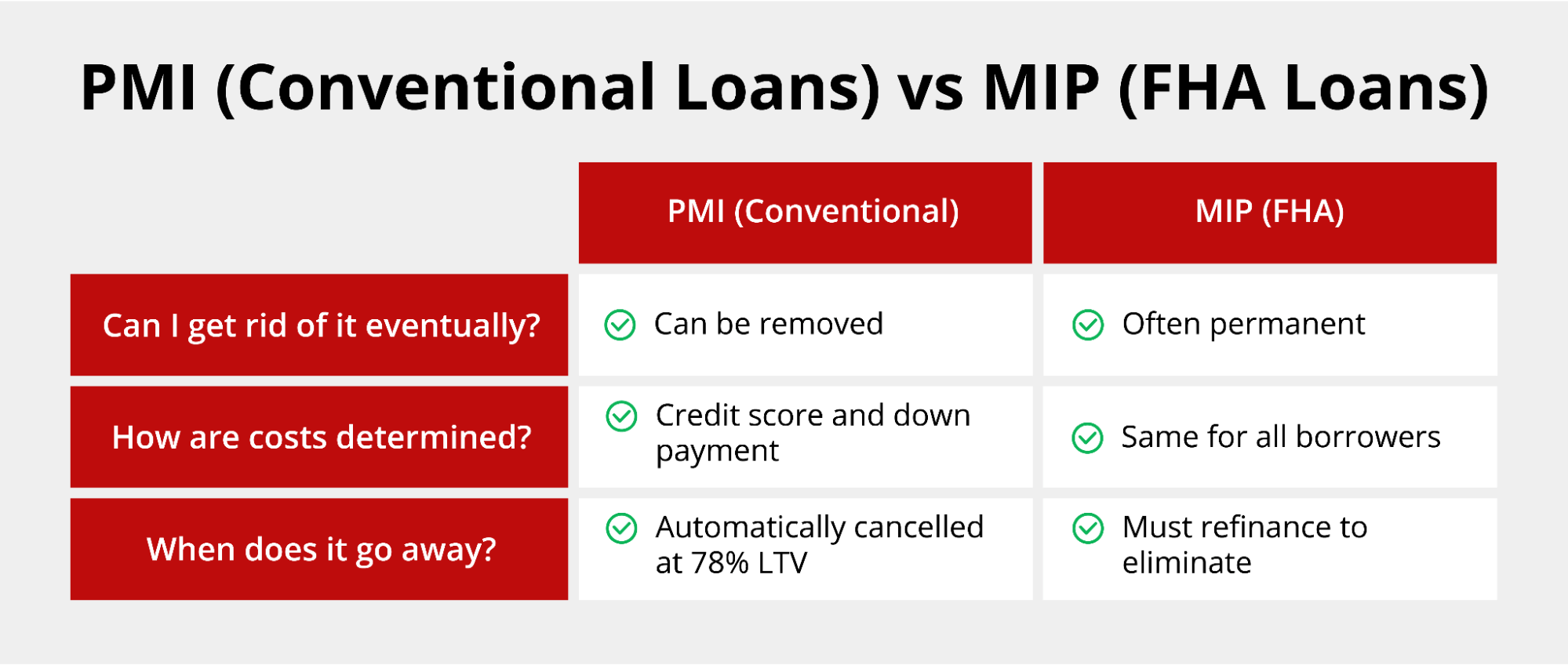

PMI only applies to conventional loans. There’s no PMI on VA loans, though veterans do pay a one-time funding fee instead. Meanwhile, FHA loans use a mortgage insurance premium (MIP) rather than PMI, which works differently and is harder to remove. Additionally, non-qualified mortgages typically don’t come with a PMI requirement.

PMI protects the lender, not the borrower. You pay the premium, but the insurance company compensates the lender if you default.

Average PMI costs can range from 0.5% to 1.5% of your loan amount annually. Lenders then calculate PMI by multiplying your loan amount by that rate and dividing it by twelve. On a $300,000 mortgage, that’s $125 to $375 monthly. Learning how to get rid of PMI should be a priority once you’re eligible.

Use our down payment calculator to see how different down payments affect your purchasing power and monthly costs. Remember, putting down less than 20% means you’ll pay PMI until you build enough equity.

How PMI Works on Different Types of Mortgages

Understanding how PMI applies to your specific loan type helps you plan the right removal strategy.

Conventional Loans and PMI

Again, PMI only applies to conventional loans, but only if a borrower makes a down payment of less than 20% of the property’s purchase price. You’ll encounter two types:

- Borrower-paid PMI: You pay a monthly premium that can be canceled once you meet equity requirements.

- Lender-paid PMI: Your lender covers the insurance cost in exchange for a slightly higher interest rate that stays for the life of your loan unless you refinance.

FHA Loans and Mortgage Insurance

FHA loans require mortgage insurance premiums (MIPs) regardless of your down payment size. All FHA borrowers pay both an upfront MIP of 1.75% of the loan amount at closing and an annual MIP that’s divided into monthly payments.

FHA loans require mortgage insurance premiums (MIPs) regardless of your down payment size. All FHA borrowers pay both an upfront MIP of 1.75% of the loan amount at closing and an annual MIP that’s divided into monthly payments.

The removal rules depend on your down payment. If you put down less than 10%, MIP stays for the entire life of your loan. If you put down 10% or more, the lender can remove MIP after 11 years of regular payments.

The main difference between PMI vs. MIP is that MIP cannot be removed early through home appreciation or equity building. The only way to eliminate MIP before the 11-year mark or if you made a down payment of less than 10% is to refinance into a conventional loan.

How to Get Rid of PMI on a Mortgage

You have multiple paths to PMI removal, and the best option depends on your financial situation and timeline. Your options for removing PMI include:

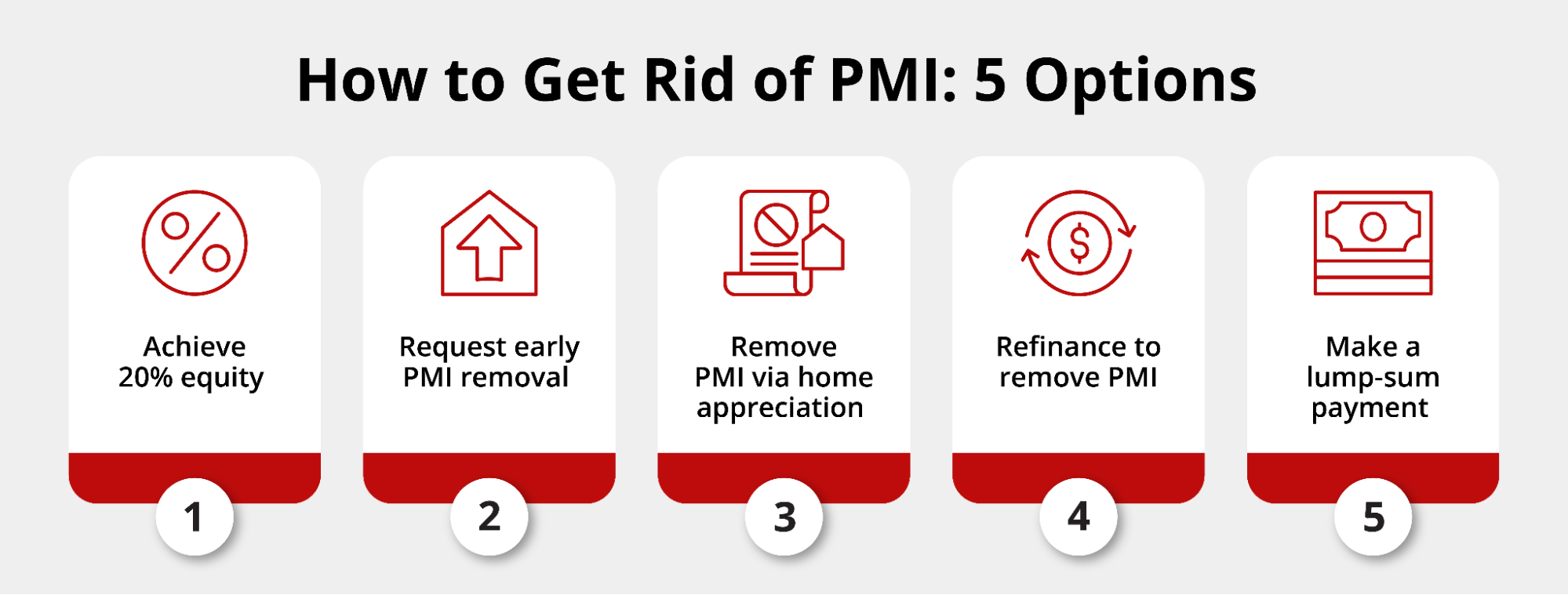

1. Reach 20% Equity Through Mortgage Payments

1. Reach 20% Equity Through Mortgage Payments

Federal law under the Homeowners Protection Act of 1998 requires lenders to automatically cancel PMI when your loan balance reaches 78% of the property’s original purchase price. This happens without any action on your part as long as you’re current on your payments.

You can also request PMI removal once you hit 80% loan-to-value ratio. The Homeowners Protection Act PMI cancellation rights give you legal backing to remove insurance once you’ve met equity thresholds, though lenders can add conditions like good payment history.

2. Request PMI Removal Early

You don’t have to wait for automatic PMI cancellation. Once you’ve built 20% equity in your home based on the purchase price, you can ask your lender how to get PMI removed. This means your remaining loan balance needs to be at or below 80% of what you originally paid for the property.

Contact your servicer in writing to start the process. Here’s what lenders typically require:

- Payment history verification: You’ll need a solid track record with no late payments in the past 12 months. Most lenders may not approve PMI removal if you’ve had any 30-day late payments recently.

- Current loan balance confirmation: Your lender verifies that your remaining mortgage balance is at or below 80% of the original property value using either the sales price or appraised value from the purchase.

- Seasoning requirements: Many lenders impose waiting periods, typically requiring at least two years of payments before considering early PMI removal requests, though some accept removal after just 12 months.

3. Use Home Appreciation to Remove PMI

Rising home values create equity without extra principal payments. If your neighborhood has seen significant appreciation, ordering a new appraisal can prove you’ve crossed the 20% equity threshold.

Lender requirements for appraisal-based PMI removal vary, but most follow similar guidelines. You’ll pay for the appraisal yourself. The property must be in good condition, and some lenders require a minimum payment period, often 24 months, before considering appreciation-based removal.

4. Refinance to Eliminate PMI

Refinancing into a new loan can eliminate PMI if you’ve built enough equity through home appreciation or principal paydown. Refinance your mortgage when your home value has increased enough to put you above 20% equity (80% LTV). When comparing a home loan refinance vs. a new appraisal to remove PMI, consider what each option offers.

A refinance replaces your entire loan with a new mortgage. You’ll pay closing costs, but you also get the chance to secure a lower interest rate if rates have dropped since you bought your home. This means you can eliminate PMI and potentially reduce your monthly payment through a better rate.

5. Make a Lump-Sum Principal Payment

Paying down your mortgage principal to remove PMI faster gives you control over the timeline. If you get a bonus, tax refund, inheritance, or other windfall, applying it directly to your mortgage principal can push you past the 80% LTV threshold.

Calculate exactly how much you need to reach 80% LTV, then make a single large payment. For example, if you owe $240,000 on a home worth $300,000, you’re at 80% LTV and eligible for PMI removal. If you owe $250,000, you’d need to pay down $10,000 to hit that threshold.

This strategy works best when you’re close to the 20% equity mark and have cash available that isn’t needed for emergencies or higher-interest debt. If you’re carrying credit card balances at 18% or 20%, pay those off first since the interest savings will exceed what you’d save on PMI. But if your only other debts are low-interest car loans or student loans, eliminating PMI immediately can free up hundreds of dollars monthly.

How Long Does It Take to Get PMI Removed?

The timeline to get PMI removed varies based on which method you choose and how quickly you build equity. Automatic cancellation happens when your loan balance is 78% of the original value through scheduled payments. For a 30-year mortgage with 5% down, this typically takes 10 to 11 years. Requesting PMI removal at 80% LTV speeds up the timeline by about a year.

Several factors affect how quickly you can remove PMI:

- Loan-to-value ratio: Your starting down payment determines how much equity you need to build. A 5% down payment requires more time to reach 20% equity than a 10% or 15% down payment.

- Home value changes: Markets with strong appreciation help you build equity faster through rising property values, while stagnant markets slow the process.

- Extra principal payments: Additional payments beyond your required monthly amount directly reduce your loan balance and accelerate equity growth.

PMI Removal Rules to Know

Federal and lender-specific rules govern when and how you can cancel private mortgage insurance. A few rules to know are:

- Federal PMI cancellation laws: The Homeowners Protection Act requires automatic PMI termination when your loan balance reaches 78% of the original property value. You have the right to request removal at 80% LTV if you’re current on payments.

- Lender-specific overlays: Some lenders require a minimum number of payments before considering PMI removal requests or mandate specific payment history standards.

- Seasoning and appraisal requirements: Lenders commonly require a 12-to-24-month waiting period before accepting PMI removal requests based on appreciation. When you need an appraisal, expect to pay for it yourself.

Common Mistakes That Delay PMI Removal

Borrowers often make avoidable errors that postpone PMI cancellation. These mistakes include:

- Assuming PMI drops automatically at 20%: PMI doesn’t automatically drop when you hit 20% equity. You must request removal at 80% LTV or wait until 78% LTV for automatic cancellation.

- Confusing FHA MIP with PMI: FHA mortgage insurance follows different rules and generally can’t be removed without refinancing. Many borrowers assume their FHA MIP will drop like conventional PMI.

- Not tracking home value increases: Failing to track your home’s value means you might miss opportunities to request early PMI removal when appreciation pushes you past 20% equity.

- Missing lender communication: Delayed responses to lender notices about PMI cancellation eligibility can extend the timeline and keep you paying unnecessary premiums.

Explore PMI Removal Options

At Griffin Funding, we help homeowners eliminate PMI and reduce their monthly mortgage costs. Whether you’ve built equity through regular payments, benefited from home appreciation, or want to explore refinancing options, our loan experts can guide you through the PMI removal process.

We also offer no PMI mortgage programs for borrowers who want to avoid this expense from the start. Track your mortgage payments and monitor your equity growth through the Griffin Gold app to stay on top of your PMI removal timeline.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can you remove PMI without refinancing?

What’s the fastest way to get rid of PMI?

- Making a large lump-sum principal payment can immediately push you past the 20% equity threshold if you’re close.

- If your home has appreciated significantly, requesting a new appraisal to prove current value might qualify you for removal faster than waiting for principal paydown.

- Refinancing works quickly when rates are favorable and you’ve gained enough equity through appreciation.

Can PMI be removed if my home value has increased?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...