How Many Times Can You Refinance a House?

KEY TAKEAWAYS

- No legal limit exists on how many times you can refinance your home, but practical considerations like closing costs, credit requirements, and waiting periods come into play.

- Each refinance requires sufficient home equity, typically at least 20% for conventional loans to avoid PMI.

- The financial benefits of refinancing should outweigh the costs—generally, look for interest rate drops of at least 0.5-1%.

- Different loan types (FHA, VA, conventional) have specific waiting periods between refinances that you must consider.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformRefinancing your home can provide financial benefits like lower interest rates, reduced monthly payments, or access to equity. But how many times can you actually refinance a house? The answer might surprise you. Explore the possibilities and limitations of refinancing multiple times so you make informed decisions about your mortgage.

KEY TAKEAWAYS

- No legal limit exists on how many times you can refinance your home, but practical considerations like closing costs, credit requirements, and waiting periods come into play.

- Each refinance requires sufficient home equity, typically at least 20% for conventional loans to avoid PMI.

- The financial benefits of refinancing should outweigh the costs—generally, look for interest rate drops of at least 0.5-1%.

- Different loan types (FHA, VA, conventional) have specific waiting periods between refinances that you must consider.

What Does It Mean to Refinance a House?

Refinancing a house involves replacing your existing mortgage with a new loan, typically with different terms that better suit your current financial needs. The new mortgage pays off the original loan, and you begin making payments on the new one.

Three main types of refinancing options exist:

- Rate-and-term refinance: With this option you change your interest rate, loan term, or both, while keeping the loan balance essentially the same. The rate-and-term refinance works well if you want to reduce your interest rate or change from a 30-year to a 20-year or 15-year mortgage.

- Cash-out refinance: You borrow more than you owe on your current mortgage and receive the difference in cash. Many homeowners choose this option to refinance for home improvements, consolidate high-interest debt, or fund major expenses like education.

- Streamline refinance: Available for FHA loans and VA loans, these simplified refinances require less documentation and sometimes no appraisal, making the process faster and less expensive.

Homeowners choose to refinance for various reasons, including:

- Taking advantage of lower interest rates

- Reducing monthly payments

- Shortening the loan term to pay off the mortgage faster

- Converting between adjustable and fixed-rate mortgages

- Tapping into home equity for major expenses

- Removing a co-borrower from the mortgage

Is There a Limit to How Many Times You Can Refinance a House?

The short answer: No, there is no legal limit to how many times you can refinance your home. You could theoretically refinance multiple times throughout your homeownership journey. However, several considerations limit how often you can refinance your home.

While no federal law restricts how many times you can refinance a house, individual lenders often establish their own guidelines. Most lenders require a “seasoning period,” or a waiting time between refinances (typically ranging from six months to two years). These policies help protect both you and the lender from the financial strain of continuous refinancing.

Different loan types have specific requirements regarding how often you can refinance:

- Conventional loans: Most lenders require a six-month waiting period between refinances, though some may make exceptions for rate-and-term refinances.

- FHA loans: FHA guidelines mandate a 210-day waiting period (about seven months) from your current loan’s first payment date before you can refinance again. Some FHA streamline refinances may have different requirements.

- VA loans: VA loans require a minimum of 210 days after the first payment on your current mortgage and six consecutive payments made before refinancing through the VA Interest Rate Reduction Refinance Loan (IRRRL) program.

Factors That Affect Your Ability to Refinance Multiple Times

Your ability to refinance multiple times depends on several factors beyond just waiting periods. Understanding these elements helps you determine if and when you can refinance your home again.

- Home equity: You typically need at least 20% equity for a conventional refinance to avoid private mortgage insurance (PMI). Cash-out refinances usually require more equity (often 20-30%). Market value fluctuations directly impact your available equity.

- Credit score and financial profile: Most lenders require a minimum credit score of 620 for conventional refinances, but higher scores (740+) qualify you for the best interest rates. Your debt-to-income ratio generally needs to be below 43%. Stable employment and income history reassure lenders of your ability to repay.

- Interest rates and market conditions: Market fluctuations determine available interest rates, so the gap between your current rate and new rates affects potential savings. Economic conditions might influence lender requirements and loan availability.

- Closing costs and fees: Each refinance incurs closing costs (typically 2-5% of the loan amount). The cost to refinance includes application fees, origination fees, appraisal fees, and title insurance. Frequent refinancing creates multiple sets of closing costs that affect your overall savings.

- Loan-to-value ratio (LTV): Most conventional refinances require an LTV of 80% or less. Higher LTVs may still qualify but typically require mortgage insurance. FHA loans allow higher LTVs (up to 97.75% for rate-and-term refinances).

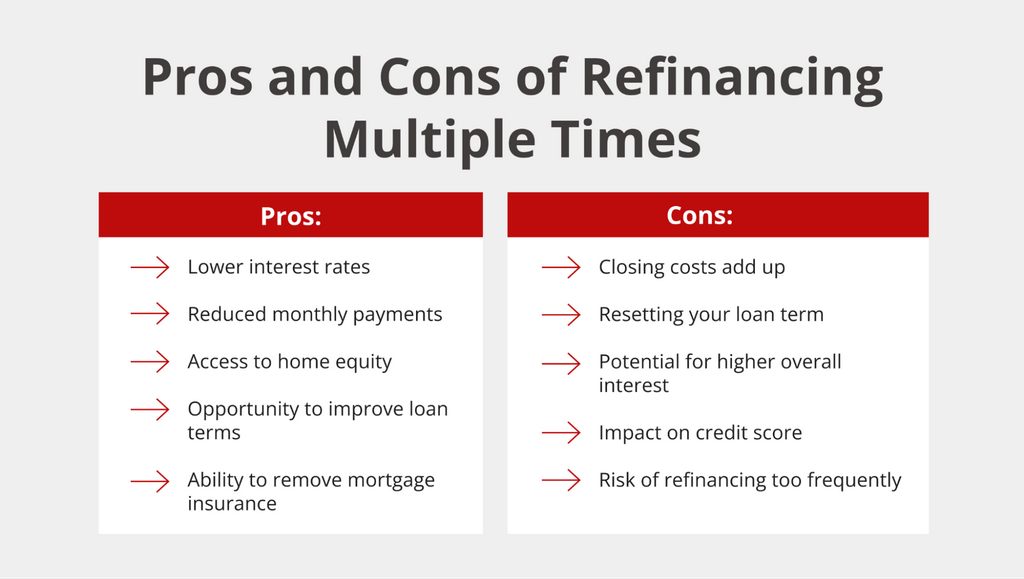

Pros and Cons of Refinancing Multiple Times

Before deciding to refinance your home again, carefully weigh these advantages and disadvantages:

Pros of refinancing multiple times:

- Lower interest rates: Securing a lower rate can significantly reduce your monthly payments and the total cost of your loan over time.

- Reduced monthly payments: Refinancing can make your mortgage more affordable through lower rates or extended terms, freeing up cash for other financial goals.

- Access to home equity: Cash-out refinancing allows you to tap into your home’s equity for major expenses without taking out separate, higher-interest loans.

- Opportunity to improve loan terms: You can switch from an adjustable-rate to a fixed-rate mortgage for more stability, or change your loan term to better align with your financial goals.

- Ability to remove mortgage insurance: If you’ve reached 20% equity, refinancing can eliminate private mortgage insurance requirements.

Cons of refinancing multiple times:

- Closing costs add up: Each refinance requires paying closing costs, which can total thousands of dollars and diminish your overall savings.

- Resetting your loan term: Starting a new 30-year mortgage means extending the time until you’re mortgage-free, potentially increasing the total interest paid over the life of the loan.

- Potential for higher overall interest: Even with a lower rate, extending your repayment timeline might result in paying more interest in total.

- Impact on credit score: Each refinance application creates a hard inquiry on your credit report, potentially lowering your score temporarily.

- Risk of refinancing too frequently: Refinancing before recouping closing costs from your previous refinance can result in a net financial loss.

When Does It Make Sense to Refinance Again?

Knowing when to refinance can save you thousands of dollars over the life of your loan. The fundamental rule of thumb: The savings from your refinance should outweigh the costs. Before pursuing any mortgage refinance solutions, calculate whether the financial benefits justify the expenses involved. Here are the situations that typically justify refinancing your home again:

- Significant interest rate drops: The traditional rule of thumb suggests refinancing when rates drop at least 1-2 percentage points below your current rate. However, even a 0.5% reduction might make financial sense if you plan to stay in your home for several years. Calculate your break-even point (when your monthly savings exceed your closing costs) to determine if refinancing makes sense for you.

- Improved credit score: If your credit score has increased significantly since your last mortgage, you might qualify for much better interest rates now. Many borrowers initially purchase homes with less-than-perfect credit and can benefit from refinancing once their credit improves. A jump of 50-100 points in your credit score could translate to savings of 0.5-1% on your interest rate.

- Changing from adjustable to fixed-rate: If you have an adjustable-rate mortgage (ARM) approaching its adjustment period, refinancing to a fixed-rate loan can protect you from potential rate increases. This strategy provides payment stability and peace of mind, especially in rising rate environments.

- Need for cash from equity: When you need funds for major expenses, a cash-out refinance allows you to borrow against your home equity. This option works well when you’ve built substantial equity and need capital for home improvements, debt consolidation, education costs, or other significant expenses.

- Removing a co-borrower: Major life changes like divorce or separation might necessitate refinancing to remove someone from the mortgage. While this refinance type isn’t primarily financially motivated, it’s often necessary for legal and practical reasons.

Find Out If Refinancing Is Right for You

Determining how many times you can refinance your home ultimately comes down to your unique financial situation. While no legal limit exists on refinance frequency, practical considerations like costs, equity, and waiting periods play crucial roles in the decision.

Griffin Funding can help you navigate the refinancing process with personalized guidance tailored to your specific needs. Our experienced loan officers will analyze your current mortgage, financial goals, and market conditions to determine if refinancing makes sense for you. Plus, take advantage of our Griffin Gold app to plan for homeownership, access affordability calculators, and track your home’s value over time.

Contact Griffin Funding today to explore your refinancing options and take the next step toward achieving your financial goals.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...