Crypto-Backed Mortgages: What They Are & How They Work

KEY TAKEAWAYS

- Cryptocurrency mortgages use your digital assets as collateral rather than requiring you to sell them for cash for your down payment or outright home purchase.

- This approach allows crypto holders to maintain their investment positions while accessing funds for real estate purchases.

- Crypto mortgage lending comes with unique risks, including volatility concerns and limited lender availability.

- Cryptocurrency asset depletion mortgages allow you to use your crypto as income rather than your tax returns to qualify for the monthly payments.

- Only certain lenders offer these loans, making research and due diligence essential before proceeding.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformThe rise of cryptocurrency has opened up new financial opportunities, including innovative mortgage solutions. Crypto-backed mortgages allow homebuyers to leverage their digital assets without selling them, creating an alternative path to homeownership. This financing option is appealing to crypto investors who want to access the housing market while keeping their cryptocurrency portfolios intact.

What Is a Crypto-Backed Mortgage?

A crypto mortgage is a home loan that uses cryptocurrency as collateral instead of following traditional lending practices. Unlike conventional mortgages that rely heavily on income verification and credit history, these loans focus on the value of your digital asset holdings. This approach has gained traction as cryptocurrency adoption has expanded beyond early adopters into mainstream investment portfolios.

The key difference from standard home loans is how you access funds. Rather than liquidating your Bitcoin, Ethereum, or other cryptocurrencies to generate a down payment, you pledge these assets to secure the loan. This cryptocurrency mortgage approach appeals to investors who believe their digital holdings will appreciate over time and don’t want to trigger taxable events by selling. Many crypto investors have watched their portfolios grow significantly and prefer to maintain their positions rather than convert to cash.

Traditional mortgage underwriting focuses on employment history, debt-to-income ratios, and credit scores as primary qualification factors. Crypto-backed mortgages shift this emphasis toward collateral value and the borrower’s ability to maintain adequate cryptocurrency reserves throughout the loan term. This difference makes these loans accessible to entrepreneurs, freelancers, and others whose income streams don’t fit conventional lending criteria but who have built substantial cryptocurrency wealth.

How Do Crypto Mortgages Work?

The crypto mortgage process is similar to the traditional mortgage process, but there are a few differences. Learning the steps can help you prepare for what can be a complex but rewarding experience.

Once you’ve chosen a lender and found a property to purchase, the steps to get a crypto mortgage typically are:

- Collateralize your crypto: Pledge your cryptocurrency as security for the loan and transfer it to the lender’s secure custody solution upon preliminary approval.

- Get final approval: Complete detailed financial verification while lenders assess your crypto collateral value, volatility risk, and overall loan qualification based on their specific criteria.

- Loan funding and home purchase: Receive traditional fiat currency to complete your real estate transaction while your cryptocurrency remains securely held as collateral throughout the loan term.

Crypto mortgage lenders employ sophisticated security measures to protect digital asset collateral throughout the loan period. Most partner with institutional custody providers who specialize in securing large cryptocurrency holdings using bank-level security protocols.

Lenders continuously monitor collateral values using real-time market data feeds to track portfolio performance. When cryptocurrencies fluctuate significantly, automated systems calculate whether additional collateral is needed to maintain required loan-to-value ratios. This ongoing monitoring protects both lender and borrower interests by ensuring adequate collateral coverage.

Key Benefits of Crypto Mortgage Lending

These specialized loans offer several advantages for qualified borrowers:

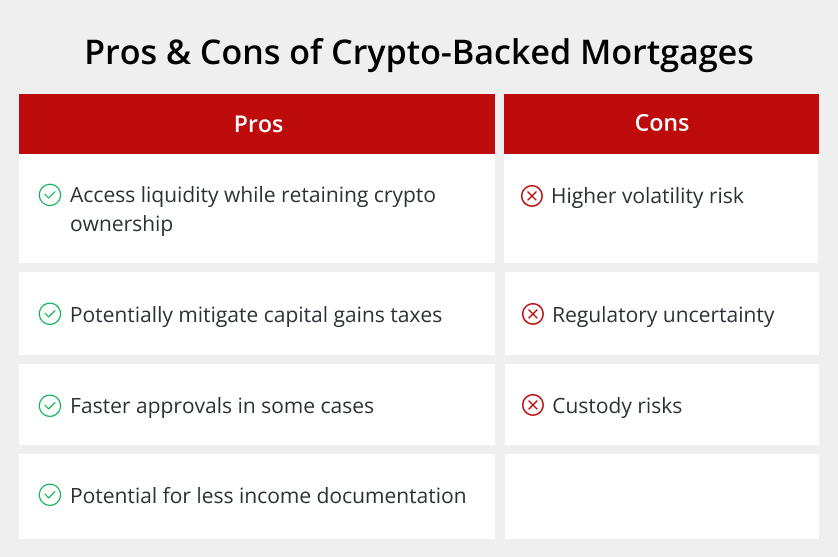

- Enables borrowers to retain ownership of their crypto while accessing liquidity: You keep your cryptocurrency investments while accessing their value for real estate purchases, allowing continued participation in potential market gains.

- Potential tax advantages by avoiding capital gains from crypto liquidation: Avoiding crypto sales eliminates immediate capital gains tax obligations that could significantly reduce your available funds for home buying. However, keep in mind that you may have to sell your crypto to secure the loan, and thus would still pay capital gains taxes. Speak with a tax advisor and consult with your lender for information regarding your unique situation.

- Faster approvals and fewer income documentation requirements in some cases: Rather than complex income verification, some crypto mortgage lenders offer streamlined processing with reduced paperwork since collateral value is the primary consideration.

- Non-QM asset depletion crypto loans do not require you to pledge your crypto as collateral. The only time you need to pledge your crypto and transfer it to a third-party custodian wallet is if you are using it as collateral for your down payment or full home purchase without a mortgage.

Risks and Challenges

As you navigate the mortgage process and housing market, keep in mind that crypto-backed mortgages come with important risks that borrowers should consider before proceeding. These include:

- Volatility exposure: Cryptocurrency price swings can trigger margin calls (demands for additional collateral) or forced liquidation if collateral values fall below required thresholds, potentially at unfavorable market conditions.

- Regulatory uncertainty: The constantly changing regulations for digital assets create potential complications for both borrowers and lenders in this space.

- Custody risks: Transferring cryptocurrency to third-party control introduces counterparty risk, meaning you depend on the lender or custody provider’s financial stability and security practices to protect your assets.

Who Can Benefit From a Crypto-Backed Mortgage?

Crypto-backed mortgages work best for specific borrower types, including:

- Crypto investors with substantial digital assets and limited cash flow: These individuals often have significant wealth tied up in cryptocurrency but struggle to qualify for traditional mortgages due to income documentation challenges or irregular earnings from freelancing, consulting, or business ownership.

- Tech-savvy homebuyers looking to diversify real estate holdings without liquidating crypto: Rather than selling appreciating digital assets, they can leverage them for property investments while maintaining their cryptocurrency exposure and potential for future gains.

- High-net-worth individuals seeking alternative lending strategies: This demographic often has complex financial situations where traditional lending doesn’t adequately serve their needs, using these loans for investment properties, second homes, or even primary residences when conventional financing is not an option.

How to Apply for a Crypto-Backed Mortgage

The application process for cryptocurrency mortgages consists of these simple steps:

- Choose lender: Research and select a crypto mortgage lender that accepts your cryptocurrency types and offers favorable terms, comparing loan-to-value ratios, interest rates, and custody arrangements.

- Transfer collateral: Move your cryptocurrency to the lender’s secure custody solution, completing any required account setups and verification procedures with their institutional storage partner.

- Underwriting: Submit financial documentation and undergo a credit evaluation while the lender assesses your crypto collateral value, portfolio stability, and overall loan qualification.

- Closing: Complete the final loan documentation, receive your funds, and proceed with your real estate purchase while your cryptocurrency remains securely held as collateral.

Before applying, understand that most lenders have specific qualification criteria you’ll need to meet, such as:

- Minimum crypto holdings: Requirements vary significantly between lenders, with most requiring substantial cryptocurrency portfolios to qualify for these specialized loans.

- Supported currencies: These typically include Bitcoin and Ethereum, with some lenders accepting alternatives, though options vary significantly between providers.

- Credit checks: These remain standard practice with minimum score requirements, though standards may be more flexible than traditional mortgages since cryptocurrency collateral provides primary loan security.

To ensure a smooth application process, organize comprehensive records showing your cryptocurrency acquisition history and current holdings across all wallets and exchanges before applying. Gather traditional financial documents, including tax returns and bank statements, as these are important for income verification.

Consider consolidating your crypto holdings into widely accepted currencies to improve lender compatibility. You can also work with financial and tax professionals familiar with crypto-backed lending to understand implications for your overall strategy and potential tax obligations.

Explore Cryptocurrency Mortgage Options

Crypto-backed mortgages are still fairly new, but they’re opening doors for investors who want to buy real estate without selling their digital assets. As more lenders get comfortable with cryptocurrency, we’ll likely see better terms and more options for borrowers.

Due diligence is still important when working with crypto mortgage lenders. Research their track record, custody practices, and margin call policies. The intersection of real estate and cryptocurrency creates unique considerations that require careful evaluation.

Before using your cryptocurrency for a mortgage, consult with financial professionals who understand both real estate and digital asset markets. They can help you assess whether this approach makes sense based on your investment goals and risk tolerance. You can also consider exploring alternative non-QM loans or investment property financing.

The newly passed Genius Act could pave the way in the future to allow for cryptocurrency assets to be used in traditional mortgage underwriting on conventional and government-backed loans.

Griffin Funding offers comprehensive mortgage solutions and financial planning tools to help you explore all your financing options. Use our home affordability calculator to understand your purchasing power, and consider downloading the Griffin Gold app for additional tools to support your real estate investment strategy.

Get started online today to find a mortgage that’s right for you.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

How do I find a crypto mortgage lender?

At Griffin Funding, we offer flexible mortgage solutions and stay current with emerging financing options to help borrowers explore all available paths to homeownership.

Do I have to pledge my crypto?

What is the difference between a crypto-backed mortgage and a crypto asset depletion mortgage?

Does FHA allow the use of cryptocurrency to get a mortgage?

Can I use crypto as collateral for a mortgage?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...