Conditional Approval: Meaning & Next Steps

KEY TAKEAWAYS

- Conditional approval means your mortgage application has been reviewed and will likely be approved once specific conditions are met.

- Conditional approval is an encouraging step in the home-buying process, but not a final approval.

- To move forward, you must satisfy all conditions, usually related to documentation or financial verification.

- Understanding the difference between pre-qualification, pre-approval, conditional approval, and final approval helps you navigate the mortgage process smoothly.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformBuying a home can be an exciting—but sometimes overwhelming—journey. One step that often brings relief and confusion in equal measure is getting conditionally approved for a mortgage. If you’ve received a notice from your lender stating you’ve been conditionally approved, you might be wondering what that really means and how close you are to getting the keys to your new home.

What Does Conditionally Approved Mean?

Being conditionally approved means your lender has reviewed your financial documents and believes you’re a strong candidate for the loan. However, certain conditions still need to be met before final approval is granted. These may include:

- Submitting additional documents

- Verifying assets

- Clarifying parts of your credit or employment history

Think of conditional approval as a green light following the mortgage pre-approval process, but with a few caveats. You’re mostly there, but you need to finish a bit more paperwork or clear up outstanding details.

Mortgage lenders use conditional approval to ensure everything checks out before committing fully to funding your home purchase. Conditional approval also signifies that a mortgage underwriter has thoroughly reviewed your application. Unlike a pre-approval, which may rely on estimates and self-reported data, conditional approval involves in-depth analysis of your credit report, income documentation, and other financial indicators.

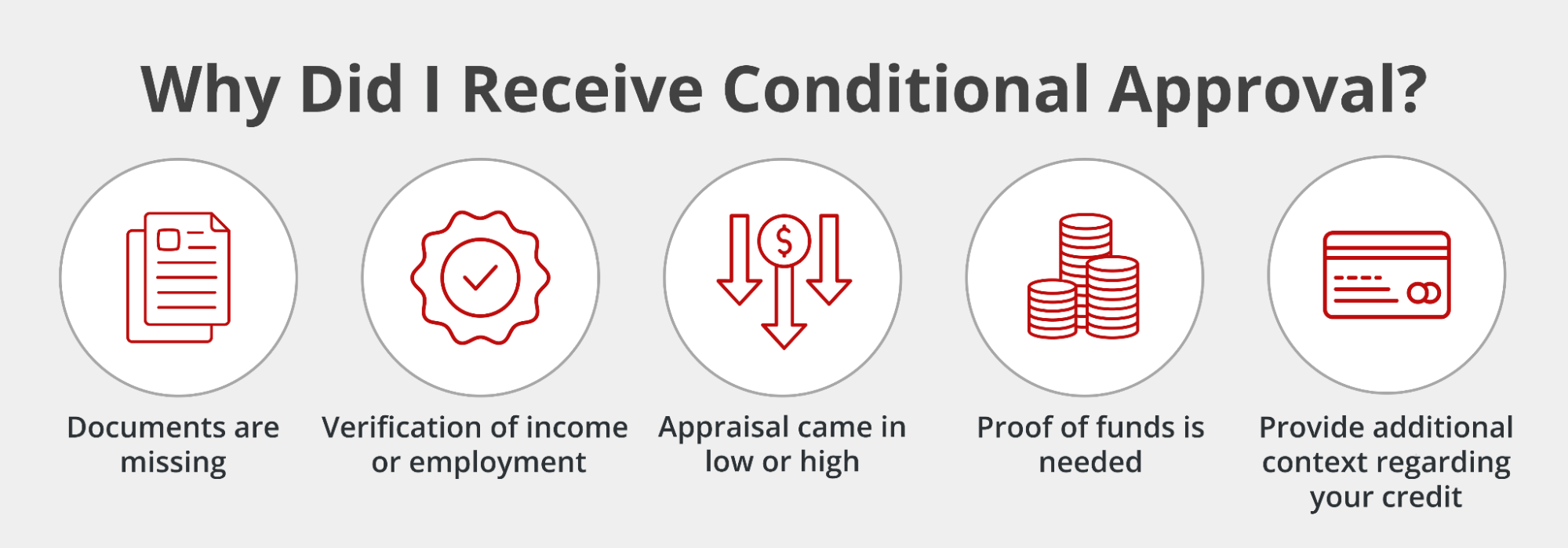

Common Reasons for Conditional Approval

Here are some common reasons why a mortgage might get conditionally approved rather than receiving final approval:

- Missing documents: A few forms or mortgage documents might still be needed, like tax returns, pay stubs, or bank statements.

- Verification of income or employment: Your lender might request a verbal or written verification from your employer as proof of income or employment.

- Appraisal issues: The home may need to be appraised at or above the purchase price. If the appraisal comes in low, this can affect your loan-to-value (LTV) ratio and even cause the lender to adjust or deny your loan.

- Proof of funds: The lender may ask for documentation showing you have enough money for the down payment and closing costs. This could be in the form of bank statements or a letter confirming liquid assets.

- Credit explanation: The lender may require a written explanation if there are recent changes or anomalies in your credit report. For example, if you opened a new line of credit or made a large purchase recently, the lender might need context.

Other common conditions may include clearing any outstanding judgments, proving the source of recent large deposits, or even showing updated homeowners insurance documentation. Every loan is different, so the specific conditions depend on your financial profile.

What Happens After Conditional Approval?

Once conditionally approved, the next step is simple: fulfill the lender’s conditions. That usually means submitting any outstanding paperwork and being available for follow-up questions.

Your mortgage underwriter will review all your documents again to ensure everything aligns with lending requirements. If everything checks out, you’ll move to what’s called clear to close, which means:

- The loan has final approval

- You’ll receive a closing disclosure

- A closing date will be set

- You’ll sign your mortgage documents

- You’ll get the keys to your new home!

This stage is often one of the most exciting and nerve-racking for buyers. It signals that you’re on the cusp of homeownership, but staying responsive and thorough is also critical. Any delays in documentation or lack of communication can stall the closing process.

Before closing, your lender may perform a final credit check and employment verification to make sure that your financial situation hasn’t changed since the initial application. Use a closing cost calculator to prepare for your final expenses and ensure you have sufficient funds available.

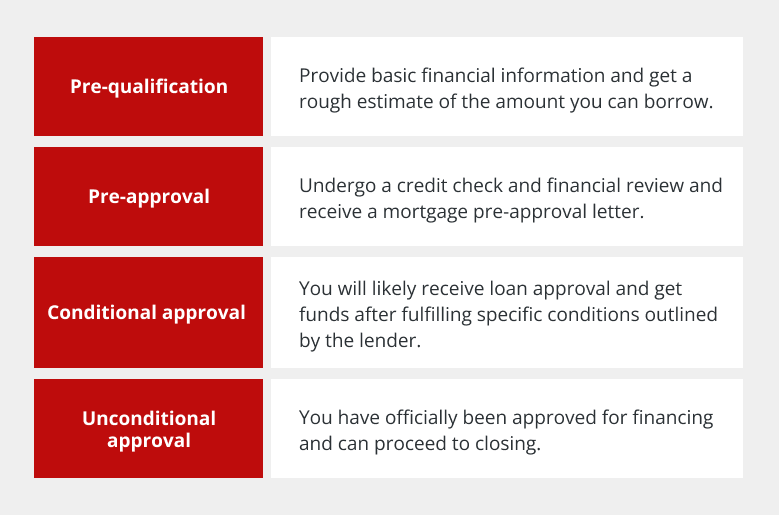

The Different Types of Mortgage Approvals

Understanding conditional approval in context helps to see where it fits within the broader mortgage approval timeline.

Pre-qualification

Pre-qualification is the earliest, most informal step in the mortgage process. You provide basic financial information to the lender, and they roughly estimate how much you can borrow. Here are the key characteristics:

- No credit pull is performed

- Not a binding commitment from the lender

- Helps you explore what types of loan products may be available

- Useful starting point for conversations about financing options

- Sellers and agents view it as a preliminary indicator rather than a firm commitment

- Helps set realistic expectations about how much home you can afford

Pre-approval

In the pre-approval stage, your credit is checked and financial documents are reviewed. This is a stronger signal of buying power and is often required before submitting an offer on a home.

Key features include:

- Pre-approval letters are typically valid for 60 to 90 days

- Gives you a defined window to shop for a home with confidence

- Your lender provides a pre-approval letter to include with offers

- Demonstrates your seriousness and financial readiness to sellers

- You can increase your mortgage pre-approval amount by reducing debt, increasing your down payment, or optimizing your credit score

Learn more about pre-approval vs pre-qualification to understand which stage you’re in.

Conditional approval

If you receive conditional approval, this means that a lender is largely satisfied with your loan application.

Here’s what the conditional approval stage typically involves:

- A mortgage underwriter has thoroughly reviewed your application and you’re close to the finish line

- You may need to provide more documentation or information before final sign-off

- Gives sellers and real estate agents confidence in your offer

- Makes you a more reliable buyer in competitive housing markets

- Involves in-depth analysis of your credit report, income documentation, and financial indicators

Unconditional approval

Unconditional approval is also known as formal approval, and this means that the lender has officially approved you for a mortgage. This is a huge milestone in the mortgage process because it indicates that you’ve secured financing. What happens at this stage:

- All that’s left is to close on the home and officially transfer ownership

- You’ll receive a closing disclosure with final loan terms

- The house title and earnest money will be handled during the closing process

- You’re ready to schedule your closing date and prepare for homeownership

Begin Your Home Buying Journey

Understanding conditional approval helps demystify one of the most important milestones in the mortgage process. You’ll be better positioned to take advantage of the many benefits of homeownership once you successfully navigate this stage.

Griffin Funding makes it easy to track your progress, submit documents, and confidently move toward final approval. The Griffin Gold app gives you 24/7 access to your loan status and financial management tools so that you can manage everything on the go.

If you’re ready to qualify for a mortgage, now is a great time to get started. Whether you’re a first-time home buyer or a seasoned investor, Griffin Funding provides various loan programs designed to meet your unique needs. Take the first steps toward getting pre-approved today!

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Is conditional approval a good sign?

Yes! Conditional approval is a very positive sign. It means the lender has already reviewed your application and believes you’re a good candidate for a mortgage. As long as you meet the remaining conditions, you're well on your way to securing the loan.

It also gives sellers and real estate agents confidence in your offer, especially in a competitive housing market. Conditional approval demonstrates that you’ve completed a substantial part of the underwriting process, making you a more reliable buyer than someone who’s only pre-approved.

Can you be denied after getting conditional approval?

Unfortunately, yes. The lender can revoke the approval if something changes in your financial situation, like job loss, increased debt, or significant credit issues. That’s why staying financially stable between conditional approval and closing is essential.

Lenders may also deny the loan if you fail to meet one or more of the conditions outlined in your approval letter. This could be as simple as missing paperwork or a delayed employment verification. Responding promptly and thoroughly to all lender requests is key.

How long does it take to close after getting conditional approval?

Typically, it can take a few days to a few weeks to close after conditional approval. The timeline depends on how quickly you can provide the requested documents and how complex your financial situation is. If everything goes smoothly, you could be clear to close within a week.

However, delays in appraisal reports, title searches, or document submission can extend this timeframe. Staying in regular contact with your lender and loan officer can help keep things on track and ensure you’re moving forward toward closing without unnecessary delays.

Some loans, such as VA loans or FHA loans, may take longer depending on the requirements. Your loan officer can give you a more accurate timeline based on your individual case.

Does conditional approval expire?

Your lender will then need to re-verify your employment, income, and creditworthiness through the underwriting process again. The timeline for your conditional approval home loan status can vary based on market conditions and lender workload, so staying in close communication with your loan officer helps ensure you complete all requirements before expiration.

Can I make an offer on a house with conditional approval?

Unlike buyers with only pre-qualification or pre-approval, you've had your financial documents thoroughly reviewed by an underwriter. This gives sellers confidence that your financing is more likely to go through, which can be especially valuable in competitive markets.

Does getting conditional approval lock in my interest rate?

Conditional approval means your loan has been reviewed and is likely to be approved once you meet specific conditions. You'll need to specifically request a rate lock from your lender, which typically protects your interest rate for 30 to 60 days while you complete the remaining conditions and move toward closing.

Talk to your loan officer about the best timing for your rate lock.

How will I know when my conditions are cleared?

What should I avoid doing after receiving conditional approval?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...