Bridge Loans

Finding your perfect new home is exciting — but what if you need to buy it before selling your current house? Bridge loans are designed for homeowners who want to buy a new house while waiting for their existing one to sell. These loans offer a simple solution to a common real estate problem.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformWhat Is a Bridge Loan?

A bridge loan, sometimes called a gap or swing loan, is a short-term loan you can use to invest in real estate or buy a new home while your current property is still on the market. These loans can be categorized as residential transition loans (RTL) or hard money loans, which typically last 6-12 months and use your current home’s equity as collateral.

This loan is a valuable tool for investors and those in need of quick financing. Bridge loans are faster to close and more flexible than traditional financing, making them perfect for time-sensitive real estate deals. Unlike traditional 30-year mortgages, a bridge loan mortgage is specifically designed to bridge the financial gap between buying and selling properties.

The main purpose of these loans is to give you more financial flexibility during the home-buying process. With a mortgage bridge loan, you can make an offer on a new home without waiting for your current property to sell. This can be helpful in competitive real estate markets where you need to act quickly to secure a property.

How Does a Bridge Loan Work?

Bridge loans work by leveraging the equity in your current home to finance your new home purchase. The process looks like this:

- Loan amount: Lenders typically offer up to 80% of your current home’s equity. For example, if your home is worth $500,000 with a $200,000 mortgage balance, you have $300,000 in equity. The lender might approve a bridge loan for up to $240,000. This money can be used as a down payment on your new home or to temporarily cover both properties.

- Repayment options: Bridge loans offer two main repayment structures — monthly until your current home sells or deferred payments where all interest is paid when your current home sells. Some lenders offer interest-only payment options during the bridge period to make monthly payments more manageable. Your choice will depend on your cash flow and how quickly you expect your current home to sell.

- Qualification requirements: Since you’ll temporarily hold two loans, lenders evaluate your ability to manage both your current mortgage and the bridge loan. This includes having sufficient income, a strong credit history, significant equity in your home, and a solid debt-to-income ratio. Lenders typically want to see at least 20% equity in your current home and a combined loan-to-value ratio of no more than 80%. Your credit requirements may also be higher than with traditional loans.

- Interest rates: Bridge loan rates are typically higher than conventional mortgage rates due to their short-term nature and increased lender risk. Rates are typically a few percentages above the prime rate, depending on your creditworthiness and market conditions. While these rates are higher, remember that you’ll only be paying them for a short period.

- Closing process: The bridge loan approval and closing process is often faster than traditional mortgages. Lenders understand the time-sensitive nature of these loans and can close faster. However, you’ll still need to provide documentation like income verification, home appraisal, and proof of assets.

Is a bridge loan right for you? Use the Griffin Gold app to explore your options and get personalized guidance.

Bridge Loan Use Cases

Bridge loans can be helpful for any number of situations. Here are the most common scenarios where they’re useful:

- Competitive market purchases: When housing inventory is limited, sellers often prefer buyers without home sale contingencies. A bridge loan lets you make stronger offers by removing this contingency, increasing your chances of securing your desired property.

- New construction timing: For buyers building a new home, construction timelines rarely align perfectly with selling their current property. Bridge loans provide the flexibility to manage both transactions effectively, especially when completion dates shift.

- Investment property acquisition: Real estate investors use bridge loans to quickly secure investment property loans when time-sensitive opportunities arise.

- Relocation requirements: Job transfers often require quick moves to new locations. Bridge loans let you purchase in your new area immediately while marketing your current home, eliminating the need for temporary housing.

Pros and Cons of Bridge Loans

Bridge loans are a great choice for anyone looking to purchase a new property while selling their existing one. However, you should weigh all aspects of this financial option.

Benefits of bridge loans include:

- Makes non-contingent offers possible, strengthening your position as a buyer: Sellers prefer offers without home sale contingencies because they’re more likely to close. Your offer becomes as strong as a cash buyer’s, giving you an edge.

- Provides time to sell your current home at the best possible price: Instead of rushing to sell before buying your new home, you can take time to properly stage and market your current property, which can lead to better offers and more profitable sales.

- Eliminates the need for temporary housing between properties: You won’t have to rent storage units, find short-term housing, or move twice. This saves both money and stress during your transition.

- Allows quick action on desirable properties: When you find the perfect home, you can make an offer immediately without waiting for your current home to sell. In hot markets, this speed can help you secure your dream home.

- Offers flexibility in timing between purchase and sale: You can close on your new home first and take time moving out of your current one. This flexibility lets you plan your move on your schedule rather than rushing to coordinate two closings.

However, like any loan, bridge loans also have some potential drawbacks to consider:

- Higher interest rates: Because these loans are short-term and riskier for lenders, you’ll have a higher interest rate than you would with a conventional mortgage.

- Requires qualifying for two loans simultaneously: You’ll need to prove you can handle two payments on both your current mortgage and the bridge loans.

- Additional closing costs and fees: Beyond the higher interest rate, you’ll pay closing costs on both your bridge loan and your new home’s mortgage.

- Short repayment terms create pressure to sell quickly: Most bridge loans must be repaid within 6-12 months. If your current home doesn’t sell during that timeframe, you might face some tough decisions about pricing or refinancing.

- Stricter qualification requirements: Lenders typically want to see excellent credit scores, significant equity in your current home, and strong income. Many also require your current home to be actively listed for sale before approval.

- Limited lender options as not all institutions offer bridge loans: You might need to shop around more to find a lender, and few options typically mean less negotiating power on rates and terms. You’ll want to decide if going with a residential transition loan from a private lender or a hard money loan.

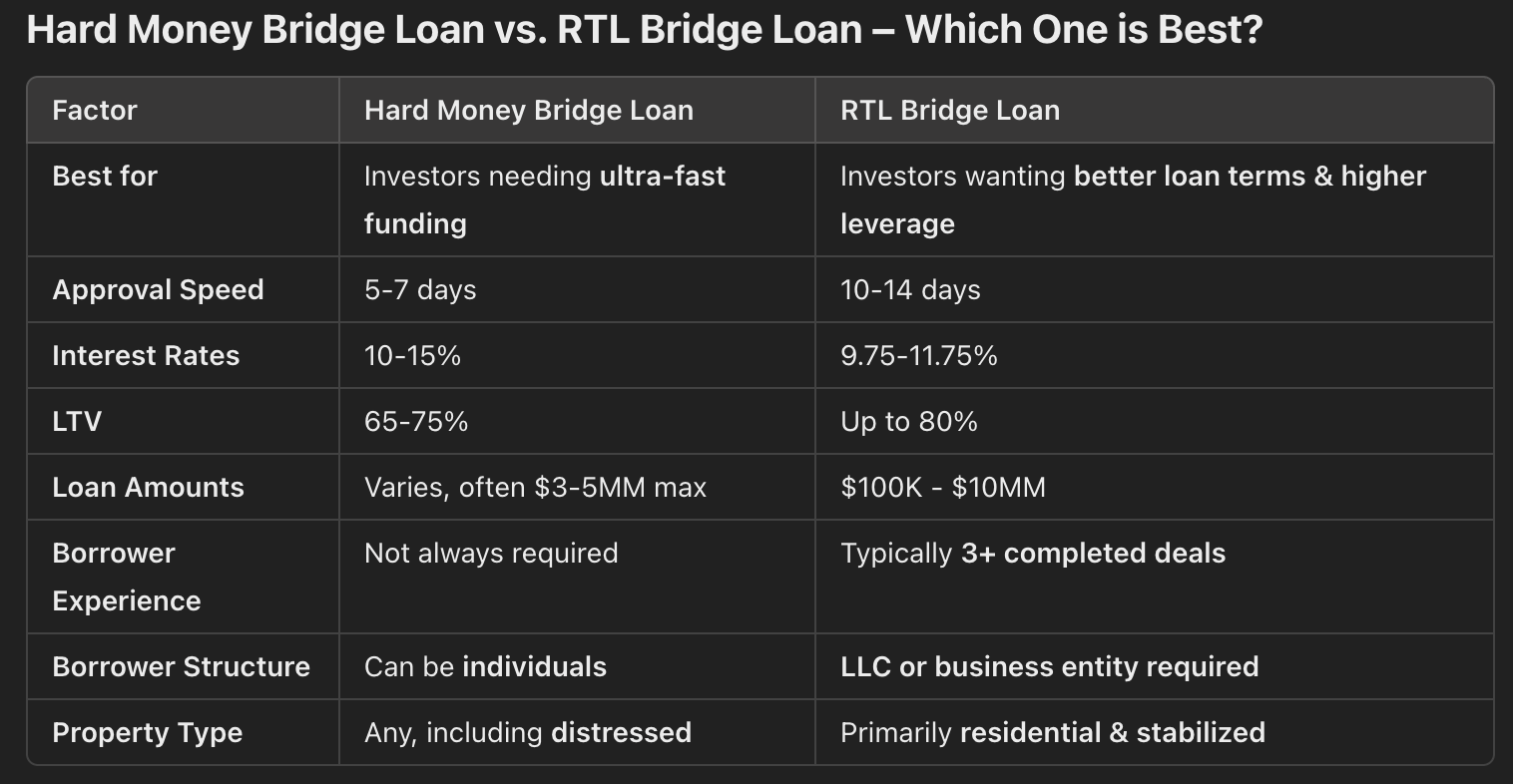

Bridge Loan: Hard Money vs. RTL – When to Choose Which?

Bridge Loans are both Hard Money Loans and Residential Transition Loans (RTL), so investors must decide which lender type—hard money or private money RTL financing—best suits their situation. While both options provide short-term capital for real estate investments, they differ in terms of borrower requirements, cost, and loan structure.

When to Use a Hard Money Lender for a Bridge Loan:

Hard money lenders are typically more flexible and focus on asset-based lending, meaning they prioritize the property’s value over the borrower’s financial background. Choose a hard money lender for a bridge loan when:

- You have low credit or limited experience – Hard money lenders often approve loans based on property value and potential, not credit scores or borrower experience.

- You need maximum speed and flexibility – Hard money loans can close in as little as 5-7 days, making them ideal for investors needing ultra-fast funding.

- The property is unconventional or distressed – Hard money lenders are often more willing to fund non-traditional properties (e.g., rural locations, mixed-use properties, non-warrantable condos).

- You don’t have strong financials or a business entity structure – RTL lenders typically require business entities (LLCs or corporations), while many hard money lenders allow individual borrowers.

- You need short-term financing but don’t meet traditional lender requirements – If you’ve been denied by banks or institutional RTL lenders, a hard money lender can be a great fallback option.

Downsides of Hard Money for a Bridge Loan:

- Higher interest rates (often 10-15% vs. 9.75-11.75% for RTLs).

- Lower loan-to-value (LTV) ratios (typically 65-75% LTV, while RTL bridge loans can go up to 80%).

- More expensive fees (hard money lenders may charge higher origination and servicing fees).

When to Use an RTL Lender for a Bridge Loan:

Residential Transition Loan (RTL) lenders operate more like institutional lenders and provide structured loan products tailored to experienced investors. Choose an RTL lender for a bridge loan when:

- You have real estate investment experience – Many RTL lenders require at least 3-5 completed transactions for higher leverage and better pricing.

- You want better loan terms – RTL lenders offer lower interest rates (9.75-11.75%), higher loan-to-cost (LTC) ratios, and potentially lower fees.

- Your investment is a straightforward real estate project – RTL lenders prefer stabilized residential properties, fix and flips, and multifamily investments in strong markets.

- You plan to refinance into permanent financing – RTL bridge loans often transition more smoothly into long-term financing (e.g., DSCR loans or agency-backed loans).

- You need higher leverage – RTL lenders can provide up to 80% LTV and 90% of purchase price, whereas hard money bridge loans typically offer less leverage.

Downsides of RTL Lenders for a Bridge Loan:

- More structured underwriting – RTL lenders may require entity formation (LLC, S-Corp, etc.), stronger financials, and borrower experience.

- Longer approval process – While RTL loans are faster than traditional bank loans, they often take 10-14 days to close, compared to 5-7 days with a hard money lender.

- Stricter property criteria – RTL lenders focus on stabilized or transition-ready properties, while hard money lenders fund distressed or unconventional assets.

Bottom Line: Which Should You Choose?

Bottom Line: Which Should You Choose?

- Go with a Hard Money Bridge Loan if: You need fast, flexible funding, have lower credit or experience, or are purchasing an unconventional or distressed property.

- Go with an RTL Bridge Loan if: You want better rates, higher leverage, and structured financing, and you have a strong track record of real estate investing.

Ultimately, both bridge loan types serve the same purpose—providing short-term capital for real estate investors—but the right choice depends on your experience, property type, and financing goals.

Explore Your Bridge Loan Mortgage Options

A bridge loan can be the best solution when you’ve found your dream home but haven’t sold your current property yet. This flexible financing option lets you make strong offers, avoid temporary housing, and take control of your moving timeline. Whether you’re exploring conventional loans or non-QM loans, a bridge loan is often a strategic choice for making your next move happen smoothly.

Ready to learn more? Our experienced lending team will help you understand how a bridge loan can work for your specific situation and guide you through the simple preapproval process. Get started today!