Who Pays Closing Costs?

KEY TAKEAWAYS

- Buyers typically pay 2% to 5% of the purchase price in closing costs.

- Sellers usually pay 6% to 10%, largely due to agent commissions.

- Your loan type determines specific rules about seller contribution limits and allowable fees.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformClosing costs are a significant expense in any real estate transaction, but the financial responsibility doesn’t fall on just one party. Both buyers and sellers face fees when a home changes hands. The specific amount each party pays depends on several factors, including local customs, loan type, market conditions, and negotiation.

What Are Closing Costs?

Closing costs refer to all the fees and expenses you pay to finalize a real estate transaction. These costs are due on closing day and the typical range falls between 2% and 5% of the home’s purchase price, though this percentage varies based on location, property value, and loan type.

Buyers and sellers have different closing costs. Buyers primarily handle loan-related fees and prepaid expenses like property taxes and insurance. Sellers typically cover real estate agent commissions, transfer taxes, and various administrative fees.

Use a closing cost calculator for home purchase to help you estimate numbers more precisely.

Who Covers Closing Costs in a Real Estate Transaction?

Traditionally, buyers handle financing-related expenses, while sellers pay transfer-related fees. Local and regional customs influence these payment responsibilities. For example, California sellers often pay for owner’s title insurance, while Texas buyers usually handle this expense.

Market conditions play a role too. Strong seller’s markets may shift more costs to buyers, while buyer’s markets often result in sellers accepting more financial responsibility.

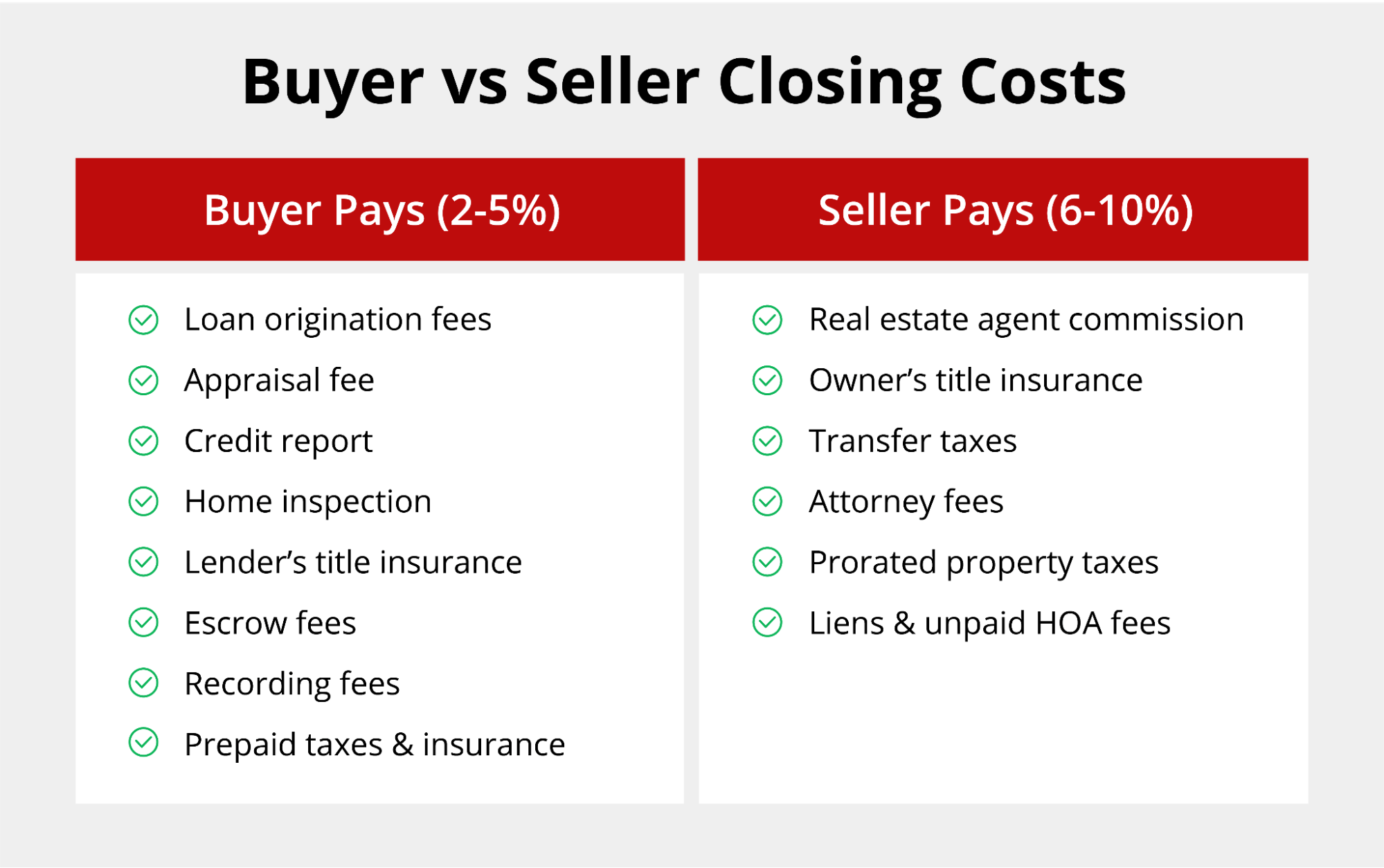

Closing Costs for Buyers

Closing Costs for Buyers

Common buyer closing costs include:

- Loan origination fees: Your lender charges this fee, typically 0.5% to 1% of the loan amount.

- Appraisal fee: A licensed appraiser assesses your property’s market value, costing between $300 and $600 for most residential properties.

- Credit report fee: Lenders typically charge $25 to $50 per report.

- Home inspection: Professional inspectors examine the property’s condition for $300 to $500.

- Title search and lender’s title insurance: Title companies research property ownership and provide insurance protecting your lender against title defects.

- Escrow fees: Escrow companies or attorneys facilitate the closing process and charge $500 to $2,000 based on property value.

- Recording fees: County offices charge $25 to $250 to record your deed and mortgage documents in public records.

- Prepaid items: You pay upfront for property taxes, homeowners insurance, and mortgage interest.

Buyers typically invest between 2% and 5% of the purchase price in closing costs. Your specific amount depends on your loan type, property location, lender fees, and the number of prepaid months required for your escrow account.

Traditional mortgages generally fall in the middle of the closing cost range, while non-qualified mortgages might carry higher origination fees due to specialized underwriting.

Closing Costs for Sellers

Seller costs usually include:

- Real estate agent commissions: Agent fees represent the largest seller expense, typically ranging from 5% to 6% of the sale price.

- Owner’s title insurance: This policy protects the buyer against title defects and costs 0.5% to 1% of the sale price in most states.

- Transfer taxes: State and local governments charge transfer taxes based on the sale price.

- Attorney fees: Some states require attorney representation at closing.

- Prorated property taxes: You pay property taxes through the closing date.

- Outstanding liens or HOA fees: You must satisfy any property liens, unpaid HOA fees, or special assessments.

Sellers typically pay between 6% and 10% of their home’s sale price in closing costs. However, high-transfer-tax states like New York or Washington add money to seller expenses.

Additionally, strong buyer’s markets may require you to offer concessions or pay additional buyer costs to attract offers. Seller’s markets, on the other hand, give you leverage to refuse these requests and negotiate lower commission rates.

Can the Seller Pay the Buyer’s Closing Costs?

Sellers can contribute toward buyer closing costs through seller concessions, which allows sellers to pay some or all of the buyer’s closing costs as part of the purchase agreement.

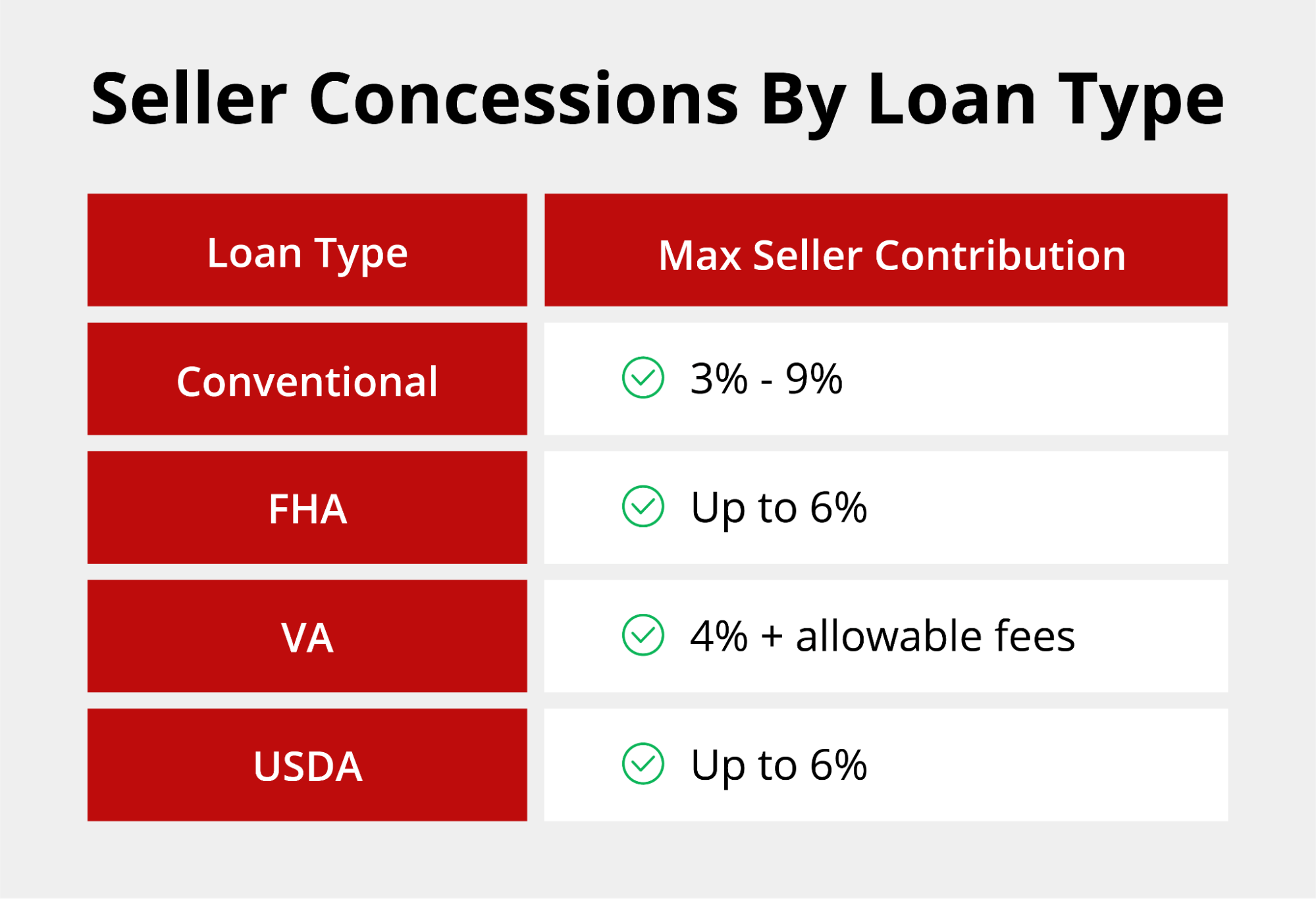

Loan programs impose specific limits on seller concessions:

- Conventional loans: 3% to 9% depending on down payment.

- FHA loans: Seller concessions cannot exceed 6% of the purchase price.

- VA loans: 4% of the purchase price plus payment of all normal closing costs and certain non-allowable fees.

Seller concessions benefit buyers by reducing their cash requirements at closing. However, sellers reduce their net proceeds from the sale. Buyers should verify that seller concessions don’t inflate the purchase price above fair market value, as appraisals must still support the inflated price.

Can the Buyer Cover the Seller’s Closing Costs?

Buyers rarely pay seller closing costs, but specific situations make this arrangement practical. Competitive markets sometimes require buyers to sweeten their offers beyond the purchase price. A buyer might agree to cover the seller’s title insurance or transfer taxes to make their offer more attractive than competing bids.

Additionally, buyers who negotiate a lower purchase price might agree to pay certain seller costs, offsetting the savings against their additional expenses. Properties requiring significant repairs could also see buyers covering seller costs in exchange for taking the home as-is. Your home affordability analysis should account for any non-traditional cost arrangements.

How Loan Type Affects Who Pays Closing Costs

Your mortgage program establishes specific rules about seller contributions and permissible fees. Each loan type restricts how much sellers can contribute toward buyer closing costs:

- Conventional Loans: Contribution limits are based on your down payment percentage, ranging from 3% to 9% of the purchase price.

- FHA Loans: The FHA caps seller concessions at 6% of the purchase price and permits contributions toward closing costs, prepaid expenses, and discount points.

- VA Loans: The VA allows 4% seller contributions plus unlimited payment of certain fees like the VA funding fee.

- USDA Loans: The USDA permits sellers to pay up to 6% of the purchase price toward buyer closing costs for properties in eligible rural areas.

Different loan programs prohibit certain fees from appearing in closing costs:

- Conventional Loans: Lenders cannot charge application fees to obtain rate locks, and buyers cannot pay real estate commissions.

- FHA Loans: The FHA restricts certain fees and requires lenders to waive or reduce costs in specific circumstances, protecting buyers from excessive charges.

- VA Loans: VA loan closing costs prohibit veterans from paying certain fees entirely, including attorney fees for title work and some portions of escrow and processing fees.

- USDA Loans: The USDA restricts buyers from paying some fees and requires specific cost distributions between buyers and sellers.

Tips for Reducing Closing Costs

Some closing cost reduction strategies for buyers include:

- Lender credits: Negotiate with your lender to accept a slightly higher interest rate in exchange for credits that cover some or all of your closing costs.

- Seller concessions: Request seller contributions toward your closing costs during purchase negotiations.

- Comparing lender fees: Shop multiple lenders and compare their Loan Estimate forms line by line.

- Timing your closing: Schedule your closing near the end of the month to reduce prepaid interest charges.

Closing cost reduction strategies for sellers include:

- Negotiating commission: Real estate commission rates are negotiable, and some agents accept lower percentages for quick sales or valuable properties.

- Understanding local transfer taxes: Research your local transfer tax requirements, as some jurisdictions offer exemptions or reduced rates for specific property types or transaction circumstances.

Understand How Closing Costs Are Split

The division of closing costs between buyers and sellers follows customary practices that vary by location and loan type. These expenses represent a significant financial consideration for both parties.

Griffin Funding provides transparent mortgage solutions that help you navigate these costs with confidence. The Griffin Gold app also offers smart budgeting tools, mortgage planning assistance, and financial management features to help you prepare for homeownership.

Take control of your home financing journey and get started with Griffin Funding today.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Do buyers or sellers usually pay more in closing costs?

Can closing costs be negotiated?

Can closing costs be rolled into a mortgage?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...