What Is Fannie Mae HomePath?

KEY TAKEAWAYS

- Fannie Mae HomePath properties are foreclosed homes owned and sold by Fannie Mae after the original borrower defaults on their mortgage.

- The First Look Initiative gives owner-occupants priority access to HomePath properties for an initial period before investors can bid.

- HomePath homes are sold as-is, meaning buyers should conduct thorough inspections and budget for potential repairs or renovations.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformFannie Mae HomePath is a platform that sells real estate owned (REO) properties acquired through foreclosure, offering buyers the chance to purchase homes at competitive prices. The program prioritizes owner-occupants through the First Look Initiative and aims to stabilize communities by returning foreclosed homes to the market.

Understanding Fannie Mae and the HomePath Program

Fannie Mae plays an important role in the housing market by purchasing and guaranteeing mortgages from lenders. The HomePath program serves as a way to manage and resell properties that Fannie Mae acquired through foreclosure.

What Is Fannie Mae?

Fannie Mae, officially known as the Federal National Mortgage Association, is a government-sponsored enterprise that was established to expand the secondary mortgage market. It buys mortgages from lenders, which frees up capital for those lenders to issue more loans. This process makes homeownership more accessible by keeping mortgage rates competitive and credit available.

Fannie Mae acquires properties through foreclosure after a borrower defaults on their mortgage payments. Once foreclosed, these REO properties become part of Fannie Mae’s inventory and are marketed for resale. The goal is to return these homes to the market quickly and efficiently while supporting local housing markets.

What Is the HomePath Program?

The HomePath program is Fannie Mae’s initiative to sell foreclosed properties directly to buyers. HomePath properties are REO homes that Fannie Mae owns and lists for sale through licensed real estate agents and online platforms.

Ultimately, HomePath helps Fannie Mae recover some losses from defaulted mortgages while also stabilizing communities. The program aims to maintain neighborhood property values by encouraging owner-occupants to purchase these homes first.

What Is a Fannie Mae HomePath Property?

What Is a Fannie Mae HomePath Property?

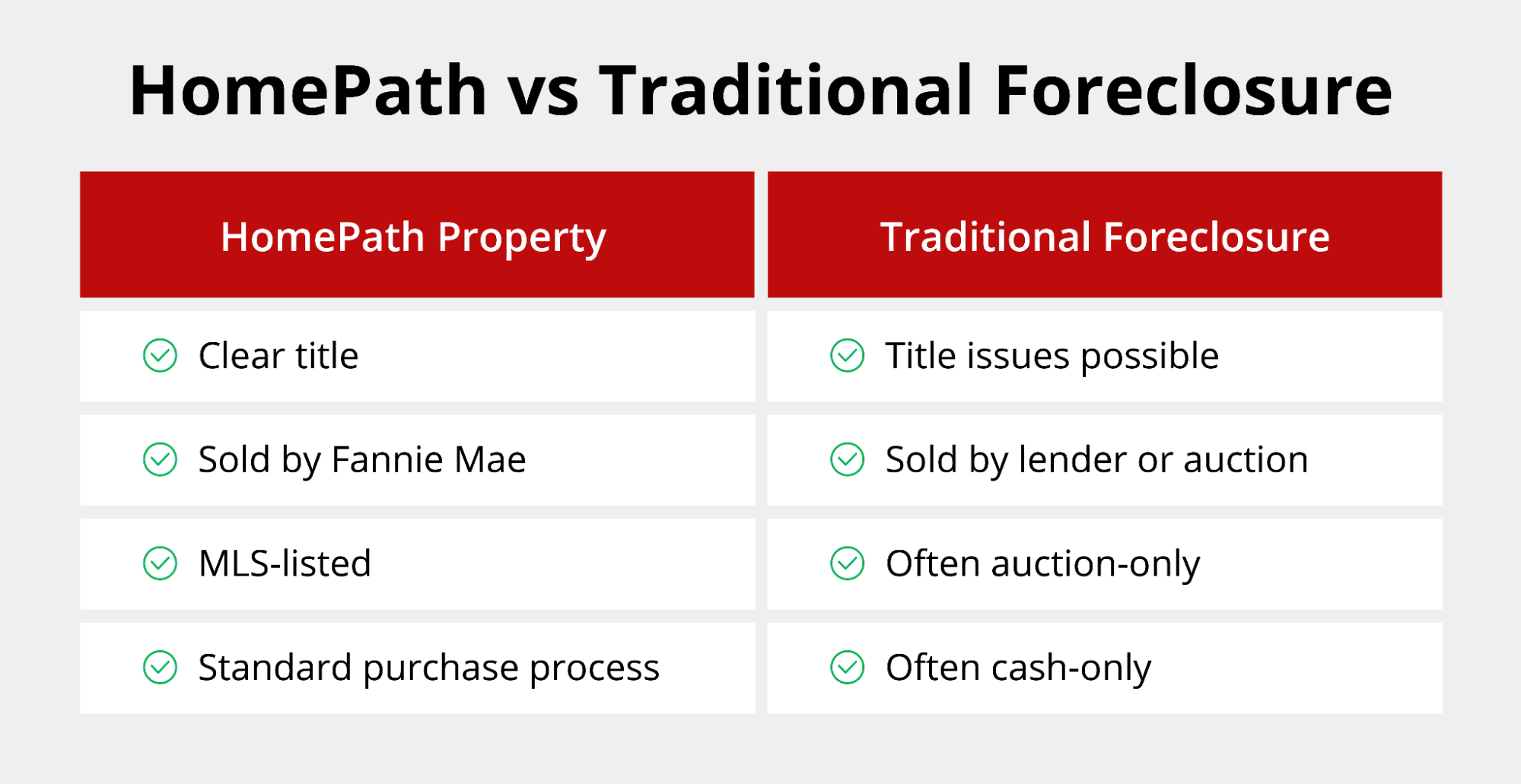

A Fannie Mae HomePath property is a foreclosed home that Fannie Mae has taken ownership of after the borrower failed to make mortgage payments. These properties differ from traditional foreclosures because they are bank-owned and ready for immediate purchase without going through an auction process.

HomePath properties are sold as-is, meaning Fannie Mae does not make repairs before listing them for sale. Buyers take on the responsibility of any necessary renovations or updates.

The types of properties available through HomePath include:

- Single-family homes: Detached houses suitable for families and individuals.

- Condos: Attached units in multi-unit buildings with shared amenities.

- Townhomes: Multi-level properties that share walls with neighboring units.

- Multifamily properties: Buildings with two or more units, available in limited cases for investors.

How the HomePath Buying Process Works

Purchasing a HomePath property follows a structured process designed to give priority to buyers who will use the home as their primary residence.

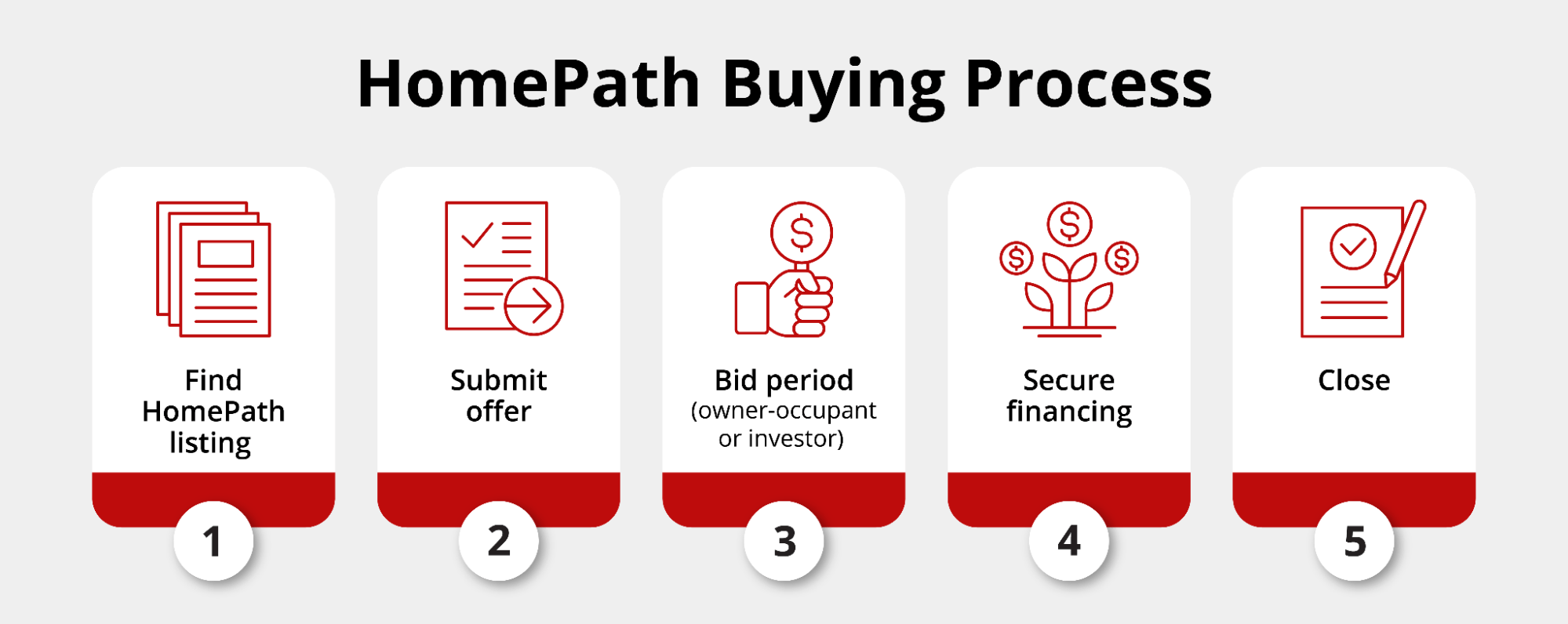

1. Finding HomePath Properties

1. Finding HomePath Properties

HomePath properties are listed through multiple channels. Buyers can search for available homes through the Multiple Listing Service (MLS), where licensed real estate agents have access to property details. Fannie Mae also has dedicated search tools through the HomePath website that allow buyers to browse listings directly.

Real estate agents who specialize in REO properties can provide guidance throughout the search process as well. These professionals understand the unique aspects of buying bank-owned homes and can help buyers identify properties that meet their criteria.

2. Making an Offer on a HomePath Property

HomePath properties are subject to distinct bidding periods. The First Look Initiative gives owner-occupants who plan to live in the property time to submit offers before investors can participate. This period typically lasts 20 to 30 days after the property lists on the MLS, though the duration can vary by state.

During the First Look period, only buyers who intend to occupy the home as their primary residence can make offers. This helps ensure that families and individuals have a fair chance to purchase homes without competing against investors. After the First Look period expires, the property becomes available to all buyers.

3. Financing a HomePath Home

Buyers can use various mortgage options to finance HomePath properties. Traditional mortgages like conventional loans, FHA loans, and VA loans are all acceptable financing methods. Some properties may even qualify for renovation financing, such as a home renovation loan. Properties needing extensive repairs may require non-qualified mortgages or alternative loan products.

Benefits of Buying a Fannie Mae HomePath Property

Potential advantages of HomePath properties include:

- Competitive pricing: HomePath properties are often priced below market value to facilitate quick sales.

- Clear title: Fannie Mae ensures that all title issues are resolved before listing properties.

- No seller disclosure requirements: HomePath homes are sold without traditional seller disclosures, though buyers should still conduct thorough inspections. Note that state laws may also still require certain seller disclosures.

- Sometimes lower closing costs: Fannie Mae occasionally offers closing cost assistance or incentives, particularly for owner-occupants.

Ideal buyer profiles of a Fannie Mae HomePath property include:

- First-time buyers: Those entering the housing market who want affordable options and can handle some repairs or updates may find excellent value in HomePath properties.

- Move-up buyers: Families looking for more space or better locations can often find larger homes at prices below traditional market rates.

- Long-term investors: Real estate investors seeking rental properties benefit from the competitive pricing and acquisition process.

Risks of Buying a HomePath Property

HomePath properties come with unique challenges, such as:

- Homes sold as-is: Buyers accept the property in its current condition with no recourse for hidden defects discovered after purchase.

- Possible repair or renovation needs: Many HomePath properties require updates ranging from minor cosmetic improvements to major structural repairs.

- Inspection importance: Thorough professional inspections are critical to identify problems before closing.

- Financing challenges with distressed properties: Properties in poor condition may not qualify for conventional financing.

Proper budgeting for first-time buyers and experienced purchasers is important for any unexpected repairs. It’s necessary to understand the full scope of work before making an offer to avoid any financial surprises after closing.

Who Is Eligible to Buy a HomePath Property?

HomePath properties are available to a wide range of buyers, but certain restrictions affect who can purchase during specific timeframes. Eligibility is particularly important for those exploring first-time home buyer programs, as HomePath can complement other assistance programs.

Owner-occupants who plan to live in the property as their primary residence receive priority through the First Look Initiative. These buyers submit offers during the exclusive period when investors are not yet allowed to participate. Occupancy requirements apply to these buyers as they must intend to occupy the home as their primary residence for at least one year.

After the First Look period expires, the property becomes available to all buyers, including investors, buyers of second homes, and entities purchasing for rental purposes. These buyers face no occupancy restrictions and can use the property however they choose after purchase.

A common misconception is that HomePath properties are restricted to first-time buyers or those meeting income limits. In reality, the program does not impose income restrictions or require buyers to be first-time purchasers. The primary distinction is between owner-occupants who receive early access and other buyers who can participate after the First Look period.

See If the Fannie Mae HomePath Program Is Right for You

HomePath homes can open doors to the many benefits of homeownership at a more accessible price point. However, buyers must approach purchases with realistic expectations and adequate budgets for potential repairs.

Griffin Funding specializes in helping buyers secure financing for various property types, including bank-owned homes that may need renovations. Our experienced mortgage professionals can guide you through the financing options that best suit your situation. Plus, track your home-buying progress and stay organized with the Griffin Gold app.

Contact Griffin Funding today to explore your financing options or get started online right away and take the next step toward homeownership.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can you use a mortgage to buy a Fannie Mae HomePath home?

How do I know if a HomePath property is right for me?

How do I find Fannie Mae HomePath properties?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...