What Is a Subject-To Mortgage?

KEY TAKEAWAYS

- A subject-to mortgage lets buyers acquire property without paying off the seller’s existing loan, which remains in the seller’s name.

- The buyer takes ownership and makes mortgage payments, but the seller stays legally responsible for the debt.

- Due-on-sale clauses give lenders the right to demand full repayment, though enforcement varies by lender and market conditions.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformA subject-to mortgage allows buyers to purchase property while the seller’s existing loan remains in place. This creative financing strategy can help buyers access lower interest rates and avoid traditional loan qualification, though it carries unique risks for both parties.

What Is a Subject-To Mortgage?

A subject-to mortgage, often called “buying subject to the existing mortgage” or “sub to,” refers to a real estate transaction where the buyer takes ownership of a property while the seller’s original mortgage remains in place. The buyer agrees to make the monthly mortgage payments, but the loan stays in the seller’s name.

The phrase “subject to” means the property transfer happens subject to the existing loan terms. Ownership transfers through a deed, but the mortgage lien remains attached to the property. This means that the buyer essentially takes over mortgage payments from the seller without formally assuming the loan or going through the lender’s approval process.

How a Subject-To Mortgage Works

The subject-to real estate process involves several steps that transfer ownership while keeping the original financing intact:

- Seller has an existing mortgage: The property owner carries a mortgage with specific terms, interest rates, and remaining balance.

- Buyer and seller agree to a subject-to purchase: Both parties negotiate the purchase price. They draft a subject-to real estate contract that outlines payment responsibilities, deed transfer, and contingencies.

- Title transfers to buyer: The seller signs a deed transferring legal ownership to the buyer.

- Existing mortgage stays in seller’s name: The original loan remains unchanged. The lender receives payments as usual, but the buyer makes those payments instead of the seller.

Title companies play an important role in this process by conducting title searches, preparing documents, and recording the deed transfer. Many subject-to transactions also include escrow arrangements where the buyer sends payments to a third party who forwards them to the lender, creating a payment trail.

Insurance then transfers to the buyer’s name, though the mortgage company may require notification of ownership changes. Finding a real estate attorney experienced in subject-to transactions helps protect both parties throughout this process.

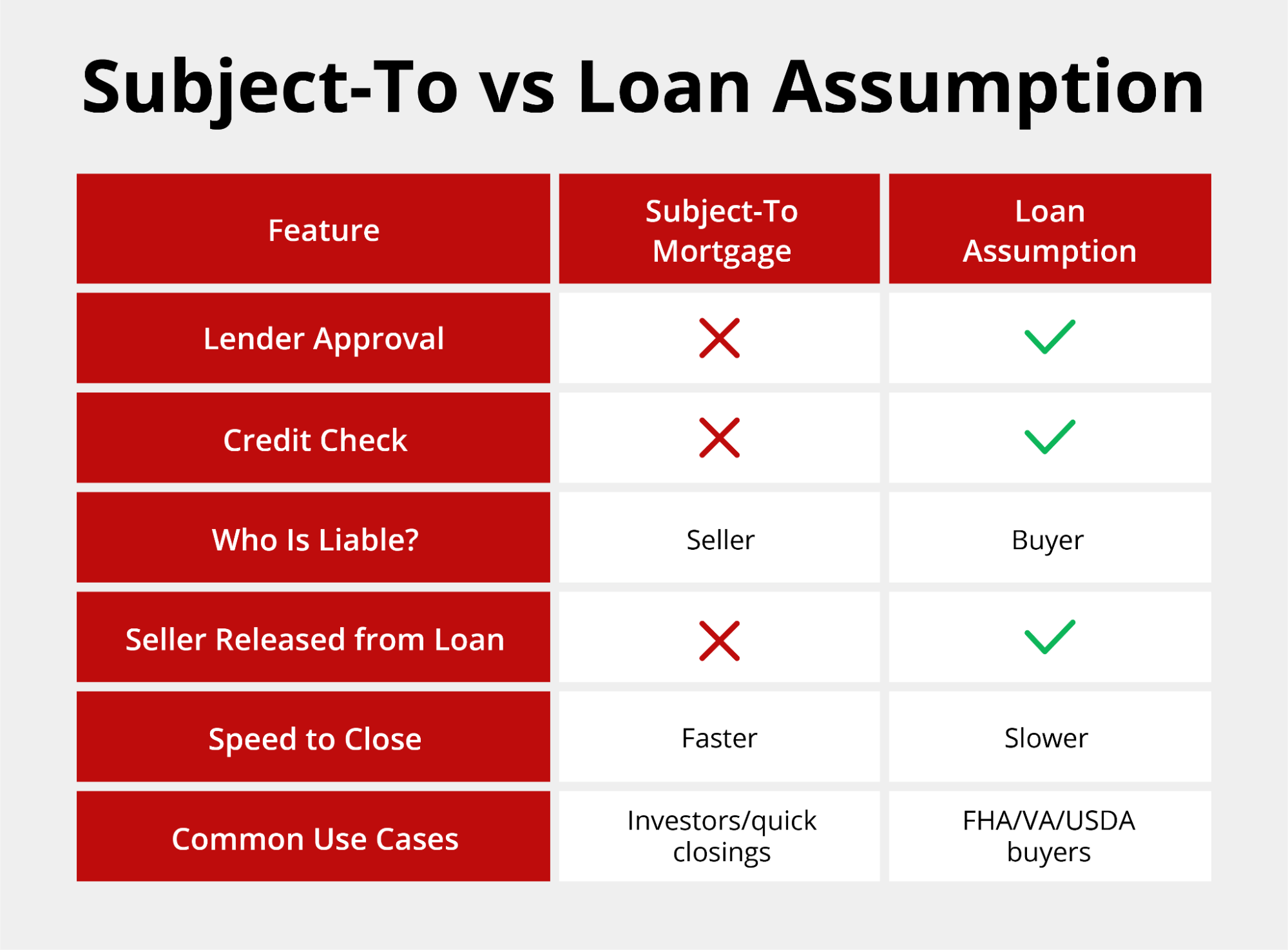

Subject-To Mortgage vs Loan Assumption

Subject-to mortgages and loan assumptions both involve taking over existing financing, but they differ in structure and legal implications.

Lender approval: Loan assumptions require formal lender approval. The buyer must qualify based on credit score, income, and debt-to-income ratio. Subject-to transactions happen without lender involvement or approval.

Lender approval: Loan assumptions require formal lender approval. The buyer must qualify based on credit score, income, and debt-to-income ratio. Subject-to transactions happen without lender involvement or approval.- Liability and credit responsibility: Assuming a mortgage transfers legal responsibility from seller to buyer. The seller’s name comes off the loan, releasing them from future liability. In subject-to deals, the seller remains legally liable for the debt.

- FHA loan assumable options: Some government-backed loans, particularly FHA and VA mortgages, offer streamlined assumption processes. These assumable mortgages provide middle-ground alternatives between subject-to arrangements and new financing.

Overall, assumptions work better for sellers seeking complete release from mortgage obligations. Subject-to arrangements suit situations requiring speed or where buyers cannot qualify for traditional financing.

Why Buyers Use Subject-To Existing Mortgages

Buyers pursue subject-to mortgages for several advantages that traditional financing cannot provide:

- Lower interest rates: Buyers can access existing low interest rates that may be better than current market rates.

- Avoiding new loan qualification: Buyers bypass strict lending standards, credit checks, and income verification requirements that might disqualify them from traditional mortgages or non-qualified mortgages.

- Lower closing costs: Subject-to transactions eliminate loan origination fees, appraisal costs, and other lender charges. Use a closing cost calculator to compare traditional financing expenses against subject-to arrangements.

- Faster transactions: Closing can happen in days rather than weeks since no loan underwriting is required.

Real estate investors frequently use subject-to strategies for buying investment properties, particularly when working with distressed sellers facing foreclosure. First-time home buyers occasionally consider this approach, though it carries more risk than conventional financing.

The strategy works best for finding motivated sellers who need quick solutions and have attractive existing loan terms. Buyers in markets with rising interest rates particularly benefit from preserving older, lower-rate mortgages.

Why Sellers Consider Subject-To Mortgages

Some situations where sellers may benefit from subject-to mortgages include:

- Avoiding foreclosure: Sellers behind on payments can transfer ownership to buyers who resume payments.

- Relocating quickly: Job transfers or family emergencies require immediate moves, and subject-to deals close faster than waiting for qualified buyers with new financing.

- Difficulty selling traditionally: Properties with limited equity, unfavorable locations, or condition issues may not attract conventional buyers willing to pay full market value.

Sellers should understand the risks before agreeing to subject-to terms. The mortgage remains on their credit report, affecting their debt-to-income ratio for future loans. They remain legally liable if buyers stop making payments, potentially facing foreclosure in their name. Lenders can also invoke due-on-sale clauses, demanding immediate full repayment.

Pros and Cons of a Subject-To Mortgage

Subject-to mortgages offer advantages and disadvantages that both buyers and sellers must carefully weigh.

Pros of a subject-to mortgage:

- Access to existing low interest rates: Buyers can benefit from the seller’s original loan terms, potentially securing rates several percentage points below current market rates.

- Minimal upfront financing: Lower closing costs and reduced down payment requirements make properties more accessible.

- Faster closings: Transactions complete quickly without lengthy underwriting processes, appraisals, or lender approval delays.

Cons of a subject-to mortgage:

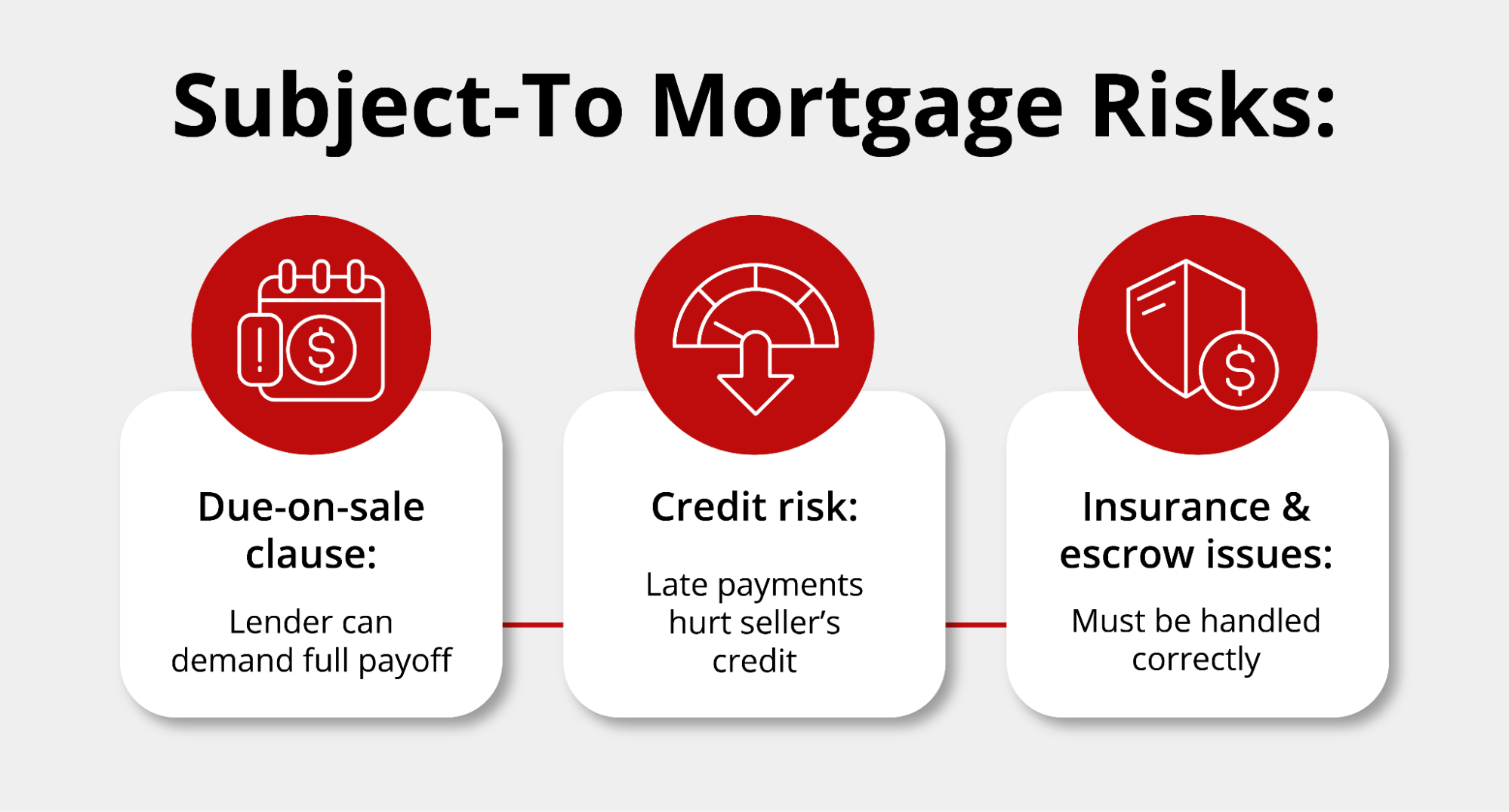

- Due-on-sale clause risk: Lenders maintain the right to call loans due immediately upon discovering ownership transfers.

- Seller remains liable for the loan: Original borrowers stay legally responsible for debt, face continued credit impact, and risk foreclosure if buyers default on payments.

- Limited lender protections: Neither party enjoys the legal safeguards that come with formal loan assumptions or new mortgages.

Legal and Financial Risks of Subject-To Mortgages

The due-on-sale clause, included in most mortgage contracts, gives lenders the right to demand full loan repayment if property ownership changes. This means that lenders can accelerate the loan, requiring immediate payment of the entire remaining balance once they discover the property transfer.

The due-on-sale clause, included in most mortgage contracts, gives lenders the right to demand full loan repayment if property ownership changes. This means that lenders can accelerate the loan, requiring immediate payment of the entire remaining balance once they discover the property transfer.

Enforcement of the due-on-sale clause varies by lender and market conditions. Large institutional lenders may monitor ownership changes through property records, insurance notifications, or escrow account updates. However, many lenders choose not to enforce these clauses as long as payments continue on time, particularly in markets where existing loan rates exceed current rates.

If a lender calls the loan due in a subject-to deal, the buyer must refinance or pay off the balance quickly. Insurance, taxes, and escrow missteps also create problems. Buyers and sellers should prioritize finding a real estate attorney experienced in subject-to transactions and use proper subject-to real estate contract templates to document responsibilities, payment methods, and contingency plans.

Who Should Consider a Subject-To Mortgage?

Ideal buyer profiles for subject-to mortgages include experienced real estate investors comfortable with creative financing risks. These buyers understand how to find motivated sellers for subject-to deals, can evaluate properties quickly, and maintain sufficient reserves to handle unexpected complications. Investors seeking multiple properties also benefit from subject-to financing’s speed and lower capital requirements compared to conventional loans.

Subject-to real estate arrangements may not fit buyers who need lender protections or low risk structures. Anyone evaluating home affordability through subject-to arrangements must account for both the immediate financial obligation and potential refinancing costs if lenders enforce due-on-sale clauses. Anyone comparing risks of buying a house with someone else’s mortgage should assess credit exposure, legal support, and exit strategies before moving forward.

Is a Subject-To Mortgage Right for You?

A subject-to mortgage can unlock opportunities that traditional financing cannot. Griffin Funding helps buyers evaluate every option, from creative structures to conventional solutions. Plus, the Griffin Gold app provides tools and guidance to track goals and explore financing paths.

Connect with an experienced Griffin Funding advisor today to unlock financing options that match your goals or get started online right away.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Is a subject-to mortgage legal?

What are alternatives to subject-to mortgages?

Does a subject-to mortgage affect credit?

What is the difference between a subject-to mortgage and a wraparound mortgage?

A wraparound mortgage (or "wrap") works differently. The seller acts as the lender and creates a new, larger loan that "wraps around" the existing mortgage. The buyer makes payments to the seller at a higher interest rate, and the seller continues paying the original mortgage. For example, if a property has a $200,000 existing mortgage and sells for $250,000, the wraparound note might be for $250,000 at a higher rate than the underlying loan. The seller profits from the interest rate spread while continuing to service the original debt.

The key differences:

- Payment structure: Subject-to buyers pay the lender directly; wraparound buyers pay the seller, who pays the lender

- Interest rates: Subject-to preserves the original rate; wraps typically charge buyers higher rates than the underlying mortgage

- Seller involvement: Subject-to sellers receive their equity upfront; wraparound sellers receive ongoing payments and earn interest income

- Complexity: Wraps require more documentation and create an additional layer of financing beyond the original loan

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...