HELOC Draw vs Repayment Period

KEY TAKEAWAYS

- The HELOC draw period offers maximum flexibility with interest-only payments, while the repayment period requires full principal in addition to interest payments.

- Payment shock is common when transitioning into the repayment phase, so early planning and budgeting are essential.

- Refinancing, converting to fixed-rate options, or paying down principal early can help manage or avoid higher future payments.

- Choosing the right lender, like Griffin Funding, can provide better guidance, tools, and HELOC strategies tailored to your needs.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformA home equity line of credit (HELOC) works differently from a standard loan because it has two distinct phases: the draw period and the repayment period.

Understanding how the draw period vs repayment period works with a HELOC helps homeowners know when they can borrow, when they must start paying back principal, and how their monthly payments will change. This breakdown is essential for budgeting, planning renovations, consolidating debt, or using equity strategically.

A home equity line of credit is a revolving credit line secured by your home that allows you to borrow money as needed, similar to using a credit card with a large limit. Unlike a home equity loan, which gives you a lump sum upfront with fixed payments, a HELOC provides ongoing access to your equity during the draw period.

HELOCs are popular because they offer flexibility in the form of interest-only payment options, variable borrowing amounts, and the ability to reuse paid-off credit. This flexibility makes them a great option when it comes to big projects, ongoing renovations, sudden emergencies, and long-term financial planning.

What Is the HELOC Draw Period?

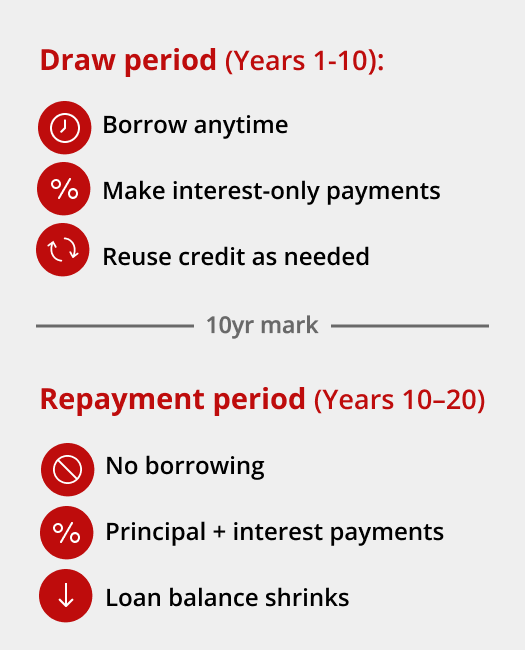

The draw period is the initial phase of a HELOC when you can borrow freely from your credit line.

Definition

The HELOC draw period is the timeframe, typically 5 to 10 years, during which you can access your available equity and borrow funds as needed. During this phase, your HELOC functions like a revolving credit line, allowing you to use, repay, and reuse funds multiple times.

How Payments Work During the Draw Period

- Payments are typically interest-only, meaning you’re not required to pay down the principal yet.

- You can borrow, repay, and borrow again, as long as you stay within your credit limit.

- Your available balance changes depending on how much of your credit you use. As you pay back principal, your borrowing power increases again.

- Because only interest is due, monthly payments tend to stay low and predictable during this phase.

- Interest rates are often variable and priced based on factors such as credit, CLTV, lien position, product type, and the index plus margin. Term options (including draw length) can influence pricing, but it varies by lender.

- Griffin Funding offers draw periods of 2, 3, 5, or 10 years.

Benefits of the HELOC Draw Period

- Maximum flexibility to use funds when needed: You can access your credit line at any time and use the funds however you’d like, making it one of the most adaptable home equity solutions available.

- Lower monthly payments during the draw phase: Because payments are often interest-only, your monthly obligations stay low, which helps with budgeting and cash flow.

- Ability to borrow, repay, and borrow again: A revolving line of credit gives you control over how much you use, making it great for long-term renovation projects or other dynamic situations.

- Useful for large or unpredictable expenses: Common use cases include home renovations, medical expenses, tuition, business cash flow needs, and unexpected repairs.

- Ideal for financial flexibility: The draw period lets you manage short-term cash needs without committing to fixed principal payments.

Drawbacks of the Draw Period

- Potential for payment shock once repayment starts: Switching from interest-only payments to full payments can significantly increase how much you pay each month.

- Higher risk of over-borrowing: Easy access to the funds can lead some borrowers to get carried away and take on more debt than they originally intended.

- Variable interest rates introduce unpredictability: Most HELOCs have adjustable rates, which can increase your payments during the draw period.

- No forced principal reduction: Because you’re not required to pay down principal, the full balance may remain when repayment begins.

What Is the HELOC Repayment Period?

The repayment period begins once the draw period ends and borrowers must start paying back the principal they used.

Definition

The HELOC repayment period is the phase when your outstanding balance must be fully repaid, typically lasting 10–20 years depending on the lender. During this stage, whether it’s a traditional HELOC or a first-lien HELOC (a HELOC in first position, meaning it replaces your existing first mortgage rather than sitting behind it), you can no longer access the credit line, and your loan transitions into full amortization.

How Payments Change During the Repayment Period

- Interest-only payments end, and you begin paying down the principal and interest each month.

- No new borrowing is allowed, even if you’ve paid down part of the balance.

- Monthly payments usually increase significantly because they now include both principal repayment and any remaining interest charges.

- HELOC rates are often variable, so your payment during repayment depends on your rate at that time (index + margin) and your remaining term, along with factors like credit and CLTV.

Benefits of the Repayment Period

- Principal reduction begins automatically: Each payment chips away at your balance, steadily lowering your debt.

- Predictable amortization schedule: Payments follow a set timeline, making it easier to plan long-term finances and eventual payoff.

- Helps prevent long-term overuse of credit: Once borrowing ends, you’re focused solely on repayment rather than continuously drawing more funds.

- More financial structure: Some homeowners appreciate the discipline of required principal payments after years of flexible borrowing.

Drawbacks of the Repayment Period

- Higher monthly payments: Payments can rise significantly when principal repayment begins, creating strain on your budget.

- Loss of borrowing flexibility: You cannot draw additional funds, even if you’ve paid down part of the balance.

- Possible difficulty adjusting to the new payment structure: Borrowers accustomed to interest-only payments may struggle with the new, higher costs.

- Less useful for ongoing financial needs: If you still need access to equity, you may have to refinance, take out a new HELOC, or explore alternative financing products.

HELOC Draw Period vs Repayment Period: Key Differences

Understanding the differences between the draw period and repayment period helps you anticipate how your payments, flexibility, and borrowing power will change over time.

- Payment structure: During the draw period, payments are typically interest-only. In the repayment period, payments switch to full principal and interest.

- Borrowing access: The draw period allows you to borrow, repay, and borrow again as needed. Once the repayment period begins, borrowing stops and the credit line is closed.

- Monthly payment size: Payments are usually much lower during the draw period. They can increase significantly in the repayment period because you begin paying down the principal.

- Flexibility: The draw phase offers maximum flexibility for projects, emergencies, or recurring expenses. The repayment phase is more rigid since all funds must be paid back according to a set schedule.

- Financial planning considerations: The draw period is easier on short-term budgets but can lead to payment shock later. The repayment period provides a clear timeline for payoff but requires stronger budgeting due to higher payments.

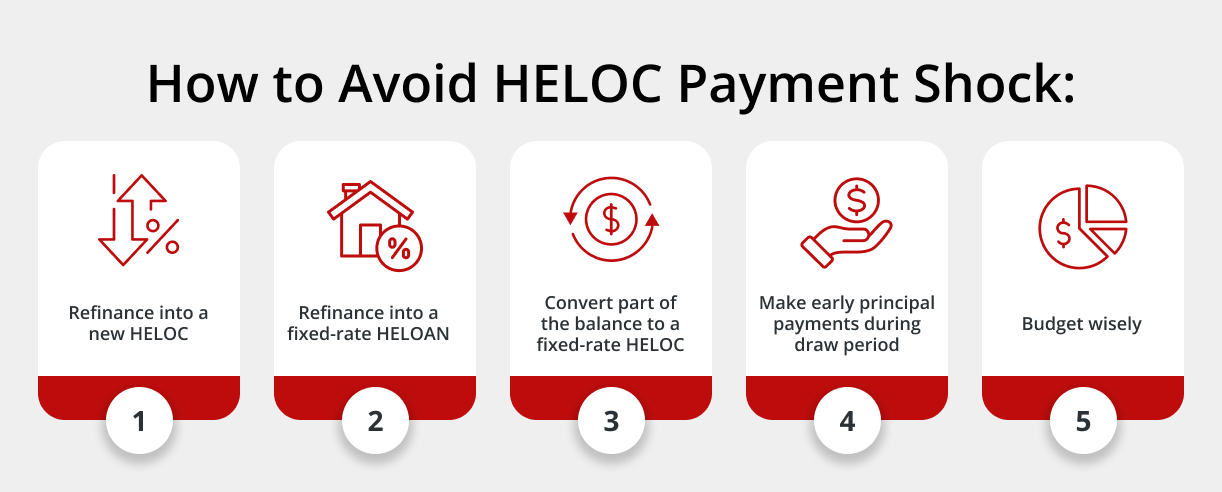

Strategies to Manage or Avoid HELOC Payment Shock

Consider these strategies to avoid getting overwhelmed once your HELOC repayment period starts:

- Refinance into a new HELOC

If your HELOC draw period is ending, refinancing into a new HELOC can restart the draw phase, restore borrowing flexibility, and delay full payments. This option may also secure better terms if your credit or home value has improved. - Refinance into a fixed-rate home equity loan

Converting your variable-rate HELOC into a fixed-rate home equity loan provides predictable monthly payments and protection from rising interest rates. Review home equity loan limits to see how much you may be able to borrow with a new HELOAN or refinanced HELOC. - Convert part of the balance to a fixed-rate option (if your lender allows it)

Griffin Funding offers a fixed-rate HELOC feature that lets you lock in your rate, allowing for more predictability in terms of monthly payments. - Pay down principal early during the draw period

Even small voluntary principal payments can dramatically lower your future monthly payments. Reducing your balance before the repayment period begins is one of the most effective ways to avoid payment shock. - Budgeting and cash-flow planning

Start estimating your future HELOC repayment-period payments early so you can prepare for the transition. Adjust your budget, reduce discretionary spending, and build a savings buffer to ease the shift from interest-only to principal and interest payments.

Payment shock example: If you drew $80,000 at 8% APR, an interest-only payment is about $533/month. If that balance converts to a 15-year repayment schedule, the payment can increase significantly (your actual payment depends on your rate, term, and balance).

Choose the Right HELOC Strategy for Your Needs

Selecting the best HELOC approach depends on your financial goals, repayment timeline, and how you plan to use your home’s equity. Understanding how the HELOC draw period vs repayment period works is key to avoiding financial hazards when using this type of loan product.

Griffin Funding offers a range of HELOC and home equity solutions designed to help homeowners manage borrowing and repayment with confidence. With personalized guidance and tools like the Griffin Gold app, you can track your loan, manage documents, and stay fully informed every step of the way, making it easier to choose the HELOC strategy that truly fits your needs.

Reach out to learn more or get started online today.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

Can you pay off a HELOC during the draw period?

How long is the HELOC draw period vs the repayment period?

Can I extend or refinance my HELOC repayment period?

What happens when a HELOC draw period ends?

Can I pay principal during the draw period, and will it reduce payment shock?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...