Griffin Funding vs United Wholesale Mortgage (UWM): Mortgage Lender Comparison

KEY TAKEAWAYS

- Griffin Funding excels with VA, self-employed, and investor-focused programs, offering flexible documentation and a direct-to-consumer experience.

- UWM provides highly competitive rates on traditional mortgages through its broker-driven wholesale model, making it ideal for W-2 borrowers with strong credit.

- Your income type, property goals, and need for flexibility are the biggest factors in choosing between the two lenders.

- Borrowers wanting hands-on guidance and non-traditional options may prefer Griffin Funding, while those prioritizing the lowest conventional rates often benefit from working with a broker who can access UWM.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage PlatformChoosing the right mortgage lender can depend heavily on your income type, loan needs, and whether you prefer working directly with a lender or through a broker.

Griffin Funding and United Wholesale Mortgage (UWM) serve very different borrower profiles — one focuses on specialized loan programs for individuals, while the other operates as the nation’s largest wholesale lender supporting independent mortgage brokers.

This comparison breaks down how each company works so you can decide which model fits your situation best.

Company Overview: Griffin Funding vs United Wholesale Mortgage (UWM)

Let’s look at each company in turn: who they are, whom they serve, and how they operate, so you can see how they stack up.

Griffin Funding Overview

Griffin Funding Overview

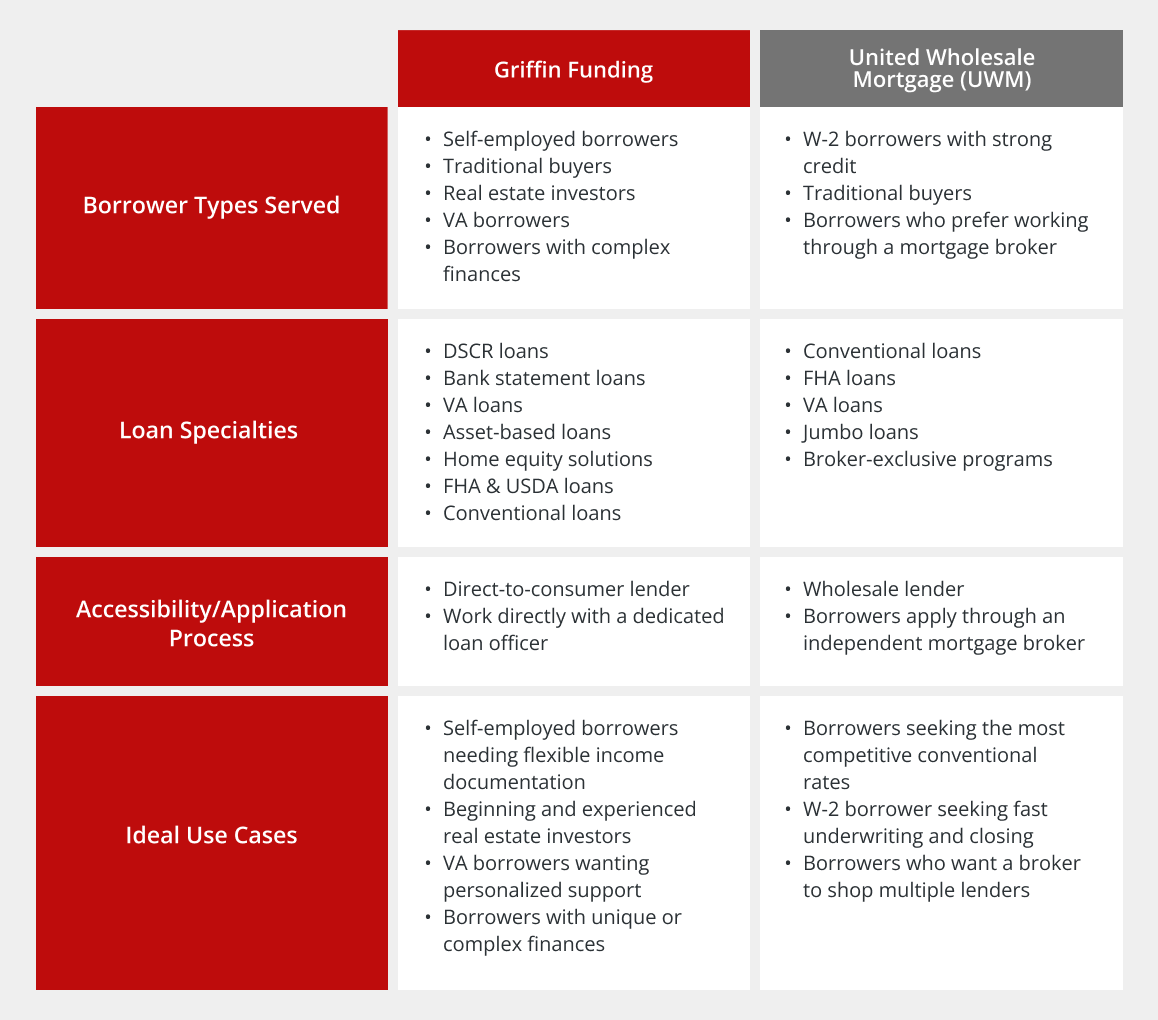

Griffin Funding is a direct-to-consumer mortgage lender known for specializing in VA loans, DSCR loans for real estate investors, and alternative-income loan programs such as bank-statement loans for self-employed borrowers. They primarily serve veterans, active-duty service members, real estate investors, and individuals who may not qualify through traditional W-2–based underwriting.

Operating across most of the United States, Griffin Funding offers mortgage products in 47 states and Washington, D.C., giving them near-nationwide reach. The company’s strengths lie in its flexible underwriting guidelines, niche loan program expertise, and high-touch customer service approach aimed at making non-traditional borrowers feel supported throughout the lending process.

United Wholesale Mortgage Overview

United Wholesale Mortgage is the largest wholesale mortgage lender in the country and operates exclusively through independent mortgage brokers rather than working directly with consumers.

Founded in 1986 and headquartered in Michigan, UWM has become a dominant force in the mortgage industry through its broker-centric model and large-scale loan production. The company’s market position is built on fast turn times, competitive pricing, and technology tools designed to help brokers streamline applications and close loans efficiently.

Key differentiators include its investment in proprietary technology, strong broker partnerships, and an operational structure that supports brokers instead of maintaining retail branches, making UWM a powerful backend lending engine for borrowers who prefer securing loans through a mortgage broker.

Loan Products Offered

Griffin Funding Loan Programs

Griffin Funding provides a mix of traditional loans and non-traditional mortgage products, with a strong emphasis on options for self-employed borrowers and real estate investors.

Key loan programs include:

-

- Designed for veterans, active-duty service members, and eligible spouses

- 100% financing in many cases, flexible credit guidelines, no mortgage insurance

-

- Created for real estate investors

- Approval based on the property’s cash flow rather than personal income

- Ideal for borrowers with multiple properties or complex financials

-

- Tailored for self-employed borrowers who don’t qualify using W-2s

- Income verified using 12–24 months of bank statements

- Helpful for those with high cash flow but irregular taxable income

-

- Standard conforming mortgage options

- Fixed-rate and adjustable-rate products

-

- Low down payment options (as low as 3.5%)

- More flexible credit requirements

-

- Qualification based on liquid assets rather than income

- Useful for retirees, high-net-worth individuals, or borrowers with significant savings

-

- Equity-based financing solutions for borrowers seeking cash-out

- Useful for investors and homeowners tapping equity for additional purchases

Griffin Funding stands out for offering multiple alternative-income programs, making them a strong fit for self-employed borrowers, gig workers, and investors who often struggle with strict documentation requirements at traditional banks.

UWM Loan Programs

UWM focuses heavily on a wide range of traditional mortgages, offered exclusively through its network of independent mortgage brokers. Major loan programs offered through brokers include:

- Conventional Loans

- Conforming mortgages backed by Fannie Mae/Freddie Mac

- Competitive rates due to UWM’s large-scale wholesale pricing

- FHA Loans

- Low down payments and flexible credit options

- Popular for first-time homebuyers

- VA Loans

- Zero-down options for qualified veterans and military borrowers

- Brokers often leverage UWM’s fast underwriting for quicker closings

- Jumbo Loans

- High-balance financing for luxury or high-cost-area properties

- Often paired with UWM’s speed-focused underwriting

- Broker-Exclusive Specialty Products

- Programs only available through UWM’s approved broker network

- Examples may include competitive temporary buydowns, niche refinance options, or broker-specific pricing incentives

How the broker-driven structure shapes borrower options:

- UWM does not lend directly to consumers—borrowers must work with a mortgage broker.

- Brokers can shop multiple lenders, but UWM is often the backend lender chosen for its fast turn times, competitive rates, and strong technology platform.

- This structure may offer borrowers more options, since brokers compare products across multiple wholesale lenders, not just UWM alone.

Customer Experience & Support

Griffin Funding Customer Experience

What borrowers typically experience:

- Personalized service model

- One-on-one communication with a dedicated loan officer

- Direct-to-consumer setup means fewer intermediaries

- Fast pre-approvals and underwriting

- Streamlined workflows for VA, DSCR, and bank-statement loans

- Quick documentation reviews, especially for alternative-income products

- Strong borrower feedback

- Many Griffin Funding reviews highlight transparency, responsiveness, and clear explanations of non-traditional loan options

- Borrowers often cite non-QM loan testimonials referencing smoother experiences compared to big banks

- Support for non-traditional borrowers

- Specialized assistance for self-employed clients and real estate investors

- Guidance through complex or alternative documentation scenarios

UWM Reviews

Because UWM works exclusively through mortgage brokers, its customer experience is shaped by the broker–lender partnership.

Key trends in United Wholesale Mortgage reviews:

- Positive trust signals

- Fast underwriting and closing times

- Competitive pricing that brokers can pass on to borrowers

- Common borrower praise

- Speed, efficiency, and smooth backend processing

- Brokers note that UWM’s communication systems make status updates easy

- Common complaints

- Borrowers sometimes unclear about UWM’s role because they interact mainly with the broker

- Any issues often stem from the broker–borrower communication gap

- Impact of the broker-driven model

- Brokers handle all borrower communication, so experiences can vary widely

- When paired with a strong broker, UWM is often reviewed as one of the fastest and easiest wholesale lenders to work with

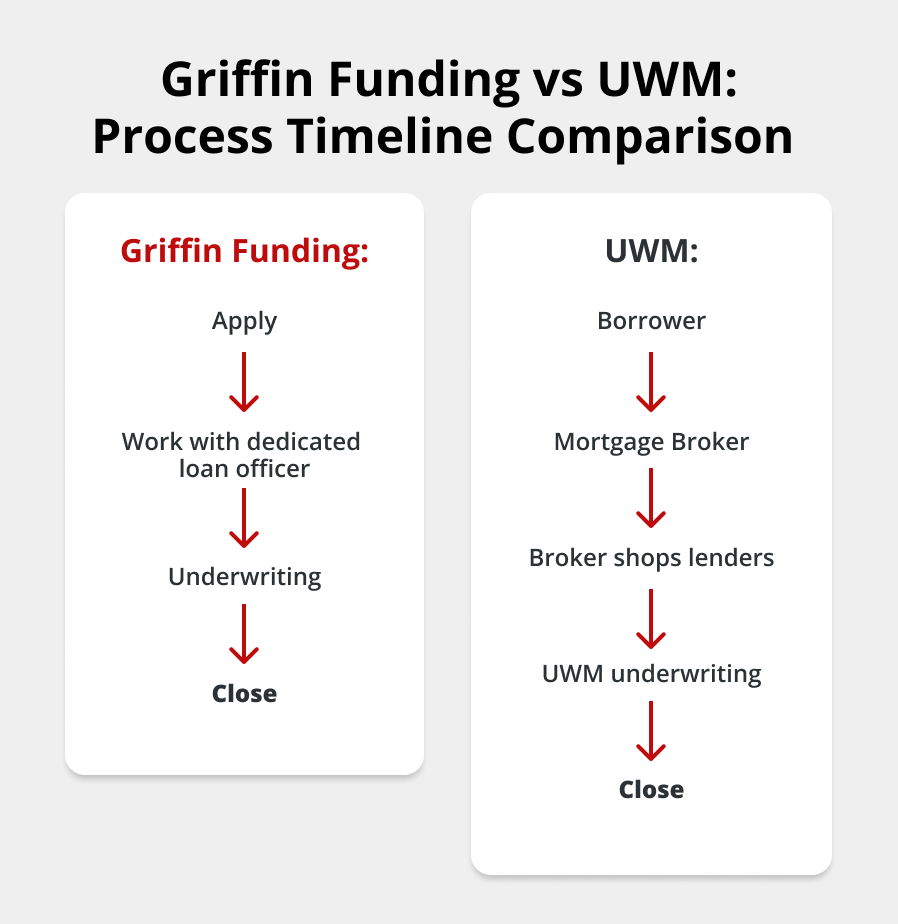

Technology, Speed, & Approval Process

Griffin Funding Technology & Turn Times

- Digital mortgage platform

- Online application portal, document upload tools, and mobile-friendly borrower dashboard

- Fast underwriting timelines

- Particularly efficient for VA and non-QM loans

- Processes bank statements, assets, and investor documentation quickly

- AI-driven underwriting

- Griffin Funding recently incorporated an AI-driven underwriting platform to speed up credit evaluation, risk assessment, and document review

- Overall speed

- Pre-approvals delivered quickly

- Many alternative-income loans close faster than at traditional retail banks due to flexible guidelines

UWM Technology & Turn Times

- Ultra-fast broker-supported closings

- Many loans clear underwriting in days, not weeks

- Brokers leverage UWM’s tech tools (like its proprietary processing system) to keep files moving quickly

- Streamlined systems

- Automated disclosures, fast appraisal ordering, and real-time loan status

Pros & Cons: Griffin Funding vs UWM

Griffin Funding Pros & Cons

Pros:

- Strong programs for VA borrowers: Competitive VA loan expertise and streamlined processing.

- Excellent for self-employed borrowers: Bank-statement, asset-based, and other alternative mortgage loans are available, as well as flexible documentation options.

- Investor-friendly offerings: DSCR loans, cash-flow underwriting, and equity-based financing.

- Direct-to-consumer service model: Personalized attention, dedicated loan officers, and hands-on guidance.

- Fast turn times on non-traditional loans: Helpful for borrowers shut out from traditional banks.

Cons:

- Not ideal for borrowers seeking the lowest conventional rates: Wholesale lenders and big banks may price conventional loans more aggressively.

- Non-QM loans can carry higher rates/fees: Tradeoff for flexibility and unique underwriting programs.

- Less appealing for “simple file” borrowers: W-2 borrowers with strong credit may find cheaper options elsewhere.

UWM Pros & Cons

Pros:

- Wholesale pricing advantage: Brokers access competitive rates that often beat retail banks.

- Extremely fast underwriting and closings: Popular among brokers for quick turn times.

- Wide range of traditional products: Strong options for conventional, FHA, and VA borrowers.

- Technology-driven efficiency: Broker tools, automatic disclosures, and streamlined processing.

- Broker shopping power: Borrowers can compare UWM against other wholesale lenders through their broker.

Cons:

- Broker-only access: Borrowers cannot apply directly. Instead, they must work through a mortgage broker.

- Experience varies by broker quality: Communication, clarity, and support depend on the broker, not UWM.

- Focus on traditional mortgages: Limited availability of alternative-income or non-QM programs.

- Borrowers may feel disconnected: Some borrowers don’t realize UWM is the actual lender behind the scenes.

Broker Pricing: UWM’s Margin, Broker’s Compensation, & How It Affects Your Rate

Because UWM is a wholesale lender, you can’t go to UWM directly; you must work through a mortgage broker. That broker is your primary point of contact, but UWM is still the lender funding the mortgage behind the scenes.

Here’s why that matters for pricing:

- UWM’s total gain margin (company metric): In Q4 2025 reporting, UWM disclosed a total gain margin of 122 bps (1.22%) for the quarter, down from 130 bps in Q3 2025. For the full year 2025, UWM’s gain margin was 116 bps (1.16%). This is an operational metric that reflects company economics across production — not a guaranteed “fee” on any single borrower’s loan.

- Broker compensation (a separate layer): With a wholesale lender, the broker is compensated separately — typically either borrower-paid OR lender-paid (structure varies by transaction and broker model, and it can’t be both). For QM loans, Regulation Z points-and-fees limits apply (often described as ~3% for larger loans, but the limits are tiered by loan size). Many wholesale lenders also set lender-paid broker compensation limits (often around ~2.75%) to help stay within points-and-fees constraints once other origination charges are included.

- The combined effect (what borrowers should compare): When a loan is brokered to UWM, the “all-in” cost you feel can show up as a higher rate, higher closing costs, or both, depending on how pricing and compensation are structured. The best way to compare Griffin Funding vs. a broker/UWM option is to review the full Loan Estimate side-by-side (rate, points, lender fees, broker fees/comp, and total cash to close). Illustrative example (not your exact loan): If a wholesale lender’s company-level gain margin is 1.22% for a period, and a broker’s lender-paid comp is 2.75% on a given transaction, the combined economics in that simplified example total 3.97%. That total doesn’t automatically appear as one line-item fee — but it can show up through the rate, points, and/or closing costs, which is why the Loan Estimate comparison matters.

By contrast, Griffin Funding is a consumer direct lender, meaning you work with the lender’s team directly from application to closing. That typically reduces layering, increases transparency, and gives you a direct line to the people making underwriting and pricing decisions—especially helpful for VA borrowers, self-employed borrowers, and investors.

How to Choose Between Griffin Funding and UWM

When deciding between Griffin Funding and UWM, the best choice depends on your income type, loan goals, and how much guidance you want during the process.

Choose Griffin Funding if:

- You’re self-employed and need bank-statement, asset-based, or alternative-income options

- You’re an investor using DSCR loans or purchasing multiple properties

- You’re a VA borrower who wants personalized guidance and fast pre-approvals

- You prefer working directly with a lender (dedicated loan officer, fewer intermediaries)

- Your financial situation is complex, and you need flexibility that large retail or wholesale lenders may not offer

Choose UWM (through a mortgage broker) if:

- You have strong credit and standard W-2 income

- You want access to multiple lenders’ options, not just one

- Your priority is speed, especially if your broker leverages UWM’s rapid underwriting and closing

Wrapping Up

Choosing between Griffin Funding and UWM ultimately comes down to your borrower profile and the type of support you prefer during the mortgage process. If you’re self-employed, an investor, or someone who needs flexible documentation and personalized guidance, Griffin Funding offers a direct-to-consumer experience that’s hard to beat.

Griffin Funding’s specialty loan programs, fast underwriting, and dedicated service make them an excellent option for borrowers who don’t fit the traditional mold. Plus, with tools like the Griffin Gold app, you can track your loan, manage documents, and stay connected throughout the entire process.

Get started online and find the right mortgage for your unique situation.

Find the best loan for you. Reach out today!

Get StartedFrequently Asked Questions

How do UWM rates compare to Griffin Funding rates?

Do borrowers pay more when using a broker (UWM) instead of a direct lender (Griffin Funding)?

If UWM is the lender, why doesn’t the broker “control” the loan?

What’s the main difference between Griffin Funding and UWM?

Who is Griffin Funding best for?

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 24 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...