A Guide to Budgeting for First-Time Home Buyers

KEY TAKEAWAYS

- Budgeting is essential for a successful first-time home purchase and can help you avoid mistakes that many new buyers make.

- Beyond the down payment, factor in closing costs, inspections, moving expenses, and ongoing costs like property taxes, insurance, HOA fees, and maintenance that can add up quickly.

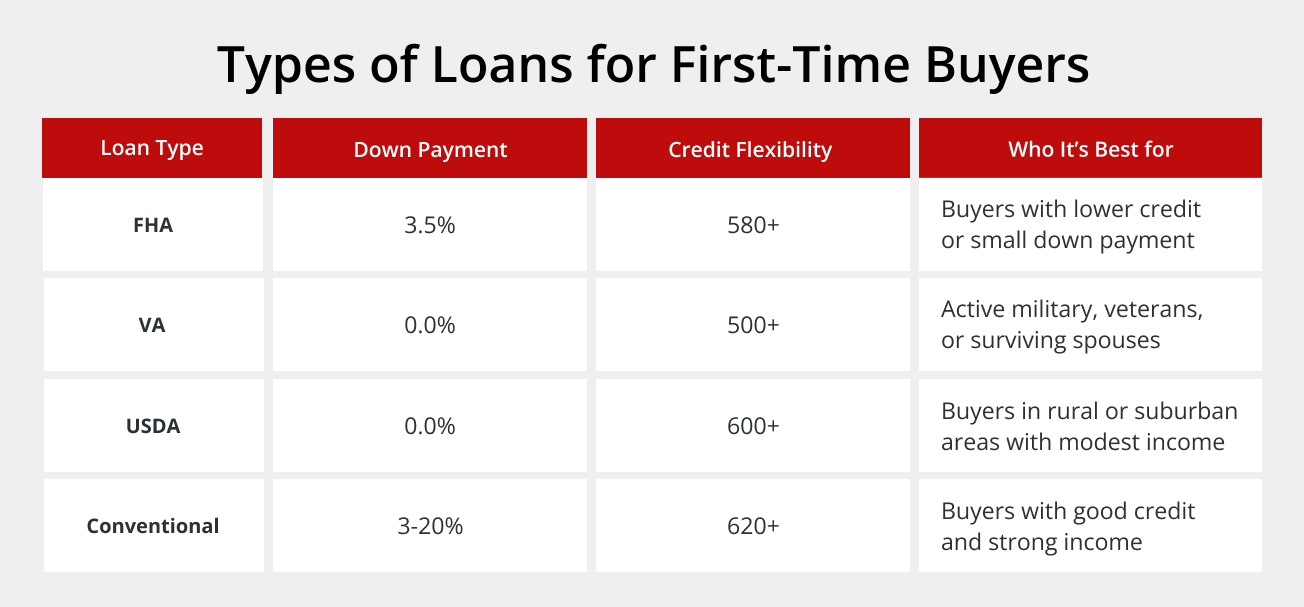

- Take advantage of first-time buyer programs and government-backed loans like FHA, VA, or USDA loans that come with lower down payment requirements and more flexible qualification standards.

- Stick to a monthly housing payment that’s no more than 28% of your gross income to maintain financial stability and leave room for other goals.

Outstanding Client Experience

Outstanding Client Experience Specialized Lending Solutions

Specialized Lending Solutions Direct-to-Consumer Advantage

Direct-to-Consumer Advantage We're Advisors, NOT Salespeople

We're Advisors, NOT Salespeople Effortless Digital Mortgage Platform

Effortless Digital Mortgage Platform

Buying your first house is exciting, but it can also feel overwhelming when you start looking at all the costs involved. The good news is that with proper planning and a solid budget for first-time home buyers, you can navigate the entire process confidently and avoid costly surprises along the way.

This guide will break down everything you need to know about budgeting for your first home purchase.

Why Budgeting Is Crucial for First-Time Home Buyers

The home buying process involves way more than just the purchase price you see listed online. There are upfront costs, ongoing monthly expenses, and unexpected repairs that can catch new homeowners off guard. Without a clear budget for first-time home buyers, you might find yourself house-poor or unable to qualify for the mortgage you need.

Proper budgeting helps you in several ways. It shows lenders that you’re financially responsible and ready for homeownership. Mortgage lenders like Griffin Funding look at your debt-to-income ratio, savings history, and overall financial picture when deciding whether to approve your loan. Budgeting also ensures you can actually afford the home you want to buy, not just the monthly payment. You’ll need to have money set aside for maintenance, emergencies, and other life expenses.

Ultimately, you never want to overextend yourself when buying a house, and having a budget can help you avoid financial strain.

When you understand your true financial capacity, you can shop for homes confidently and make offers knowing you’re within your means. This preparation also speeds up the buying process since you’ll already have your finances organized and ready for lender review.

How Much to Save for a House: First-Time Buyer Guidelines

The amount you need to save depends on several factors, but here’s a breakdown of the typical upfront costs you’ll face when buying your first house:

- Down payment: Your down payment is usually the largest upfront expense. Conventional loans require at least 3% down, though putting more down can help you save money by avoiding private mortgage insurance (PMI). An FHA loan requires just 2.5% down, while a VA loan for military members requires no down payment at all.

- Closing costs: Closing costs usually range from 2% to 6% of the home’s purchase price. These cover loan origination fees, title insurance, and prepaid items like property taxes and insurance.

- Inspection and appraisal: Inspection and appraisal are essential steps that protect you from buying a home with serious problems or paying more than it’s worth. Both services come with separate fees you’ll pay out of pocket.

As a general rule, a budget for first home buyers should include saving at least 5% to 10% of the home’s purchase price for all upfront costs combined. So, if you’re looking at homes around $250,000, plan to have $12,500-$25,000 saved up. If you can save closer to 15-20%, you’ll have even more options and better loan terms.

What Is a Good Budget for a First House?

Financial experts recommend following the 28/36 rule when determining your budget. This means your total monthly housing costs (including mortgage, taxes, and insurance) shouldn’t exceed 28% of your gross monthly income. Your total debt payments, including housing, shouldn’t exceed 36% of your gross income.

Let’s say you earn $5,000 per month before taxes. Using the 28% rule, you could afford up to $1,400 in monthly housing costs. If you’re already paying $300 monthly for other debts, your total debt payments would be $1,700, which is 34% of your income and within the 36% limit.

These ratios help ensure you have enough money left over for other important expenses like food, transportation, healthcare, and savings. However, some loan programs are more flexible. An FHA loan might allow higher debt-to-income ratios, especially if you have strong credit or significant savings.

Getting pre-approved for a mortgage is crucial because it shows you exactly how much lenders are willing to let you borrow based on your income, debts, and credit score. The pre-approval amount is your maximum borrowing limit, so you can use it to determine your realistic price range and shop for homes with confidence.

Common Costs First-Time Buyers Overlook

Many first-time buyers focus so much on the down payment and the monthly mortgage that they forget about other significant costs. Here are the expenses that can catch new homeowners off guard:

- Property taxes and insurance: Property taxes can add significantly to your monthly payment, and they tend to increase over time. Homeowners insurance is also required by most lenders to protect your investment.

- HOA fees: If you’re buying a condo or home in a planned community, homeowner association (HOA) fees will add to your monthly costs. These fees cover landscaping, community amenities, and exterior maintenance, but they’re an ongoing expense that doesn’t build equity.

- Maintenance and repairs: Once you own the home, you are responsible for all maintenance and repairs. You should make an annual budget for upkeep to cover everything from HVAC servicing to roof repairs and appliance replacements.

- Moving and setup costs: Moving expenses can add up quickly depending on distance and the amount of belongings you have. You might also need to buy new furniture, appliances, or home improvement items right after moving in. Setting aside money for these immediate post-purchase expenses will help you settle in without financial stress.

Building a Realistic First-Time Home Buyer Budget

Creating a comprehensive plan starts with understanding your current finances and setting goals for your home purchase. Here are the essential steps to build a budget that works:

- List your income and expenses: Document all your monthly income sources and subtract your existing debts and expenses to see how much money you have available for housing costs and savings.

- Determine your timeline: If you want to buy within the next year, you’ll need to save aggressively. If you have a few years, you can build your savings more gradually.

- Set realistic savings goals: Use a home affordability calculator to get a realistic picture of what you can afford based on your earnings, debts, and expected down payment.

- Use organizational tools: Consider using budgeting apps or spreadsheets to track your progress. Set up automatic transfers to a dedicated house fund so you can consistently build your savings. The Griffin Gold app can help you manage your finances and track your home buying progress.

- Find ways to boost savings: Look for ways to increase your savings by cutting discretionary spending or picking up extra income through side jobs or overtime. Having all your financial information in one place makes it easier to stay on top of your budget and see how close you are to your savings goals.

Loan Programs and Assistance for First-Time Buyers

Several government-backed programs are designed to help first-time home buyers overcome common barriers like large down payment requirements or strict credit standards. These include:

- Government-backed loan options: FHA loans are popular because they allow down payments as low as 3.5%. Meanwhile, VA loans are available to qualifying military first-time buyers with no down payment and no private mortgage insurance required. USDA loans help buyers purchase homes in rural and suburban areas.

- Additional assistance programs: Beyond federal programs, many states offer down payment assistance grants or low-interest programs for first-time buyers. Some programs provide several thousand dollars toward your down payment or closing costs, while others offer favorable loan terms or tax credits.

Griffin Funding has experience with these loan types and can help you determine which programs you qualify for. Working with knowledgeable lenders who understand first-time buyer programs can save you money and simplify the process.

Mistakes to Avoid When Budgeting for Your First Home

First-time buyers can make costly mistakes that impact their financial stability for years to come. Being aware of these pitfalls can help you make smarter decisions throughout the home buying process.

- Underestimating total costs: One of the biggest mistakes new buyers make is focusing only on the monthly mortgage payment while forgetting about property taxes, insurance, maintenance, and utilities. This can lead to financial strain once they move in and realize their actual monthly housing costs are much higher than expected. Just because a lender approves you for a certain amount doesn’t mean you should borrow it all.

- Ignoring long-term financial goals: Don’t let homeownership consume your entire financial capacity. You still need to contribute to retirement accounts, maintain an emergency fund, and save for other goals. A house shouldn’t prevent you from building wealth in other areas or preparing for unexpected life changes.

- Not shopping around for mortgage terms: Many first-time buyers make the mistake of not comparing rates and terms from multiple lenders. Even a small difference in interest rates can save or cost you thousands of dollars over the life of the loan. Get quotes from at least three lenders and compare not just rates but also fees and closing costs.

- Skipping important steps: Don’t skip important steps like home inspections to save money upfront. Check out this comprehensive first-time home buyer checklist to make sure you don’t miss any crucial steps in the process.

Find the Right First-Time Home Buyer Loan

Budgeting for your first home doesn’t have to be overwhelming when you have the right guidance and loan programs working in your favor. Griffin Funding has the expertise to help you find the perfect home loan for your financial situation.

Ready to start your home buying journey? Contact Griffin Funding today to explore your loan options and get the financing process underway.

Find the best loan for you. Reach out today!

Get Started

Bill Lyons is the Founder, CEO & President of Griffin Funding. Founded in 2013, Griffin Funding is a national boutique mortgage lender focusing on delivering 5-star service to its clients. Mr. Lyons has 25 years of experience in the mortgage business. Lyons is seen as an industry leader and expert in real estate finance. Lyons has been featured in Forbes, Inc., Wall Street Journal, HousingWire, and more. As a member of the Mortgage Bankers Association, Lyons is able to keep up with important changes in the industry to deliver the most value to Griffin's clients. Under Lyons' leadership, Griffin Funding has made the Inc. 5000 fastest-growing companies list five times in its 12 years in business.

Recent Posts

LLC for Rental Property Purchase: Pros & Cons

What Is an LLC for Rental Property? A limited liability company (LLC) is a type of business structure that giv...

How to Get the Lowest Mortgage Rate: 7 Strategies

How Mortgage Rates Are Set Before we teach you how to get the lowest mortgage rate, it helps to understand wha...

What Is an Escalation Clause in Real Estate?

A real estate escalation clause is an addendum to a purchase offer that authorizes your bid to increase automa...